.jpg)

.jpg)

.jpg)

Simple Home Loans That Make Buying Easier

Buying a home can feel like a maze of rates, paperwork, timelines, and unfamiliar terms. But the loan itself should not make the process harder. The best simple home loans are built around clarity: a clear budget, a clear path to approval, clear document requests, and clear communication from the first conversation through closing.

Simple does not mean careless, one-size-fits-all, or too good to be true. A home loan still needs proper underwriting, accurate disclosures, and borrower protections. What makes it simpler is the way the process is organized around the buyer, with technology handling the busywork and knowledgeable guidance helping you make confident decisions.

If you are preparing to purchase a home, here is what to look for in a mortgage experience that makes buying easier without cutting corners.

What simple home loans should actually mean

A simple home loan is not necessarily the loan with the fewest questions or the fastest advertisement. It is a mortgage that is easy to understand, easy to compare, and easy to move through because each step is explained before you reach it.

For buyers, that usually means three things. First, you understand what you can afford before you start making offers. Second, you know which loan options fit your credit, income, down payment, and goals. Third, you have a reliable process for submitting documents, reviewing terms, and staying on schedule.

That distinction matters because home financing is still a major financial commitment. The Consumer Financial Protection Bureau recommends comparing Loan Estimates from lenders so you can review interest rate, monthly payment, closing costs, and other terms side by side. A simpler process should make those details easier to see, not hide them behind vague promises.

A borrower-friendly lender should be able to explain what you are applying for, why certain documents are needed, and how your loan terms affect your monthly payment and cash to close. New Era Lending takes this kind of modern, guided approach by combining technology-driven tools with personalized human support across home purchase, refinance, and equity access solutions.

The key ingredients that make a home loan easier

Most buyers do not need more jargon. They need a better sequence. A simple mortgage experience should help you move from uncertainty to readiness in a logical order.

