.jpg)

.jpg)

.jpg)

How to Shorten Your Loan Term Without Stress

Shortening your mortgage loan term can be one of the most powerful ways to reduce total interest and build equity faster. The stressful part is usually not the math. It is the fear of locking yourself into a higher payment, draining cash reserves, or making a refinance decision you later regret.

The good news: you do not have to choose between financial progress and breathing room. There are several ways to shorten your loan term while keeping your monthly budget manageable, and the right path depends on your rate, income stability, savings, and long-term plans for the home.

Below is a practical, low-pressure way to think through your options.

What It Really Means to Shorten Your Loan Term

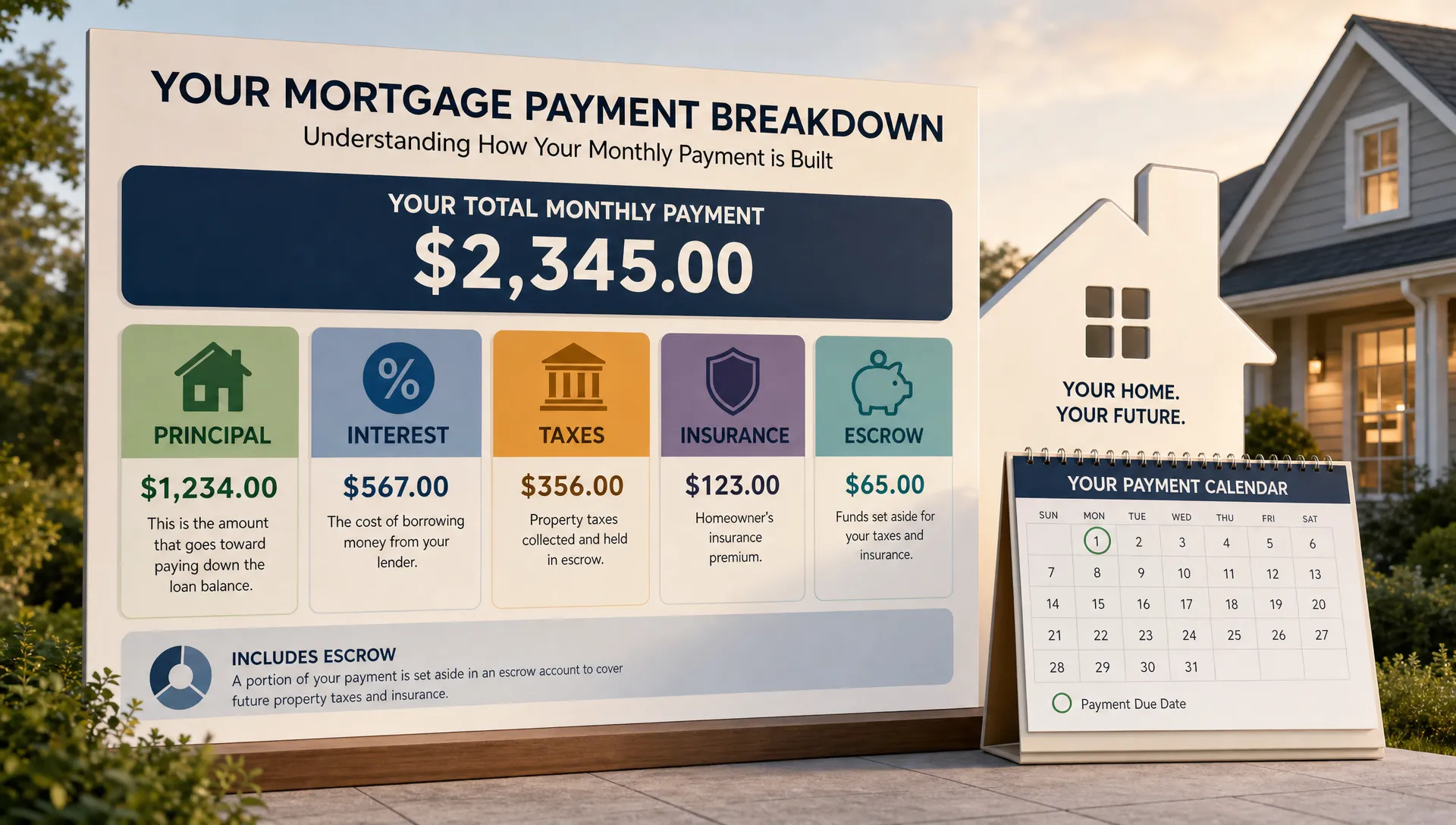

Your loan term is the length of time your mortgage is scheduled to take if you make the required payments. Common mortgage terms include 30, 20, and 15 years, although some lenders may offer other structures depending on the loan type and borrower profile.

