.jpg)

.jpg)

.jpg)

Mortgage Loan Options: A Simple Guide for Every Buyer

Mortgage shopping can feel like learning a new language overnight. Fixed vs ARM, FHA vs conventional, points, buydowns, DTI, LTV, and a dozen other acronyms, all while you are trying to decide what you can comfortably afford.

This guide breaks down today’s most common mortgage loan options in plain English, and gives you a simple way to narrow to the best fit for your goals, your property, and your timeline.

Start with the 3 “why” buckets: buy, refinance, or access equity

Most loan choices make more sense once you’re clear on the outcome you want.

1) Buying a home (purchase loans)

Purchase loans are built around qualifying you for a home price and monthly payment that fits your budget, then matching you to the right program based on down payment, credit, and the property.

2) Refinancing a current mortgage (refi loans)

A refinance replaces your existing mortgage. People refinance to lower their rate, change their term (30 to 15, or 30 to 20), switch from an ARM to fixed, remove mortgage insurance, or take cash out.

If your goal is specifically refinancing, you may want a dedicated deep dive after this overview. New Era Lending has a helpful guide on refinance decision-making in 2026.

3) Using home equity without replacing your whole mortgage (equity options)

If you already have a great first-mortgage rate, you might prefer a second-lien option like a HELOC or home equity loan, depending on your payment preference and how you plan to use funds.

For a focused comparison, see equity mortgage loan vs HELOC.

