.jpg)

.jpg)

.jpg)

Best Home Loan Paths for First-Time Home Buyers

Buying your first home is exciting, but choosing the right mortgage can feel like learning a new language. Conventional, FHA, VA, USDA, grants, credits, mortgage insurance, cash to close, debt-to-income ratio, it is a lot to sort through when you are also thinking about neighborhoods, inspections, and moving boxes.

The good news is that the best home loan for first-time home buyers is not about finding one universal winner. It is about finding the path that matches your cash savings, credit profile, income, location, military service history if applicable, and comfort with monthly payments.

A strong mortgage plan starts with a simple question: What problem does your loan need to solve? Some buyers need the lowest possible down payment. Others need more flexible credit guidelines, help with closing costs, a lower monthly payment, or a program designed for veterans or rural home purchases. Once you know your main constraint, the right loan path becomes much easier to identify.

Start With the Three Numbers That Shape Your Loan Path

Before comparing loan programs, get clear on the numbers that will guide every decision.

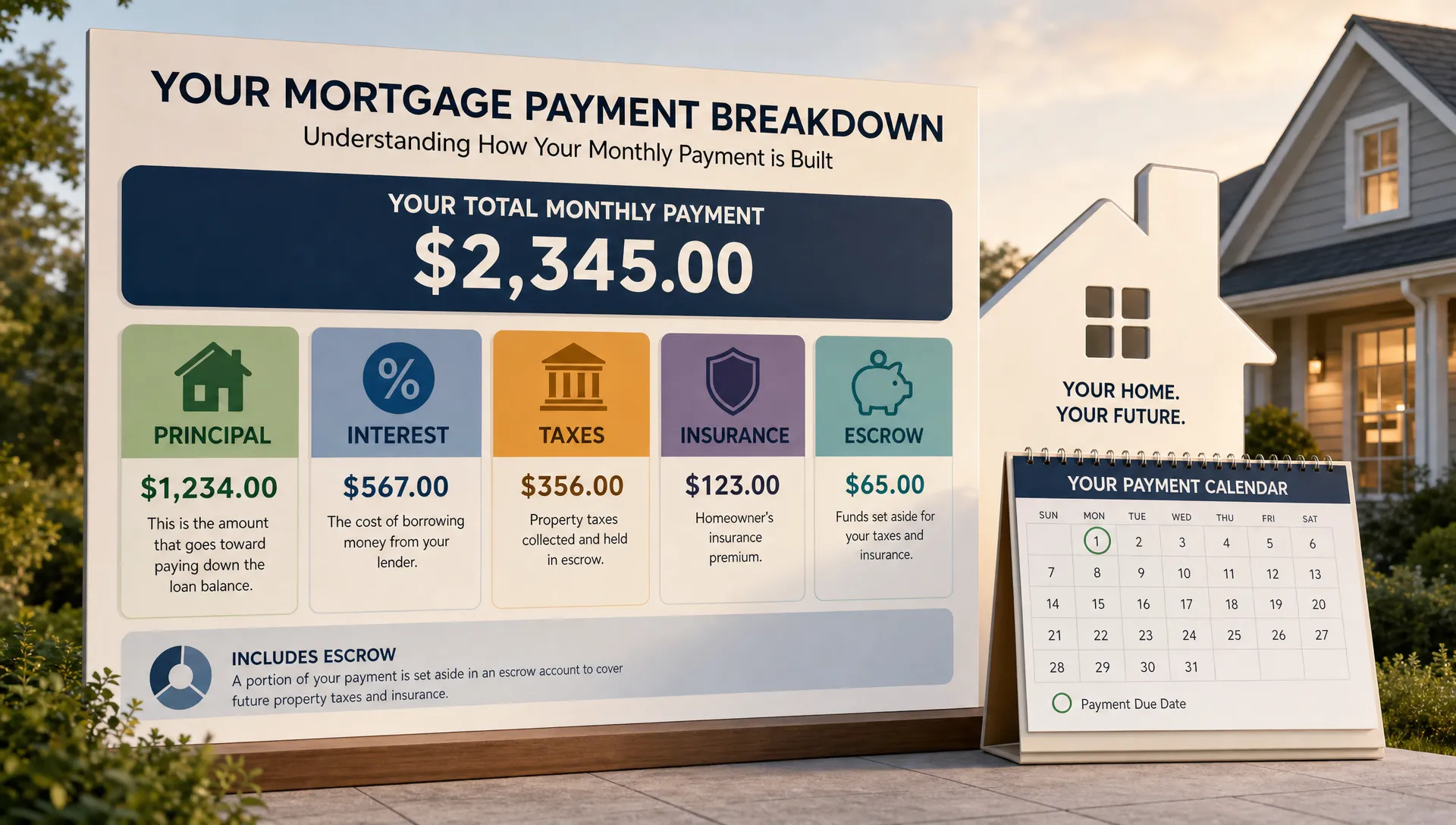

First, estimate your cash to close. This is more than your down payment. It can include closing costs, prepaid property taxes, homeowners insurance, initial escrow deposits, and other fees. Many first-time buyers focus only on the down payment and are surprised later by the full amount needed at closing.

Second, focus on your monthly payment, not just the home price. A mortgage payment may include principal, interest, property taxes, homeowners insurance, mortgage insurance, and possibly HOA dues. Two homes with the same price can have very different payments if property taxes, insurance, or HOA fees differ.

Third, understand your approval profile. Lenders generally review credit, income, employment history, debts, assets, and the property itself. If you are new to the process, New Era Lending’s overview of home loan basics every buyer should know can help you understand the core terms before you compare specific programs.

With those numbers in mind, here are the main home loan paths first-time buyers should consider.

Path 1: Conventional Loans for Buyers With Stronger Credit

A conventional loan is one of the most common mortgage options for first-time home buyers. It is not insured by a government agency, and it is often a strong fit for buyers with solid credit, stable income, and manageable debt.

