.jpg)

.jpg)

.jpg)

How Home Mortgage Loan Rates Are Priced

Two borrowers can call the same lender on the same morning and receive different mortgage rate quotes. That does not always mean one person is getting a bad deal. It usually means the loan is being priced around different risks, costs, and choices.

A home mortgage loan rate is not just “today’s rate.” It is a custom price built from market conditions, lender costs, loan type, borrower profile, property details, lock timing, and decisions like whether to pay discount points or use lender credits. Once you understand those layers, rate quotes become much easier to compare.

The short version: mortgage rates price risk, time, and tradeoffs

Mortgage rates are priced around a simple idea: the lender and the investors behind the loan need to be compensated for lending money over time. The more risk, uncertainty, or cost built into the loan scenario, the more pricing can change.

When a loan officer quotes a mortgage rate, the quote usually reflects four major layers:

- The broader interest rate market, especially mortgage-backed securities and investor demand

- The lender’s own costs, profit margin, servicing strategy, and available investor outlets

- Your loan details, including credit profile, down payment, property type, occupancy, and loan program

- Your pricing choice, such as paying points for a lower rate or accepting a lender credit for higher upfront savings

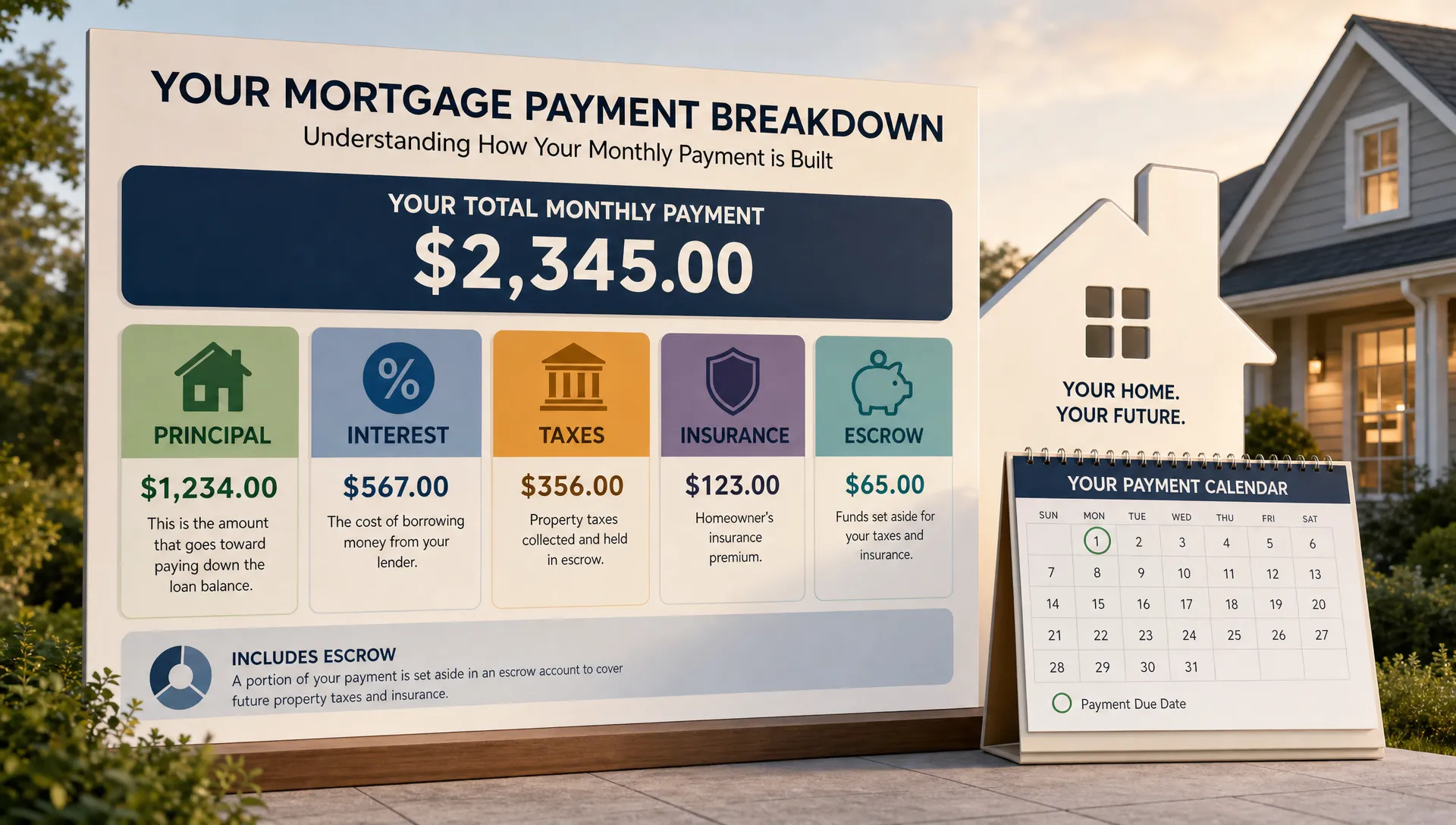

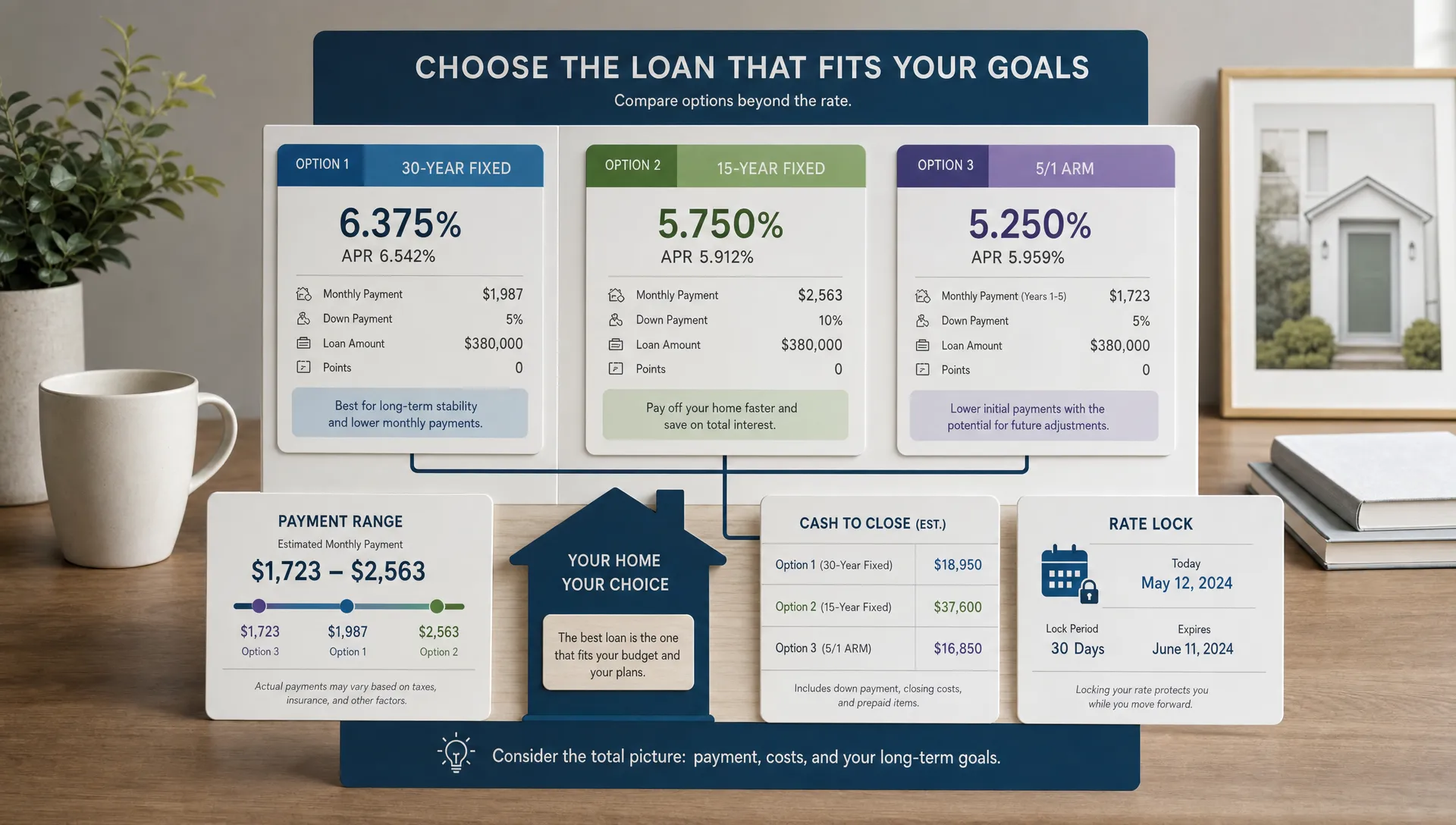

That is why the lowest advertised rate is not always the best real-world option. A rate only makes sense when you understand the loan amount, fees, points, APR, monthly payment, cash to close, and how long you expect to keep the loan.

Layer 1: the mortgage market sets the starting point

Most home mortgage loan rates begin with the broader bond market. Many mortgages are packaged into mortgage-backed securities, often called MBS. Investors buy those securities and expect a return based on inflation expectations, economic data, Treasury yields, prepayment risk, and overall market uncertainty.