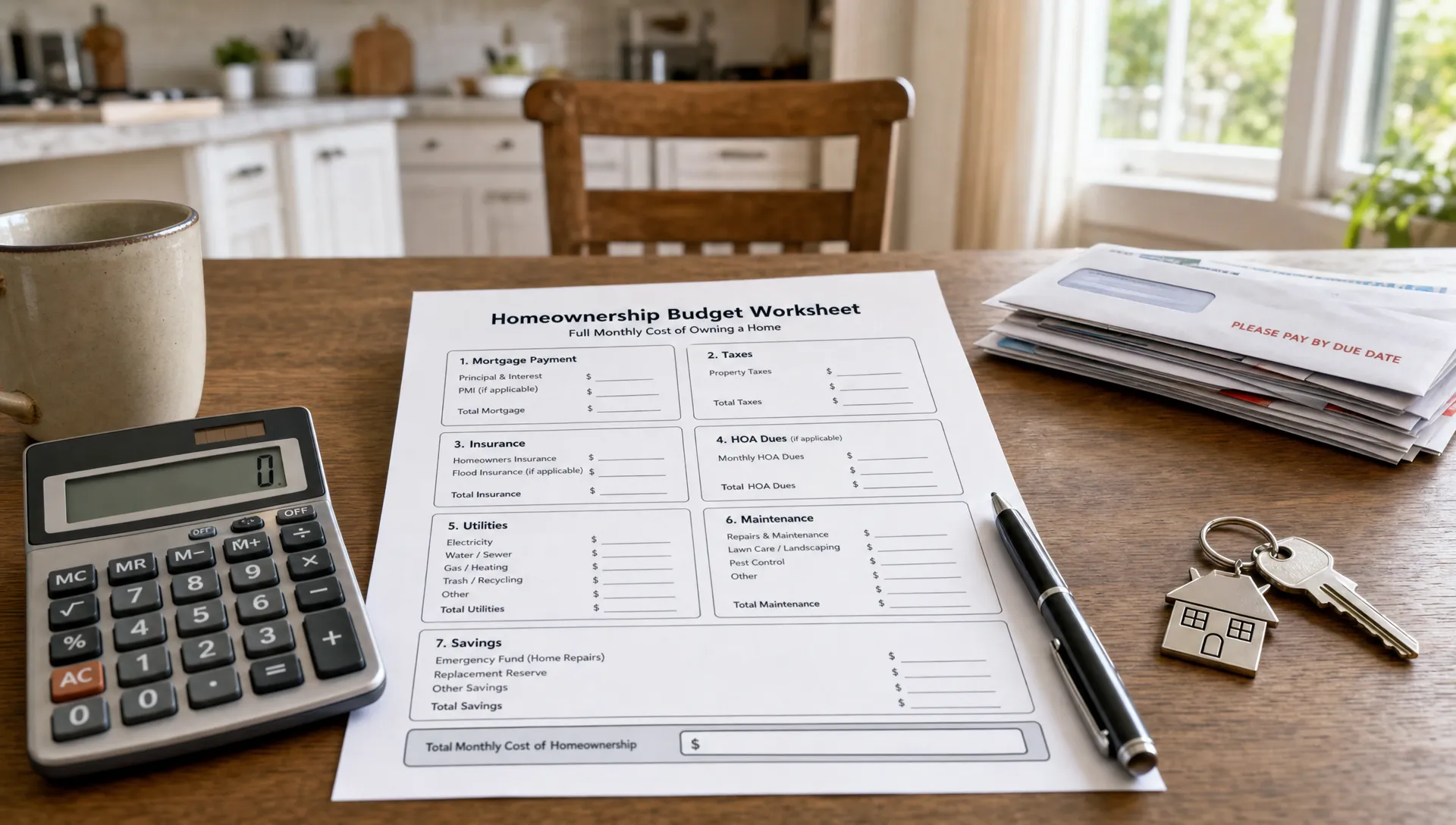

A clear starting budget

Before you focus on homes, focus on numbers. Your budget should account for more than the listing price. A realistic estimate includes principal and interest, property taxes, homeowners insurance, possible mortgage insurance, HOA dues, and closing costs.

Pre-approval can make this step much easier because it helps you understand your buying power before you start touring homes seriously. It can also help you make stronger offers because sellers often want to know that a buyer has already taken steps toward financing.

Still, the goal is not to stretch to the highest possible approval amount. The goal is to find a payment that fits your life. Simple home loans are most helpful when they support a sustainable purchase, not just a bigger purchase.

A short, organized document process

Mortgage documents can feel overwhelming when requests arrive randomly or without context. A simpler process tells you what is needed, why it is needed, and how to provide it securely.

Common documents may include pay stubs, W-2s, bank statements, tax returns for certain borrowers, identification, and information about debts or assets. Self-employed buyers or buyers with complex income may need additional documentation.

Modern lending tools can reduce friction with secure document uploads and e-signature support. The benefit is not just convenience. It also helps reduce delays, missing paperwork, and last-minute confusion.