To shorten the term, you generally need to do one of two things: pay down principal faster or refinance into a shorter repayment schedule. Both can work, but they feel very different in real life.

Extra principal payments give you flexibility because you can usually adjust or pause the extra amount when life changes. A shorter-term refinance can be more structured and may come with a lower rate, but it can also raise the required monthly payment. That is why the least stressful approach starts with your budget, not the payoff date.

Start With a Budget-Safe Payoff Goal

Before choosing a strategy, define what stress-free actually means for your household. A loan term that looks great on paper is not helpful if it leaves you anxious every month.

Focus on three numbers first:

- Your comfortable monthly housing payment: Include principal, interest, property taxes, homeowners insurance, mortgage insurance if applicable, HOA dues, and a cushion for increases.

- Your emergency reserve target: Many homeowners prefer to keep several months of essential expenses available before accelerating mortgage payoff.

- Your timeline goal: Decide whether you want to save a few years, cut the term in half, or simply avoid restarting a 30-year clock when refinancing.

This is where a data-driven mindset helps. Businesses often test scenarios before committing resources, and the same concept works for homeowners. Growth teams such as User Story use measurement and iteration to make smarter decisions, and borrowers can apply that same principle by modeling several payoff paths before changing their mortgage.

The point is not to make the most aggressive move. The point is to make a move you can sustain.

Option 1: Make Extra Principal Payments

The simplest way to shorten your loan term is to pay extra toward principal. You keep the same mortgage, the same required payment, and the same loan documents, but you reduce the balance faster.

This can be done in several manageable ways:

- Add a fixed amount each month, such as $50, $100, or $250.

- Round your payment up to the next comfortable number.

- Make one extra principal payment per year using a bonus, tax refund, or commission check.

- Apply small savings from canceled subscriptions, paid-off debts, or reduced insurance costs.

The key is making sure the extra money is applied to principal, not simply held as an early payment for the next month. Contact your mortgage servicer and confirm how to label extra payments correctly. You should also check whether your loan has any prepayment restrictions, although most standard residential mortgages do not penalize reasonable extra principal payments.

Here is a simple illustration. Suppose a homeowner has a $300,000 mortgage at 6.5% on a 30-year term. The principal and interest payment would be about $1,896 per month, not including taxes, insurance, or other costs. Adding $150 per month toward principal could reduce the payoff timeline by roughly five years and save a significant amount of interest over the life of the loan.

The exact result depends on your rate, balance, remaining term, and payment timing, but the lesson is clear: modest extra payments can matter.