This is why mortgage rates often move when reports come out about inflation, jobs, consumer spending, or Federal Reserve policy expectations. The Federal Reserve does not directly set 30-year fixed mortgage rates, but Fed policy can influence the market conditions that affect them.

For a useful market benchmark, many borrowers follow the Freddie Mac Primary Mortgage Market Survey, which tracks average weekly mortgage rates. Just remember that averages are not personalized quotes. Your actual rate can be higher or lower depending on your loan scenario.

Rates can also move quickly. In volatile markets, lenders may update rate sheets during the day. A quote from Monday morning may not be available Tuesday afternoon, and sometimes it may not even be available later the same day unless it was locked.

Layer 2: the lender turns market prices into a rate sheet

Lenders do not simply copy a national average and offer it to every borrower. They create rate sheets, which show how different interest rates are priced for different loan scenarios.

A rate sheet connects the interest rate to a cost or credit. For example, one rate may be available with no discount points, a slightly lower rate may require upfront points, and a slightly higher rate may provide a lender credit toward closing costs.

This is where borrowers often get confused. A “lower rate” might actually cost more at closing. A “higher rate” might be intentional because it reduces cash needed upfront. Neither choice is automatically right or wrong.

Lender pricing can also reflect:

- Operational costs and compensation structure

- Investor relationships and available loan channels

- Servicing value, meaning whether the lender expects to keep or sell servicing rights

- Risk tolerance for certain property types, credit profiles, or loan programs

- Rate lock duration, since longer locks expose the lender to more market risk

