.jpg)

.jpg)

.jpg)

What to Know Before You Buy Your First Home

Buying your first home can feel like a race: find a listing, make an offer, get the keys. In reality, the smartest first-time buyers slow down before they speed up. They learn what lenders look for, how much the home will truly cost, and which decisions can affect their budget long after closing day.

Before you buy your first home, it helps to think beyond the sale price. Your mortgage, insurance, taxes, maintenance, loan program, inspection results, and closing timeline all shape whether the home is affordable and sustainable. Here is what to know before you start shopping seriously.

Start With the Life Plan, Not the Listing

A home is a financial decision, but it is also a lifestyle decision. Before browsing homes every night, ask yourself what you need the home to do for you over the next several years.

Are you planning to stay in the area for at least three to five years? Is your household likely to grow or change? Will your commute, school needs, or work-from-home setup matter? Do you want a move-in-ready home, or are you comfortable with repairs?

These questions matter because the “right” home is not always the highest-priced home you can qualify for. A smaller payment with more breathing room may be better than stretching into a house that leaves no room for furniture, repairs, travel, savings, or life changes.

The same principle applies to any major long-term goal: a plan works best when it is realistic and supported. Whether you are building financial stability or pursuing personalized coaching for lasting results, success usually comes from consistent habits, good guidance, and choices that fit your real life.

Know the Numbers Lenders Will Review

When you apply for a mortgage, lenders evaluate your ability and likelihood to repay the loan. That review is more detailed than simply checking whether you have a job.

The main numbers include:

- Credit profile: Your credit score, payment history, account balances, and recent credit activity can affect loan eligibility and pricing.

- Income: Lenders look for stable, documentable income from employment, self-employment, retirement, military benefits, or other acceptable sources.

- Debt-to-income ratio: This compares your monthly debt payments to your gross monthly income.

- Cash to close: This includes your down payment, closing costs, prepaid items, and any required reserves.

- Assets and reserves: Money left after closing can help strengthen your file and protect you after move-in.

A common first-time buyer mistake is assuming that approval is based only on the down payment. In practice, a buyer with a modest down payment, strong credit, manageable debts, and steady income may be in a better position than someone with more cash but high monthly obligations.

Get Pre-Approved Before You Fall in Love With a Home

A mortgage pre-approval gives you a clearer buying range and helps you understand what loan options may fit your situation. It can also make your offer more credible to sellers.

Pre-approval is different from casually estimating affordability online. A serious pre-approval usually involves reviewing income, assets, debts, credit, and the type of property you plan to buy. The more accurate the information, the more useful the pre-approval becomes.

Before pre-approval, gather basic documents such as pay stubs, W-2s, tax returns if needed, bank statements, ID, and explanations for any unusual deposits or credit events. If you are self-employed, have variable income, or receive military benefits, your documentation may look different.

Once you are pre-approved, avoid making major financial changes. Do not open new credit cards, finance a car, move large sums without documentation, or change jobs without talking to your loan officer first. Even positive changes can require new paperwork and may slow down underwriting.

You May Not Need 20% Down, But You Do Need a Cash Plan

Many first-time buyers delay homeownership because they think 20% down is required. In many cases, it is not. Conventional, FHA, VA, USDA, and assistance programs may offer lower down payment paths depending on eligibility, location, credit, income, and property type.

That said, “low down payment” does not mean “no money needed.” You still need to plan for closing costs, prepaid taxes and insurance, inspection fees, appraisal costs, moving expenses, and post-closing reserves.

If down payment is your main concern, review your options early rather than guessing. New Era Lending’s guide to down payment assistance for first-time home buyers explains common program types and eligibility considerations.

The goal is not always to put down as much as possible. Sometimes preserving cash after closing is the smarter move, especially if the home may need repairs, appliances, furniture, or seasonal maintenance.