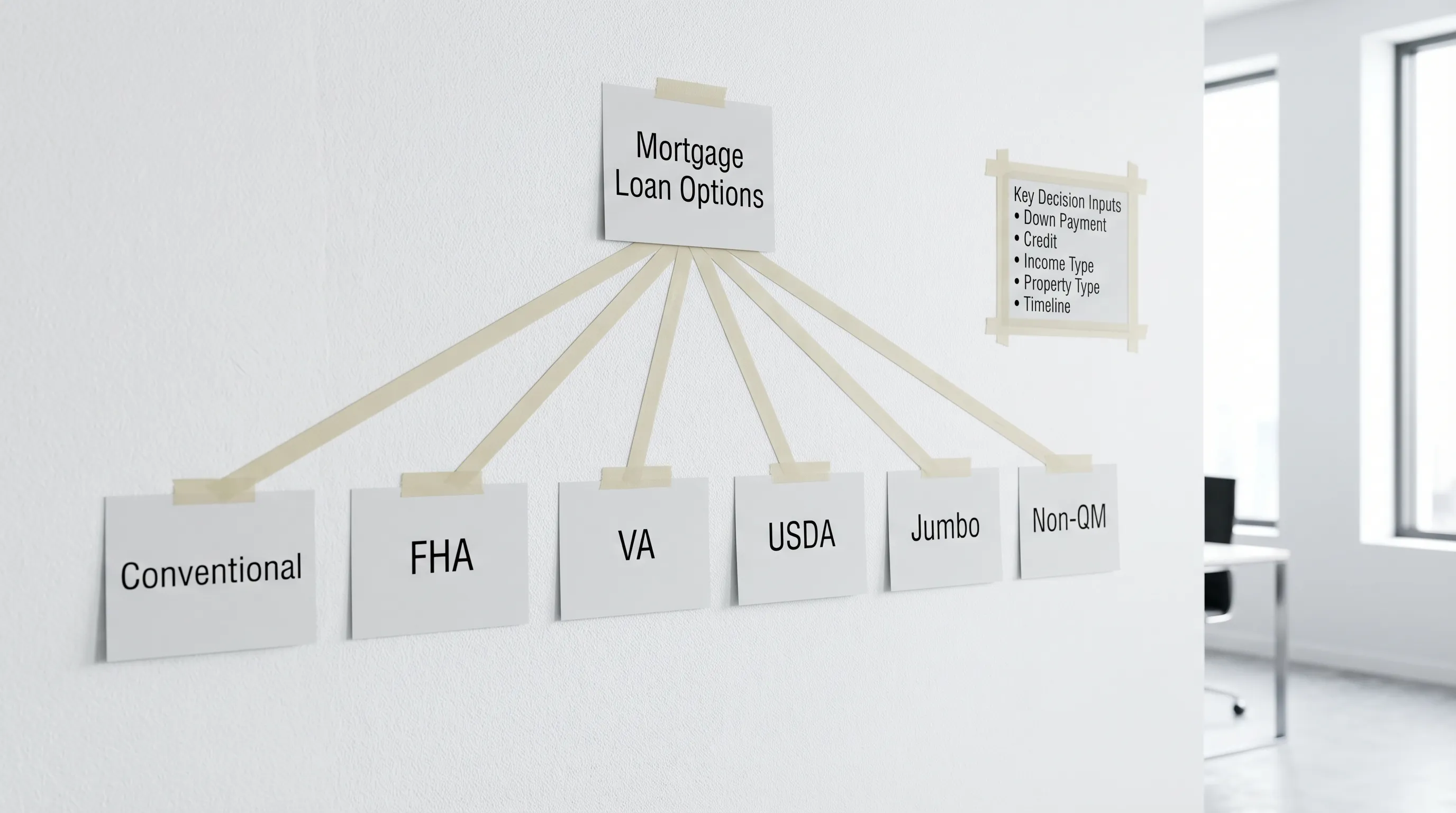

The core mortgage loan options (and who they’re best for)

There is no universal “best loan.” The best option is usually the one that balances:

- Cash needed upfront

- Monthly payment stability

- Total cost over your expected time in the home

- Property eligibility and competitiveness

Below is a simple, buyer-friendly tour of the programs you will see most often.

Conventional loans (often the default)

“Conventional” typically means a mortgage that is not insured by the federal government. Many conventional loans are “conforming,” meaning they follow Fannie Mae or Freddie Mac guidelines.

Conventional financing is often a strong fit when:

- You have solid credit and documented income

- You want flexibility (primary home, second home, or investment, depending on the program)

- You can bring a down payment that keeps the payment comfortable

If you put less than 20 percent down, conventional loans usually require private mortgage insurance (PMI), which can often be removed later once you reach the required equity.

FHA loans (more flexible qualification for many buyers)

FHA loans are insured by the Federal Housing Administration. They are commonly used by first-time buyers and buyers rebuilding credit because the guidelines can be more forgiving.

FHA can be a strong fit when:

- Your credit score is lower than what conventional pricing rewards

- You need a smaller down payment

- You want a standardized program with clear rules

FHA mortgages include mortgage insurance premiums (MIP), and the long-term cost depends on your down payment and loan structure.

If you want a focused, side-by-side explanation without the noise, New Era Lending also has a dedicated breakdown of what makes an FHA loan different from a conventional loan.

VA loans (for eligible service members, veterans, and some surviving spouses)

VA loans are backed by the U.S. Department of Veterans Affairs and are one of the most powerful options in the market for eligible borrowers.

VA loans can be a great fit when:

- You qualify through military service

- You want to minimize cash to close

- You want to avoid monthly mortgage insurance (VA loans do not use PMI, though there may be a VA funding fee in some cases)

Because VA has property and occupancy rules, it’s smart to confirm early that the home you want will pass the VA’s requirements. If you are exploring that route, see VA loan property types and occupancy rules.

USDA loans (for eligible rural and some suburban areas)

USDA loans are backed by the U.S. Department of Agriculture and are designed to expand homeownership in eligible locations.

USDA can be a strong fit when:

- The property is in an eligible area (many are surprised what qualifies)

- Your household income fits program limits

- You want low down payment options

USDA guidelines can be specific, so the key is verifying address eligibility and income rules early, before you get attached to a home.

Jumbo loans (for higher loan amounts)

A “jumbo” loan is generally a mortgage that exceeds conforming loan limits. Jumbo underwriting often emphasizes stronger credit, larger down payments, and more reserves.

Jumbo can be a fit when:

- You are purchasing a higher-priced home

- You have strong income and assets

- You want to avoid splitting financing into multiple loans

Jumbo is not automatically “hard,” but it is more sensitive to documentation, assets, and overall borrower profile.

Non-QM and portfolio loans (when your income is real but harder to document)

“Non-QM” (non-qualified mortgage) and portfolio products are designed for scenarios that do not fit standard agency guidelines. This does not mean subprime, it usually means the lender is using alternative methods to evaluate your ability to repay.

These programs can help when:

- You are self-employed, commission-based, or have variable income

- Your tax returns do not reflect your true cash flow (common with write-offs)

- You need more flexible guideline interpretation for a unique scenario

If self-employment applies to you, New Era Lending also outlines what lenders typically look for in how to qualify for a self-employed mortgage loan.

Renovation and construction-related loans (when the property needs work)

Not every home fits a standard loan, especially fixer-uppers or new builds. Renovation and construction options can roll certain costs into the financing so you are not forced to fund everything out of pocket.

