.jpg)

.jpg)

.jpg)

Refinance Rates for Mortgages: When to Refi in 2026

Refinancing is one of those money moves that can be incredibly smart, or quietly expensive, depending on timing and goals. In 2026, the “should I refi?” question is less about guessing where rates go next and more about whether today’s refinance rates for mortgages meaningfully improve your situation after costs.

This guide gives you a practical framework to decide when refinancing makes sense, how to compare offers correctly, and what numbers matter most.

Refinance rates for mortgages in 2026: what you are really shopping

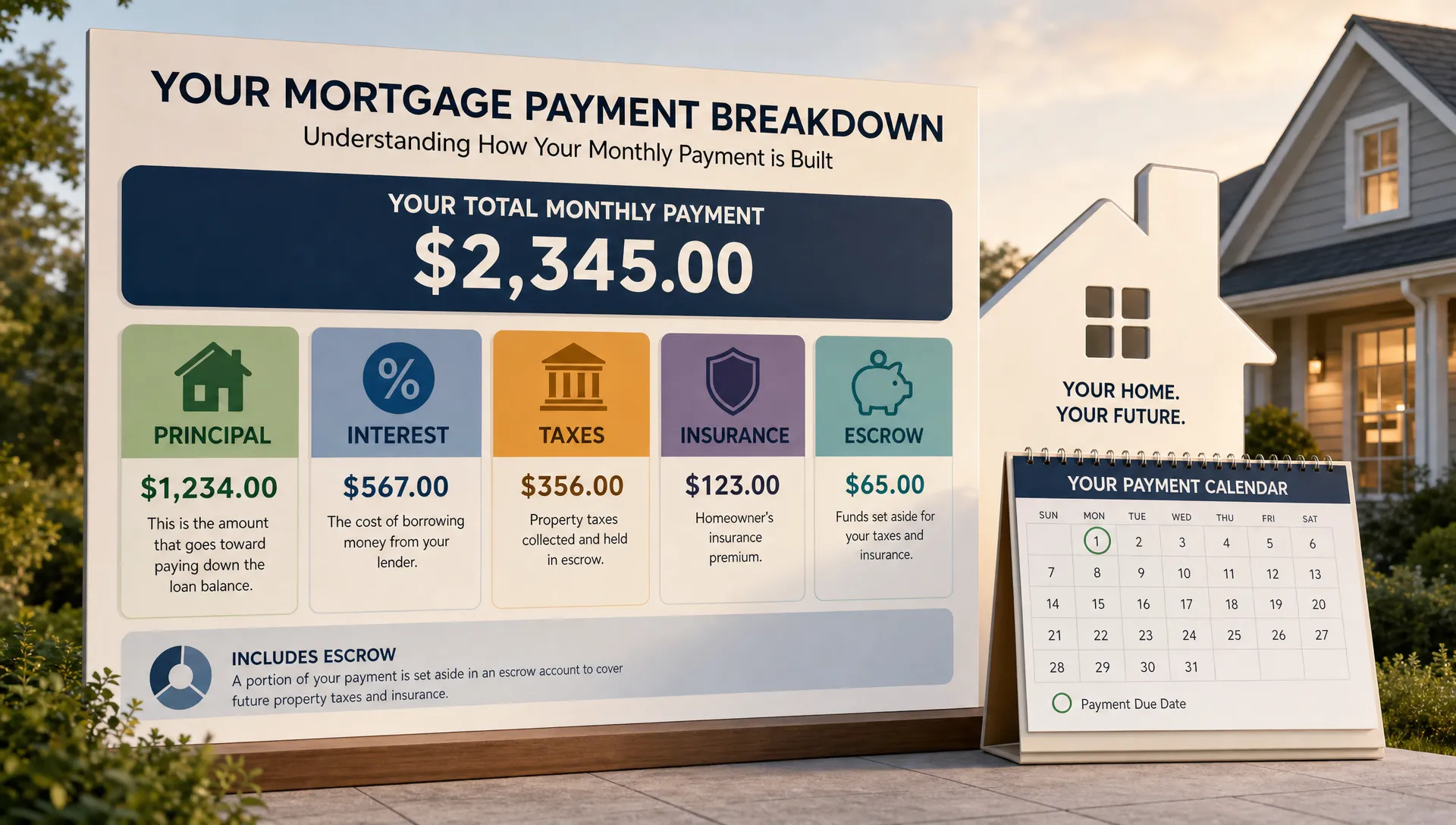

When people say “refinance rate,” they usually mean the interest rate on the new loan. But your total cost depends on more than that.