Many first-time buyers assume conventional loans require 20% down. That is not always true. Some conventional programs allow eligible buyers to put down as little as 3%. The 20% figure matters because putting at least 20% down can help you avoid private mortgage insurance, often called PMI, but it is not always required to buy.

A conventional loan may be a strong path if you:

- Have good credit and want competitive pricing

- Can qualify with your current debt and income

- Have at least a small down payment saved

- Want flexibility on property type, depending on lender and program guidelines

- Hope to remove PMI later if you build enough equity and meet requirements

The tradeoff is that conventional underwriting can be less forgiving than some government-backed options. If your credit score is lower, your debt-to-income ratio is tight, or your cash reserves are limited, another path may offer more flexibility.

Path 2: FHA Loans for Flexible Credit and Lower Down Payment Needs

FHA loans are insured by the Federal Housing Administration and are popular with first-time buyers because they can offer more flexible credit requirements than many conventional programs. They also allow a low down payment for eligible borrowers.

This path often works well for buyers who have steady income and enough cash to move forward, but may not have a long credit history or a high credit score. FHA loans can also be useful if your debt-to-income ratio is a little higher than what a conventional program may comfortably allow, though approval still depends on the full loan file and current guidelines.

FHA may be a good fit if you:

- Need a lower down payment option

- Have credit challenges but a stable income history

- Want a program widely used by first-time buyers

- Are purchasing a primary residence

- Can handle mortgage insurance as part of the payment

The key tradeoff is mortgage insurance. FHA loans typically include both an upfront mortgage insurance premium and annual mortgage insurance paid monthly. That does not make FHA a bad choice. It simply means you should compare the full payment and long-term cost against other options.

Path 3: VA Loans for Eligible Veterans, Service Members, and Surviving Spouses

For eligible borrowers, a VA loan can be one of the most powerful first-time home buyer paths available. VA loans are backed by the U.S. Department of Veterans Affairs and are designed to help qualifying veterans, active-duty service members, certain National Guard and Reserve members, and eligible surviving spouses buy homes.

The biggest advantage is that VA loans may allow qualified buyers to purchase with no down payment. They also do not require monthly mortgage insurance, which can make the monthly payment more attractive compared with some other low-down-payment options.