These options can be relevant when:

- The home needs repairs that affect livability or appraisal

- You are buying a home specifically to remodel

- You are building a new home and need a construction-focused structure

The details vary by program and property condition, so the practical move is to bring a contractor bid scope (even a rough one) into your early lender conversation.

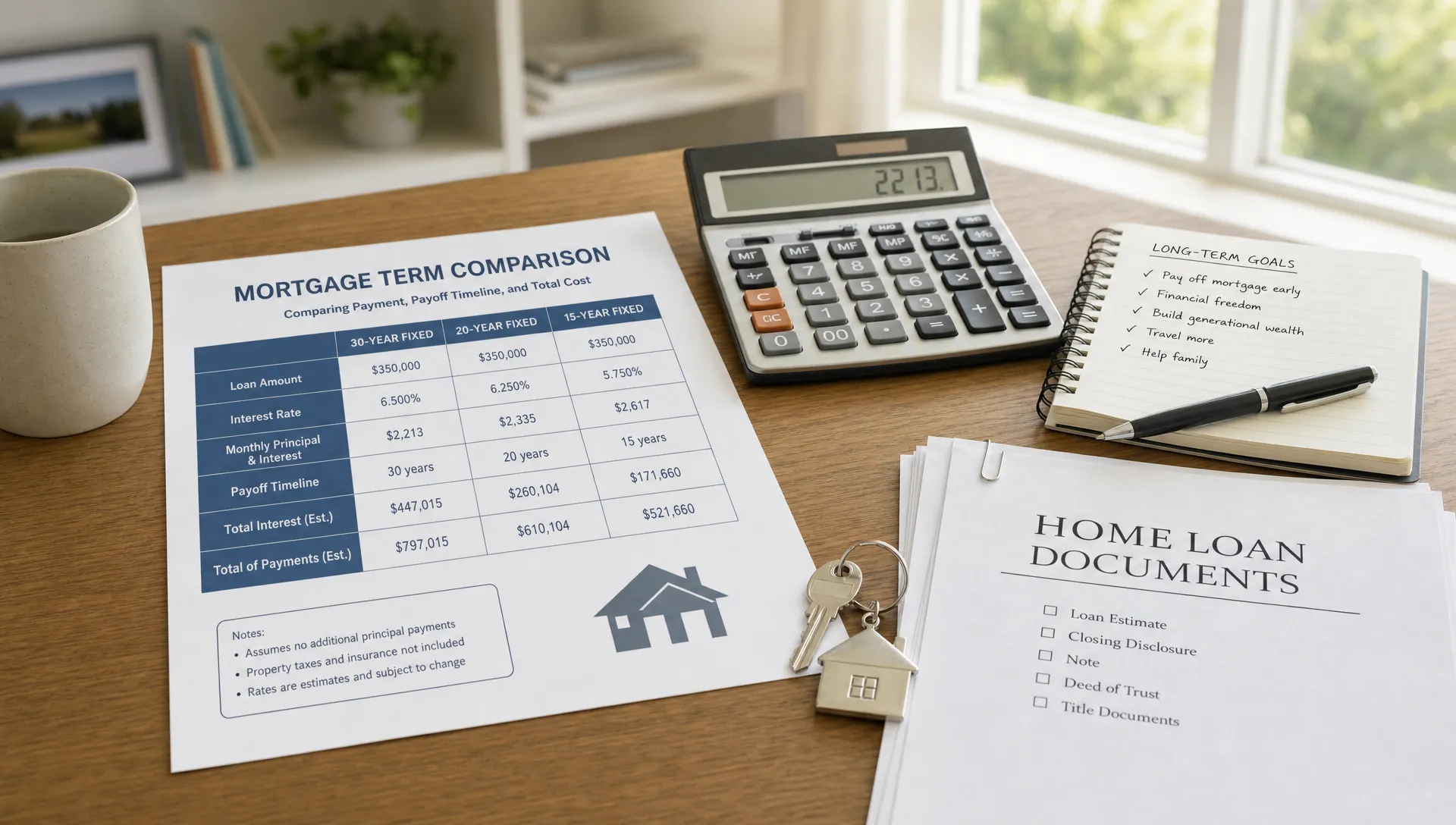

Rate structure choices: fixed, ARM, and temporary strategies

Once you pick the mortgage program, you still choose the structure of the interest rate and payment.

Fixed-rate mortgages

Your principal and interest payment is stable for the life of the loan (assuming you do not refinance). This is the simplest option for long-term planners.

