.jpg)

.jpg)

.jpg)

What Changes My Rate on a Mortgage Offer?

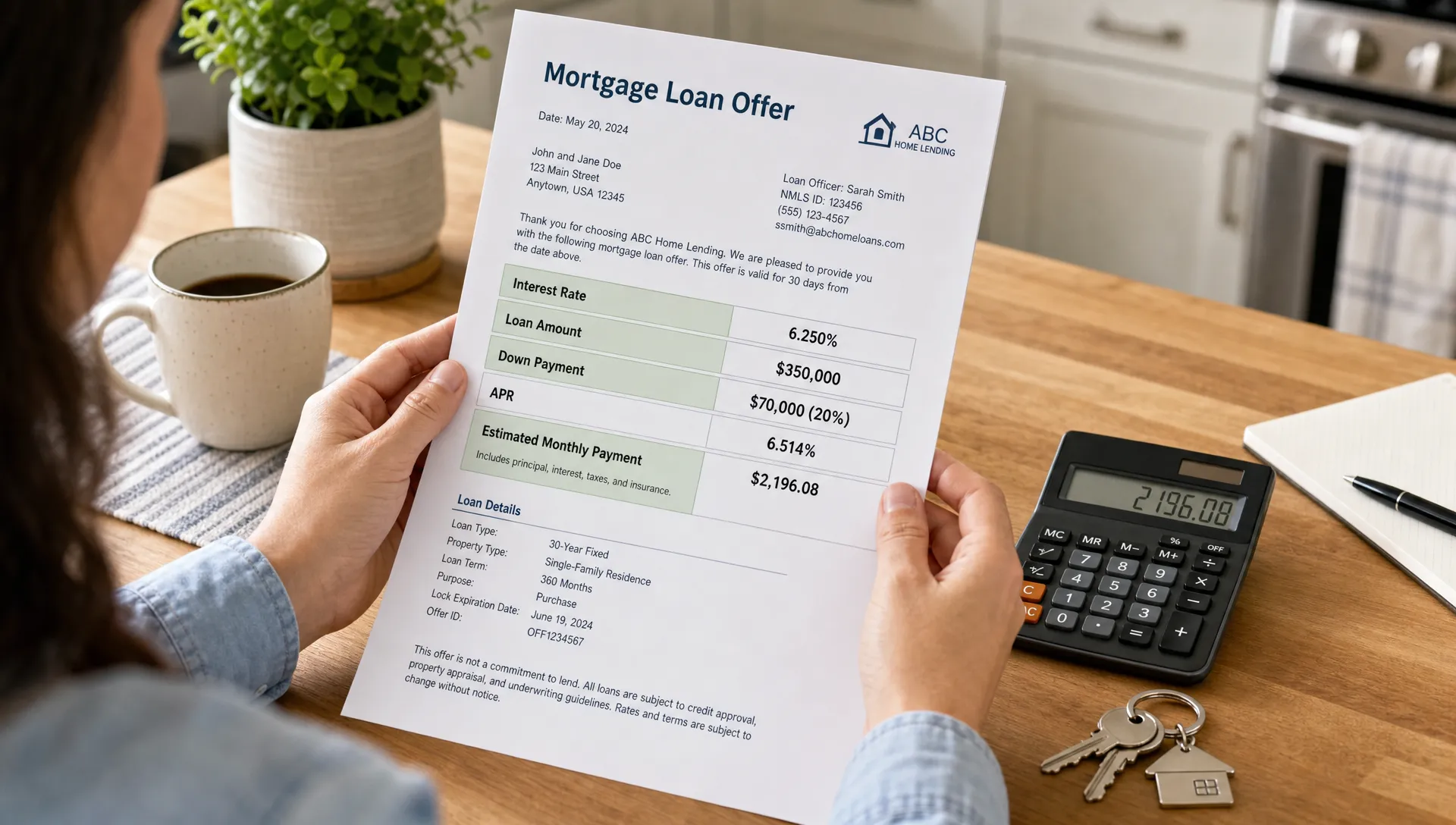

A mortgage offer can feel surprisingly specific. One borrower sees 6.50%, another sees 6.875%, and someone else gets quoted a different rate the next morning. If you are asking, “What changes my rate?” the short answer is this: mortgage pricing is built from both market conditions and the details of your loan file.