This is one reason two lenders may quote different rates for the same borrower on the same day. They may be using different investors, margins, lock policies, or cost structures.

Layer 3: your borrower profile changes the final price

After the market and lender set the starting point, your personal loan scenario determines how the rate is adjusted. Mortgage pricing is risk-based. The lender is asking, “How likely is this loan to perform as expected, and how easy would it be to recover the balance if something goes wrong?”

Credit profile

Your credit score is one of the best-known pricing factors. In general, stronger credit can qualify you for better pricing because it signals lower repayment risk. Credit history also matters. Late payments, collections, high revolving balances, or recent major credit events can affect eligibility, not just pricing.

It is important to separate credit score from full credit profile. Two borrowers with the same score may still be priced differently if one has thin credit, a recent delinquency, or a much higher debt load.

Down payment, equity, and loan-to-value ratio

Loan-to-value ratio, or LTV, compares the loan amount to the property value. A lower LTV generally means the borrower has more equity in the home, which can reduce lender risk.

For purchases, your down payment drives LTV. For refinances, your current equity and appraised value drive LTV. A borrower putting 20% down may receive different pricing than a borrower putting 3% or 5% down, and mortgage insurance may also come into play.

That said, putting more down is not always the best financial move if it drains your emergency fund. The better question is how each down payment level affects rate, mortgage insurance, cash to close, monthly payment, and post-closing reserves.

Loan program

Different mortgage programs are priced differently. Conventional, FHA, VA, USDA, jumbo, investment property, renovation, and non-QM loans all have different rules, risk profiles, and cost structures.

