.jpg)

.jpg)

.jpg)

How to Choose a Lender as a First-Time Home Buyer

Choosing the right lender can make your first home purchase feel clear, manageable, and financially safer. Choosing the wrong one can leave you confused about costs, scrambling for documents, or discovering too late that your loan terms are not what you expected.

For a first-time home buyer, a good lender does more than offer a mortgage. They help you understand what you can afford, explain your loan options, prepare you for closing costs, and guide you through the process without pressure or guesswork.

Here is how to choose a lender as a first-time home buyer, what to compare beyond the interest rate, and which warning signs to watch before you apply.

Why your lender matters so much as a first-time buyer

When you buy your first home, almost every decision feels new: pre-approval, down payment, loan type, rate locks, appraisals, underwriting, closing documents, and monthly payment estimates. Your lender is one of the few professionals involved from the beginning of your search through closing day.

That means the lender you choose can affect:

- How much home you can confidently afford

- Which loan programs you qualify for

- How quickly you can make a competitive offer

- How clearly you understand your total monthly payment

- How prepared you are for closing costs and cash-to-close

- Whether your loan process feels organized or stressful

A low advertised rate may get your attention, but the best lender for first-time home buyers is usually the one that combines competitive terms with clear communication, realistic guidance, and dependable execution.

Start by understanding your own buying profile

Before you compare lenders, take a few minutes to define what you need from the mortgage process. A lender can help refine the numbers, but you should have a basic sense of your situation first.

Think through your estimated price range, savings for down payment and closing costs, credit score range, income stability, debt payments, preferred timeline, and whether you may qualify for a special program such as FHA, VA, USDA, or down payment assistance.

This matters because different lenders may be stronger in different areas. Some may focus heavily on conventional loans. Others may be better equipped to guide first-time buyers through lower down payment options, assistance programs, or veteran loan benefits.

If you are still early in the process, it can help to review the basics of budgeting, pre-approval, and loan comparison before you start contacting lenders. New Era Lending’s guide on what to know before you buy your first home is a useful starting point for understanding the major moving pieces.

Look for education, not just approval

A first-time buyer-friendly lender should be willing to explain your options in plain language. Getting approved is important, but understanding why a loan fits your situation is just as important.

During your first conversation, pay attention to whether the lender explains:

- The difference between pre-qualification and pre-approval

- How your credit, income, debts, and assets affect your options

- How down payment size changes your payment and cash-to-close

- Whether mortgage insurance applies

- Which loan programs may fit your goals

- How closing costs, prepaid items, and escrow accounts work

A lender who only asks, “How much do you want to borrow?” may not be giving you enough guidance. A stronger lender will ask about your payment comfort zone, available cash, timeline, employment situation, and long-term plans for the home.

For example, a buyer with limited savings but steady income may need a different strategy than a buyer with a larger down payment but variable self-employed income. The right lender should help you compare those trade-offs instead of forcing you into a one-size-fits-all loan.

Compare loan options, not just lender names

First-time buyers often assume the choice is simply, “Which lender has the lowest rate?” In reality, you should also compare which loan options each lender can offer and explain.

Common first-time buyer loan options may include conventional loans, FHA loans, VA loans for eligible service members and veterans, USDA loans for eligible rural and suburban areas, and certain state or local assistance programs. Each option has different rules for down payment, credit, mortgage insurance, property eligibility, and seller contributions.

A good lender will not make the decision for you without context. Instead, they should show you how different loan options affect your monthly payment, upfront costs, and long-term flexibility. If you want a deeper overview of common mortgage types, New Era Lending’s guide to mortgage loan options for buyers can help you understand the basics before you compare lenders.

This is especially important if you are considering down payment assistance. Assistance programs can be valuable, but they may come with income limits, location rules, repayment terms, occupancy requirements, or extra approval steps. Your lender should be able to explain those details clearly before you depend on the assistance to make your offer work.

