.jpg)

.jpg)

.jpg)

How to Lower Rates Without Hurting Your Budget

A lower mortgage rate can save you real money, but chasing the lowest number at any cost can backfire. Some “lower rate” offers require high upfront points, a larger down payment than you planned, or a loan structure that creates payment risk later. The better goal is not simply to make the rate look lower. It is to lower rates in a way that protects your cash flow, keeps your emergency savings intact, and fits the time you expect to own the home or keep the loan.

For buyers, refinancers, and homeowners tapping equity, the smartest strategy starts with one question: What is the lowest total-cost option that still leaves my budget healthy after closing?

Start With the Real Budget, Not Just the Rate

Mortgage shopping often starts with the interest rate, but your household budget cares about more than that. Your monthly payment may include principal, interest, property taxes, homeowners insurance, mortgage insurance, HOA dues, and sometimes escrow adjustments. A lower interest rate helps, but it does not automatically mean the loan is affordable.

Before comparing options, set a practical payment range. This should be based on your actual monthly life, not only what a lender may approve. Include groceries, utilities, car payments, childcare, retirement contributions, insurance, subscriptions, and a cushion for repairs or unexpected expenses.

A budget-safe mortgage plan should pass three tests:

- It leaves enough cash after closing for reserves and moving costs.

- It keeps the monthly payment comfortable under normal income and expense conditions.

- It avoids taking on future payment changes you do not understand or cannot absorb.

The Consumer Financial Protection Bureau recommends using the Loan Estimate to compare loan offers because it shows more than the rate. It also shows APR, projected payments, closing costs, and cash to close. That document is one of the best tools for spotting whether a “great rate” is really a good deal.

Know What Actually Makes Mortgage Rates Lower

Mortgage rates are influenced by the broader market, but your personal loan terms also matter. You cannot control inflation reports, bond yields, or lender pricing changes. You can control many of the factors lenders use to price your specific loan.

The most common borrower-level factors include credit profile, loan-to-value ratio, loan program, property type, occupancy, loan term, points, and debt-to-income ratio. A primary residence usually prices differently than an investment property. A borrower with stronger credit and lower debt may have more favorable options than someone with recent late payments or high revolving balances.

That does not mean you need a perfect financial profile to get a good loan. It means a small amount of preparation can sometimes improve your pricing before you apply or lock.

Improve Your Credit Without Overspending

Credit is one of the most important pricing factors for many mortgage programs. Improving your credit profile can help you qualify more smoothly and may help lower your rate or mortgage insurance cost. The key is to focus on moves that do not create new financial stress.

Start by checking your credit reports early. You can access free reports through AnnualCreditReport.com, the federally authorized source for free credit reports. Look for errors, unfamiliar accounts, incorrect late payments, or balances that have already been paid down. If something is wrong, dispute it before you are deep into a purchase or refinance timeline.

Next, focus on revolving balances. Paying down credit cards can sometimes improve credit utilization, which may help your score. But avoid draining your cash reserves to chase a small score change. If paying down a balance leaves you short on closing costs or emergency savings, it may hurt the bigger picture.

Also avoid opening new credit before or during the mortgage process. New accounts can change your credit profile, add inquiries, and create documentation issues. Even “same as cash” furniture financing can complicate underwriting if it appears before closing.

Lower Debt-to-Income Ratio the Smart Way

Your debt-to-income ratio, often called DTI, compares monthly debt obligations to qualifying income. A lower DTI can strengthen your application and may expand your loan options. But not every debt payoff strategy is budget-friendly.

For example, paying off a small installment loan with only a few payments remaining may not always help enough to justify using your cash. Paying down a high credit card minimum might help more. The right move depends on how the debt reports, how the lender calculates it, and how much cash you need for closing.

A loan officer can help you identify which debts matter most before you move money. Sometimes the best strategy is not “pay off everything.” It may be “pay down the account that improves both credit utilization and monthly obligations while preserving reserves.”