Government-backed loans may have competitive rates, but they can also include program-specific costs such as mortgage insurance premiums, guarantee fees, or funding fees. Conventional loans may be more sensitive to credit score, LTV, property type, and occupancy. Jumbo loans often have stricter underwriting and may price differently because they are not sold through the same standard agency channels.

The “best rate” is not always found in the same program for every borrower. A veteran eligible for a VA loan, a first-time buyer with limited down payment, and a self-employed borrower with complex income may each need a different pricing strategy.

Property type and occupancy

A primary residence is usually priced more favorably than a second home or investment property because borrowers are statistically more likely to prioritize payments on the home they live in.

Property type can also affect pricing. Single-family homes, condos, manufactured homes, multi-unit properties, and mixed-use properties may be priced differently. Some property types require additional reviews, warranties, or underwriting steps, which can affect both pricing and timeline.

Loan purpose and loan size

Purchase loans, rate-and-term refinances, cash-out refinances, and home equity loans can all price differently. Cash-out refinances often carry higher pricing because the borrower is increasing the loan balance and reducing equity.

Loan size can matter too. Very small loans may have pricing challenges because fixed lender costs are spread across a smaller balance. Very large loans may fall into jumbo territory or require more reserves, stronger credit, and more documentation.

Lock period

A rate quote is not fully secured until it is locked. A rate lock protects you from market movement for a defined period, such as 30, 45, or 60 days. Longer locks usually cost more because they require the lender to hold pricing for a longer time.

If your closing timeline is uncertain, choosing the cheapest short lock can backfire. If the lock expires, you may need an extension, and extensions can come with a cost. The right lock period should match the realistic timeline for appraisal, underwriting, title work, and closing.

Layer 4: points and lender credits shape the quote you choose

Once the loan is priced, you may have choices. The most common are discount points and lender credits.

A discount point is prepaid interest. One point equals 1% of the loan amount. Paying points can lower the interest rate, but it increases upfront cost. A lender credit works in the opposite direction. You accept a higher rate, and the lender gives you a credit that can reduce closing costs.

Here is a simple example. Suppose paying $3,000 in points lowers your payment by $60 per month. Your rough break-even point is 50 months. If you expect to keep the loan longer than that, the lower rate may be worth considering. If you plan to sell or refinance sooner, keeping the cash may make more sense.

This is why pricing should fit your life, not just your rate preference. After closing, you may still need money for movers, repairs, furniture, appliances, school expenses, or local services if you are settling into a new community, from utility setup to booking a haircut or color appointment at Kingdom Cute Hair Salon in Warner Robins, GA. A lower rate is helpful, but not if it leaves you cash-poor at the wrong time.

If you want a deeper breakdown of how points affect total cost, read New Era Lending’s guide to APR, points, and amortization.

Why advertised mortgage rates can be misleading

Advertised rates are often based on ideal or specific assumptions. They may assume a certain credit score, down payment, loan amount, property type, occupancy, purchase price, location, and discount point cost.

That does not mean the advertisement is automatically wrong. It means the rate may not apply to your situation.

Before comparing an advertised rate to a personalized quote, ask:

- What credit score and down payment does this assume?

- Is this for a primary residence, second home, or investment property?

- Does the rate include discount points?

- What loan amount and loan program does it assume?

- How long is the lock period?

- What fees are included or excluded?

A rate without those details is incomplete. A lender can quote a very attractive rate by adding points, shortening the lock period, or assuming a borrower profile that may not match yours.

Interest rate vs APR: why both matter

Your interest rate is the note rate used to calculate principal and interest payments. APR, or annual percentage rate, is designed to show a broader cost of borrowing by including certain finance charges.

APR can be useful because it helps reveal whether a low rate comes with higher upfront costs. However, APR is not perfect. It depends on assumptions about how long you keep the loan, and it may not capture every cost that matters to your budget.

The most reliable way to compare offers is to review the standardized Loan Estimate. The Consumer Financial Protection Bureau explains the Loan Estimate as a form that helps borrowers understand key loan terms, projected payments, closing costs, and cash to close.

