.jpg)

.jpg)

.jpg)

Equity Mortgage Loan vs HELOC: Which Is Better for You?

Tapping your home’s equity can be a smart way to fund big goals, but choosing the wrong product can create payment shocks, unnecessary interest, or a longer payoff timeline than you planned. The two most common options are an equity mortgage loan (often called a home equity loan) and a HELOC (home equity line of credit).

They both use your home as collateral, but they behave very differently once you close. Here’s how to compare them, and how to decide which fits your budget, timeline, and risk tolerance.

Quick definitions (so we’re comparing the right things)

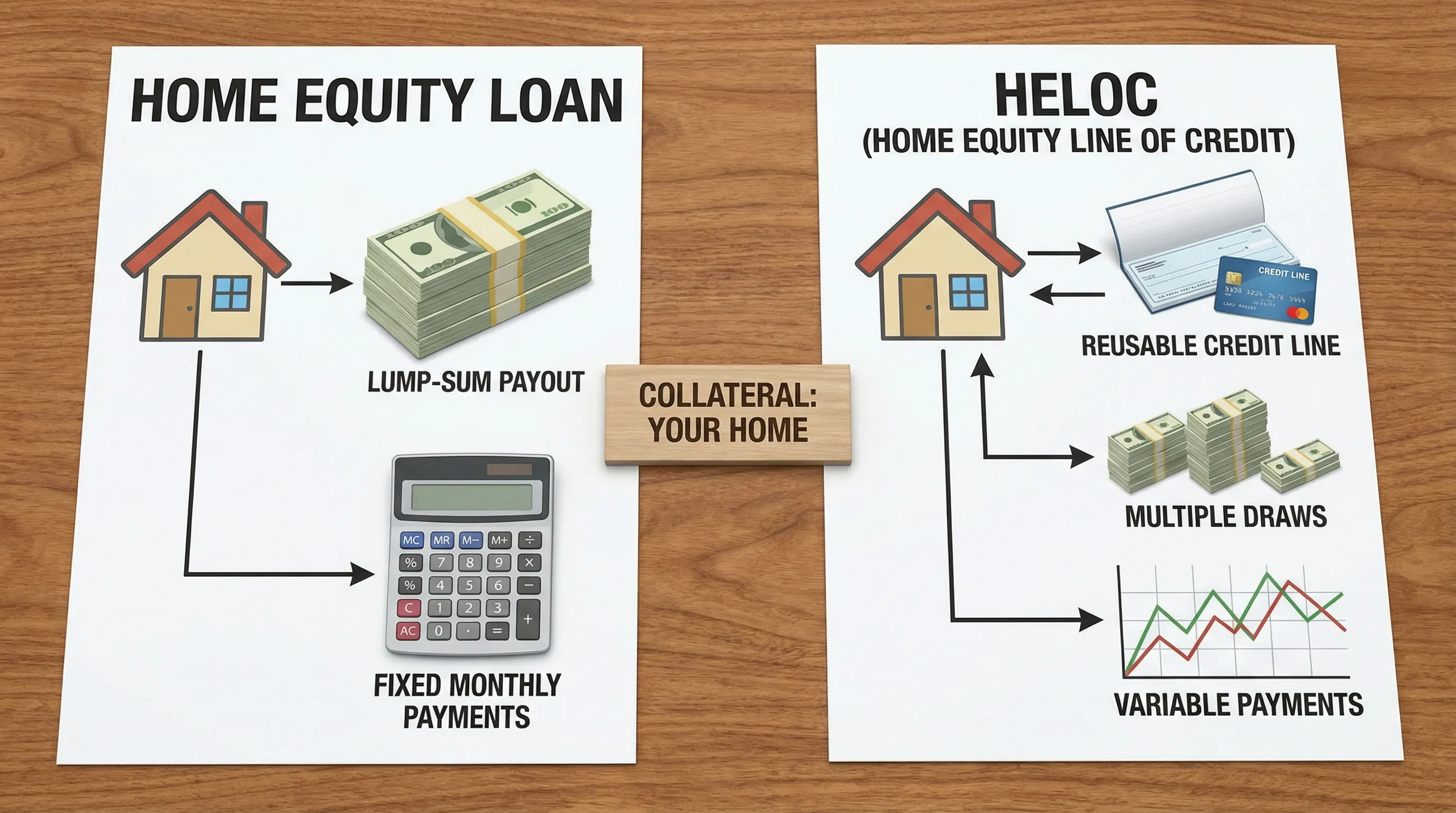

What is an equity mortgage loan?