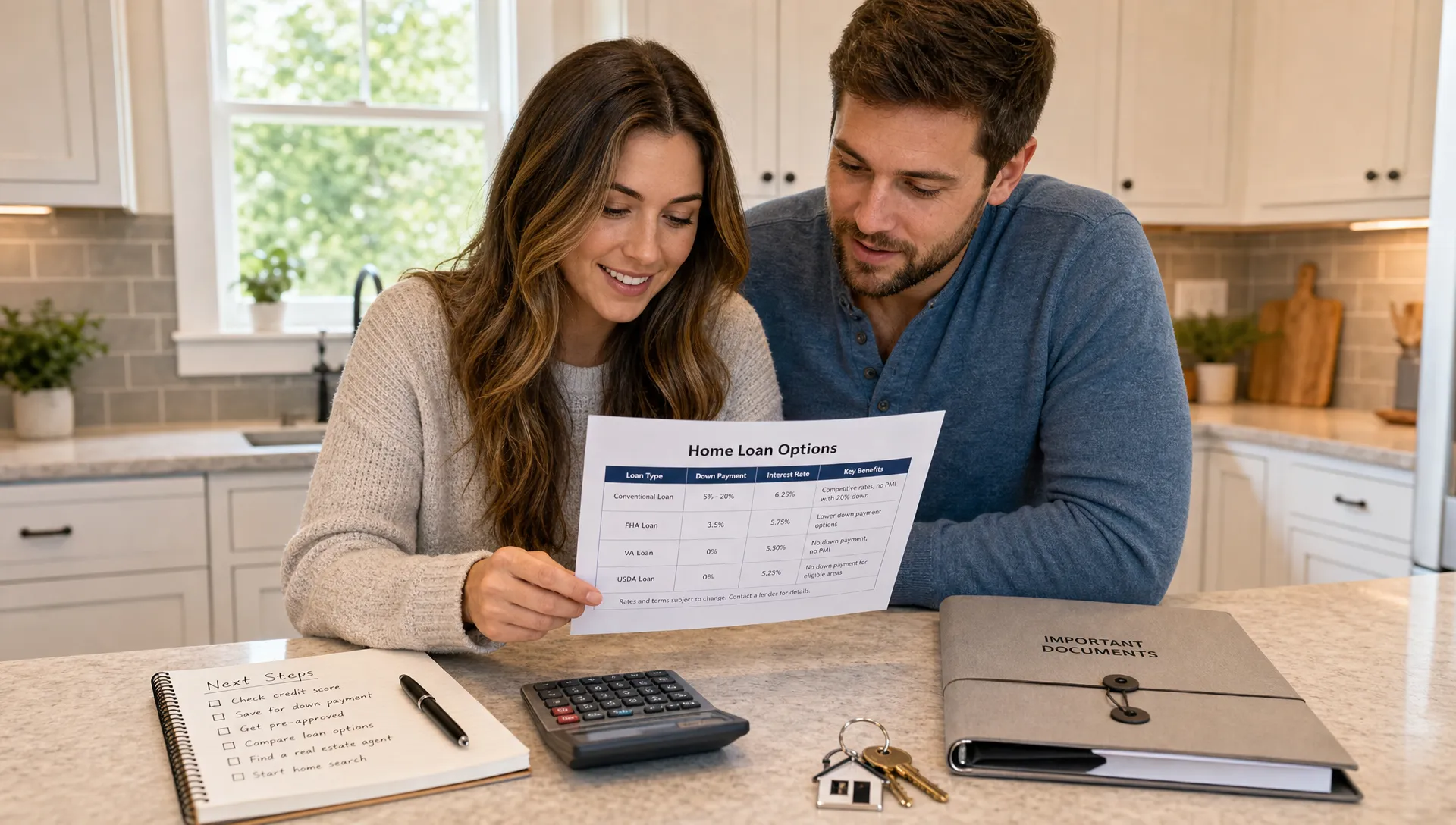

Loan options that match your situation

The easiest loan is not the same for every buyer. A conventional loan may work well for one household, while an FHA, VA, USDA, jumbo, or other program may be more appropriate for another. The right fit depends on eligibility, location, down payment, credit profile, property type, and long-term plans.

If you want a broader breakdown of common programs, New Era Lending’s guide to mortgage loan options for every buyer explains how different loan types can support different borrower needs.

What matters most is that your lender does not simply quote one option and move on. A simple home loan experience should help you compare practical choices in plain language, including how each option affects your payment, upfront costs, and flexibility.

Simple does not mean skipping borrower protections

In lending, easy should never mean risky. A smooth process still needs complete disclosures, accurate numbers, secure handling of sensitive information, and enough time for you to review the terms.

Borrower protections are part of what make a loan easier to trust. For example, the Loan Estimate helps you understand the terms after you apply, and the Closing Disclosure helps you review final costs before closing. These documents are designed to make mortgage details more transparent.

This is why the best simple home loans balance speed with care. Fast approvals and digital tools are useful, but they should be paired with clear explanations. If something changes, such as your rate, closing costs, required documents, or estimated cash to close, your lender should explain what changed and why.

For a deeper look at this balance, New Era Lending explains how easy lending can still protect borrowers while keeping the mortgage experience clear and efficient.

How technology makes home buying less stressful

Technology can make home financing easier when it removes repetitive tasks and helps buyers stay informed. It should not replace thoughtful guidance, but it can make the process feel far less scattered.

Digital mortgage tools can help buyers complete applications, upload documents securely, sign forms electronically, and respond to requests faster. This is especially valuable when you are also coordinating with a real estate agent, reviewing inspection results, comparing homes, and preparing for a move.

The real advantage is momentum. When documents are easy to submit and updates are easy to follow, fewer things fall through the cracks. You spend less time wondering what is next and more time making informed decisions.

New Era Lending’s article on smart home lending tools that simplify mortgages explores how digital convenience and human guidance can work together throughout the loan process.

Home loan options that can simplify buying

The right loan program can make a major difference in how manageable your purchase feels. While eligibility rules vary, these are some of the common options buyers often compare.

