.jpg)

.jpg)

.jpg)

Thinking About Changing Mortgage Terms? Read This First

Changing mortgage terms can be a smart way to make your home loan fit your life better, but it is not a decision to make based on one lower payment quote or one headline rate. Your mortgage term affects your monthly budget, total interest, payoff timeline, equity strategy, and sometimes your ability to qualify for other financial goals.

Before you refinance, recast, modify, or start making extra payments, take a step back. The right move depends on what you are trying to solve, how long you plan to keep the home, what the new loan will cost, and whether the change improves your full financial picture.

What does changing mortgage terms actually mean?

Many homeowners use the phrase “changing mortgage terms” to mean any adjustment that makes a mortgage payment look different. In practice, it can involve several separate parts of your loan.

Your mortgage terms may include your interest rate, loan length, payment structure, amortization schedule, loan type, escrow setup, mortgage insurance, and whether you are taking cash out of your equity. Some changes require a new loan. Others may be handled through your current servicer, depending on the loan and your situation.

For example, refinancing from a 30-year fixed mortgage into a 20-year fixed mortgage is a formal term change because you are replacing your current loan. Making extra principal payments can shorten your payoff timeline without rewriting the loan. A loan recast may lower your payment after a large principal payment while keeping the same interest rate. A loan modification is usually reserved for hardship situations and is handled differently from a standard refinance.

That distinction matters. Two options can produce a similar monthly payment but very different long-term costs.

Why homeowners consider changing mortgage terms

Most homeowners start looking at term changes because something has shifted. Maybe rates have moved, income has changed, home values have increased, or the original loan no longer fits the household budget.

Common reasons include lowering the monthly payment, paying the loan off sooner, switching from an adjustable-rate mortgage to a fixed-rate mortgage, removing mortgage insurance, accessing equity, or consolidating higher-interest debt. Sometimes the motivation is not the mortgage itself, but a life change that affects cash flow.

A growing family, a career transition, medical expenses, tuition, caregiving costs, or specialized support services can all change what a comfortable payment looks like. For instance, resources such as community-based day programs show how education, care, work, and activity support can become part of a broader household planning conversation. When non-housing needs shift, your mortgage strategy may need to shift too.

The key is to identify the real problem before choosing the tool. If the problem is short-term cash flow, a lower payment may help. If the problem is long-term interest cost, shortening the term or paying extra principal may be better. If the problem is financial uncertainty, predictability may matter more than the lowest possible payment.

The main ways to change mortgage terms

There is no single best way to adjust a mortgage. Each option has a different purpose, approval process, and cost profile.