An equity mortgage loan typically refers to a home equity loan. It’s usually a second mortgage that gives you a lump sum at closing, with a fixed interest rate and fixed monthly principal and interest payment over a set term.

People often use home equity loans for a one time cost where the amount is known upfront, like paying off higher interest debt, covering a major home project with a firm contract price, or buying out a co-owner.

What is a HELOC?

A HELOC is a revolving credit line secured by your home. You can draw funds as needed up to your limit during a draw period, then repay during the repayment period. HELOC rates are often variable, which means the monthly payment can change as market rates move.

If you want a consumer friendly overview, the CFPB’s HELOC explanation is a solid starting point.

The real differences that matter (beyond “loan vs line of credit”)

1) How you receive the money

With an equity mortgage loan, you receive all funds at once. With a HELOC, you get access to money and borrow only what you use.

A practical way to think about it:

- If you need $60,000 on day one, a home equity loan fits naturally.

- If you might need anywhere from $10,000 to $60,000 over time, a HELOC can reduce interest cost because you do not pay interest on money you never draw.

2) Rate certainty (fixed vs variable)

This is the biggest “sleep at night” difference.

Home equity loans are commonly fixed-rate, which helps with budgeting. HELOCs are commonly variable-rate, often tied to an index plus a margin.

If you’re already stretching your budget, rate variability can be the deciding factor. A HELOC can start cheaper and become more expensive later, especially if rates rise or stay elevated.

3) Payment stability and payment shock risk

A home equity loan generally has a stable payment schedule from month one.

A HELOC can be trickier because:

- During the draw period, some HELOCs allow smaller payments (sometimes interest-only, depending on the terms).

- When repayment begins, the payment can jump because you’re paying principal too.

- If the rate is variable, the payment can change even during the same phase.

If predictability matters more than flexibility, the equity mortgage loan often wins.

4) Flexibility for uncertain projects

HELOCs shine when the cost is not fully known.

Common examples:

- Renovations in phases (kitchen now, roof later)

- Ongoing tuition expenses across semesters

- A liquidity backstop for irregular income (for example, commission or self-employment)

In these situations, borrowing exactly what you need, when you need it, can be more efficient than taking a lump sum and paying interest on the full amount right away.

5) Closing costs, fees, and fine print

Both products can have lender fees, appraisal requirements, and closing costs, but the fee structure is often different.

With HELOCs, watch for items like:

- Annual fees

- Inactivity fees

- Introductory rate periods and what happens after they end

With home equity loans, watch for:

- Prepayment penalties (not always present, but important if you plan to pay it off quickly)

- Total closing costs relative to how long you’ll keep the loan

The key is not just “what is the rate,” but “what is the total cost if I keep this for 2 years vs 10 years?”

6) How each option fits your payoff strategy

If your plan is “borrow and pay down steadily,” a fixed-payment equity mortgage loan aligns with that discipline.

If your plan is “borrow, repay, borrow again,” a HELOC is designed for that, as long as you have the income stability and budget controls to avoid turning a line of credit into long term lifestyle debt.

When an equity mortgage loan is usually the better choice

An equity mortgage loan tends to be a strong fit when:

- You have a one-time expense with a known price.

- You want a fixed rate and consistent payment.

- You are consolidating higher-interest debt and need a clear payoff timeline.

- You want to reduce the risk of rising payments.

A common scenario is a major home repair that cannot wait (roof, foundation, HVAC) where you want to lock in the total cost and move on.

When a HELOC is usually the better choice

A HELOC tends to be a strong fit when:

- Your expense is staged or uncertain.

- You want ongoing access to funds for a period of time.

- You expect to borrow some money, repay it, and potentially borrow again.

- You have enough financial cushion to handle variable-rate payment changes.

A good example is a remodel with multiple contractor draws, or a long project timeline where you do not want to pay interest on the entire budget from day one.

The “better” option depends on your risk tolerance and your life right now

Money decisions are rarely just math. Borrowing against your home can feel heavy, especially if the funds are tied to stressful life events (medical issues, caregiving, job changes, divorce). If the process is bringing up anxiety or you feel stuck, it can help to talk with a professional support team, for example comprehensive psychiatric services in NYC that can help you manage stress and decision fatigue while you work through major financial choices.

Back to the lending side, here are the two most important personal questions:

Can your monthly budget absorb surprises?