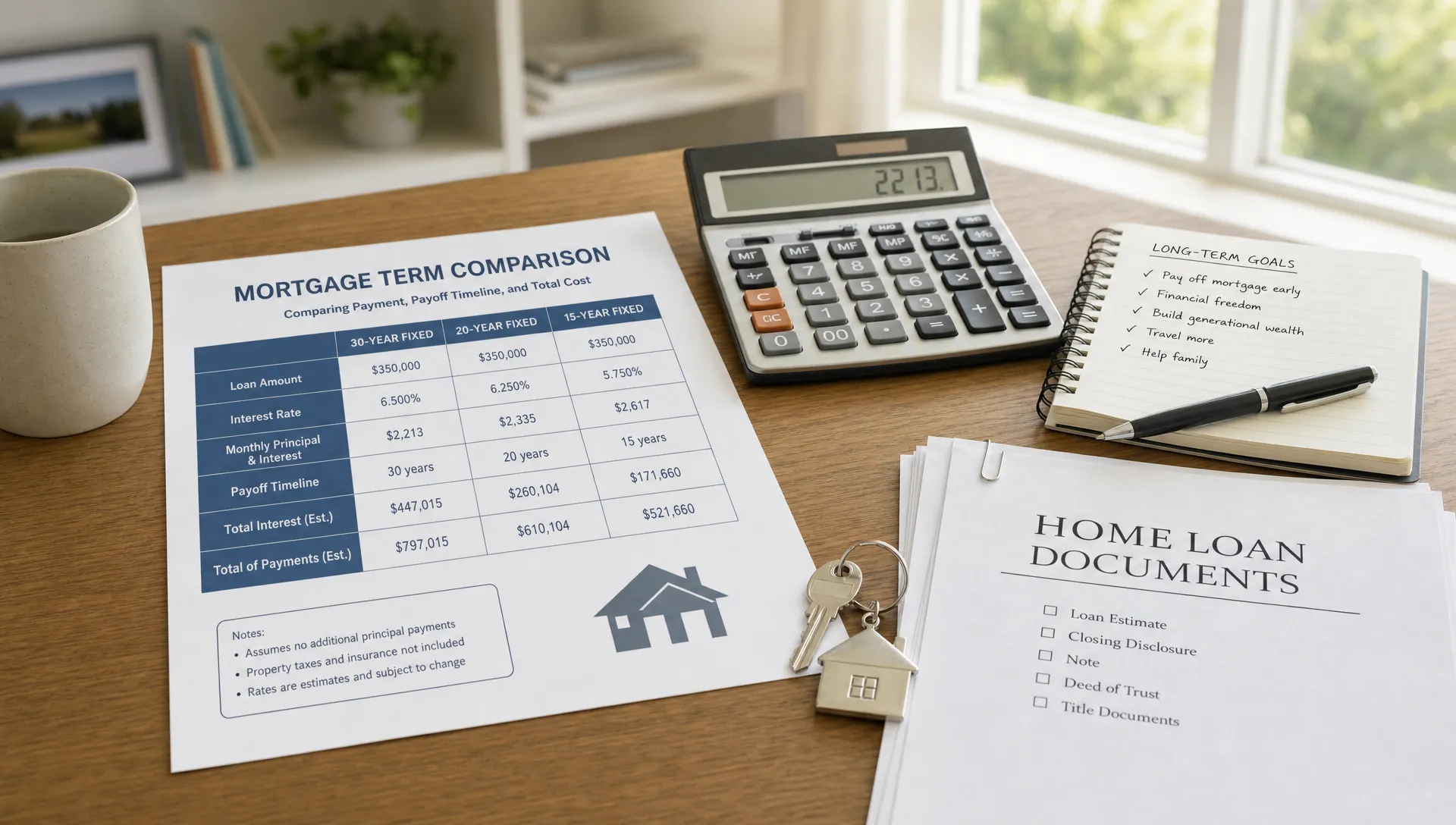

Conventional loans

Conventional loans are widely used and may be a good fit for buyers with stronger credit profiles, stable income, and enough funds for down payment and closing costs. They can work for first-time buyers as well as repeat buyers.

The simplicity of a conventional loan often comes from familiarity. Many sellers, agents, and lenders work with them frequently, and the structure can be straightforward for qualified borrowers. However, requirements vary by lender and by loan scenario, so it is still important to compare terms.

FHA loans

FHA loans are often considered by buyers who may need more flexible credit or down payment requirements. They can be useful for first-time buyers, although they are not limited only to first-time buyers.

The tradeoff is that FHA loans include mortgage insurance requirements, which can affect both upfront and monthly costs. A simple explanation from your lender should show not only whether you qualify, but also how the full payment compares with other options.

VA loans

VA loans can be a powerful option for eligible veterans, service members, and certain surviving spouses. These loans may offer benefits such as no required down payment for eligible borrowers, subject to program rules and lender requirements.

Because eligibility and funding fee details can vary, buyers should work with a lender that understands veteran loan programs. New Era Lending offers specialized veteran loan programs, which can be especially helpful for buyers who want guidance from pre-approval through closing.

USDA loans

USDA loans may help eligible buyers purchase homes in qualifying rural or suburban areas. Like VA loans, USDA programs may allow no down payment for eligible borrowers, but income limits, location requirements, and property rules apply.

For buyers who are open to eligible locations, USDA financing can make homeownership more accessible. The key is confirming eligibility early so you do not lose time shopping in areas or price ranges that do not fit program guidelines.