Rate-and-term refinance

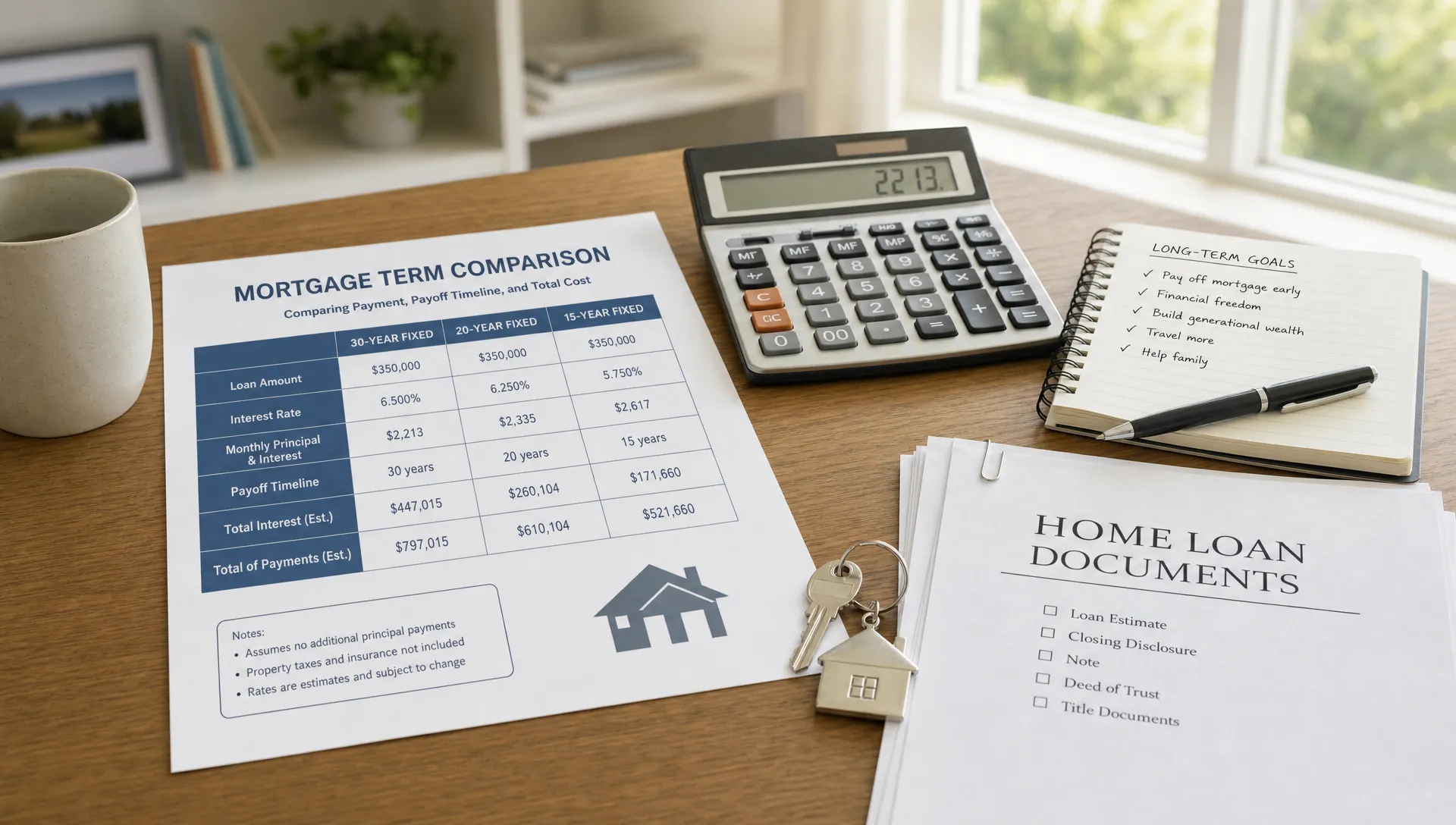

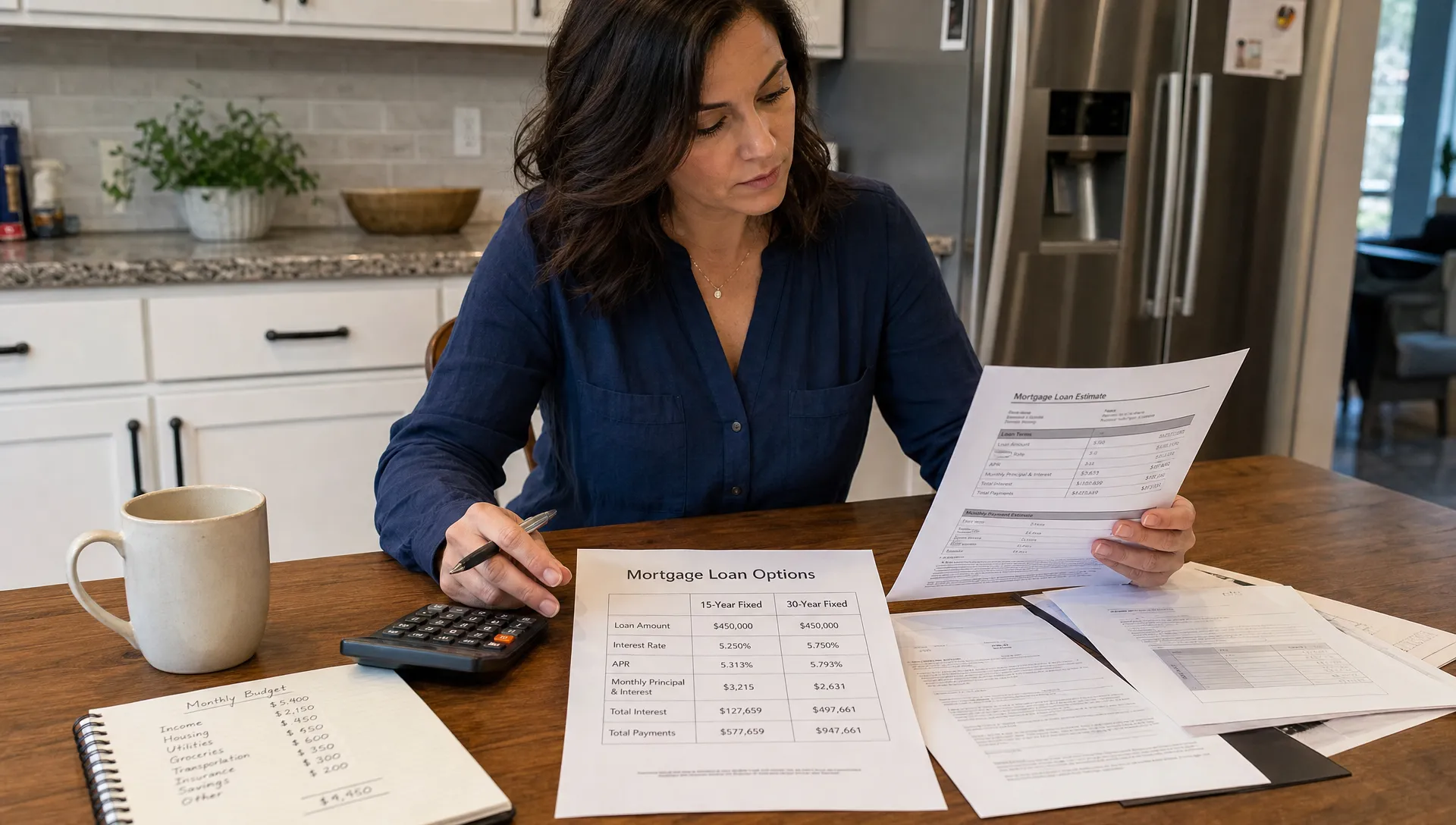

A rate-and-term refinance replaces your current mortgage with a new one, usually to change the interest rate, loan length, or both. This is often the first option homeowners think about when rates drop or when they want to move from a 30-year loan into a shorter term.

A lower rate can reduce monthly payments and total interest, but the full picture depends on closing costs, the new term length, and how long you keep the home. If you are comparing a refinance primarily because the rate looks better, it is worth asking whether a new mortgage rate is good enough to refinance after fees and timeline are included.

Shorter-term refinance

Refinancing into a shorter term, such as moving from 30 years to 20 or 15 years, can help you build equity faster and reduce total interest. The tradeoff is usually a higher monthly payment.

This can be a strong strategy for homeowners with stable income and enough room in the budget. It can be risky if it leaves no margin for emergencies, insurance increases, repairs, or income changes. If your goal is faster payoff without creating pressure, compare a formal refinance with flexible strategies like extra principal payments. New Era Lending’s guide on how to shorten your loan term without stress goes deeper into that balance.

Longer-term refinance or term extension

Extending the term can reduce the monthly payment, which may create needed breathing room. However, it can also increase total interest because you may be restarting the repayment clock.

This does not mean extending the term is automatically wrong. If a lower payment prevents missed payments, preserves emergency savings, or helps stabilize the household, it may be the practical choice. The mistake is focusing only on the lower monthly payment without measuring the lifetime cost.

Cash-out refinance

A cash-out refinance replaces your current loan with a larger one and gives you access to part of your home equity in cash. Homeowners often consider this for renovations, debt consolidation, major expenses, or investment in the property.