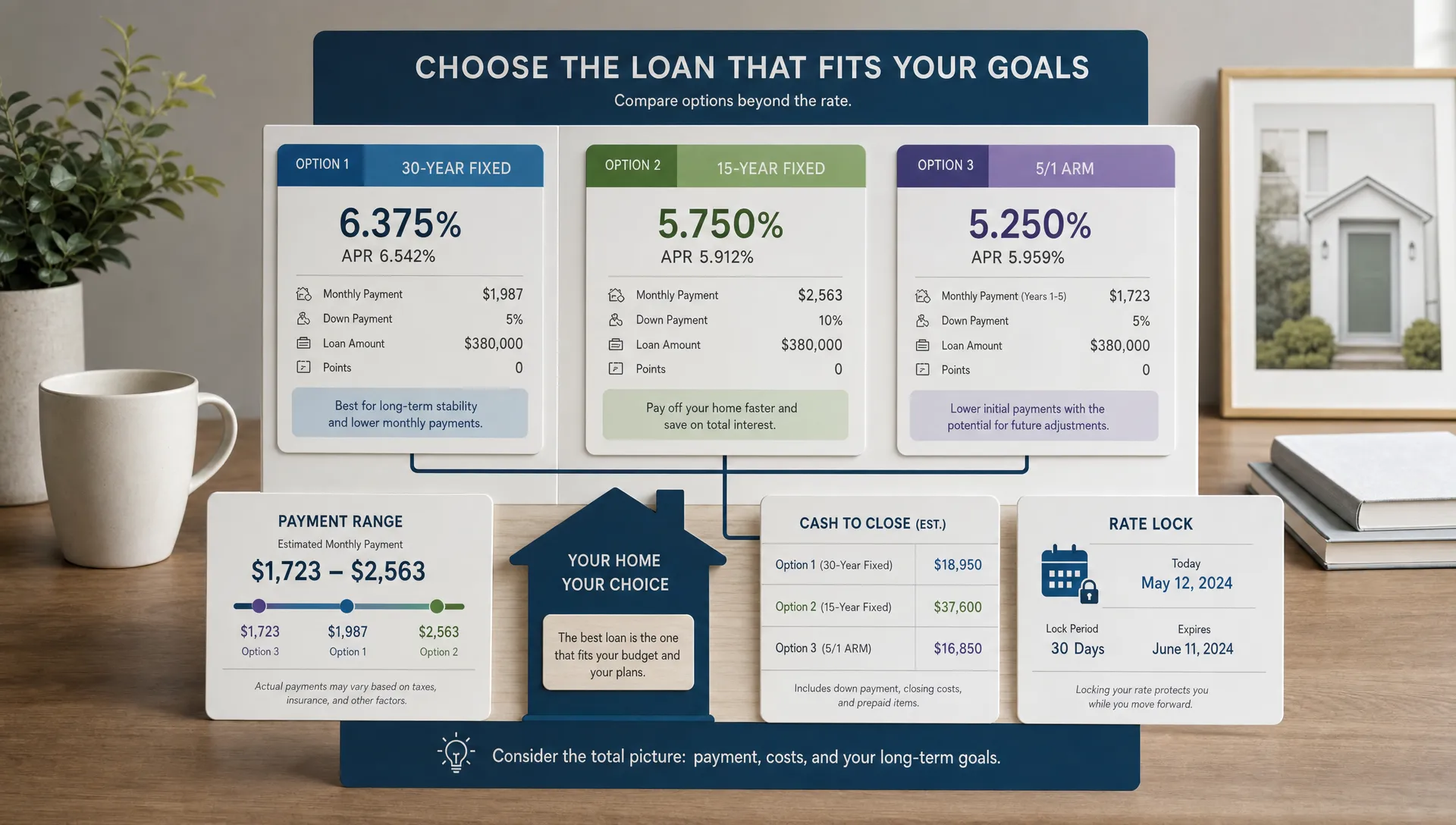

Know how to compare rates and fees correctly

Mortgage rates matter, but they do not tell the full story. Two lenders can quote the same interest rate while charging very different upfront costs. Another lender may quote a lower rate, but only because you are paying discount points at closing.

When comparing lenders, ask for the same loan scenario from each one. Use the same purchase price, down payment, credit profile, loan type, occupancy, and estimated closing date. Otherwise, you may be comparing different assumptions rather than different lenders.

Focus on these items:

- Interest rate: The percentage used to calculate your monthly principal and interest payment.

- APR: A broader cost measure that includes certain loan costs, useful for comparing similar loans.

- Discount points: Upfront fees paid to reduce the interest rate.

- Origination or lender fees: Charges from the lender for processing or originating the loan.

- Lender credits: Credits that may reduce upfront costs, often in exchange for a higher rate.

- Mortgage insurance: Required on many low down payment loans, depending on loan type and structure.

- Estimated cash-to-close: The total amount you may need at closing, including down payment, costs, and prepaid items.

Be careful not to judge a lender by the lowest monthly payment alone. A lower payment could come from a lower rate, but it could also come from a larger down payment assumption, a temporary buydown, missing taxes and insurance, or fees shifted elsewhere.

Test the lender’s communication before you commit

The mortgage process is deadline-driven. Once your offer is accepted, delays in communication can create real problems. Before choosing a lender, notice how they handle the early conversation.

Do they respond promptly? Do they answer the question you asked? Do they explain next steps clearly? Do they provide written details after the call? Do they make you feel comfortable asking basic questions?

Choosing a lender is still a professional-services decision. You would not hire a contractor, advisor, or creative partner without reviewing how they work, the way a business might assess a filmmaker’s portfolio and production services before investing in a brand video. Your lender deserves the same level of diligence because the outcome affects one of the largest purchases of your life.

For first-time buyers, communication style matters as much as speed. You want someone who can move quickly, but not so quickly that you feel rushed or confused.

Ask about the process from pre-approval to closing

A lender may sound helpful on day one, but you also need to understand how their process works after you apply. Ask what happens between pre-approval and closing so you know what to expect.

Key process questions include:

- How do I securely upload documents?

- Will I have a single point of contact or a team?

- How quickly do you typically issue pre-approval letters after receiving documents?

- What documents should I prepare now?

- How do you communicate during underwriting?

- When can I lock my rate?

- What could delay closing?

- How soon will I receive final numbers before closing?