VA loans may be a strong fit if you:

- Have eligible military service or surviving spouse eligibility

- Want to explore no-down-payment financing

- Prefer avoiding monthly mortgage insurance

- Are buying a primary residence

- Can meet VA and lender requirements for income, credit, and property condition

There may be a VA funding fee, although some borrowers are exempt. Property requirements also matter, so it is important to work with a lender and real estate agent who understand VA purchases. If this path may apply to you, New Era Lending’s guide to VA loans for first-time home buyers explains eligibility and next steps in more detail.

Path 4: USDA Loans for Eligible Rural and Suburban Areas

USDA loans can be a valuable option for first-time buyers who are open to homes in eligible rural or some suburban areas. These loans are backed by the U.S. Department of Agriculture and are designed to support homeownership in qualifying locations.

Like VA loans, USDA loans may allow eligible borrowers to buy with no down payment. However, the home must be in an eligible area, and the borrower must meet income limits and other program requirements.

USDA may be worth exploring if you:

- Are open to rural or eligible suburban locations

- Need a no-down-payment option

- Meet household income limits for the area

- Are buying a primary residence

- Want a fixed-rate loan option with structured program guidelines

The main limitation is geography. Some buyers are surprised to find eligible areas near growing suburbs, while others discover that their preferred neighborhood does not qualify. USDA can be excellent when the location, income limits, and property all line up.

Path 5: Down Payment Assistance for Buyers Short on Cash

Down payment assistance can be a game changer for first-time home buyers who can afford a monthly payment but have not saved enough for the upfront costs. Assistance programs vary by state, county, city, housing agency, nonprofit, and sometimes employer or profession.

Assistance can come in different forms, including grants, forgivable loans, deferred second mortgages, or low-interest second loans. Some programs help with the down payment, some help with closing costs, and some can help with both.

This path may work well if you:

- Have steady income but limited savings

- Meet income or purchase price limits

- Are willing to complete required homebuyer education if needed

- Plan to occupy the home as your primary residence

- Understand whether the assistance must be repaid

The details matter. Some assistance is forgiven over time if you stay in the home. Some becomes due when you sell, refinance, or move out. Some may affect the loan options available to you or the interest rate you receive. Before assuming assistance is free money, read the terms carefully and compare your full payment.

For a deeper breakdown, review New Era Lending’s guide to down payment assistance for first-time home buyers.

Path 6: Seller Credits and Lender Credits to Reduce Cash Needed

Not every affordability strategy is a separate loan program. In some markets, first-time buyers can use seller credits or lender credits to reduce out-of-pocket costs at closing.

A seller credit means the seller agrees to contribute toward certain buyer closing costs, within program limits. This can be negotiated as part of the purchase contract. It may be especially useful if a home has been on the market for a while or the seller is motivated.

A lender credit can also reduce upfront costs, though it often comes with a higher interest rate. That may make sense if preserving cash is more important than securing the lowest possible rate, but it should be compared carefully.

These strategies can be useful when your monthly income is strong but your savings are tight. However, they do not eliminate the need to qualify, and they must fit within the rules for your loan type.

Path 7: Rate Buydowns for Buyers Focused on Payment Comfort

A rate buydown is another tool that can help with affordability. With a buydown, funds are used to reduce the interest rate, either temporarily or permanently, depending on the structure.

A temporary buydown may lower the payment for the first year or two, while a permanent buydown uses discount points to reduce the rate over the life of the loan. These can be paid by the buyer, seller, builder, or another allowed party, subject to loan rules.

This path may make sense if you have enough cash or seller concessions available and want to improve payment comfort. Still, do not rely on future income increases to make a payment affordable. A temporary buydown should be understood clearly, including what the payment will be after the reduced period ends.