Rate vs. APR (and why APR is the better comparison tool)

- Interest rate: the cost of borrowing, expressed annually.

- APR (Annual Percentage Rate): the interest rate plus certain lender fees and points, spread over the loan term.

APR is helpful when comparing two offers with different fees or points, because it reflects the overall cost more accurately. The Consumer Financial Protection Bureau (CFPB) explains how to use APR and Loan Estimates to compare loans effectively in its mortgage resources: CFPB mortgage help.

Why your neighbor’s refinance rate is not your refinance rate

Your refinance pricing is heavily tied to risk and loan structure. Common drivers include:

- Credit score and credit profile

- Loan-to-value (LTV), meaning how much equity you have

- Loan type (conventional, FHA, VA, jumbo)

- Term length (30-year vs 15-year)

- Occupancy (primary home vs investment property)

- Cash-out vs rate-and-term refinance (cash-out often prices differently)

Also, the market benchmark you see in headlines is usually a broad national average. For context on weekly average mortgage rates, many consumers track Freddie Mac’s Primary Mortgage Market Survey (PMMS): Freddie Mac PMMS.

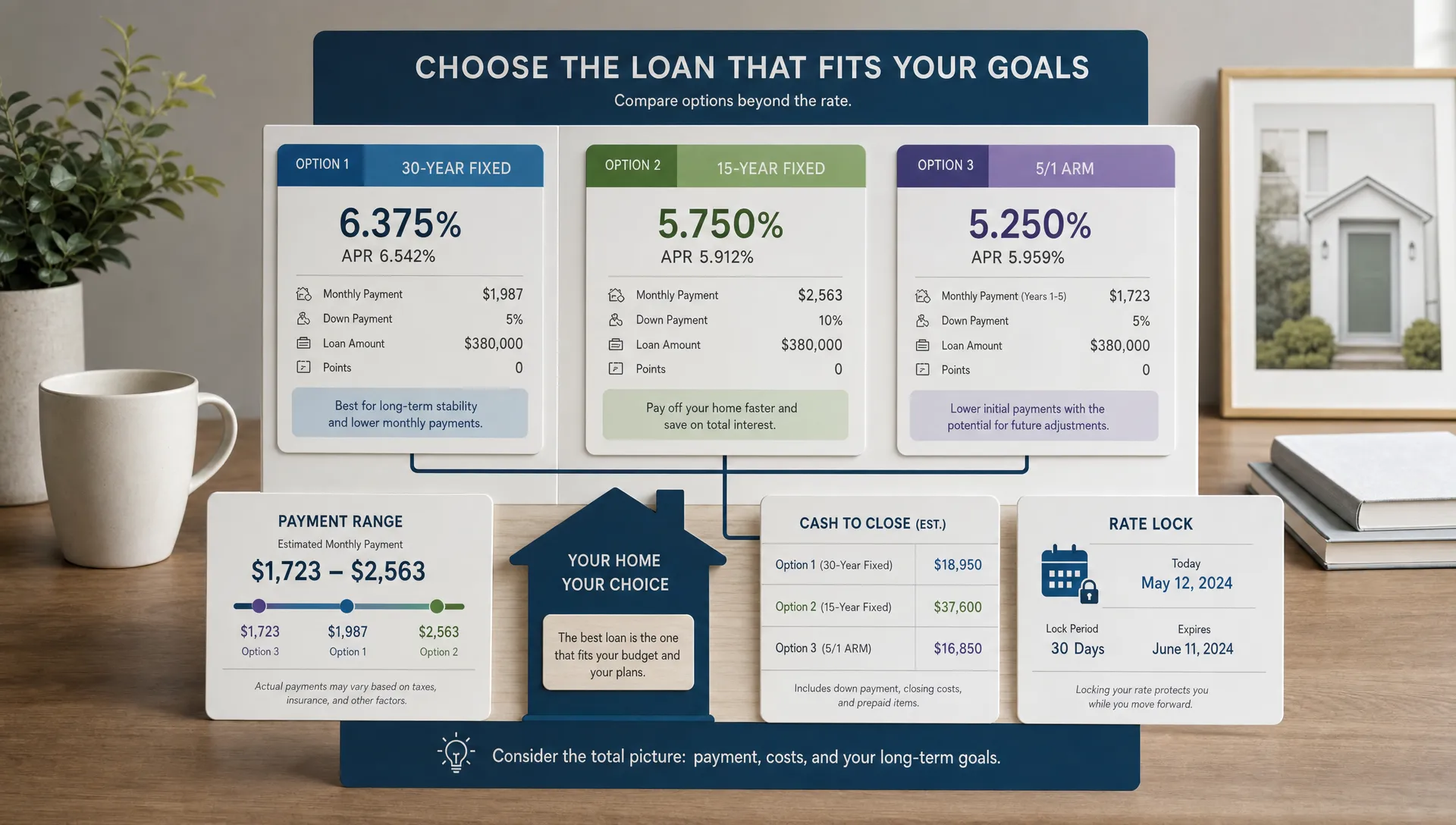

The 2026 decision framework: “Is it worth it?” (not “Did rates drop enough?”)

Old rules of thumb like “refinance when rates drop 1%” can be misleading because they ignore loan size, fees, and how long you will keep the mortgage.

A better approach in 2026 is:

- Define your goal.

- Calculate total refinance costs.

- Calculate monthly savings (or other benefit).

- Compare that benefit to your expected time in the home.

Start with break-even math

Break-even answers: How many months will it take for savings to exceed closing costs?

A simplified way to estimate:

Break-even months = Total refinance costs ÷ Monthly payment savings

Example:

- Total refinance costs: $5,000

- Monthly savings: $200

- Break-even: 25 months

If you plan to move in a year, this probably does not work. If you plan to stay 5 to 10 years, it might.

Here is a quick reference table to help you interpret results.

Break-even timeline | What it usually means | Typical next step

