.jpg)

.jpg)

.jpg)

How a Home Mortgage Loan Works From Start to Close

A home mortgage loan can feel complicated because several things happen at once: your finances are reviewed, the property is evaluated, title is checked, the rate is locked, documents are prepared, and funds move between multiple parties. But when you understand what each step is meant to prove, the process becomes much easier to follow.

At its core, a mortgage is a loan secured by real estate. You agree to repay the money over time, and the lender uses the home as collateral. From start to close, the lender is answering three big questions: can you repay the loan, is the property acceptable collateral, and are all legal documents ready for a clean transfer or refinance?

Below is a plain-English walkthrough of how the mortgage journey works, what happens behind the scenes, and how to keep your file moving toward closing with fewer surprises.

What a Home Mortgage Loan Actually Does

A mortgage loan is more than a monthly payment. It is a legal and financial structure that connects the borrower, lender, property, seller, title company, appraiser, insurance provider, and closing agent.

When you buy a home, the lender provides funds at closing so the seller can be paid. In exchange, you sign a promissory note agreeing to repay the debt and a mortgage or deed of trust that gives the lender a security interest in the property. If you refinance, the new loan usually pays off the existing mortgage and replaces it with new terms.

Your monthly payment may include principal, interest, property taxes, homeowners insurance, mortgage insurance, and sometimes homeowners association dues. The exact structure depends on your loan program, down payment, property type, and whether you use an escrow account.

The important thing to remember is this: a mortgage is approved in layers. Your personal qualifications matter, but the home itself must also meet lender and program requirements.

Step 1: Start With Your Budget and Buying Goal

Before you apply, clarify what you want the loan to accomplish. Are you buying your first home, upgrading, relocating, refinancing, or accessing equity? The answer affects which loan programs make sense and what documents you will need.

For a purchase, the most useful starting point is not the maximum price you could technically qualify for. It is the monthly payment and cash-to-close amount you can comfortably handle. Cash to close usually includes your down payment, closing costs, prepaid taxes and insurance, and any required reserves.

Your home search should also consider lifestyle factors that affect how long you may keep the property. Commute, future family plans, schools, and neighborhood stability can all influence whether a fixed-rate loan, adjustable-rate mortgage, or buydown strategy fits best. Families making a major relocation often research community resources early, including school admissions and local education options such as Colegio Bilingüe en Chicureo when evaluating a move abroad.

If you are still getting familiar with basic mortgage numbers, New Era Lending’s guide to home loan basics every buyer should know is a helpful companion resource.

Step 2: Get Pre-Approved Before You Shop Seriously

Pre-approval is the first major checkpoint. It tells you how much financing you may qualify for based on a review of your credit, income, assets, debts, and overall financial profile.

A strong pre-approval is different from a quick estimate. A quick estimate may rely on self-reported information. A real pre-approval typically requires documentation such as pay stubs, W-2s, tax returns if applicable, bank statements, identification, and permission to review credit.

Pre-approval helps in three ways. First, it gives you a more realistic price range. Second, it helps identify issues early, such as debt-to-income concerns, documentation gaps, or credit items that need explanation. Third, it can strengthen your offer because sellers want confidence that the buyer can close.

During this stage, avoid making major financial changes. Opening new credit, financing a car, changing jobs, moving large unexplained deposits, or increasing credit card balances can affect approval later.