Your rate is not based on one factor alone. It is shaped by the broader bond market, your credit profile, your down payment or equity, the property, the loan program, the length of your rate lock, and the cost structure you choose. Understanding these moving parts helps you compare offers more confidently and avoid surprises before closing.

First, know whether your rate is quoted or locked

One of the biggest reasons a mortgage rate changes is timing. A rate quote is an estimate based on current pricing and the information available at that moment. A rate lock is a lender commitment, subject to the terms of the lock and the accuracy of your application details.

Until your rate is locked, it can move with the market. Mortgage rates often change daily, and sometimes more than once in a day when market volatility is high. That means a quote from Monday may not match pricing on Wednesday, even if nothing about your financial profile changed.

A rate lock can protect you from market movement for a set period, commonly 30, 45, or 60 days. Longer locks may cost more because the lender is taking on more market risk. The Consumer Financial Protection Bureau explains that borrowers should ask when the rate can be locked, how long the lock lasts, and whether any fees apply.

Even after a lock, your offer may still change if key facts change. For example, if your credit score is updated, your appraised value comes in lower than expected, or you switch from a primary residence to an investment property, the lender may need to reprice the loan.

Market conditions can change your rate before you lock

Mortgage rates are heavily influenced by the bond market, especially mortgage-backed securities and broader investor demand for long-term debt. Lenders update rate sheets as market conditions change.

A few common market forces include:

- Inflation expectations

- Federal Reserve policy expectations

- Treasury yield movement

- Mortgage-backed securities demand

- Economic reports on jobs, wages, and consumer prices

- Global financial uncertainty

The Federal Reserve does not directly set your mortgage rate, but its policy decisions can influence the financial markets that mortgage lenders watch. That is why rates may shift after major economic news, even if your application has not changed.

If you want a deeper look at the pricing chain behind lender rate sheets, New Era Lending’s guide on how home mortgage loan rates are priced explains how market forces, lender costs, borrower details, and product choices all come together.

Your credit score is one of the biggest borrower-level factors

Credit score matters because it helps lenders estimate risk. In general, higher credit scores tend to qualify for stronger pricing, while lower scores may lead to higher rates, higher fees, or a different loan program recommendation.

Mortgage lenders often use credit score tiers. A small change may not matter if you remain within the same tier, but crossing into a different tier can affect your rate or costs. For example, moving from one pricing band to another may change the lender’s adjustment to your offer.

Your score can also change during the process if new debt appears, balances increase, payments are missed, or a credit report is refreshed. That is why borrowers are often advised to avoid opening new accounts, financing large purchases, or running up credit cards before closing.

Credit is not the only factor, but it is one of the easiest to accidentally disrupt. If you are close to a stronger pricing tier, a mortgage professional may be able to help you understand whether paying down certain balances could improve your offer.

Debt-to-income ratio can raise or lower perceived risk

Your debt-to-income ratio, often called DTI, compares your monthly debt obligations with your qualifying income. Lenders use it to evaluate whether the proposed mortgage payment fits your financial picture.

DTI can affect your rate because a higher ratio may make the loan appear riskier. It can also affect which loan programs are available to you. In some cases, a loan may still be approvable, but pricing may not be as favorable as it would be with a lower DTI.

Monthly debts that can affect DTI include car payments, student loans, credit card minimum payments, personal loans, alimony or child support, and other mortgage obligations. New debt during the loan process can change your DTI and may change your approval terms.

This is especially important for business owners and self-employed borrowers. If you are considering a business investment, such as adding cash-flow equipment from a nationwide ATM machine provider, speak with your mortgage advisor before taking on new financing or changing your business cash flow. A smart business decision can still affect mortgage documentation, debt obligations, or qualifying income timing.

Down payment, equity, and loan-to-value ratio matter

Your down payment, or your available equity in a refinance, affects your loan-to-value ratio. LTV compares the loan amount with the property value. A lower LTV usually means the lender has more collateral protection, which can improve pricing.

For a home purchase, a larger down payment may help your offer by lowering the lender’s risk and possibly reducing or eliminating mortgage insurance. For a refinance, more equity may improve pricing and expand available options.