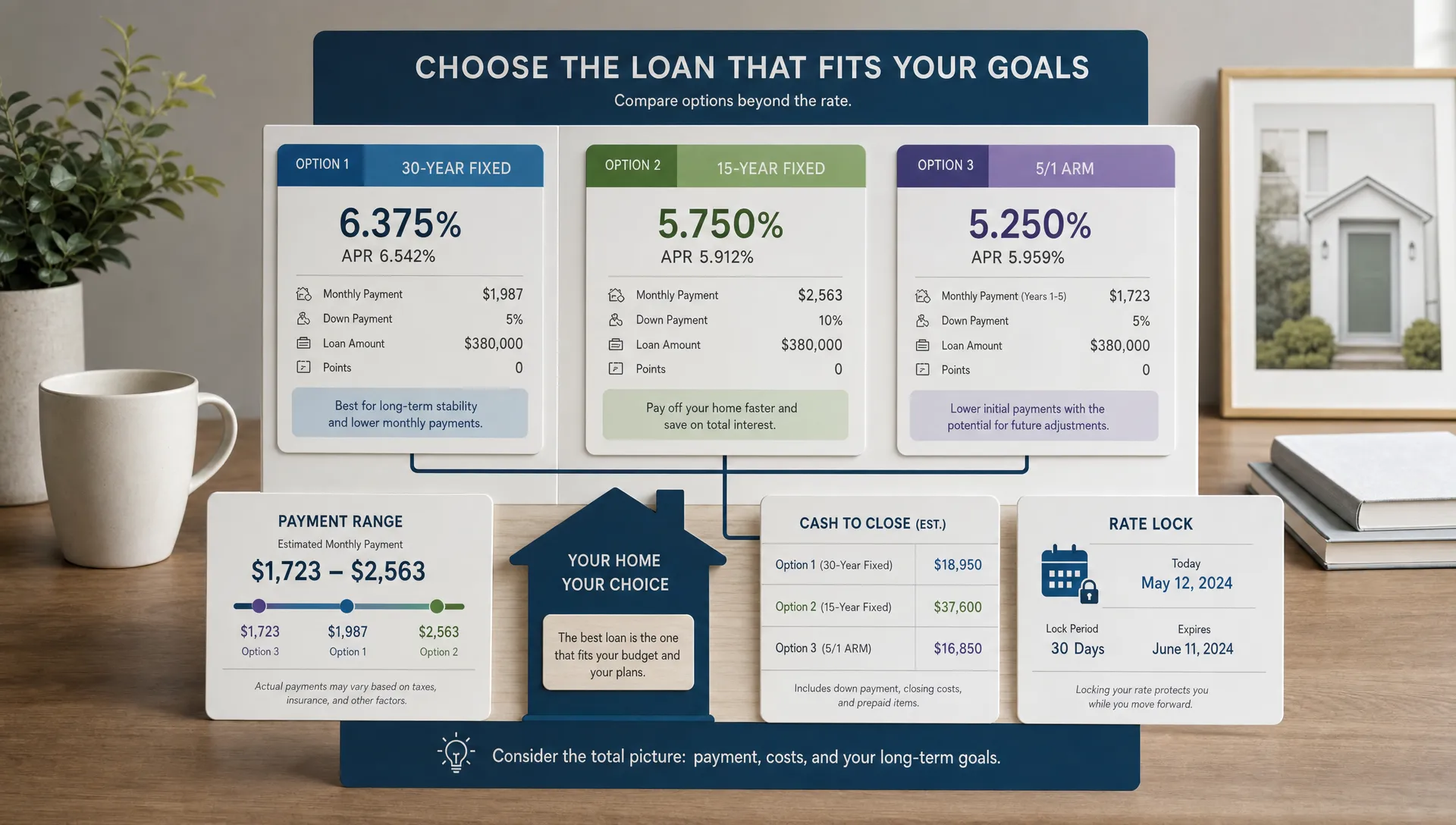

Compare Loan Programs, Not Just Lenders

A lower rate may be available through a different loan program, but the program must fit your situation. Conventional, FHA, VA, USDA, jumbo, and other loan types can price differently and carry different mortgage insurance rules, fees, and eligibility requirements.

For example, an FHA loan may help a buyer with limited down payment or less-than-perfect credit, but FHA mortgage insurance can affect the monthly and long-term cost. A VA loan may be powerful for eligible veterans and service members because it typically does not require monthly mortgage insurance, though the VA funding fee and eligibility rules still need to be considered. A conventional loan may be attractive for borrowers with stronger credit and enough equity or down payment to manage PMI costs.

The point is simple: the lowest interest rate on one program is not always the lowest total-cost option. Compare the full monthly payment, upfront costs, mortgage insurance, cash to close, and future flexibility.

Be Careful With Discount Points

Discount points let you pay upfront to reduce the interest rate. They can be useful, but only when the math works for your timeline and budget.

A simple way to evaluate points is to calculate your break-even period. Divide the upfront cost of the points by the estimated monthly savings. If points cost $4,000 and save $100 per month, the break-even period is 40 months. If you expect to sell, refinance, or pay off the loan before then, the points may not be worth it.