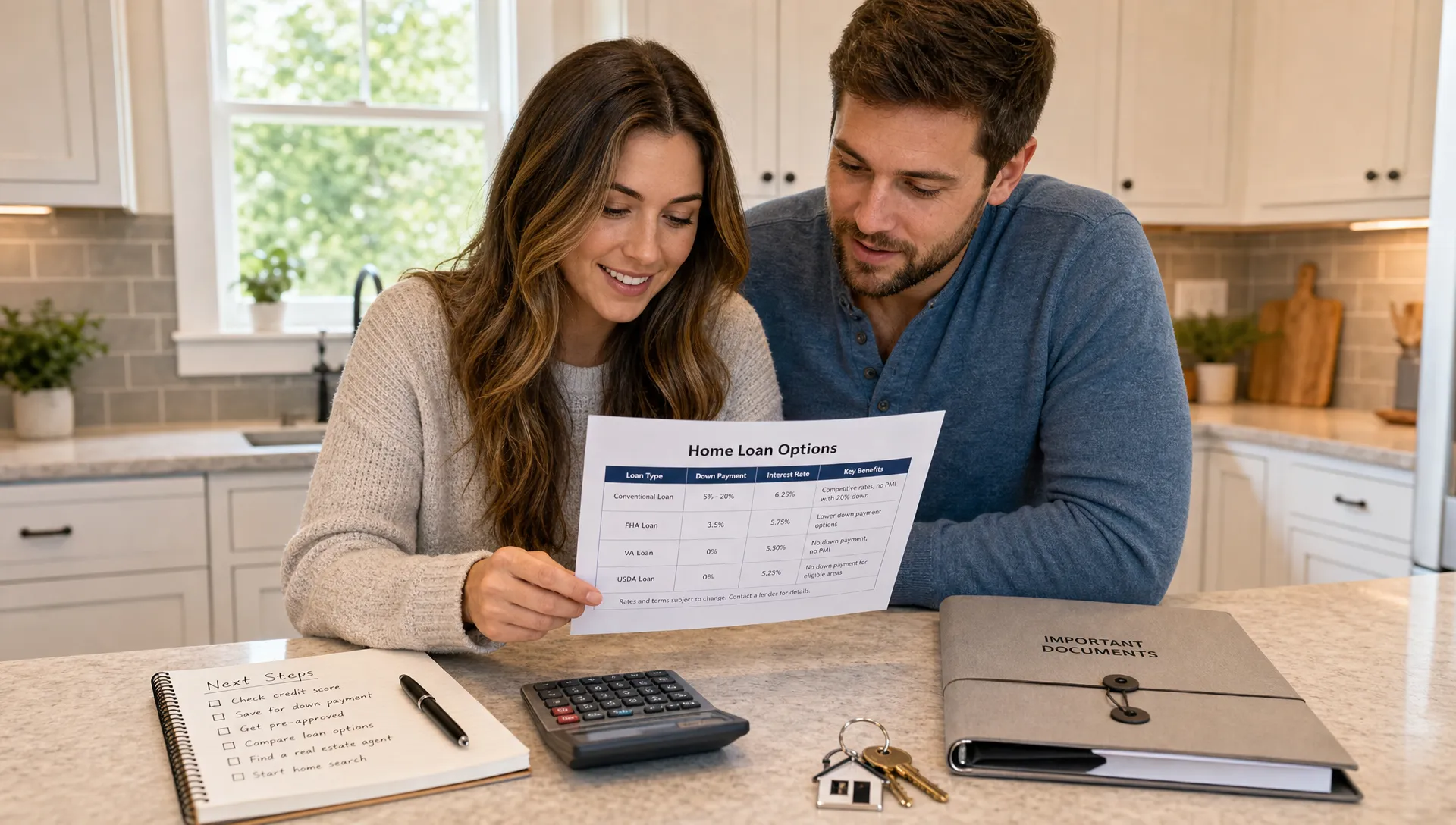

Step 3: Compare Loan Options, Not Just Rates

Once your lender understands your profile and goals, the next step is matching you with the right loan structure. Common options include conventional loans, FHA loans, VA loans for eligible borrowers, USDA loans for eligible rural properties, jumbo loans, and specialized programs for unique income or property scenarios.

Your loan option affects more than the interest rate. It can change the required down payment, mortgage insurance, seller contribution limits, property standards, appraisal requirements, and approval flexibility.

You should compare offers using the full picture, including:

- Interest rate and APR

- Estimated monthly payment

- Down payment and total cash to close

- Mortgage insurance or funding fees

- Discount points or lender credits

- Loan term and rate lock period

- Program rules and property requirements

The Consumer Financial Protection Bureau explains that the standardized Loan Estimate is designed to help borrowers compare mortgage offers more clearly. It is one of the most important documents you will receive during the process.

If you want a deeper comparison of program choices, see New Era Lending’s guide to mortgage loan programs.