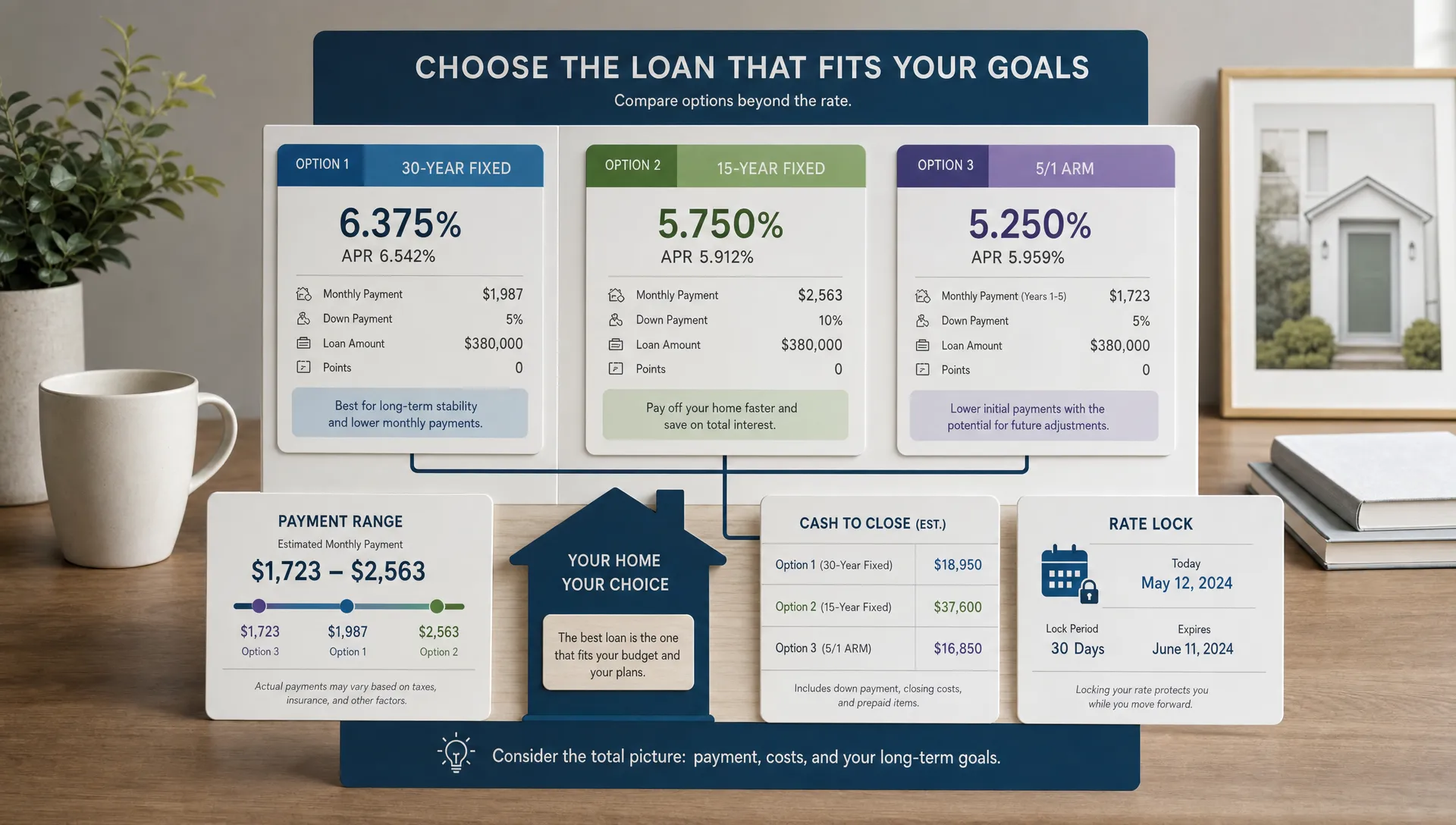

Option 2: Refinance Into a Shorter Term

A refinance can shorten your loan term more directly. For example, a homeowner might move from a 30-year mortgage to a 20-year or 15-year mortgage. This can be especially attractive if the new rate is competitive and the homeowner has enough income to handle the higher required payment.

But this is where stress can creep in. A 15-year mortgage can create meaningful interest savings, but the monthly payment may jump more than expected. If the new required payment stretches your budget too thin, the shorter term may not be worth the pressure.

A 20-year refinance can be a middle path. It may shorten the payoff timeline without increasing the payment as sharply as a 15-year loan. Some borrowers also consider custom-term options when available, especially if they want to avoid extending their payoff schedule.

When comparing refinance options, look beyond the rate. Review:

- Interest rate and APR

- Closing costs and lender credits

- Monthly principal and interest payment

- Total estimated interest over the new term

- Break-even point on refinance costs

- Whether mortgage insurance changes or can be removed

- How long you expect to keep the home

The Consumer Financial Protection Bureau explains that the Loan Estimate is designed to help borrowers compare mortgage offers more clearly. Use it to compare the same loan amount, term, and assumptions across options.

If you want a deeper look at refinancing for term reduction, New Era Lending also covers this topic in Mortgage Loan Refinance: Options to Lower Payment or Term.

Option 3: Refinance for a Better Rate, Then Keep Paying the Old Amount

Not every term-shortening refinance has to be a formal move into a 15-year loan. In some cases, homeowners refinance to a lower rate or better structure, then voluntarily keep paying the old monthly amount.

This approach can reduce stress because your required payment may be lower, while your chosen payment stays higher. If money gets tight, you may have the option to fall back to the required payment instead of being locked into a larger obligation.

For example, if your required payment drops by $200 after refinancing, you could continue paying the previous amount and direct the difference toward principal. Over time, that extra principal can shorten the effective payoff timeline.

This strategy works best when the refinance costs make sense. If the closing costs are high or you plan to sell soon, the math may not work. Always calculate the break-even point and compare the total cost, not just the monthly savings.

Option 4: Use a DIY Biweekly Payment Strategy

Biweekly mortgage payments are often marketed as an easy way to pay off your loan faster. The idea is simple: instead of making 12 monthly payments per year, you make half a payment every two weeks. Since there are 26 two-week periods in a year, this equals 13 full payments annually.

That extra payment can reduce principal and shorten the loan term. However, homeowners should be careful with third-party biweekly payment services that charge fees.

A simpler option is to divide one monthly principal and interest payment by 12, then add that amount to each monthly payment as extra principal. This creates a similar effect without needing a separate service.

Before doing this, confirm that your servicer applies the extra amount to principal and does not hold partial payments in a suspense account.

Option 5: Redirect Savings After Other Costs Drop

One of the least stressful ways to accelerate payoff is to wait for another expense to disappear, then redirect that money to your mortgage principal.

Common examples include:

- A car loan that gets paid off

- Credit card debt that has been eliminated

- Private mortgage insurance that is canceled

- A raise or income increase

- Reduced homeowners insurance after shopping policies

This works because your lifestyle does not have to change dramatically. You are simply reassigning money that was already leaving your budget.