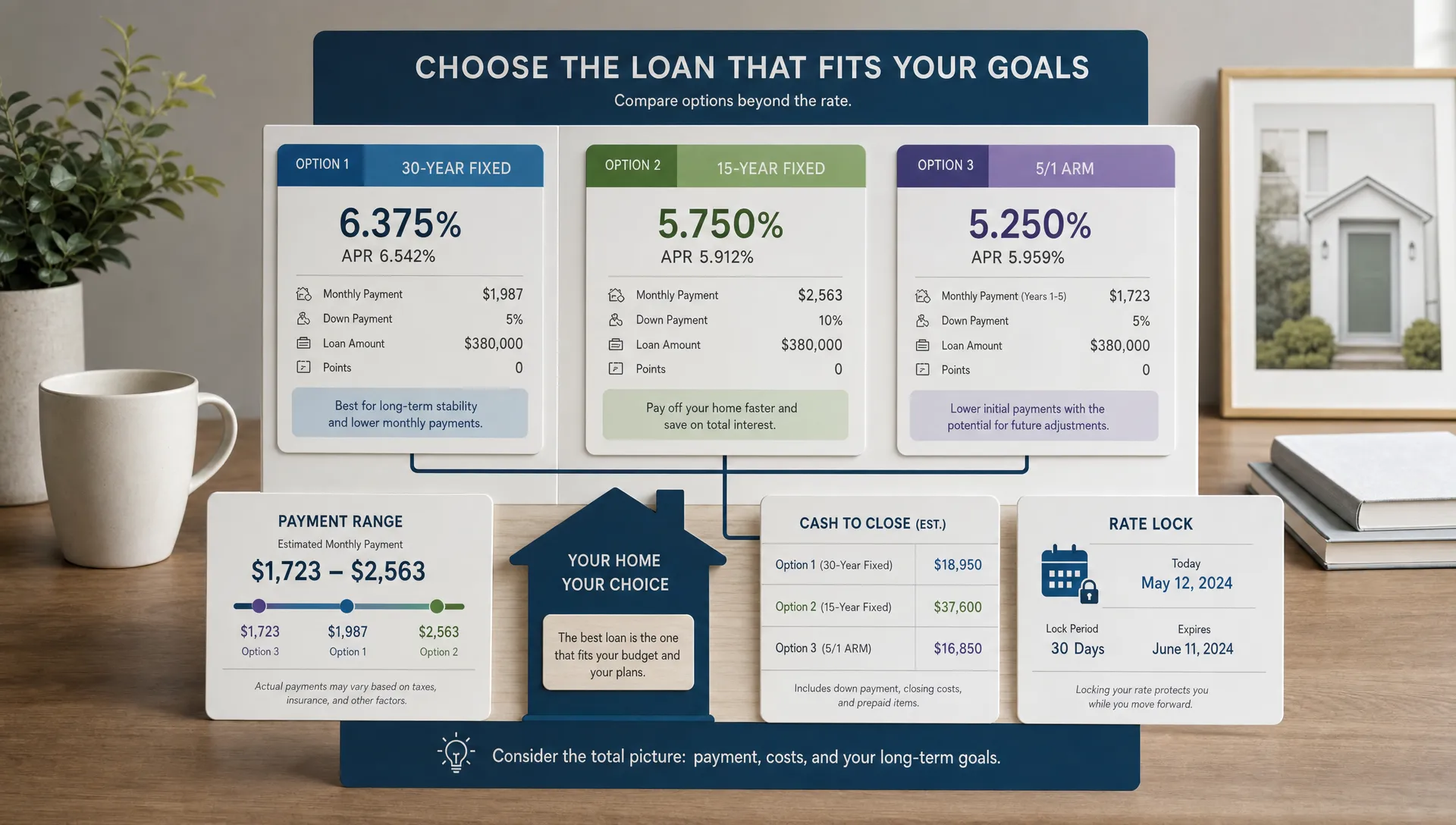

How to Decide Which Home Loan Path Is Best for You

The right first-time buyer loan path depends on how each program performs across four areas: upfront cash, monthly payment, approval flexibility, and long-term cost.

Ask yourself these questions before you commit to one option:

- Do I need the lowest down payment possible, or can I bring more cash to closing?

- Is my credit profile stronger, average, or still improving?

- Am I eligible for VA benefits, USDA financing, or local assistance?

- How long do I expect to stay in the home?

- Would I rather pay less upfront or aim for the lowest long-term cost?

- How much payment cushion do I want after closing?

A buyer with excellent credit and 5% down may find that conventional financing is the cleanest fit. A buyer with limited savings and eligible military service may find that VA is hard to beat. A buyer with steady income but lower credit may benefit from FHA. A buyer open to eligible rural or suburban areas may find USDA worth serious consideration. A buyer who qualifies for a local assistance program may combine that help with an FHA or conventional loan.