Step 4: Submit the Full Loan Application

After you choose a property or decide to move forward with a refinance, the lender completes a full loan application. This application collects information about you, the property, your employment, income, assets, debts, and the type of loan you are requesting.

For a purchase, the signed purchase contract becomes part of the loan file. For a refinance, the lender will review your current mortgage, payoff details, property value, and refinance purpose.

After application, you receive disclosures. These explain the estimated terms, costs, payments, and important rights related to your loan. Review them carefully, especially the Loan Estimate, because it shows your projected rate, APR, closing costs, cash to close, and monthly payment.

At this point, accuracy matters. If your application has missing information or inconsistent details, the file may slow down later during processing or underwriting.

Step 5: Processing Organizes the File

Loan processing is the stage where the file is assembled, verified, and prepared for underwriting. A processor may request updated pay stubs, bank statements, explanations for deposits, homeowners insurance information, or missing pages from documents.

This is also when third-party work begins. The lender may order an appraisal, title search, flood certification, payoff statement if refinancing, and verification of employment. For condos, additional association documents may be needed.

A common misconception is that document requests mean something is wrong. Often, they simply mean the lender must document the file according to program guidelines. Mortgage approvals are evidence-based, so underwriters need a complete paper trail.

To help the process move smoothly, respond quickly, send complete documents, and avoid altered or partial files. If the lender asks for all pages of a bank statement, send all pages, even if the last page is blank.