Points can be especially tempting when rates feel high. But using cash to buy down the rate can hurt your budget if it leaves you with too little money after closing. A slightly higher rate with lower upfront costs may be the better choice if it preserves liquidity.

This is where APR can help, but it should not be your only decision tool. APR includes certain loan costs and spreads them over the loan term, which can be useful for comparing offers. However, if you will not keep the loan for the full term, APR may not reflect your real-world outcome. Always pair APR with break-even math and your expected time horizon.

Use Seller Credits and Temporary Buydowns Thoughtfully

If you are buying a home, seller credits may help cover closing costs or fund certain rate strategies, depending on loan program rules and transaction details. This can reduce the amount of cash you need at closing, which may protect your budget.

Temporary buydowns can also lower the payment for the first one, two, or three years, depending on the structure. They may be useful if you expect income to rise or want a softer landing into homeownership. But they are not the same as permanently lowering your rate. You need to be comfortable with the full payment after the buydown period ends.

A permanent buydown lowers the note rate for the life of the loan, while a temporary buydown subsidizes early payments. Both can be helpful in the right situation, but both should be reviewed against your cash flow, time horizon, and risk tolerance.

Consider the Loan Term Carefully

Shorter loan terms often come with lower rates, but they usually have higher monthly payments because the loan is repaid faster. A 15-year mortgage may save interest over time, but it can strain the monthly budget if the payment is too aggressive.

A longer term may have a higher rate, but a lower required payment. That can preserve monthly flexibility. Some borrowers choose a 30-year term and make extra principal payments when cash flow allows. This can provide flexibility, though it requires discipline and does not produce the same guaranteed payoff schedule as a shorter term.

The best term is not always the one with the lowest rate. It is the one that balances interest savings, payment comfort, and financial resilience.

Do Not Ignore Adjustable-Rate Mortgages

Adjustable-rate mortgages, or ARMs, may start with a lower rate than fixed-rate loans in some markets. They can make sense for borrowers who expect to sell, refinance, or pay off the loan before the adjustment period begins. But they are not right for everyone.

The budget risk is future uncertainty. If the rate adjusts upward later, your payment may increase. Before choosing an ARM, understand the initial fixed period, adjustment frequency, margin, index, caps, and maximum possible payment.

An ARM may be budget-friendly only if you have a clear exit plan or enough income flexibility to handle future changes. If a payment increase would create stress, a fixed-rate loan may be the safer choice even if the starting rate is higher.

Watch the Tradeoff Between Down Payment and Cash Reserves

A larger down payment may lower your loan amount, reduce mortgage insurance, improve loan-to-value ratio, and sometimes help pricing. But putting every available dollar into the down payment can leave you “house poor.”

Cash reserves matter. New homeowners often face moving expenses, furniture needs, repairs, utility deposits, and maintenance surprises. Homeowners refinancing may need funds for future tax or insurance increases, repairs, or income interruptions.

Instead of assuming the largest down payment is best, compare several scenarios. Look at 3 percent, 5 percent, 10 percent, 20 percent, or other relevant options based on your loan program. The right answer is often the point where the monthly savings are meaningful but your post-closing cash remains strong.

Lock the Rate Based on Your Timeline

Mortgage rates can change quickly. A rate lock protects your rate for a set period while your loan moves toward closing. The right lock strategy depends on your closing timeline, market volatility, and loan complexity.

Locking too short can create extension costs if the file is delayed. Locking too long may cost more upfront or price slightly differently. Floating the rate may help if rates improve, but it also exposes you to increases.

A budget-conscious lock strategy starts with realistic timing. If your transaction involves an appraisal, title work, condo review, self-employed income, gift funds, or property repairs, build in enough time. Saving a small amount on the rate is not helpful if a rushed lock creates avoidable stress or costs.

Compare Loan Estimates Side by Side

Advertised rates can be misleading because they may assume a specific credit score, loan amount, down payment, property type, occupancy, and points. Personalized Loan Estimates are much more useful.

When comparing offers, make sure the scenarios match. The loan amount, property value, down payment, loan term, lock period, points, and occupancy should be the same. If one quote includes points and another does not, the rate comparison is not apples to apples.

Focus on these items:

- Interest rate and APR

- Monthly principal and interest payment

- Mortgage insurance, if applicable

- Total estimated monthly payment

- Discount points and lender fees

- Third-party closing costs

- Cash to close

- Rate lock period

Do not choose a lender based only on the lowest rate quote. Execution matters too. A lender who communicates clearly, anticipates documentation issues, and closes on time can protect you from costly delays.