When comparing Loan Estimates, focus on the same scenario. Same loan amount, same program, same lock period, same down payment, and same point structure. If one quote includes points and the other does not, you are not comparing equal offers.

How lenders may price the same loan differently

Even when the borrower, property, and loan program are identical, lenders may quote different rates. That can happen for several legitimate reasons.

One lender may have a better investor outlet for that exact loan type. Another may have a lower margin but higher fees. Another may be pricing aggressively to win business in a certain market. Another may have a longer standard lock period built into the quote.

This is why you should compare the full package:

- Interest rate

- APR

- Discount points or lender credits

- Origination and lender fees

- Estimated third-party closing costs

- Monthly payment

- Cash to close

- Lock period

- Underwriting and closing timeline

The lowest rate is not always the strongest offer if it comes with high fees, unrealistic timing, or poor communication. In a competitive purchase situation, a lender’s ability to close on time can matter nearly as much as the interest rate.

What you can control before your rate is priced

You cannot control the bond market or lender rate sheets, but you can influence many parts of your pricing profile.

Start with credit. Review your credit reports early, dispute clear errors, avoid new unnecessary debt, and try to reduce high credit card balances before applying. Revolving utilization can affect credit scores, and even a modest score improvement may change available pricing.

Next, review your debt-to-income ratio. DTI may not always directly change the rate, but it affects approval strength and program options. Paying down or restructuring certain debts before applying may help you qualify for a better loan path.

Then compare down payment scenarios. Sometimes adding a little more down can improve pricing or reduce mortgage insurance. Other times, the improvement is small and keeping cash reserves is smarter. You will not know until you model both options.

Finally, be clear about your timeline. If you are buying soon, a strong pre-approval and realistic lock plan can help. If you are months away, your best move may be preparation rather than chasing daily rate changes.

For more practical strategies, see New Era Lending’s article on how to lower rates without hurting your budget.

A simple process for comparing home mortgage loan rates

The goal is not to find the lowest number on a website. The goal is to find the best-priced loan for your actual financial situation.

Use this process when comparing quotes:

- Define the exact loan scenario you want quoted, including loan amount, down payment, property type, occupancy, program, and lock period.

- Ask each lender for quotes on the same day when possible, because market pricing can change quickly.

- Request a no-points option first, then ask for a points option only if you want to evaluate the break-even.

- Compare Loan Estimates instead of relying only on verbal quotes or screenshots.

- Decide based on total cost, monthly payment, cash to close, confidence in closing, and how long you expect to keep the loan.

This approach makes rate shopping more accurate and less stressful. It also helps you avoid choosing a loan that looks cheap upfront but costs more over time.

Frequently Asked Questions

Are home mortgage loan rates based only on credit score? No. Credit score is important, but lenders also consider loan program, LTV, property type, occupancy, loan amount, lock period, points, and broader market conditions.

Does the Federal Reserve set mortgage rates? Not directly. The Fed sets short-term policy rates, which can influence financial markets. Mortgage rates are more closely tied to mortgage-backed securities, investor demand, inflation expectations, and bond market movement.

Why is my APR higher than my interest rate? APR includes certain loan costs in addition to the interest rate, so it is often higher than the note rate. A large gap between rate and APR can indicate higher upfront costs or points.

Are discount points worth paying? Points may be worth it if the monthly savings exceed the upfront cost over the time you keep the loan. If you plan to sell or refinance soon, points may not provide enough time to break even.

Can my quoted mortgage rate change? Yes, unless it is locked. Mortgage rates can change with the market, and your final pricing can also change if loan details change, such as credit score, property type, appraised value, loan amount, or lock period.

Why did another borrower get a lower rate than I did? Their loan may have had a different credit score, down payment, loan size, property type, occupancy, program, lock period, or points. Mortgage rates are personalized, so comparisons only help when the loan scenarios are the same.

Get a mortgage rate quote based on your real scenario

Understanding how rates are priced helps you ask better questions, but personalized numbers matter most. New Era Lending combines smart mortgage technology with human guidance to help borrowers compare purchase, refinance, and equity-access options with clearer terms and a simpler process.

If you want to see how your rate could be priced based on your credit profile, down payment, loan type, and goals, connect with New Era Lending to review personalized mortgage scenarios before you lock.