Fixed can be especially attractive when:

- You plan to keep the home a long time

- You prefer payment certainty over optimization

Adjustable-rate mortgages (ARMs)

An ARM usually starts with a lower introductory rate for a set period, then adjusts based on an index and margin. ARMs can be useful, but only when paired with a realistic time horizon.

ARMs may make sense when:

- You expect to sell or refinance before the first adjustment

- You want lower initial payments and can handle future variability

Points and temporary buydowns

These are tools that can reduce the rate temporarily or permanently, typically in exchange for upfront cost (sometimes paid by the buyer, seller, or builder).

The key question is not “Is the rate lower?” It’s “Will I keep the loan long enough to benefit?”

A simple framework to choose the right option (without getting overwhelmed)

Instead of comparing every loan on the internet, narrow your choices by answering five practical questions.

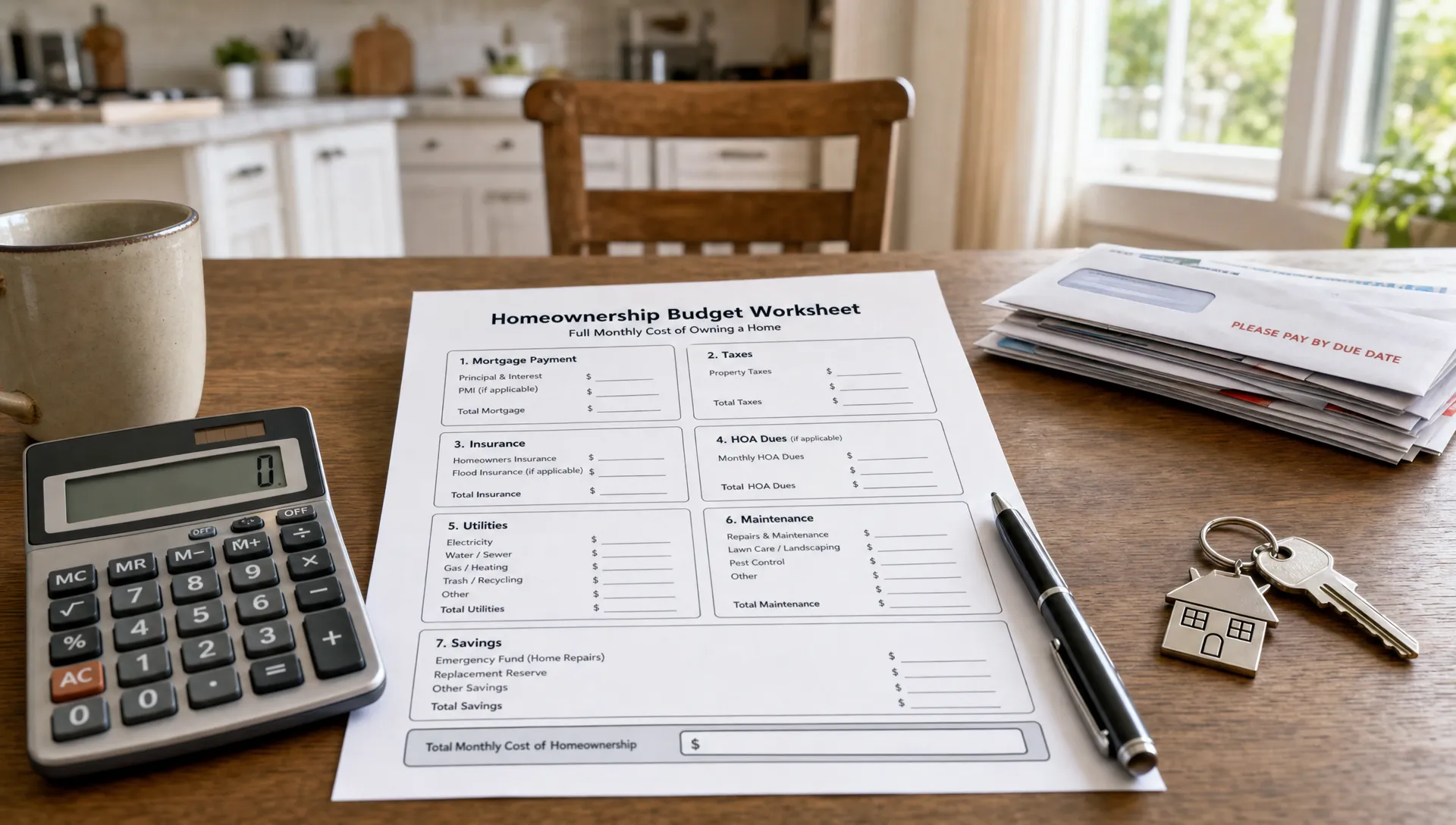

1) How much cash do you want to bring to closing?

