.jpg)

.jpg)

.jpg)

Smart Mortgage Solutions for Modern Homebuyers

Buying a home today is not just about finding a house and choosing a rate. Modern homebuyers are balancing changing market conditions, tighter budgets, faster offer timelines, digital paperwork, and more loan choices than ever before. That is where smart mortgage solutions make a real difference.

A smart mortgage solution is not simply an online application. It is a more connected way to finance a home, one that uses secure technology to reduce friction, clear comparisons to support better decisions, and experienced human guidance to help you avoid expensive mistakes.

For buyers, the goal is simple: understand what you can afford, compare realistic loan options, move quickly when the right home appears, and close with confidence.

What makes a mortgage solution “smart”?

A mortgage becomes smarter when it is built around your actual life, not a generic loan quote. Two buyers can have the same purchase price and still need very different mortgage strategies because their income, credit, savings, timeline, and future plans are different.

Smart mortgage solutions usually combine five things:

- Personalized loan guidance that accounts for your budget, credit profile, down payment, property type, and goals.

- Digital convenience such as secure document uploads, e-signatures, and streamlined communication.

- Transparent comparisons that show payment, rate, APR, cash to close, mortgage insurance, and closing costs.

- Program flexibility across common loan options such as conventional, FHA, VA, USDA, jumbo, refinance, and equity-access products when eligible.

- Human expertise from a mortgage professional who can explain tradeoffs, flag underwriting issues early, and help you choose a path that fits.

Technology can make the mortgage process faster and easier, but the smartest approach still includes a person who understands how loan guidelines apply to your situation. A strong digital system can collect information efficiently. A strong loan officer can help interpret it.

Why modern homebuyers need a better mortgage experience

Home financing has always required documentation and careful review, but today’s buyers face added pressure. Homes can move quickly. Rates can shift. Household budgets are sensitive to property taxes, insurance premiums, HOA dues, and mortgage insurance. Many buyers also have income profiles that do not fit a simple W-2 template, such as self-employment, commission income, bonus income, or multiple income sources.

A less organized mortgage process can leave buyers guessing. They may know the rate but not the full monthly payment. They may have a pre-qualification that has not been reviewed deeply enough. They may compare two offers without realizing one has points, higher fees, or different assumptions.

The Consumer Financial Protection Bureau encourages borrowers to use the Loan Estimate to compare offers because it standardizes key costs and terms. That is important because a mortgage decision should not be based on one number alone. The lowest advertised rate is not always the lowest-cost option, and the lowest monthly payment is not always the best long-term fit.

Smart mortgage solutions help turn scattered information into a clear picture.

The key ingredients of a smarter home loan strategy

A mortgage strategy should answer more than “Can I qualify?” It should help you understand what you can comfortably manage before, during, and after closing.

A pre-approval based on real numbers

A strong pre-approval looks beyond a rough estimate. It should consider income, assets, credit, debt-to-income ratio, loan program fit, and available cash for down payment and closing costs. For buyers in competitive markets, this can matter because sellers and real estate agents want confidence that financing is realistic.

This is also where guidance matters. Being approved for a certain amount does not automatically mean that amount is comfortable. A smart lender helps you separate maximum approval from sustainable affordability.

