.jpg)

.jpg)

.jpg)

Loan Terms Explained: APR, Points, and Amortization

Most borrowers know to ask, “What’s the interest rate?” Fewer know the follow-up questions that actually protect your wallet: “What’s the APR?”, “Are there points?”, and “How does the amortization work?”

These three loan terms shape (1) your monthly payment, (2) your cash needed at closing, and (3) your total cost over time. Once you understand them, comparing lenders gets a lot easier, and you’re far less likely to be surprised by fees or long-term interest.

Why these loan terms matter (even if you already have a great rate)

A mortgage is a bundle of decisions, not a single number.

- Interest rate heavily influences your monthly principal and interest payment.

- APR estimates the loan’s “all-in” cost when you include certain fees.

- Points are upfront costs (or credits) that change your rate and cash-to-close.

- Amortization determines how your payment is split between interest and principal over time (and how quickly your balance falls).

In real life, two lenders can offer the same interest rate but very different APRs because of fees. Or one lender can show a slightly higher rate but lower total cost because the fees (or points) are different.

If you’re shopping for a purchase loan, refinance, or cash-out option, these are the terms that help you compare offers apples-to-apples.

APR explained (and what it does better than “rate”)

APR (Annual Percentage Rate) is a standardized estimate of borrowing cost that includes:

- Your interest rate, and

- Certain finance charges (often including some lender fees and points)

Because it rolls interest plus specific costs into one number, APR is designed to help you compare loans that have different fee structures.

The CFPB’s plain-English overview is helpful if you want a regulator’s definition of what APR is and how it’s used: CFPB explanation of APR.

Interest rate vs APR: the simplest way to think about it

- Interest rate answers: “What percentage does the lender charge on the amount I borrow?”

- APR answers: “If I spread certain upfront costs over the life of the loan, what’s the approximate yearly cost?”

It’s common for APR to be higher than the interest rate because it includes finance charges.

What APR usually includes (and what it often does not)

APR commonly includes:

- Discount points (if you pay points)

- Some underwriting or processing type lender fees

- Certain prepaid finance charges tied directly to the loan

APR often does not include:

- Your homeowner’s insurance premium

- Your property taxes

- Many “third-party” costs (depending on how they’re categorized)

That’s why APR is powerful, but not perfect. You should still review the Loan Estimate line by line for real cash-to-close.

When APR is most useful

APR is especially useful when you’re comparing:

- Two fixed-rate loans with the same term length (example: 30-year fixed vs 30-year fixed)

- Offers where one lender charges higher fees but advertises a lower rate

When APR can be less helpful

APR can be less apples-to-apples when:

- You’re comparing different structures (example: ARM vs fixed, or 15-year vs 30-year)

- You know you’ll keep the loan for a short time (because APR assumes a long time horizon)

- One option includes large lender credits or points, and the time horizon is uncertain

In those cases, you still look at APR, but you also do break-even math and review the payment risk.

If you’re comparing loan structures (fixed vs ARM vs buydowns), you may also like: Mortgage Options Compared: Fixed vs ARM vs Buydowns.

Points explained (discount points, and “negative points” lender credits)

Points are a pricing tool that lets you trade upfront cost for interest rate.

What is a point?

- 1 point = 1% of the loan amount.

- On a $400,000 loan, 1 point costs $4,000.

Points often show up on the Loan Estimate as “Discount Points” (a charge). Sometimes you’ll also see the opposite: a lender credit (a credit) where you accept a higher rate in exchange for the lender paying some of your closing costs.

Discount points: paying more now to pay less later

Discount points are usually used to:

- Reduce the interest rate

- Lower the monthly principal and interest payment

- Potentially reduce total interest over the life of the loan

Whether that’s a good deal depends mainly on how long you’ll keep the mortgage.

Lender credits (sometimes called “negative points”)

A lender credit is basically the reverse trade:

- You accept a slightly higher rate

- The lender provides a credit to offset closing costs

This can be useful when you want to minimize cash-to-close, or when you think you’ll refinance or sell before “paying back” the higher rate.

The break-even test: how to know if points make sense

A simple break-even calculation is:

Break-even months = upfront cost of points / monthly payment savings

Example (hypothetical numbers for illustration):

- Option A: No points, payment is $2,528 (principal and interest only)

- Option B: Pay $4,000 in points, payment drops to $2,468

- Monthly savings: $60

Break-even months = $4,000 / $60 = about 67 months, or about 5.5 years

If you expect to keep the loan longer than about 5.5 years, points may make sense. If you’re likely to refinance, move, or pay the loan off sooner, paying points can be a costly bet.

A note on taxes

Mortgage interest and points can have tax implications, but the rules vary by scenario (purchase vs refinance) and by your filing situation. It’s best to confirm with a tax professional rather than assuming points will be fully deductible in the year you pay them.