Cash-to-close includes down payment plus closing costs and prepaid items. Lower down payment can preserve savings, but may increase the monthly payment due to mortgage insurance or higher loan amount.

If you want a realistic picture of cash needs, keep in mind that closing costs often run a few percent of the loan amount depending on location and scenario. (New Era Lending explains this clearly in Closing Costs: The Fees Nobody Tells You About.)

2) What does your credit profile actually support?

Credit affects:

- Which programs you can qualify for

- Your rate and mortgage insurance costs

- How competitive your offer feels in a fast market

If your credit is mid-rebuild, FHA may compete well. If your credit is strong, conventional pricing can be compelling.

3) What type of property are you buying?

Loan eligibility can change based on:

- Condo vs single-family

- 2 to 4 units vs 1 unit

- Condition and habitability

- Primary residence vs second home vs investment

This is why two buyers with identical income can get very different “best loan” recommendations.

4) How long do you expect to keep the home or the mortgage?

Your time horizon affects almost every tradeoff:

- Paying points can be smart if you keep the loan long enough

- An ARM can be reasonable with a shorter, realistic horizon

- Mortgage insurance strategy changes if you plan to refinance later

5) What is your tolerance for payment change?

If a payment increase would strain your budget, prioritize stability. If you have flexibility and a plan, you can consider options that optimize short-term cost.

How to compare lenders and online offers (and avoid “rate ad” confusion)

Many borrowers see an advertised rate and assume it is directly comparable to another lender’s ad. In reality, quoted rates can differ based on:

- Points or credits baked into the quote

- Credit score and down payment assumptions

- Property type and occupancy assumptions

- Timing and lock period

A good baseline is to compare actual lender disclosures (like a Loan Estimate) on the same day, for the same scenario, not marketing snippets.

It also helps to understand that a lot of online information is written to generate leads, not to educate. If you are curious how those tactics work behind the scenes, reading a no-fluff marketing publication like Solving Marketing can make you a sharper consumer when you evaluate mortgage ads and “too good to be true” offers.

The fastest path to clarity: get a real pre-approval and a side-by-side scenario

A true pre-approval does two things:

- It tells you what you qualify for (based on verified info, not guesses)

- It helps you shop with confidence, because your offer is backed by a vetted lender review

When you ask for a pre-approval, you will typically provide documentation for income, assets, and identification. The smoother your document process is, the less stressful the closing timeline tends to be.

If you are buying soon, consider requesting two scenarios instead of one:

- The “lowest cash to close” option

- The “lowest long-term payment/cost” option

Seeing both usually makes the right answer obvious.

Frequently Asked Questions

What are the main mortgage loan options for a home purchase? The most common purchase options are conventional, FHA, VA (for eligible borrowers), USDA (for eligible areas and incomes), jumbo (for higher loan amounts), and non-QM/portfolio loans for unique income scenarios.

Is a conventional loan always better than FHA? Not always. Conventional can be cheaper for strong credit profiles, while FHA can be more forgiving for credit or down payment constraints. The better option depends on total monthly cost, upfront cash, and how long you’ll keep the loan.

How do I choose between a fixed-rate mortgage and an ARM? A fixed-rate loan prioritizes payment stability. An ARM can reduce the initial rate and payment but introduces future uncertainty. Your expected time in the home and your risk tolerance should drive the decision.

Do I need 20% down to get a good mortgage? No. Many buyers qualify with lower down payments. The tradeoff is typically mortgage insurance and a higher loan amount, which can affect the monthly payment.

What’s the difference between a refinance and a HELOC? A refinance replaces your existing mortgage with a new one. A HELOC is usually a second loan that lets you borrow against equity without changing your first mortgage (often with a variable rate).

Ready to compare your best-fit options with a real scenario?

If you want help narrowing down the right mortgage path, New Era Lending combines smart, tech-driven workflow (secure document uploads and e-signatures) with personalized guidance from a mortgage professional. They support home purchase, refinance, and equity access across 39 states.

Explore your next step at New Era Lending and request a side-by-side comparison based on your goals, timeline, and budget.