.jpg)

.jpg)

.jpg)

Mortgage Loan Programs: Compare FHA, VA, Conventional and More

Most borrowers don’t get rejected because “they can’t afford a home.” They get stuck because they compare rates before they compare mortgage loan programs, and program fit determines everything that follows, down payment minimums, mortgage insurance, appraisal rules, and even how competitive your offer looks.

If you’re buying, refinancing, or tapping equity in 2026, use this guide as a plain-English map of the most common mortgage loan programs, who they’re built for, and what to watch in the fine print.

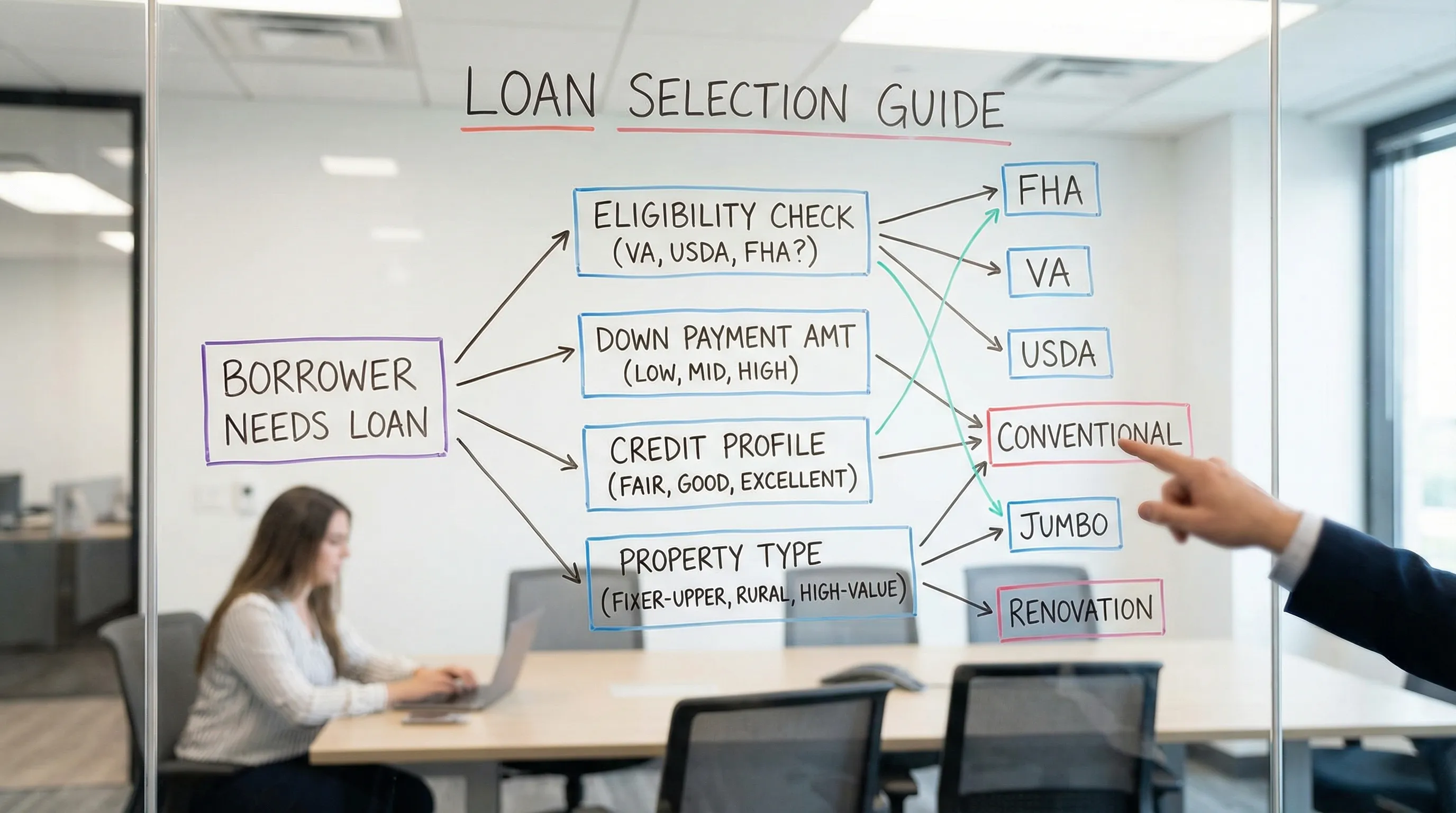

What “mortgage loan program” actually means

A mortgage loan program is the rulebook behind your loan. Two buyers can have the same interest rate quote but very different outcomes if one is using FHA and the other is using conventional.

When you compare programs, separate these three categories:

- Loan type (program): FHA, VA, USDA, conventional, jumbo, renovation, construction, etc.

- Rate structure: fixed-rate vs adjustable-rate mortgage (ARM), temporary buydowns, discount points.

- Occupancy and property: primary residence vs second home vs investment, condo vs single-family, 1–4 unit, manufactured homes.

Program fit is mostly about eligibility and total cost, not just the headline rate.

The major mortgage loan programs (quick orientation)

Here’s the practical “what it’s for” view:

- FHA loans: Flexible credit guidelines and lower down payments, with mortgage insurance required.

- VA loans: For eligible veterans, active-duty service members, and some surviving spouses, often 0% down and no monthly mortgage insurance.