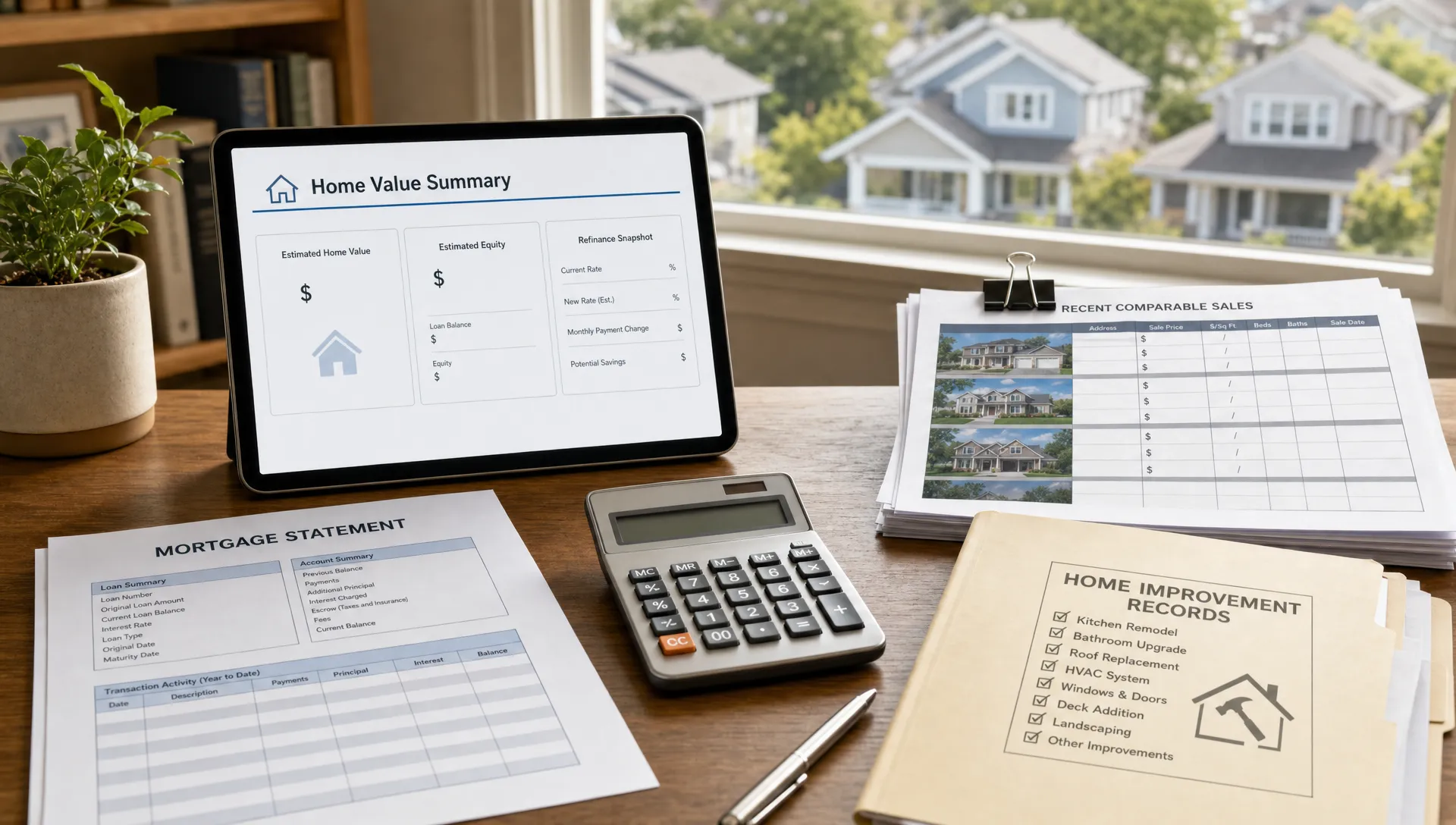

Step 6: The Property Is Reviewed

The property must support the loan. For most purchase and refinance mortgages, this involves an appraisal or an approved valuation method. The appraiser’s job is to provide an independent opinion of market value and, depending on loan type, note certain property condition issues.

The appraisal affects loan-to-value, often called LTV. LTV compares the loan amount to the property value used by the lender. If the value comes in as expected, the loan usually moves forward. If the appraisal is low, you may need to renegotiate, bring more cash, reduce the loan amount, challenge the value with supporting data, or consider another path.

Title work is another key part of property review. The title company or closing agent checks ownership history, liens, judgments, easements, and other issues that could affect the lender’s security interest or the buyer’s ownership rights.

For a more focused explanation of this stage, read New Era Lending’s guide on how a home appraisal affects mortgage approval.

Step 7: Underwriting Makes the Approval Decision

Underwriting is where the complete file is evaluated against lender and loan program requirements. The underwriter reviews your credit, income, assets, debts, property value, title information, insurance, and application details.

The underwriter may issue a conditional approval. This means the loan is approved if certain conditions are satisfied. Conditions might include updated income documents, a letter explaining a credit inquiry, proof of funds to close, title corrections, appraisal revisions, or homeowners insurance updates.

This stage can feel detailed, but it exists to confirm that the loan meets requirements before closing. The best strategy is to treat every condition as time-sensitive and answer exactly what is being requested. If you are unsure what a condition means, ask your loan officer before uploading documents.

Technology can help here. Secure document uploads and e-signatures reduce friction, but human guidance still matters because borrowers often need help understanding what underwriters are asking for and why.

Step 8: Rate Lock and Final Terms Are Confirmed

At some point before closing, your interest rate must be locked. A rate lock protects your pricing for a set period, as long as the loan closes within the lock window and the loan details do not materially change.

Lock timing is a strategy decision. Locking early can create certainty, especially if your closing date is firm. Floating may be tempting if you think rates could improve, but it also adds risk because rates can move quickly.

Your final costs can also be affected by points and lender credits. Discount points are upfront costs paid to reduce the rate. Lender credits may reduce upfront closing costs in exchange for a higher rate. Neither choice is automatically better. The right answer depends on your cash available, monthly payment goal, and how long you expect to keep the loan.

Before locking, confirm the rate, APR, points or credits, lock expiration date, estimated cash to close, and whether any float-down option exists.

Step 9: Clear to Close and Closing Disclosure

Clear to close means underwriting conditions have been satisfied and the lender is ready to prepare final closing documents. Before signing, you will receive a Closing Disclosure.

For most closed-end mortgage loans, federal rules require that borrowers receive the Closing Disclosure at least three business days before closing. This document shows the final loan terms, projected payment, closing costs, cash to close, and other important details.

Compare the Closing Disclosure to your most recent Loan Estimate. Some items can change for valid reasons, such as prepaid interest, escrow deposits, or final title charges. But you should understand every meaningful difference before signing.

Do not ignore the final review. This is your chance to confirm names, property address, loan amount, rate, monthly payment, cash to close, and whether escrows are included.