A lower-than-expected appraisal can change your rate because it increases the LTV. For example, if you expected to borrow 80% of the home’s value but the appraisal pushes the LTV to 85%, your pricing may change. You may also face mortgage insurance or different program requirements.

Down payment size should not be judged by rate alone. Keeping enough cash for reserves, repairs, moving expenses, and emergencies is also important. Sometimes the “best” rate is not the best overall financial structure if it leaves your budget too tight.

Loan program choice changes your rate structure

Different mortgage programs price risk differently. A conventional loan, FHA loan, VA loan, USDA loan, jumbo loan, fixed-rate mortgage, and adjustable-rate mortgage can all produce different offers for the same borrower.

Conventional loans often have pricing adjustments based on credit score, LTV, occupancy, property type, and other details. FHA loans may be more accessible for some borrowers but include mortgage insurance costs. VA loans are designed for eligible veterans, service members, and surviving spouses, and they have their own pricing considerations, including the VA funding fee when applicable. Jumbo loans may have stricter requirements because they exceed conforming loan limits.

This is why comparing rate quotes without comparing the program can be misleading. A lower interest rate may come with higher upfront costs, mortgage insurance, or a different long-term payment structure.

If you are eligible for a VA loan, the factors can be a little different. New Era Lending’s article on rates for VA loans and what changes your offer covers those program-specific details in plain English.

Property type and occupancy can affect pricing

The home itself matters. Lenders price a primary residence differently from a second home or investment property because the risk profile is different. Borrowers are statistically more likely to prioritize payments on the home they live in, so primary residences often receive better pricing than investment properties.

Property type can also affect your offer. A single-family home may price differently from a condo, multi-unit property, manufactured home, or property with unusual characteristics. Condos may require additional project review. Multi-unit properties may involve rental income analysis. Investment properties may require stronger reserves or larger down payments.

Occupancy must be accurate. If the application says the home will be your primary residence, but the transaction later changes to an investment property, your rate and approval terms can change significantly.

Loan amount, term, and rate type can move your offer

The structure of the loan itself also changes pricing. A 30-year fixed mortgage usually does not price the same as a 15-year fixed mortgage. Shorter terms often carry lower rates, but higher monthly payments because the balance is repaid faster.

Adjustable-rate mortgages may start with a lower initial rate than a fixed-rate loan, depending on the market, but the rate can adjust later according to the loan terms. Fixed-rate loans offer payment stability for principal and interest, which many borrowers value even if the initial rate is higher.

Loan amount can also matter. Very small loans, high-balance loans, and jumbo loans may price differently because of investor requirements and lender costs. Conforming loan limits can influence which investor rules apply.

When reviewing an offer, do not isolate the interest rate from the payment, fees, and term. A slightly higher rate on a lower-cost loan may be better than a lower rate that requires expensive points if you do not plan to keep the mortgage long enough to break even.

Discount points and lender credits can make the same loan look different

Two mortgage offers can show different rates because they are built with different cost choices. Discount points are upfront costs paid to lower the interest rate. Lender credits work in the opposite direction: you may accept a higher rate in exchange for help offsetting closing costs.

This is why “What is my rate?” should usually be followed by “What does that rate cost?” A 6.50% rate with points is not the same as a 6.75% rate with no points, and neither is automatically better without knowing your cash position, time horizon, and break-even point.

APR can help you compare the broader cost of credit because it includes certain loan costs, but APR is not perfect. It assumes you keep the loan for the full term and may not reflect your real plan if you expect to sell or refinance sooner.

For a deeper comparison framework, see New Era Lending’s guide on how to compare new mortgage rate offers today. It walks through rate, APR, points, fees, loan terms, and total cost.

Documentation and income changes can affect the final offer

A mortgage offer is based on verified information. If the lender receives updated documents that change your qualifying income, assets, employment status, or debts, your offer may need to be updated.

Common documentation-related changes include:

- A pay stub showing lower variable income than expected

- Tax returns showing different self-employed income than estimated

- Bank statements revealing insufficient reserves or large unexplained deposits

- A new credit account appearing before closing

- Employment changes during underwriting

- Updated insurance, tax, or HOA information affecting the payment

These changes do not always mean your loan is in trouble. Sometimes they simply require clarification. But when they affect qualifying risk, LTV, DTI, or program eligibility, they can also affect your rate or costs.