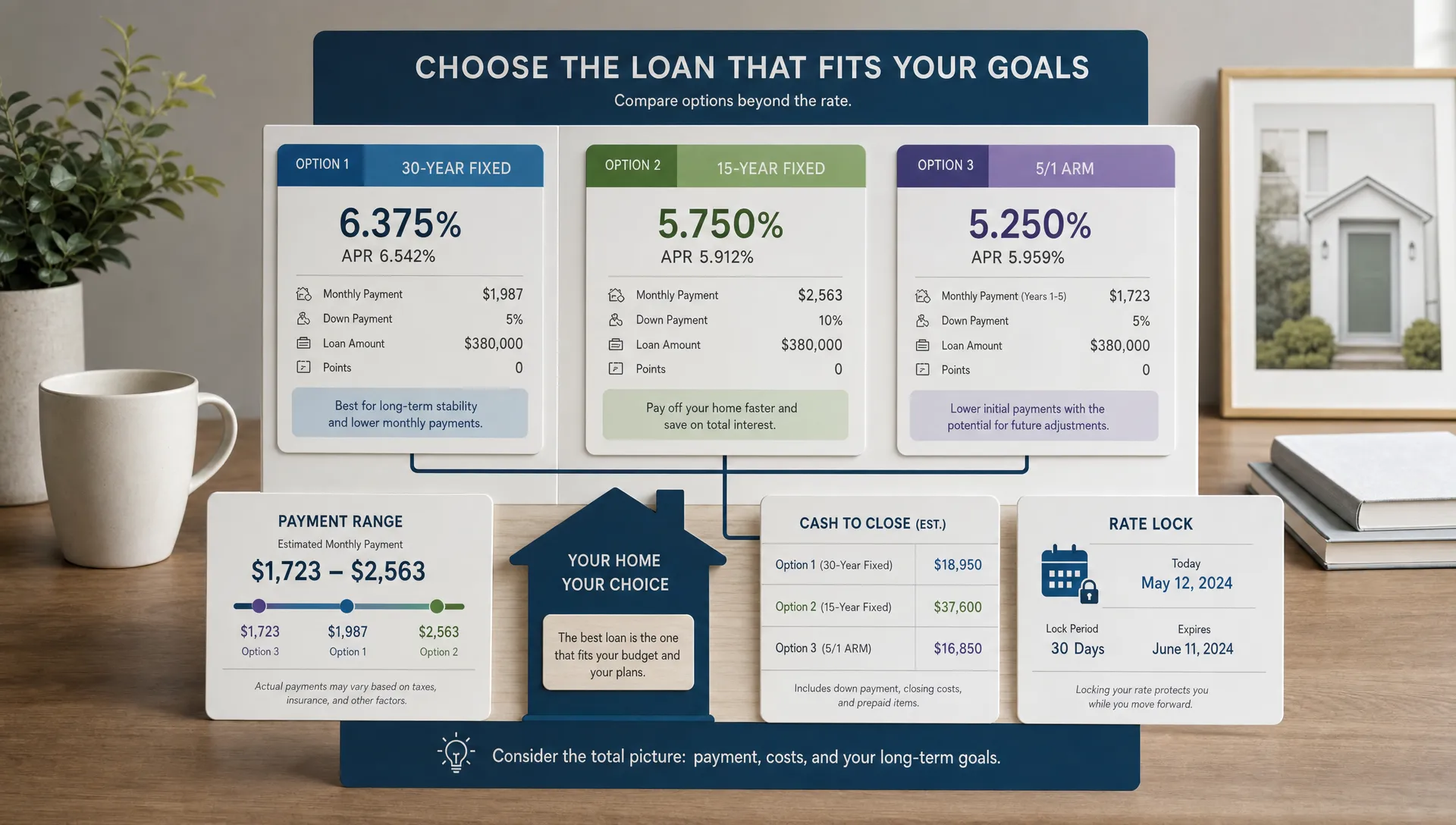

Side-by-side loan comparisons

Many buyers qualify for more than one loan program. For example, one buyer might compare conventional and FHA financing. An eligible veteran might compare VA and conventional options. A buyer in a rural area may want to understand whether USDA financing is possible.

The right question is not “Which loan is best overall?” The better question is “Which loan is best for this buyer, this property, and this timeline?”

If you want a deeper breakdown of major program types, New Era Lending’s guide to mortgage loan programs explains how FHA, VA, conventional, and other options compare.

Transparent payment planning

Your monthly mortgage payment can include principal, interest, property taxes, homeowners insurance, mortgage insurance, and HOA dues when applicable. A smart solution helps you look at the full housing payment, not just principal and interest.

This is especially important for first-time buyers who may be surprised by escrow changes, insurance costs, or mortgage insurance. A realistic payment estimate can help you shop for homes with more confidence and avoid stretching your budget too thin.

Secure digital document handling

Modern borrowers expect convenience, and mortgage technology can help. Secure uploads reduce the need for emailing sensitive documents. E-signatures can speed up disclosures and forms. Digital workflows can also make it easier to track what has been requested and what is still missing.

That convenience matters, but security and clarity matter too. A smart process should make it easier to complete tasks without leaving you wondering what comes next.

Early problem-solving

Some mortgage challenges are easier to fix before you make an offer. These can include documentation gaps, credit report issues, large deposits that need sourcing, income calculation questions, property eligibility concerns, or cash-to-close misunderstandings.

A smart mortgage process identifies potential issues early. That does not guarantee approval, since every loan is subject to underwriting and program guidelines, but it can reduce surprises and help buyers prepare a stronger file.

Smart mortgage solutions are not one-size-fits-all

The best mortgage strategy depends on the buyer. Here are a few examples of how different borrowers may benefit from a smarter, more personalized approach.

First-time homebuyers

First-time buyers often need help understanding the full cost of buying, including down payment, closing costs, prepaid expenses, mortgage insurance, and post-closing reserves. They may also benefit from learning about low down payment options or down payment assistance when available.

A smart approach helps first-time buyers move from “I think I can buy” to a clearer plan based on real numbers.

Move-up buyers

Move-up buyers may need to coordinate selling one home while buying another. They may be comparing a larger payment, a different school district, higher taxes, or whether to use proceeds from a sale for the next down payment.

For these buyers, timing and cash-flow planning are often just as important as rate.

Veterans and service members

Eligible veterans, active-duty service members, and certain surviving spouses may have access to VA home loan benefits. VA loans can offer major advantages for qualified borrowers, including the possibility of no down payment and no monthly mortgage insurance. The U.S. Department of Veterans Affairs provides an overview of VA home loan benefits on its VA housing assistance page.