This is why pre-approval matters. Online calculators can estimate, but they cannot fully evaluate your credit, income, assets, debts, property type, and program eligibility. A strong pre-approval can show you which paths are realistic before you make an offer.

Build the Right Team Early

First-time buyers often think of the loan as a one-time transaction, but it is really a coordinated process. Your lender, real estate agent, title company, insurance provider, and sometimes assistance program administrator all affect the timing and experience.

The same is true for any major milestone that has many moving parts. People hire specialists such as Luuk Broos Events for complex celebrations because details, timing, and coordination matter. Your first home purchase deserves that same mindset: clear roles, proactive communication, and professionals who know how to keep the process moving.

When comparing mortgage providers, do not look only at the quoted rate. Also consider communication, loan options, transparency, responsiveness, fees, technology, and whether the lender can explain tradeoffs in plain English. New Era Lending’s article on how to choose a lender as a first-time home buyer can help you evaluate lenders more confidently.

Watch for Tradeoffs That First-Time Buyers Often Miss

Every loan path has advantages, but every path also has tradeoffs. The goal is not to avoid tradeoffs completely. The goal is to understand them before you are under contract.

Mortgage insurance is one common example. A low-down-payment loan may help you buy sooner, but the monthly mortgage insurance can affect affordability. That may still be worth it if homeownership is the priority and the payment fits your budget.

Closing costs are another common surprise. Even with a low down payment, you may need funds for lender fees, title charges, appraisal, insurance, taxes, and escrow setup. Seller credits, lender credits, and assistance programs can help, but they must be structured correctly.

Property requirements can also shape your options. FHA, VA, and USDA loans have standards related to safety, livability, and property condition. Condos may need to meet program-specific requirements. Manufactured homes, multi-unit properties, and fixer-uppers can involve additional rules.

Finally, remember that the lowest rate is not always the best loan. A slightly higher rate with lower upfront costs may fit one buyer better, while another buyer may prefer paying points for long-term savings. The best path is the one that supports both approval and sustainable homeownership.

A Simple Way to Narrow Your Options

If you are early in the process, use this quick framework:

- If you have strong credit and some savings, start with conventional options.

- If you need credit flexibility and a lower down payment, compare FHA.

- If you have eligible military service, review VA first.

- If you are open to eligible rural or suburban areas, check USDA.

- If cash to close is your biggest obstacle, explore down payment assistance.

- If the monthly payment is your biggest concern, compare credits, buydowns, taxes, insurance, and loan structure.

You do not need to choose alone. In fact, the smartest move is often to compare two or three realistic options side by side. Look at the estimated cash to close, monthly payment, mortgage insurance, interest rate, fees, and long-term flexibility.

Frequently Asked Questions

What is the best home loan for first-time home buyers? The best home loan depends on your credit, income, savings, location, and eligibility. Conventional, FHA, VA, USDA, and down payment assistance programs can all be strong choices for the right buyer.

Do first-time home buyers need 20% down? No. Many first-time buyers purchase with less than 20% down. Some conventional programs allow low down payments, FHA can offer low-down-payment options, and eligible VA or USDA buyers may qualify for no-down-payment financing.

Is FHA always better for first-time buyers? Not always. FHA can be helpful for flexible credit and lower down payment needs, but conventional financing may be better for buyers with stronger credit or those who want different mortgage insurance options. Compare the full payment and long-term cost.

Can I combine down payment assistance with a mortgage? Often, yes, but it depends on the assistance program and loan type. Some assistance programs work with FHA, conventional, VA, or USDA loans, while others have stricter rules.

When should I get pre-approved? Get pre-approved before you start making offers. Pre-approval helps you understand your realistic budget, compare loan paths, and show sellers that you are a serious buyer.

Take the Next Step With a Clear Mortgage Plan

Your first home loan should do more than get you approved. It should help you buy with confidence, understand your payment, and avoid surprises at closing.

New Era Lending combines smart mortgage technology with personalized human guidance for home buyers across 39 states. If you are comparing loan paths, exploring low-down-payment options, or trying to understand what you can afford, connect with New Era Lending to start building a mortgage plan that fits your first home goals.