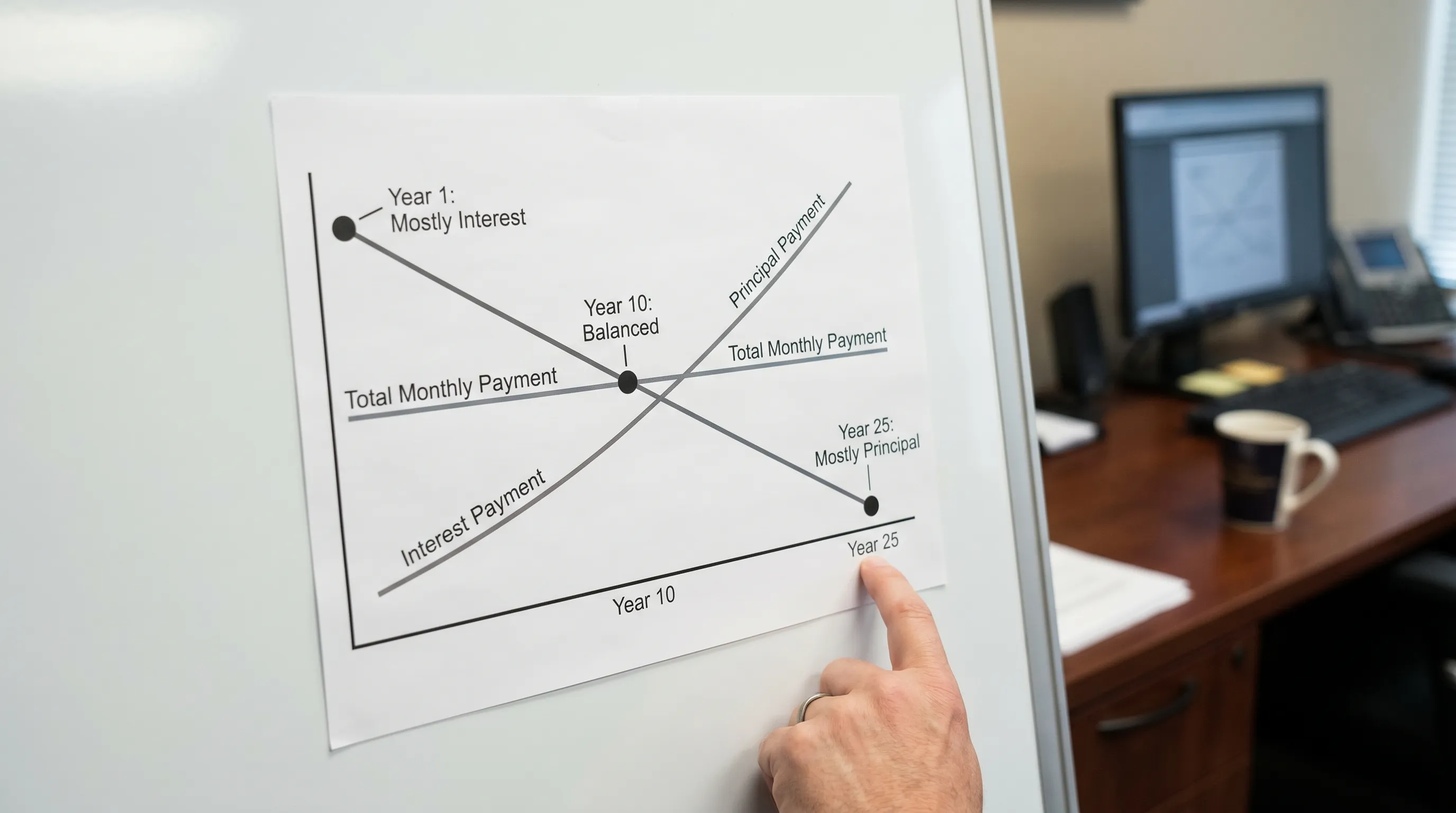

Amortization explained (the part most people feel, month after month)

Amortization is the schedule that shows how your monthly payment pays down the loan balance over time.

With a typical fixed-rate mortgage, the payment is designed so you pay the loan off by the end of the term (for example, 30 years). The key is that the payment is split differently over time:

- Early years: more of your payment goes to interest

- Later years: more of your payment goes to principal

A simple example of amortization

Assume a $400,000 loan.

- At 6.50% on a 30-year term, the principal and interest payment is roughly $2,528/month.

- The first month’s interest is roughly $400,000 x 6.50% / 12 = $2,167.

- That means only about $361 goes to principal in month one.

You are not doing anything wrong if it feels like the balance drops slowly at first. That’s how amortization works.

30-year vs 15-year amortization (why term changes everything)

Shorter terms usually mean:

- Higher monthly payment

- Much faster principal paydown

- Less total interest over the life of the loan

For the same $400,000, a 15-year payment can be meaningfully higher, but a much larger share goes to principal right away.