The best approach is to be transparent early. Tell your lender about income complexity, property details, credit events, large deposits, or planned financial moves before they become last-minute underwriting issues.

Rate lock length and closing timeline can change pricing

The length of your lock matters. A 15-day lock, 30-day lock, and 60-day lock may not have the same pricing. Longer locks can cost more because the lender must protect the rate for more time.

If closing is delayed and your lock expires, you may need a lock extension. Depending on the lender and market conditions, that extension may come with a cost. If rates have improved, you may wonder whether you can get the better rate, but lock policies vary.

To reduce lock-related surprises, ask these questions before you commit:

- When can my rate be locked?

- How long is the lock period?

- What happens if closing is delayed?

- Is there a cost to extend the lock?

- Can the rate change if my loan details change?

These questions are practical, not pushy. A transparent lender should be able to explain the lock policy in plain language.

Why your neighbor’s rate may be different from yours

It is tempting to compare your rate with a friend, coworker, or neighbor. But mortgage offers are rarely apples to apples unless every major detail is the same.

Your neighbor’s rate may differ because they applied on a different day, locked at a different time, bought points, used a different program, had a different credit score, made a larger down payment, borrowed a different amount, or purchased a different property type. Even the same lender can quote different rates for two borrowers because their risk profiles and loan structures are different.

Instead of chasing someone else’s number, compare complete Loan Estimates. Look at the interest rate, APR, monthly payment, closing costs, points, lender credits, mortgage insurance, escrow assumptions, and cash to close. The strongest offer is the one that fits your full financial picture, not just the lowest advertised rate.

How to keep your mortgage rate from changing unexpectedly

You cannot control the market, but you can reduce avoidable changes. Start by giving your lender accurate information upfront. Estimate your income conservatively if it includes bonuses, commissions, overtime, or self-employment earnings. Be clear about the property type, occupancy, down payment source, and timing.

Once you are under contract or actively refinancing, avoid major financial changes unless your lender confirms they are safe. Do not open new credit, co-sign a loan, change jobs, move large sums without documentation, or make large purchases without guidance.

Most importantly, ask for a clear explanation of what could change your offer. A good mortgage conversation should not leave you guessing. The more you understand the variables, the easier it is to choose between locking now, adjusting the loan structure, paying points, or preserving cash.

Frequently Asked Questions

Can my mortgage rate change after I receive a Loan Estimate? Yes. A Loan Estimate is based on the information available when it is issued. Your rate may change if it was not locked, if market pricing moves, or if important loan details change, such as credit score, loan amount, appraised value, occupancy, or program type.

What changes my rate the most? The biggest factors are usually market conditions, credit score, loan-to-value ratio, loan program, occupancy, property type, points or credits, and lock length. The exact impact depends on the lender’s pricing and investor guidelines.

Does a bigger down payment always get me a lower rate? Not always, but it can help. A larger down payment may lower your LTV and reduce lender risk. However, the benefit depends on your credit score, loan program, property type, and whether the extra cash would be better kept for reserves or closing costs.

Can buying points lower my mortgage rate? Yes. Discount points are upfront fees paid to reduce the interest rate. Whether points make sense depends on the cost, the monthly savings, and how long you expect to keep the loan.

Why did my rate change after the appraisal? If the appraisal comes in lower than expected, your LTV may increase. That can change pricing, mortgage insurance, or even loan eligibility. If the value supports the original numbers, the appraisal may have little or no effect on the rate.

Should I lock my rate right away? It depends on your timeline, risk tolerance, and market conditions. If the payment works for your budget and you are comfortable with the terms, locking can protect you from rate increases. If you wait, the rate could improve or get worse.

Get a clearer mortgage offer before you decide

Your mortgage rate is not random. It changes when the market moves, when your loan details change, or when you choose a different cost structure. The best way to protect yourself is to compare complete offers, understand the assumptions behind the quote, and work with a lender that explains the tradeoffs clearly.

New Era Lending combines smart mortgage technology with personalized human guidance to help borrowers purchase, refinance, or access home equity with more confidence. If you want to understand what is driving your offer, start by reviewing your options with a team that can explain the numbers in plain English.