If you recently removed mortgage insurance, for instance, you might apply the old PMI amount to principal each month. That can help shorten your loan term without increasing your total monthly outflow.

Option 6: Consider a Recast After a Large Principal Payment

A mortgage recast is different from a refinance. With a recast, you make a large principal payment, and the lender recalculates your monthly payment based on the lower balance and remaining term. Not all loans are eligible, and lender rules vary.

On its own, a recast usually lowers your required payment rather than shortening your loan term. But it can still support a stress-free payoff strategy.

Here is how: after the recast lowers your required payment, you keep paying the old amount if your budget allows. The difference goes toward principal, helping you pay off the loan faster while giving you a lower required payment as a safety net.

This can be useful after a bonus, inheritance, home sale proceeds, or other lump sum. It may also be attractive for homeowners who want flexibility but do not want to go through a full refinance.

What Not to Do When Trying to Shorten Your Term

Accelerating mortgage payoff can be smart, but only when it fits the rest of your financial life. Avoid turning a good goal into unnecessary stress.

Be cautious about these common mistakes:

- Draining your emergency fund: A paid-down mortgage is valuable, but it is not as liquid as cash in the bank.

- Ignoring high-interest debt: Credit cards and other high-rate debts may deserve attention before extra mortgage payments.

- Refinancing only for the shorter term: If the rate, fees, and payment do not make sense, the shorter term may be too expensive.

- Forgetting taxes and insurance: Even with a fixed-rate mortgage, escrowed taxes and insurance can rise over time.

- Paying for unnecessary acceleration services: You can often make extra principal payments yourself without a third-party program.

- Overcommitting during unstable income periods: If your income varies, flexibility may be more valuable than speed.

The healthiest payoff plan is one that survives real life.

A Simple Plan to Shorten Your Loan Term Without Pressure

If you are ready to take action, use this step-by-step framework.

- Find your current payoff baseline: Check your balance, interest rate, remaining term, monthly payment, and whether you have mortgage insurance.

- Choose a comfortable extra amount: Start small enough that you will not miss it, even during a busy or expensive month.

- Ask your servicer about principal payments: Confirm the exact process for applying extra funds to principal.

- Run refinance scenarios: Compare 30-year, 25-year, 20-year, and 15-year options if available, including closing costs and monthly payment impact.

- Protect your cash reserves: Keep enough savings for repairs, emergencies, and life changes before making aggressive principal payments.

- Review once a year: Revisit your income, rate environment, home value, mortgage insurance, and payoff goal.

For many homeowners, the best strategy is not one big move. It is a combination of small extra principal payments, smart refinancing only when the numbers work, and periodic adjustments as your finances improve.

How New Era Lending Can Help You Compare Term-Shortening Options

Shortening your mortgage term is easier when you can see the tradeoffs clearly. New Era Lending combines smart mortgage technology with personalized human guidance to help borrowers compare loan options, refinancing paths, rates, terms, and payments.

Whether you are considering a refinance, exploring equity access, buying a home, or simply trying to understand your current mortgage more clearly, the right guidance can help you avoid guesswork. Secure document uploads, e-signature support, transparent rate and term discussions, and educational resources can make the process feel less overwhelming.

If your goal is to pay off your home faster, the smartest question is not simply how fast can I do it. It is how fast can I do it comfortably.

Frequently Asked Questions

Can I shorten my loan term without refinancing? Yes. You can usually shorten your effective loan term by making extra principal payments on your current mortgage. Confirm with your servicer that extra payments are applied to principal.

Is a 15-year mortgage always better than a 30-year mortgage? Not always. A 15-year mortgage can reduce total interest, but it often comes with a higher required monthly payment. A 30-year loan with extra principal payments may offer more flexibility.

How much extra should I pay each month to shorten my loan term? The right amount depends on your budget, emergency savings, interest rate, and payoff goal. Even small amounts can help, but the best amount is one you can sustain consistently.

Should I refinance or just pay extra principal? Refinance may make sense if the new rate, term, closing costs, and monthly payment fit your goals. Paying extra principal may be better if you want flexibility or if refinance costs do not justify the change.

Will extra mortgage payments lower my monthly payment? Usually, extra principal payments shorten the payoff timeline but do not reduce your required monthly payment. A recast may lower the required payment if your loan is eligible and you make a qualifying lump-sum principal payment.

Is it smart to use savings to pay down my mortgage faster? It can be, but only after considering emergency reserves, higher-interest debt, retirement contributions, and upcoming expenses. Liquidity matters, especially for homeowners.

Ready to Explore a Shorter Loan Term?

You do not need to figure it out alone. New Era Lending can help you compare realistic mortgage scenarios, understand refinance options, and choose a payoff strategy that fits your budget instead of straining it.

Start with a personalized conversation at New Era Lending and see what a shorter, smarter path to homeownership could look like for you.