How to use amortization to your advantage

Amortization is not just a math concept, it’s a planning tool.

- If your goal is lowest payment, longer amortization can help (but costs more in interest).

- If your goal is paying off faster, shorter amortization or strategic extra principal can help.

- If your goal is flexibility, you may choose a payment you can comfortably afford, then make extra payments when cash flow allows.

Always confirm whether your loan has a prepayment penalty (many consumer mortgages do not, but it should still be checked).

How to compare Loan Estimates using APR, points, and amortization (without getting overwhelmed)

When you receive Loan Estimates from different lenders, don’t compare marketing promises. Compare the disclosures.

For a deeper dive on understanding fees specifically, see: Closing Costs: The Fees Nobody Tells You About.

Align the scenario first

Before you compare anything, make sure both quotes assume:

- The same loan amount

- The same term (30-year vs 15-year)

- The same rate type (fixed vs ARM)

- The same credit and down payment assumptions

Otherwise, you’re not comparing pricing, you’re comparing two different loans.

Use a “triangle” view: payment, cash-to-close, and total cost

A good comparison looks at all three:

- Monthly payment (principal and interest): what you feel every month

- Cash to close: what you must bring to closing (or roll in)

- APR and finance charges: what you pay over time

It’s normal for one offer to win on payment while another wins on cash-to-close.

Identify points and credits quickly

On the Loan Estimate, look for:

- “Discount Points” (cost)

- “Lender Credits” (credit)

Then do a quick break-even estimate based on the payment difference.

Sanity-check the amortization effect

Two offers can have the same APR but different long-term outcomes if:

- The term length is different, or

- One option is interest-only or otherwise structured differently (less common for standard qualified mortgages)

Ask your lender to show you how much principal you’ll have paid after 5 years, and how much total interest you’d pay if you kept the loan for your expected time horizon.

Common misunderstandings (that cost borrowers real money)

“The lowest rate is always the best deal.”

Not necessarily. A lower rate can be paired with higher fees or points. If you won’t keep the loan long enough, you might never recoup the upfront cost.

“APR includes every cost of homeownership.”

No. Taxes, insurance, HOA dues, maintenance, and many third-party charges are not rolled into APR. APR is still very useful, but it is not a full housing budget.

“Points are a scam.”

Points are a tradeoff, not automatically good or bad. They can be smart when your time horizon is long and cash flow supports the upfront cost.

“Amortization means I’m stuck.”

Amortization is the default schedule, but you can often influence outcomes with:

- Extra principal payments (when it makes sense for your overall finances)

- Refinancing if rates or goals change

If you’re considering refinancing in 2026 and want to think in break-even terms, this guide may help: Refinance Rates for Mortgages: When to Refi in 2026.

A quick mini-glossary of related loan terms

Loan Estimate (LE): The standardized form lenders provide early in the process showing your projected rate, payment, closing costs, and APR.

Closing costs: One-time costs to originate and close the loan (lender fees plus third-party items like title services). Some are negotiable, some are not.

Origination charges: Lender charges for making the loan, often where points and underwriting/processing fees appear.

Principal and interest (P&I): The portion of the payment that repays the loan balance (principal) and the cost of borrowing (interest). This excludes taxes and insurance.

Escrow: An account used to collect taxes and insurance as part of your monthly payment, then pay those bills when due.

One practical tip: use the same “transparent pricing” standard everywhere

Mortgage shopping gets easier when you expect clear, itemized pricing and timelines from every professional you hire, not just your lender. If you run a small business and you’re ever comparing proposals for services like local SEO or website work, the same principle applies: ask what’s included, what’s optional, and what changes the price. Agencies like Sleek Web Designs stand out by laying out scope and process clearly, which is exactly the mindset you want when reviewing Loan Estimates.

Frequently Asked Questions

Is APR the same as the interest rate? No. The interest rate is the cost of borrowing the principal. APR includes the interest rate plus certain finance charges (like points and some lender fees), expressed as a yearly rate.

Should I pay points to lower my mortgage rate? It depends on your time horizon and cash-to-close. Points can make sense when you expect to keep the loan long enough to break even, and when paying upfront does not drain your reserves.

Can two loans have the same interest rate but different APR? Yes. If lender fees, points, or credits differ, APR can differ even when the note rate is the same.

Why does my mortgage balance drop so slowly at first? Because of amortization. Early in the loan, a larger share of your payment goes to interest, and the principal portion grows over time.

What should I look at first on a Loan Estimate? Start with the loan type, interest rate, and monthly payment, then review origination charges (including points), lender credits, cash-to-close, and APR to understand the full cost tradeoffs.

Ready to compare offers with confidence?

If you’re looking at a purchase, refinance, or equity access scenario and want help translating APR, points, and amortization into a clear decision, New Era Lending can walk you through side-by-side options with transparent terms and a modern process.

Explore your next steps at New Era Lending and get guidance that combines smart tools with real human support.