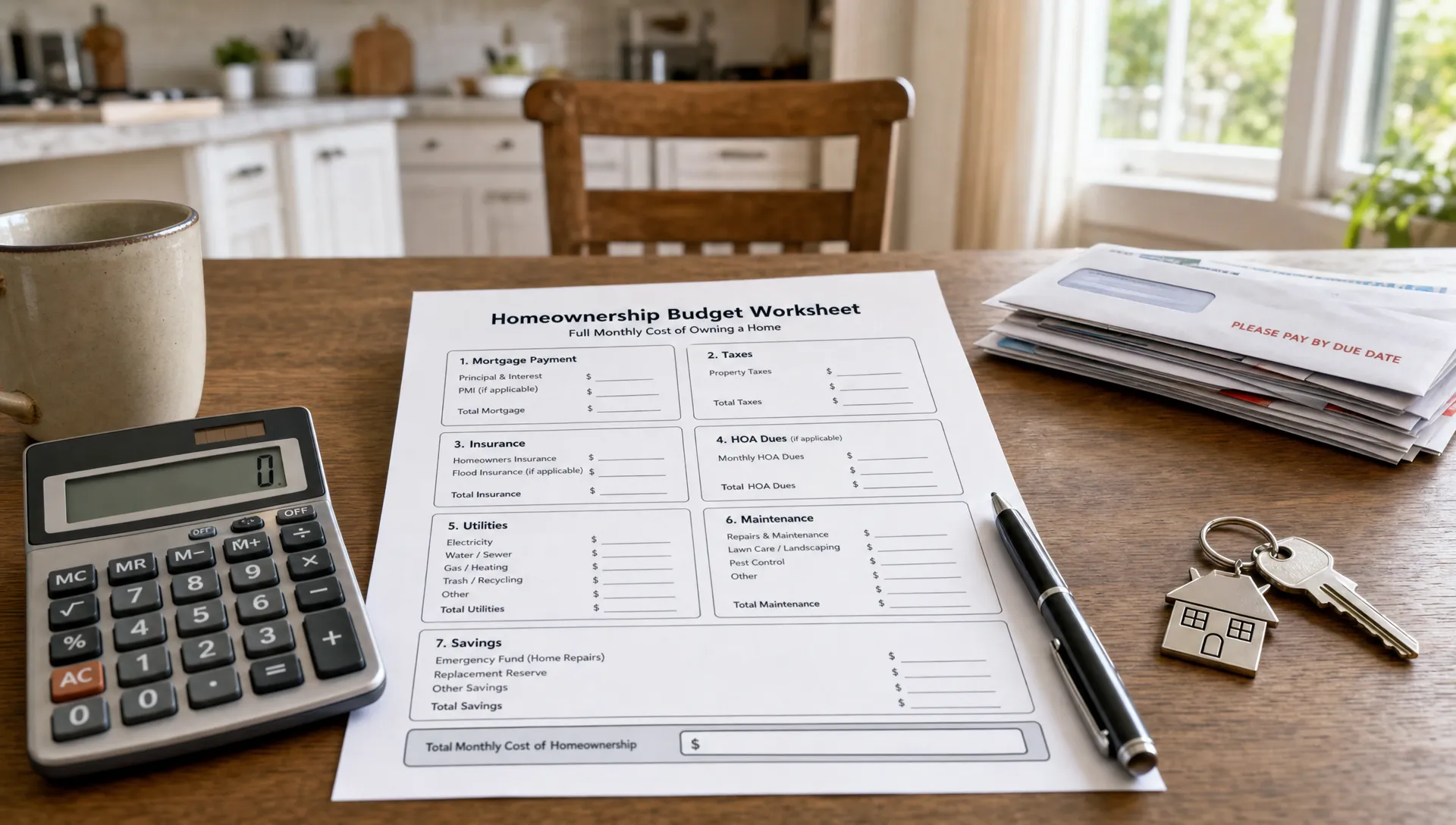

Focus on the Full Monthly Payment

The purchase price gets most of the attention, but your monthly payment is what affects daily life. A mortgage payment can include several parts:

- Principal and interest

- Property taxes

- Homeowners insurance

- Mortgage insurance, if applicable

- HOA dues, if the property has them

- Flood insurance or other required coverage in certain areas

Two homes with the same price can have very different monthly costs. One may be in an area with higher property taxes. Another may have expensive HOA dues. A third may require additional insurance coverage.

Before making an offer, ask for realistic estimates. Property taxes may change after purchase, insurance premiums can vary by property condition and location, and HOA dues may rise over time. A payment that looks manageable at first glance can become uncomfortable if you overlook these details.