Modern technology can make the process easier, especially when it supports secure document uploads, e-signatures, and faster approvals. But technology should not replace human guidance. For a first-time buyer, the best experience often combines efficient digital tools with a real person who can explain what is happening and why.

Watch for red flags when choosing a lender

Not every lender is the right fit for a first-time home buyer. If something feels unclear, rushed, or inconsistent, pause before moving forward.

Common red flags include:

- Vague answers about fees or cash-to-close

- Pressure to borrow at the top of your approval range

- A rate quote without clear assumptions

- Refusal to provide written estimates

- Little explanation of loan options

- Slow responses before you have even applied

- Promises that sound too good to be true

- Dismissive answers when you ask basic questions

A lender should not make you feel embarrassed for being new to the process. First-time buyers ask first-time buyer questions. That is normal. The right lender will expect those questions and answer them with patience.

Do not confuse pre-approval with affordability

One of the most important lessons for first-time buyers is that the amount you are approved for is not always the amount you should spend.

A pre-approval is based on financial guidelines, but your real comfort zone depends on your lifestyle, savings goals, future expenses, job stability, and risk tolerance. A lender may approve you for a certain monthly payment, but you are the one who has to live with that payment after closing.

A responsible lender should help you think through payment comfort, not just maximum qualification. They should be willing to run different scenarios so you can see how the payment changes at different prices, down payments, rates, taxes, insurance amounts, and loan types.

This is also where closing costs can surprise first-time buyers. Your down payment is only one part of the cash you may need. Closing costs, prepaid taxes, prepaid insurance, and escrow deposits can add significantly to your total cash-to-close. If you want to prepare for those expenses in more detail, New Era Lending’s article on closing costs first-time buyers often overlook is worth reviewing before you start making offers.

Choose a lender who helps you compete as a buyer

In many markets, sellers and real estate agents pay close attention to the strength of your financing. A well-prepared pre-approval can make your offer more credible, especially if the lender is responsive when the listing agent has questions.

Ask potential lenders how they support buyers during the offer stage. For example, can they update pre-approval letters for different offer amounts? Can they help you understand how changing the purchase price affects payment and cash-to-close? Can they coordinate with your real estate agent when timing matters?

This does not mean you should stretch beyond your budget to win a home. It means your lender should help you move confidently when the right home comes along.

Questions to ask before choosing your lender

Before you decide, ask each lender the same set of questions. Their answers will reveal a lot about their transparency, experience, and fit.

- What loan programs should I consider based on my situation?

- What monthly payment range would be realistic for my goals?

- What are the estimated lender fees for this loan?

- Are discount points included in the quoted rate?

- What is included in the estimated cash-to-close?

- When can I lock my rate, and how long does the lock last?

- What documents do you need for a strong pre-approval?

- How do you handle communication during underwriting?

- What common issues should I avoid before closing?

- Who will I contact if I have questions after I apply?

The strongest lenders will answer directly and explain the reasoning behind their recommendations. If you leave the conversation more confused than when you started, that may be a sign to keep looking.

How New Era Lending supports first-time home buyers

New Era Lending is built around a simpler, more transparent mortgage experience for buyers who want both smart technology and human guidance. For first-time home buyers, that combination can be especially valuable because the process involves many unfamiliar steps.

Through personalized mortgage solutions, educational support, secure document uploads, e-signature capabilities, a wide range of loan options, and guidance from experienced professionals, New Era Lending helps buyers move through home financing with more clarity. The company serves borrowers across 39 states and offers home purchase, refinance, cash-out, and specialized veteran loan programs.

If you are comparing lenders, look for the same core qualities: clear explanations, transparent rates and terms, responsive support, secure technology, and loan options that fit your actual goals.

Frequently Asked Questions

What is the best lender for a first-time home buyer? The best lender is one that explains your options clearly, provides transparent estimates, communicates quickly, and helps you choose a loan that fits your budget and goals. The right choice depends on your credit, income, savings, timeline, location, and loan needs.

Should I choose the lender with the lowest interest rate? Not automatically. A low rate may come with higher fees, discount points, or assumptions that do not match your situation. Compare the full loan estimate, including APR, lender fees, credits, mortgage insurance, and cash-to-close.

How many lenders should I compare before applying? Many first-time buyers compare at least two or three lenders. The goal is not only to compare pricing, but also communication, loan options, process, and confidence in the lender’s ability to close on time.

What should I ask a lender before getting pre-approved? Ask about loan programs, estimated payment, closing costs, required documents, rate locks, communication, approval timeline, and what could affect your final approval. A good lender will welcome these questions.

Can a first-time home buyer qualify with less than 20% down? Yes, many buyers purchase with less than 20% down, depending on the loan program and qualification details. Conventional, FHA, VA, USDA, and assistance programs may offer lower down payment paths for eligible buyers.

Take the next step with confidence

Choosing a lender as a first-time home buyer is not just about finding a mortgage. It is about finding a guide who can help you understand your numbers, compare your options, avoid surprises, and move toward closing with confidence.

If you are ready to explore your path to homeownership, connect with New Era Lending to learn how personalized guidance and modern mortgage tools can help make your first home purchase clearer and more manageable.