Because you are increasing the loan balance, the decision should be handled carefully. Cash-out refinancing may make sense when the funds have a clear purpose and the new payment fits comfortably. It can be risky if it turns short-term spending into long-term mortgage debt without changing the underlying budget.

Mortgage recast

A recast is different from a refinance. With a recast, you make a lump-sum principal payment and the lender recalculates the monthly payment based on the lower balance. Your interest rate and original maturity date usually stay the same.

Recasting can be useful after receiving a bonus, inheritance, sale proceeds, or other lump sum. It may involve a smaller fee than refinancing, but not every loan is eligible, and it does not usually lower your interest rate.

Loan modification

A loan modification changes the terms of an existing mortgage, often because the borrower is experiencing financial hardship. It may involve adjusting the rate, extending the term, adding missed payments to the balance, or other changes approved by the servicer.

This is not the same as shopping for a better refinance offer. If you are current on your mortgage and simply want better terms, a refinance or recast is usually the more relevant path. If you are struggling to make payments, contacting your servicer early is important.

The cost math you should run first

Changing mortgage terms is not only about the new payment. It is about what you pay to get that payment and how long the benefit lasts.

Start with the difference between your current monthly payment and the proposed monthly payment. Then compare that monthly savings with estimated closing costs or fees. This gives you a basic break-even point.

For example, if refinancing saves $250 per month and costs $5,000, the simple break-even point is 20 months. If you expect to sell the home in a year, that may not work. If you expect to stay for five years or more, it may be worth a closer look.

But break-even is only the beginning. You should also compare total interest, cash needed at closing, points, lender credits, escrow changes, mortgage insurance, and whether the new term adds years back onto your repayment schedule. A loan that saves money this month can still cost more over time if it stretches the debt too far.

For a broader look at the mechanics, review how different loan payment terms can raise or lower costs before you commit to a new structure.

Questions to ask before changing mortgage terms

A better mortgage decision usually starts with better questions. Before signing a refinance application or requesting a change from your servicer, make sure you can answer these clearly.

- What is my primary goal? Lower payment, faster payoff, rate stability, equity access, or debt consolidation are different goals and may require different solutions.

- How long do I expect to keep this home? The shorter your timeline, the harder it is to justify major closing costs.

- What is the all-in cost? Ask about lender fees, title fees, appraisal fees, points, credits, prepaid taxes, insurance, and escrow deposits.

- Am I resetting my loan clock? A new 30-year loan can reduce payment but may extend the time you carry mortgage debt.

- Can I comfortably afford the new payment? This matters especially when shortening the term or taking cash out.

- What happens if income changes? Build in margin for emergencies, repairs, tax changes, insurance increases, and family needs.

You should also ask what rate is being quoted, whether it is locked, how long the lock lasts, and what could change before closing. Mortgage pricing can shift based on credit score, equity, loan program, property type, occupancy, and market conditions.

When changing mortgage terms may make sense

Changing mortgage terms may be worth exploring when the new loan clearly improves your situation after costs are included.

It may make sense if you can lower your rate enough to recover closing costs within a reasonable time, especially if you plan to stay in the home. It may also make sense if you can remove mortgage insurance, shorten the term without straining cash flow, or switch from an adjustable rate to a fixed rate for more predictable payments.

A change may also be practical when your monthly payment no longer fits your life. If extending the term helps you maintain savings, avoid missed payments, or reduce pressure during a transition, the additional interest may be an acceptable tradeoff. The right answer is not always the mathematically cheapest option. It is the option that fits your goals, risk tolerance, and long-term plan.

Cash-out refinancing may be reasonable when the funds are used strategically, such as for value-adding home improvements or consolidating expensive debt with a disciplined payoff plan. The important part is knowing that home equity is not free money. It is borrowed money secured by your home.

When changing mortgage terms may not be worth it

A mortgage change may not be worth it if the savings are small, the closing costs are high, or you do not plan to keep the home long enough to benefit. It may also be a poor fit if the new payment only looks better because the loan term is being stretched far beyond your current payoff schedule.