Under 18 months | Strong candidate (if loan terms fit your goals) | Compare 2 to 3 Loan Estimates and lock strategy

18 to 36 months | Situational | Consider how long you will keep the loan and whether you are resetting the term

Over 36 months | Often not worth it for payment savings alone | Explore alternatives (recast, extra payments, HELOC) When to refinance in 2026: the most common “green light” scenarios

1) You can lower your payment and you will keep the home long enough

This is the classic refinance. It tends to work best when:

- Your rate drops meaningfully or you can remove expensive mortgage insurance.

- Closing costs are reasonable relative to your loan size.

- You expect to keep the mortgage past the break-even point.

If you are unsure about closing costs, New Era Lending has a helpful primer on what fees to expect: Closing Costs: The Fees Nobody Tells You About.

2) You want to shorten your term (pay off faster) without a payment shock

If your income has increased since you bought the home, a shorter-term refinance can reduce total interest paid. The decision is mostly about cash flow comfort, not just rate.

Two things to watch:

- Do not compare only the rate. Compare total interest over time and the payment difference.

- Avoid stretching your payoff date unintentionally. If you have already paid 6 years on a 30-year loan and refinance back into a new 30-year, you may lower payment but increase lifetime interest unless you pay extra.

3) You have an adjustable-rate mortgage (ARM) and want stability

Even if the savings are modest, refinancing from an ARM to a fixed rate can make sense if you are buying peace of mind and predictable payments.

This is especially relevant if:

- Your ARM is approaching an adjustment date.

- You would struggle with payment volatility.

4) You can remove PMI or reduce mortgage insurance

Mortgage insurance is often the hidden lever that makes a refinance attractive.

Common examples:

- Conventional loan with PMI: If your home value increased and your balance dropped, you may be able to refinance into a new conventional loan without PMI (depending on equity, credit, and underwriting).