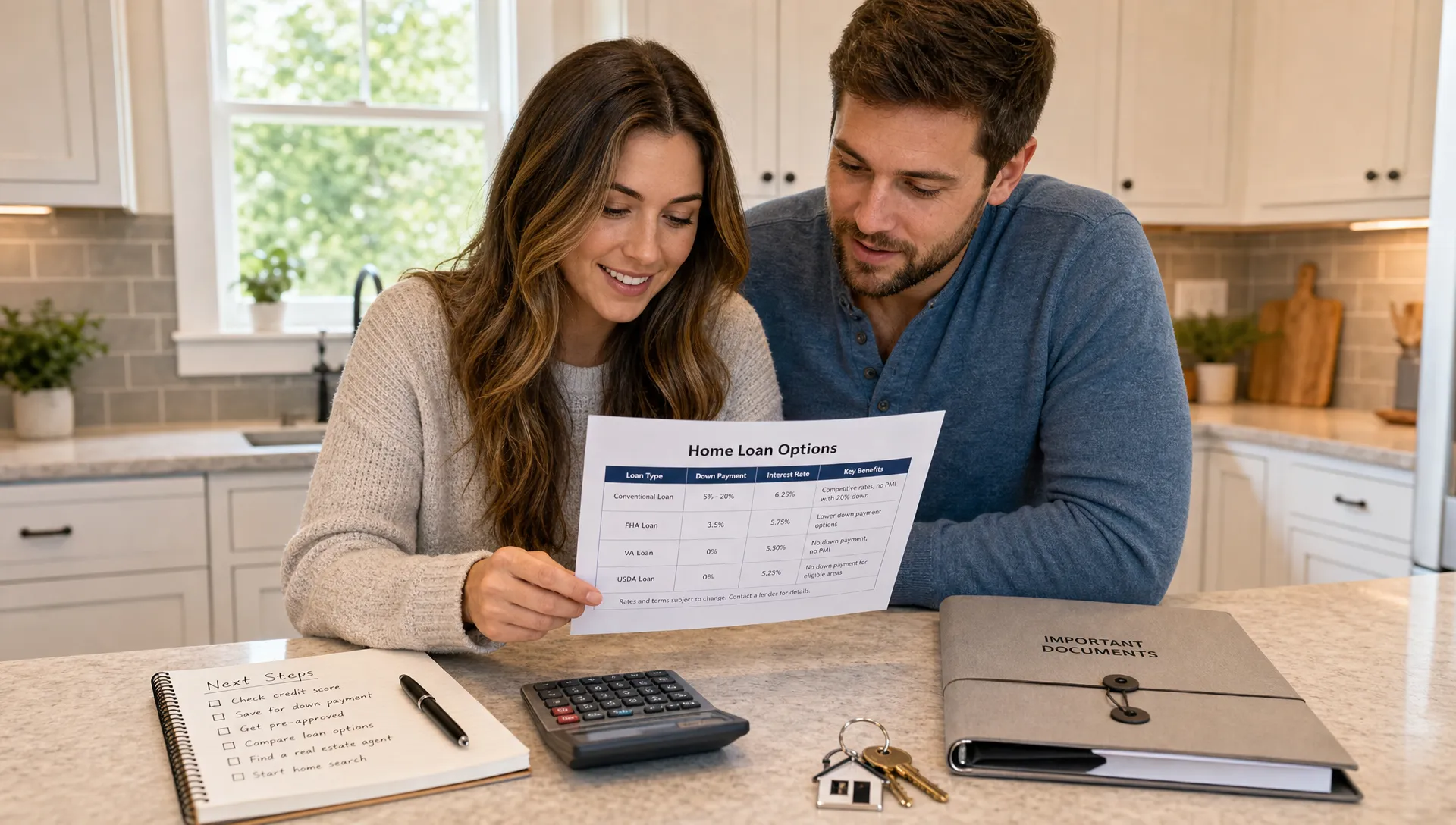

Understand Your Loan Options Before You Choose One

There is no single best mortgage for every first-time buyer. The right loan depends on your credit profile, cash available, military eligibility, location, income, property type, and long-term goals.

Common options include conventional loans, FHA loans, VA loans for eligible service members and veterans, USDA loans for eligible rural and suburban properties, and jumbo loans for higher-priced homes. Some buyers may also consider renovation financing or other specialized programs.

Each option has tradeoffs. FHA loans may be helpful for buyers with lower credit scores or smaller down payments, but mortgage insurance rules differ from conventional loans. VA loans can be powerful for eligible buyers because they may allow 0% down and no monthly private mortgage insurance, but there are service eligibility and property requirements. Conventional loans can be flexible, but pricing and mortgage insurance may depend heavily on credit and down payment.

For a deeper comparison, see New Era Lending’s guide to mortgage loan programs.

Learn How to Compare Loan Offers Correctly

A lower interest rate is not automatically the better deal. A rate can be paired with higher upfront costs, discount points, or different terms. To compare offers fairly, ask for the same scenario from each lender: same purchase price, down payment, loan type, lock period, and estimated closing date.

The key document is the Loan Estimate. According to the Consumer Financial Protection Bureau, lenders are generally required to provide a Loan Estimate within three business days after receiving a mortgage application. This document helps you compare interest rate, APR, monthly payment, closing costs, cash to close, and key loan features.

Pay close attention to:

- Whether the rate is locked or floating

- Whether points are included

- The total estimated cash to close

- Lender fees versus third-party fees

- Mortgage insurance costs

- Whether taxes and insurance are escrowed

If two offers are difficult to compare, ask your loan officer to walk through the differences line by line. Clarity before closing is far better than surprise after signing.

The Offer Is About More Than Price

When you find a home, your real estate agent will help structure the offer. Price matters, but sellers also evaluate timing, contingencies, financing strength, and confidence that the deal will close.