Be cautious if you are refinancing repeatedly without a clear reason. Each refinance can add costs, reset amortization, or reduce equity depending on how fees are handled. Also be careful with debt consolidation if you are not addressing the habits or circumstances that created the debt. Rolling credit card balances into a mortgage can lower the interest rate, but it also turns unsecured debt into debt tied to your home.

Shortening the term can also backfire if it makes your monthly payment too tight. Paying off a mortgage faster is appealing, but not at the expense of emergency savings, retirement contributions, insurance coverage, or necessary home maintenance.

How to compare offers the right way

If you decide to explore a refinance or other term change, compare offers using the same loan amount, loan type, term length, and rate-lock assumptions. Otherwise, you may be comparing very different products.

The interest rate matters, but it is not the only number. Review the annual percentage rate, closing costs, discount points, lender credits, cash to close, monthly principal and interest, mortgage insurance, escrow assumptions, and total interest over the time you expect to keep the loan.

A lower rate with high points may be better for a long-term homeowner and worse for someone planning to move soon. A no-closing-cost refinance may reduce upfront cash, but it often means a higher rate or costs rolled into the loan. Neither structure is automatically good or bad. The better choice depends on your timeline and cash flow.

Ask each lender to explain the tradeoffs in plain English. If you cannot clearly see why one option is better than another, slow down before signing.

A simple decision framework

Use this framework before changing mortgage terms:

- Define the goal: Write down the exact outcome you want, such as “lower my payment by at least $300” or “pay off the loan before retirement.”

- Know your current loan: Confirm your balance, rate, remaining term, payment breakdown, escrow status, mortgage insurance, and any prepayment terms.

- Estimate your timeline: Decide how long you realistically expect to stay in the home or keep the new loan.

- Compare total costs: Look beyond the monthly payment and include closing costs, points, credits, interest, and cash to close.

- Stress-test the payment: Make sure the new payment works if taxes, insurance, utilities, or household expenses increase.

- Choose the least complicated option that solves the problem: Sometimes that is a refinance. Sometimes it is a recast, extra payments, or no change at all.

This process helps you avoid making a permanent loan decision based on a temporary feeling of payment pressure or rate excitement.

How New Era Lending can help

Changing mortgage terms is easier when you have clear numbers and a guide who can explain the tradeoffs. New Era Lending combines a technology-driven mortgage process with personalized human guidance, helping homeowners evaluate purchase, refinance, and equity-access options with more confidence.

That means you can look at payment, term, rate, and cost scenarios without losing sight of the bigger question: does this change actually help you? With secure document uploads, e-signature support, transparent conversations around rates and terms, and loan options available across 39 states, the process is designed to be modern without feeling impersonal.

Frequently Asked Questions

Can I change my mortgage term without refinancing? Sometimes. Extra principal payments may shorten your payoff timeline without a refinance, and a recast may lower your payment after a lump-sum principal payment if your loan is eligible. A loan modification may also change terms in hardship situations, but it is different from a standard refinance.

Is changing mortgage terms the same as refinancing? Not always. Refinancing is one way to change mortgage terms because it replaces your current loan with a new one. Recasting, making extra payments, and loan modifications can also affect how your mortgage works, but they do not all create a new loan.

Does changing mortgage terms hurt my credit? Applying for a refinance can involve a hard credit inquiry, and the new loan may affect your credit profile. The impact is usually only one part of the bigger decision. On-time payments and a manageable loan structure matter more over the long run.

Should I lower my payment or shorten my mortgage term? It depends on your goal. Lowering the payment may improve cash flow, while shortening the term can reduce total interest and build equity faster. The best choice is the one that fits your income stability, savings, timeline, and risk tolerance.

How do I know if the closing costs are worth it? Compare your monthly savings with the cost to make the change, then consider how long you plan to keep the loan. If you will not keep the home or loan long enough to recover the costs, the change may not be worthwhile.

Ready to review your mortgage options?

If you are thinking about changing mortgage terms, do not rely on guesswork. The right move could save money, create flexibility, or help you pay off your home sooner, but only if the numbers support it.

Connect with New Era Lending to compare your options, understand the tradeoffs, and choose a mortgage strategy that fits your next chapter.