- FHA mortgage insurance: FHA monthly mortgage insurance can last for the life of the loan in many cases, depending on down payment and term. Some homeowners explore refinancing from FHA to conventional when credit and equity allow.

If you want a deeper overview of loan types, these New Era Lending resources can help:

- FHA vs. Conventional Loans: Which One Is Right for You?

- What Makes An FHA Loan Different From A Conventional Loan?

5) You need cash-out, but the math beats other debt options

A cash-out refinance replaces your mortgage with a larger loan and gives you the difference in cash. In 2026, it can be smart when the funds are used for:

- Home improvements that add value or reduce future costs

- Paying off significantly higher-interest debt (run the full numbers carefully)

But cash-out refinances can also increase risk because you are converting equity into debt secured by your home.

If your goal is flexible access to equity rather than replacing your first mortgage, a line of credit may be worth comparing. New Era Lending’s guide is a good starting point: An Overview of the HELOC System.

When refinancing is usually a “no” in 2026

Even with competitive refinance rates for mortgages, refinancing can backfire. Common red flags include:

You plan to move soon

If you sell before break-even, you may never recover closing costs.

You are “buying” the rate down with points you will not recoup

Discount points can be useful, but only if you keep the loan long enough. Ask the lender to show:

- The cost of points

- The payment difference

- The break-even timeline specifically for paying points

You are resetting the clock without realizing it

A lower payment can be tempting, but refinancing back into a new 30-year term after years of payments can increase lifetime interest. If your goal is payment relief, ask about:

- A shorter term option

- Making a small extra principal payment monthly

Your credit or equity is not where it needs to be (yet)

Sometimes the best move is a “pre-refi” plan:

- Clean up credit utilization

- Fix errors on your credit report

- Pay down revolving debt

- Build equity (or wait for appreciation)

Small improvements can meaningfully change your pricing.

How to compare refinance offers correctly (what to request in writing)

To evaluate lenders fairly, ask each lender for a Loan Estimate for the same scenario (same loan type, term, and lock period if possible). Then compare:

- Interest rate and APR

- Total lender fees (origination, points, underwriting)

- Third-party fees (appraisal, title, escrow)

- Prepaid items (insurance, taxes, daily interest)

- Whether escrow is required

A practical approach is to focus on the sections of the Loan Estimate that most affect your decision.

Loan Estimate area | Why it matters | What to look for

Loan Terms | Core pricing | Rate, loan amount, prepayment penalty (if any)

Projected Payments | Cash flow | Payment now vs later, especially for ARMs

Costs at Closing | Break-even | Lender fees vs third-party fees

APR | True comparison | Use it to compare offers with different fees Streamlined options for eligible homeowners

Depending on your current loan type, you may have streamlined refinance pathways (for example, VA IRRRL or FHA Streamline). Eligibility and rules vary, and not every situation qualifies, but they can reduce friction for some borrowers.

Veterans exploring refinance options may find this guide useful: How Veterans Can Optimize Every Benefit They’ve Earned.

Self-employed homeowners: prepare before you apply

If you are self-employed, documentation and income analysis can be the make-or-break factor. Before you start a refinance application, it helps to understand how lenders review income stability, write-offs, and debt-to-income ratio.

New Era Lending covers key prep steps here: How to Qualify For a Self-Employed Mortgage Loan.

A quick “When should I refi?” checklist for 2026

Use this as a practical filter before you spend time collecting quotes.

- You have a clear goal (lower payment, shorten term, remove mortgage insurance, switch from ARM, or cash-out for a specific use).

- You can estimate closing costs and compute break-even.

- You plan to keep the home and loan longer than the break-even timeline.

- Your credit and equity position support competitive pricing.

- You have compared offers using Loan Estimates (not just teaser rates).

How New Era Lending can help you decide with confidence

If you are trying to make sense of refinance rates for mortgages in 2026, the fastest path to clarity is usually a personalized comparison based on your current loan, estimated home value, credit profile, and goals.

New Era Lending combines technology with human guidance to help you evaluate refinance scenarios, review costs, and choose a structure that fits your budget. You can learn more or start the process at New Era Lending.