Refinance Only When the Savings Fit the Costs

If you already own a home, refinancing may help lower your rate or payment. But it should be measured against closing costs and your expected time in the home.

The basic break-even formula is simple: divide the refinance costs by the monthly savings. If the refinance costs $5,000 and saves $200 per month, the break-even period is 25 months. If you plan to keep the loan longer than that, the refinance may be worth considering. If you expect to sell soon, it may not.

Also look at the loan term. Refinancing into a new 30-year loan may lower the monthly payment, but it can extend repayment and increase total interest over time. That may still be the right move if cash flow relief is the goal, but you should understand the tradeoff.

For homeowners with mortgage insurance, a refinance may also help remove or reduce it if equity and program rules allow. In some cases, that can improve the monthly payment even if the rate change is modest.

Avoid “Lower Rate” Moves That Quietly Hurt Your Budget

Some strategies make the rate look better but weaken your financial position. The danger is not always obvious at first because the payment may look attractive on paper.

Be cautious if a lower-rate option requires you to empty savings, accept a payment that only works under perfect conditions, rely on future refinancing as the only plan, or ignore large closing costs. Also be careful with debt consolidation refinances if you do not have a plan to avoid rebuilding the same credit card balances later.

A lower rate should create more stability, not less. If the strategy increases risk, reduces liquidity too much, or depends on assumptions you cannot control, it may not be the right fit.

A Practical Step-by-Step Plan to Lower Rates Safely

You do not need to master every mortgage detail before speaking with a lender. But a little preparation can put you in a stronger position.

Start by defining your maximum comfortable monthly payment and ideal cash reserve after closing. Then gather your income, asset, and debt information so your loan scenarios are accurate. Review your credit reports, avoid new debt, and ask your loan officer which actions could improve pricing without hurting cash flow.

Next, compare multiple loan structures. That may include fixed-rate options, ARMs, different down payments, points versus no points, lender credits, seller credits, or refinance terms. The goal is to see the tradeoffs clearly before committing.

Finally, choose the option that fits your real timeline. If you may sell or refinance within a few years, avoid overpaying upfront for long-term savings you may never use. If you plan to stay long term, a permanent rate reduction may be more valuable.

How New Era Lending Helps You Compare Options Clearly

New Era Lending combines smart mortgage technology with human guidance to help borrowers evaluate home purchase, refinance, and equity-access options. That matters because lowering a rate is not just a math problem. It is a personal financial decision involving payment comfort, cash to close, timeline, and risk.

With secure document uploads, e-signature support, transparent rates and terms, and personalized loan guidance, New Era Lending helps borrowers compare realistic scenarios instead of guessing from advertised rates. Whether you are buying your first home, refinancing an existing mortgage, or exploring ways to access home equity, the right loan strategy should make your finances clearer, not more complicated.

Frequently Asked Questions

Is the lowest mortgage rate always the best deal? No. The lowest rate may come with higher points, fees, or cash-to-close requirements. Compare the full Loan Estimate, including APR, closing costs, monthly payment, and break-even period.

Can I lower my rate without paying points? Sometimes. Improving credit, lowering debt, adjusting down payment, choosing the right loan program, or comparing lenders may help. Whether those options are available depends on your full borrower profile and market conditions.

Are discount points worth it? Points may be worth it if you can afford the upfront cost and expect to keep the loan long enough to recover that cost through monthly savings. If the break-even period is longer than your expected timeline, points may not make sense.

Will a bigger down payment always get me a lower rate? Not always. A larger down payment can help in some cases, especially by reducing loan-to-value or mortgage insurance, but it may not produce enough savings to justify using too much cash. Compare scenarios before deciding.

Should I refinance as soon as rates lower? Not automatically. A refinance should be based on your monthly savings, closing costs, break-even point, loan term, and how long you plan to keep the home or mortgage.

How can I protect my budget while shopping for a mortgage? Set a comfortable payment range first, preserve emergency savings, compare Loan Estimates, ask about points and credits, and choose a loan structure you can afford now and later.

Lower Your Rate the Smart Way

A better mortgage rate should support your financial goals, not squeeze your budget. Before you commit to points, a different loan term, an ARM, or a refinance, compare the full picture.

If you want clear, personalized mortgage scenarios, connect with New Era Lending. Our team can help you review your options, understand the tradeoffs, and choose a path that fits your budget with confidence.