Still, VA is not automatically the best option in every situation. Property requirements, funding fees, entitlement, and offer strategy can all affect the decision. New Era Lending offers specialized veteran loan programs and can help eligible borrowers compare VA options with other available paths.

Self-employed buyers

Self-employed borrowers may have strong businesses but more complex documentation. Lenders often review tax returns, profit and loss information, business history, and income consistency. A smart process helps self-employed buyers understand how income may be calculated before they are deep into a transaction.

That preparation can help reduce underwriting friction and make the buying process less stressful.

Buyers comparing speed and certainty

In a competitive market, the strength of your financing can influence your offer. A fast, organized mortgage process can help you respond quickly when the right home becomes available. Secure document uploads, e-signature support, and responsive guidance can all support a smoother path from pre-approval to closing.

For a step-by-step view of what happens after you apply, see New Era Lending’s guide to the mortgage loan process from start to closing.

How to evaluate smart mortgage solutions before you apply

Not every lender that uses technology offers a truly smart experience. Some platforms are fast but impersonal. Others offer guidance but rely on slow, outdated processes. The best fit usually blends both.

Before choosing a lender, ask yourself these questions:

- Will I receive personalized comparisons or only a single quote? A smart mortgage solution should help you understand multiple realistic options when available.

- Will I see the full cost picture? Look for payment, APR, closing costs, points, lender credits, mortgage insurance, and total cash to close.

- Can I upload documents securely? Avoid sending sensitive financial documents through unprotected channels.

- Will a loan professional review my situation? Technology is helpful, but human review can catch details that automated systems may miss.

- Does the lender explain tradeoffs clearly? You should understand why one option may be better than another.

- Can the lender support my specific loan need? Purchase, refinance, cash-out, equity access, and veteran programs may require different expertise.

If you want a broader checklist, New Era Lending’s article on questions to ask a home loan mortgage lender can help you compare lenders more confidently.

A practical framework for choosing the right path

A smart mortgage decision starts with clarity. Before you focus on a rate quote, define what you need the loan to accomplish.

- Set your comfort payment: Decide what monthly payment fits your life after accounting for savings, debts, utilities, maintenance, and lifestyle.

- Estimate your cash to close: Include down payment, closing costs, prepaid taxes and insurance, and reserves.

- Identify your main constraint: Your biggest factor may be credit, cash, income documentation, property type, timeline, or payment stability.

- Compare loan programs: Review the options you may qualify for and how each affects upfront cost, monthly payment, and long-term cost.

- Review the Loan Estimate carefully: Compare rate, APR, points, lender fees, third-party costs, escrow items, and cash to close.

- Choose based on the full picture: The smartest loan is the one that supports your goals, not just the one with the most attractive headline number.

This framework helps buyers avoid a common mistake: choosing a mortgage based only on rate. Rate matters, but it is only one piece of the decision.

Where New Era Lending fits in

New Era Lending is built for buyers who want a clearer, more modern home financing experience. The company combines smart mortgage technology with personalized human guidance to help borrowers purchase, refinance, or access home equity with more confidence.

That means borrowers can benefit from modern conveniences such as secure document uploads and e-signature support, while still having access to loan professionals who can explain options, compare scenarios, and help navigate the details. New Era Lending offers a wide range of loan options, transparent rates and terms, educational resources, and specialized veteran loan programs across 39 states.

For modern homebuyers, that combination matters. A mortgage is too important to treat like a simple online checkout, but it should not feel confusing, slow, or opaque either.

Frequently Asked Questions

What are smart mortgage solutions? Smart mortgage solutions combine digital tools, transparent loan comparisons, and human mortgage guidance to make the home financing process clearer, faster, and more personalized.

Is an online mortgage application enough? An online application can be helpful, but it is only one part of the process. Most buyers also benefit from expert guidance on loan options, documentation, affordability, rates, fees, and underwriting requirements.

How do I know which mortgage option is best for me? The best mortgage depends on your credit, income, down payment, property type, timeline, eligibility, and long-term plans. Comparing full Loan Estimates and reviewing scenarios with a loan professional can help you make a stronger decision.

Can smart mortgage technology help me close faster? It can support a faster process by making document collection, disclosures, communication, and signatures more efficient. Actual timing still depends on the loan file, appraisal, title work, underwriting, and program requirements.

Does New Era Lending help with more than home purchases? Yes. New Era Lending offers personalized mortgage solutions for home purchase, refinancing, and equity access, with technology-driven tools and human guidance.

Take the next step with a smarter mortgage plan

The right mortgage should help you move forward with clarity, not confusion. Whether you are buying your first home, moving up, using veteran benefits, refinancing, or exploring equity access, smart guidance can help you compare options and choose a path that fits your goals.

New Era Lending brings together modern tools, transparent terms, and experienced mortgage support to simplify the process. If you are ready to explore your options, visit New Era Lending and start building a mortgage plan designed around you.