Down payment assistance and specialty programs

Some buyers may qualify for down payment assistance or other local, state, or specialty programs. These can sometimes reduce upfront barriers, but they may come with income limits, location rules, education requirements, or repayment conditions.

A simple home loan process should help you understand both the benefit and the obligation. Assistance is most useful when you know how it affects your cash to close, monthly payment, future refinance options, and long-term plans.

What the process should feel like from pre-approval to closing

A well-run mortgage process has a rhythm. You should not feel like every step is a surprise. While every transaction is unique, most purchase loans move through a few core stages.

Pre-approval comes first. This is where the lender reviews your financial picture and helps estimate what you may be able to borrow. It is also the stage where you should ask questions about payments, down payment options, and realistic cash to close.

Next comes home shopping and the offer. Once your offer is accepted, the lender will work with you to move from pre-approval toward a full application and underwriting review. The property will also be part of the process, including appraisal and title work where applicable.

Underwriting is where the lender verifies your information and evaluates the loan file. This can involve follow-up document requests. A simpler experience does not mean there will be no questions. It means the questions are organized, explained, and handled promptly.

Finally, you review closing documents, prepare funds if needed, sign, and complete the purchase. Before you reach the closing table, you should understand your final monthly payment, closing costs, and loan terms.

Questions to ask before choosing a lender

The lender you choose can make the difference between a confusing process and a clear one. Before you commit, ask questions that reveal how the experience will actually work.

- How will you explain my loan options and compare them?

- What documents should I prepare before I start shopping?

- How do you handle secure document uploads and e-signatures?

- How often will I receive updates during underwriting?

- What costs should I expect beyond the down payment?

- Who can I contact if I have questions after business hours or during a fast-moving offer situation?

The answers should feel specific, not generic. A lender does not need to promise perfection to earn your trust. They should be able to show a clear process, communicate in plain language, and help you understand the decision in front of you.

Red flags that a loan may not be as simple as it sounds

Some mortgage offers sound easy at first but become confusing later. Be cautious if a lender focuses only on speed without discussing affordability, disclosures, or documentation. Also be wary of vague cost estimates, unclear rate terms, or pressure to move forward before you understand the numbers.

A simple process should still leave room for questions. If you feel rushed, dismissed, or unsure about the payment, it is worth slowing down. The right lender should welcome informed borrowers because informed borrowers are better prepared for homeownership.

You should also be careful with any offer that makes the approval sound guaranteed before your financial profile has been reviewed. Real mortgage approval depends on income, credit, assets, debts, property details, and program requirements. Simplicity should come from better guidance, not unrealistic promises.

How to prepare for a smoother home loan experience

You can make the loan process easier before you ever apply. Start by reviewing your credit, estimating your monthly comfort zone, and gathering basic financial documents. Avoid taking on new debt or making large unexplained transfers while you are preparing to buy, since those changes can create additional underwriting questions.

It also helps to decide what matters most to you. Some buyers care most about the lowest possible monthly payment. Others want to minimize cash to close, buy sooner, access a veteran program, or compare fixed-rate and adjustable-rate options. When your goals are clear, your lender can guide you more effectively.

Most importantly, choose a lending partner that communicates in a way you understand. Home buying has enough moving parts. Your mortgage should bring structure to the process, not more uncertainty.

Frequently Asked Questions

What are simple home loans? Simple home loans are mortgage options supported by a clear, organized process. They still require proper approval and documentation, but they make buying easier through transparent terms, secure digital tools, and helpful guidance.

Does a simple home loan mean fast approval? It can include fast approvals, but speed is only one part of the experience. A truly simple loan process also includes clear communication, accurate disclosures, organized document requests, and a loan option that fits your financial goals.

Which home loan is easiest to qualify for? There is no single easiest loan for every buyer. FHA, VA, USDA, conventional, and assistance programs each have different requirements. The best option depends on your credit, income, down payment, location, eligibility, and property type.

Can first-time buyers get simple home loans? Yes. First-time buyers can benefit from a guided mortgage process that explains payment, cash to close, loan options, and documentation step by step. Some may also qualify for first-time buyer or down payment assistance programs.

How do I make the mortgage process less stressful? Get pre-approved early, gather documents in advance, ask for clear cost estimates, avoid major financial changes during the process, and work with a lender that combines digital convenience with personal guidance.

Make your next home loan easier to understand

A simpler mortgage experience starts with the right guidance. New Era Lending helps buyers move through home financing with smart technology, secure digital tools, transparent communication, and personalized support from real mortgage professionals.

Whether you are buying your first home, moving into your next one, or comparing loan options, you do not have to figure it out alone. Start your path with New Era Lending and take the next step toward a clearer, easier home buying experience.