Step 10: Closing Day, Funding, and Recording

Closing is when you sign the final documents and the loan becomes legally binding. For a purchase, the buyer signs loan documents, the seller signs transfer documents, and funds are collected and distributed through the closing agent. For a refinance, you sign new loan documents and the new loan pays off the old one after any required waiting period.

Bring a valid photo ID and follow the closing agent’s instructions for wiring funds or bringing certified funds. Always verify wire instructions directly with a trusted contact before sending money, because wire fraud is a real risk in real estate transactions.

After documents are signed, the lender reviews the closing package and authorizes funding. For a purchase, ownership typically transfers once the deed is recorded according to local rules. For a refinance on a primary residence, a three-business-day right of rescission often applies before funding, with some exceptions.

Once everything is funded and recorded, the transaction is complete. You will receive information about where to make payments, whether your loan will be serviced by another company, and when your first payment is due.

What Can Delay a Home Mortgage Loan Closing?

Many mortgage delays are preventable. The most common issues involve missing documents, late responses, changes in borrower finances, appraisal problems, title issues, insurance delays, or contract changes.

To reduce the chance of delays, keep these habits from application through closing:

- Do not open new credit or take on new debt without asking your loan officer first.

- Keep funds for closing in documented accounts and avoid unexplained cash deposits.

- Respond quickly to document requests and send complete files.

- Review disclosures as soon as they arrive.

- Keep your employment and income situation stable when possible.

- Secure homeowners insurance early.

- Ask questions before making financial moves.

The mortgage process is not only about qualifying once. Lenders may re-verify credit, employment, assets, and other details before closing. A change that seems small can still require additional documentation.

What Happens After Closing?

After closing, your loan moves into repayment and servicing. The servicer is the company that collects payments, manages escrow if applicable, sends statements, and provides tax forms. Sometimes the lender that originated your loan also services it. Other times, servicing is transferred.

Your first payment is usually due after the first full month following closing, but the exact date will be shown in your closing documents. If your payment includes escrow, part of each monthly payment goes toward future property tax and homeowners insurance bills.

Keep your closing package in a safe place. It includes important documents such as your note, mortgage or deed of trust, Closing Disclosure, escrow information, and payment instructions.

How New Era Lending Helps Simplify the Process

A mortgage has many moving parts, but borrowers should not have to manage them alone. New Era Lending combines smart technology with personalized human guidance to make the process clearer from application through closing.

That means borrowers can use modern tools such as secure document uploads and e-signatures while still having access to experienced guidance for loan options, rate and term comparisons, documentation questions, and closing preparation. Whether you are purchasing, refinancing, or accessing equity, the goal is to help you understand your choices and move forward with confidence.

Frequently Asked Questions

How long does a home mortgage loan take from start to close? Many purchase loans close in roughly 30 to 45 days, but timelines vary based on the loan type, appraisal, title work, documentation, underwriting conditions, and contract deadlines. Refinances may be faster or slower depending on the scenario.

What is the difference between pre-qualification and pre-approval? Pre-qualification is often an early estimate based on limited information. Pre-approval usually involves a deeper review of credit, income, assets, and debts, making it more useful when shopping for a home.

Can my mortgage be denied after pre-approval? Yes. A loan can run into issues if your finances change, documents do not support the application, the appraisal is too low, title problems appear, or program requirements are not met. Staying consistent financially and responding quickly helps reduce risk.

What should I review before closing? Review the Closing Disclosure, loan amount, interest rate, APR, monthly payment, cash to close, escrow details, prepayment terms, and all names and property information. Ask questions before signing if something does not look right.

Do I need 20% down to get a mortgage? Not always. Many loan programs allow lower down payments for qualified borrowers. The right amount depends on your loan type, credit profile, monthly payment comfort, mortgage insurance, and cash reserves.

Ready to Understand Your Mortgage Options?

Knowing how a home mortgage loan works is the first step. The next step is seeing how the numbers apply to your specific situation.

New Era Lending can help you compare purchase, refinance, and equity options with clear guidance, transparent terms, and a technology-driven process supported by real people. If you are preparing to buy or refinance, start with a personalized conversation so you can move from application to closing with more confidence.