If a payment increase would break your budget, lean toward more predictability (often a home equity loan) or consider delaying borrowing until the plan is clearer.

Do you have strong spending guardrails?

With a HELOC, easy access can be a benefit or a trap. If you are not confident you’ll keep draws tightly tied to a plan, a lump sum loan can prevent “just in case” borrowing.

Don’t forget the mortgage structure you already have

Before you choose between an equity mortgage loan vs HELOC, make sure you understand how it sits next to your first mortgage.

First mortgage + second lien means two payments

Most home equity loans and HELOCs are second liens. That means you keep your current first mortgage, and add a second monthly payment.

Sometimes a cash-out refinance is the real alternative

Even though this article focuses on home equity loans and HELOCs, some homeowners should at least compare a cash-out refinance if:

- Your current mortgage rate is relatively high compared to what you might qualify for now, and

- Rolling debt into one loan materially improves your monthly cash flow

A refinance is not automatically “better,” especially when closing costs are higher or your existing first mortgage rate is already excellent. The right answer is scenario-specific.

How lenders typically evaluate home equity borrowing

Underwriting varies by lender and program, but these factors commonly drive approvals and pricing:

Equity and loan-to-value

Your available equity is usually assessed using combined loan-to-value (CLTV), which considers the first mortgage plus the new home equity product compared to the home’s value.

Income and debt-to-income ratio

Even if you have a lot of equity, you still need sufficient income to support the payment. Lenders look at your overall monthly obligations.

Credit profile

Higher scores and clean payment history often help with approval odds and pricing.

Documentation and timeline

If you need funds quickly, ask early about the expected timeline and what documents will be required. Delays often come from incomplete documentation, appraisal scheduling, or title issues.

Tax note: interest deductibility depends on how you use the funds

Interest on a home equity loan or HELOC may be deductible only when the funds are used to “buy, build, or substantially improve” the home that secures the loan, subject to IRS limits and your tax situation. Rules can change, and itemizing matters.

For details, review the IRS guidance (for example, IRS Publication 936) and confirm with a qualified tax professional.

A simple decision framework (use this before you apply)

Ask yourself these questions and you’ll usually land on the right direction:

What is the money for, and is the cost known?

If the amount is known, a home equity loan is often cleaner. If the amount is uncertain or timed in phases, a HELOC is often more efficient.

Do you need flexibility or predictability?

HELOC equals flexibility. Equity mortgage loan equals predictability.

How long will you carry the balance?

If you expect to repay quickly, compare fees and any early payoff rules. If you expect to carry the balance for years, focus on long term payment comfort, not just teaser rates.

What happens if rates rise?

Run a conservative scenario with a higher HELOC rate. If that payment would cause stress, that is a red flag.

Is your goal to improve cash flow or to access cash?

If cash flow is the priority, you may need to compare all options, including refinance scenarios. If access is the priority, a HELOC or home equity loan may be enough.

Frequently Asked Questions

Is an equity mortgage loan the same as a home equity loan? In most consumer lending conversations, yes. It typically means a fixed-rate, lump-sum loan secured by your home’s equity (often as a second mortgage).

Is a HELOC hard to qualify for compared to a home equity loan? The qualification factors are similar (equity, income, credit), but approval and terms depend on the lender and your profile. The best way to know is to compare real scenarios.

Which is better for debt consolidation, a HELOC or equity mortgage loan? If you want a fixed payment and a clear payoff schedule, a home equity loan is often the simpler fit. A HELOC can work if you plan to pay down aggressively and need flexibility, but variable rates add risk.

Can my HELOC payment go up even if I don’t borrow more? Yes. With a variable-rate HELOC, the rate can change, and your payment can change, even if your balance stays the same.

Will I have closing costs on a HELOC or home equity loan? Sometimes. Costs and fee structures vary by lender, and some programs offer reduced closing costs with tradeoffs. Always review the official disclosures before committing.

How do I decide between a HELOC and cash-out refinance? Start with your current first mortgage rate, how long you’ll keep the home, and whether you prefer one payment or two. Then compare total costs and monthly payment comfort across scenarios.

Explore your best equity option with New Era Lending

The right choice is rarely universal, it depends on your goals, your timeline, and what the numbers look like for your specific home and mortgage.

If you want help comparing an equity mortgage loan vs HELOC (and, if appropriate, a cash-out refinance scenario), New Era Lending can walk you through personalized options with a tech-forward process, transparent terms, secure document uploads, and e-signature support. Learn more or start a conversation at New Era Lending.