Important offer terms may include inspection contingency, appraisal contingency, financing contingency, earnest money, seller credits, closing date, and repair negotiations. In competitive markets, buyers sometimes feel pressure to waive protections. Be cautious. Waiving an inspection or appraisal contingency can create real financial risk, especially for a first-time buyer.

An inspection helps you understand the home’s condition. An appraisal helps the lender confirm that the property value supports the loan. If the appraisal comes in low, you may need to renegotiate, bring more cash, change loan terms, or walk away if your contract allows it.

The best offer is not always the most aggressive offer. It is the offer you can afford, understand, and close with confidence.

Remember That the Property Must Qualify Too

Mortgage approval is not only about you. The property also has to meet lender and program requirements.

Lenders may review the appraisal, title report, insurance availability, occupancy type, condo approval status, property condition, and whether the home meets program rules. Government-backed loans such as FHA, VA, and USDA may have additional property standards.

This is why a beautiful home can still create financing challenges. Peeling paint, safety issues, unpermitted additions, roof problems, condo litigation, title defects, or insurance concerns can delay or disrupt closing.

Before you make an offer, ask questions about the property’s condition, HOA, recent repairs, insurance history, and any known issues. Your agent and loan officer can help flag items that may matter for financing.

Build a First-Year Homeownership Budget

Closing day is not the finish line. It is the start of ownership.

A first-year budget should include more than your mortgage payment. Plan for utility deposits, moving costs, furniture, lawn care, tools, appliance repairs, pest control, seasonal maintenance, and possible insurance or tax changes.

A good rule of thumb is to keep a post-closing emergency fund if possible. Even a well-inspected home can surprise you. Water heaters fail, HVAC systems need service, and small repairs add up quickly.

This is one reason buying at the top of your approval range can be risky. Lenders determine what may be approvable, but only you can decide what feels comfortable for your lifestyle and savings goals.

Know the Typical Timeline

Every transaction is different, but understanding the general path can reduce stress.

The process often looks like this:

- Budget and pre-approval: Review your finances, submit documents, and clarify your buying range.

- Home search: Tour homes that match your budget, location, and loan requirements.

- Offer and contract: Negotiate price, contingencies, credits, and closing date.

- Loan application and processing: Update documents, confirm loan terms, and prepare for underwriting.

- Inspection, appraisal, and title work: Verify property condition, value, ownership, and insurability.

- Underwriting and final approval: The lender reviews your file and clears remaining conditions.

- Closing: You sign final documents, bring required funds, and ownership transfers.

Delays can happen, especially if documents are missing, the appraisal takes longer than expected, repairs are required, or financial changes occur during the process. Fast communication helps. Responding quickly to document requests can keep your closing on track.

Choose Guidance That Matches the Size of the Decision

First-time buyers do not need to become mortgage experts overnight. But you do need a team that explains your options clearly and helps you avoid preventable mistakes.

A strong homebuying team may include a loan officer, real estate agent, home inspector, insurance agent, and, in some states, a real estate attorney. Each person plays a different role.

Your lender should help you understand what you qualify for, what different loan programs cost, how your payment is built, and what steps remain before closing. Technology can make the process faster, but human guidance still matters when you have questions, unusual income, tight timelines, or multiple loan options to compare.

New Era Lending combines smart mortgage tools with personalized support, including secure document uploads, e-signature support, transparent guidance, and a broad range of purchase and refinance options across 39 states.

Frequently Asked Questions

How early should I get pre-approved before buying my first home? Many buyers benefit from getting pre-approved before they start touring homes seriously. If you are six to twelve months away, an early consultation can still help you improve credit, reduce debt, or plan cash to close.

Do I need perfect credit to buy my first home? No. Different loan programs have different credit guidelines. Stronger credit can improve your options and pricing, but buyers with less-than-perfect credit may still qualify depending on income, debts, down payment, and loan type.

What is the biggest cost first-time buyers forget? Closing costs and prepaid items are commonly overlooked. Buyers also forget about the first year of ownership, including repairs, utilities, maintenance, and moving expenses.

Should I buy the most expensive home I qualify for? Not necessarily. Your approval amount is based on lending guidelines, not your personal comfort level. Choose a payment that leaves room for savings, repairs, and normal life.

Can I change loan programs after I make an offer? Sometimes, but it depends on the contract, property, timeline, and underwriting details. Changing programs can affect appraisal requirements, mortgage insurance, cash to close, and closing speed, so talk with your loan officer before making a switch.

Take the Next Step With Confidence

Before you buy your first home, get clear on your numbers, your timeline, your loan options, and the true cost of ownership. The earlier you understand those pieces, the easier it is to shop with confidence instead of uncertainty.

If you are ready to explore your options, connect with New Era Lending for personalized guidance, modern mortgage tools, and a clearer path from pre-approval to closing.