- Conventional loans: The most common option for strong credit profiles, can be low down payment but may require PMI.

- USDA loans: 0% down for eligible rural and some suburban areas, with income and location limits.

- Jumbo loans: For loan amounts above conforming limits, usually tighter underwriting.

- Renovation and construction loans: Finance purchase plus improvements, or build a home, with more documentation and oversight.

FHA loans: flexible qualifying, but understand the mortgage insurance

Best for: Buyers with moderate credit, limited savings, or higher debt-to-income ratios, who still want a fixed payment and a predictable path to approval.

Key points to know:

- Down payment: FHA allows as little as 3.5% down with qualifying credit, according to the U.S. Department of Housing and Urban Development (HUD) program guidelines.

- Mortgage insurance: FHA charges an upfront mortgage insurance premium (UFMIP) and typically a monthly mortgage insurance premium (MIP). The exact cost depends on your loan details.

- Property standards: FHA appraisals can be stricter about safety and habitability issues because the loan is government-insured.

- Loan limits: FHA loan limits vary by county and are updated annually.

FHA can be a strong “first home” program, but the tradeoff is often the long-run cost of MIP. If your credit and equity improve later, refinancing out of FHA can be a strategy.

If you want a deeper side-by-side on just this decision, New Era Lending also breaks it down in FHA vs. Conventional Loans: Which One Is Right for You?

VA loans: powerful benefits for eligible borrowers

Best for: Eligible military borrowers who want maximum purchasing power and flexibility.

Why VA loans are unique:

- Often 0% down (down payment can be required in some scenarios).

- No monthly PMI (private mortgage insurance), which can materially reduce monthly payment.

- More flexible guidelines in some areas, including residual income concepts that consider real-life cash flow.

What to watch:

- Certificate of Eligibility (COE): You’ll need eligibility documentation through the VA.

- VA funding fee: Many VA loans include a funding fee (some borrowers are exempt). The VA explains funding fee rules and exemptions on its official resources.

- Offer strategy: A well-written VA offer can be very competitive, especially with a strong pre-approval and clean documentation.

New Era Lending has a dedicated overview for service members in How Veterans Can Optimize Every Benefit They’ve Earned

Conventional loans: the “default” option, with big advantages for strong credit

Best for: Borrowers with stronger credit, stable income, and the ability to document assets cleanly.

Conventional highlights:

- Low down payment options: Some conventional programs allow 3% down for qualified first-time buyers and other eligible scenarios.

- PMI is not forever: If you put less than 20% down, you’ll typically pay PMI, but unlike FHA mortgage insurance, PMI can often be removed when you reach certain equity thresholds.

- Property flexibility: Conventional loans commonly work well for condos (subject to eligibility), second homes, and some investment properties.

Important nuance: “Conventional” includes conforming loans that follow Fannie Mae and Freddie Mac guidelines. Conforming loan limits are updated annually by the Federal Housing Finance Agency (FHFA). If your loan amount exceeds those limits, you’re typically in jumbo territory.

USDA loans: 0% down for eligible areas and incomes

Best for: Buyers who want 0% down and are open to living in eligible locations.

USDA loans (Rural Development) can be surprisingly relevant even in suburban markets. The big gates are:

- Location eligibility: The property must be in an eligible area.

- Income eligibility: Household income limits apply.

- Fees: USDA loans typically have an upfront guarantee fee and an annual fee structure.

You can verify property eligibility using the USDA’s official eligibility tools and maps on the USDA Rural Development site.

Jumbo loans: for higher loan amounts and complex profiles

Best for: Buyers purchasing higher-priced homes who exceed conforming loan limits, or borrowers with strong assets but non-standard income.

Common jumbo underwriting expectations:

- Higher credit and reserve requirements: Many jumbo scenarios require stronger FICO scores and more months of cash reserves.

- Larger down payments may be needed: Not always, but it’s common.

- More documentation: If your income is variable (bonuses, commissions, self-employment), jumbo underwriting can be detail-heavy.

If you’re self-employed, preparation matters more than the label on the program. This guide can help you anticipate documentation: How to Qualify For a Self-Employed Mortgage Loan

Renovation and construction loans: when the property needs work (or doesn’t exist yet)

Best for: Buyers who want to buy a home that needs repairs, modernize after closing, or build new.

Two common renovation categories:

- FHA 203(k): A renovation loan backed through FHA guidelines that can finance purchase plus qualified improvements.

- Conventional renovation options: Such as Fannie Mae HomeStyle Renovation (availability depends on lender overlays and project details).

Construction financing often uses a construction-to-permanent structure (one loan that transitions from build phase to long-term mortgage) or a two-loan approach.

These programs can be excellent, but expect:

- Contractor bids, draw schedules, and inspections

- Longer timelines than a standard purchase

- More rules around what improvements qualify

Fixed vs ARM: rate structure changes your risk, not just your payment

Once you pick the right program, you still need the right rate structure.

- Fixed-rate mortgage: The rate and principal-and-interest payment stay the same for the loan term. This is the simplest for long-term planning.

- Adjustable-rate mortgage (ARM): The rate is fixed for an initial period, then adjusts based on an index plus a margin, subject to caps.

ARMs can be useful if you expect to sell or refinance before the adjustment period ends, but you should be comfortable with the worst-case payment under the caps.

Temporary strategies you may hear about:

- Discount points: Paying upfront to reduce the interest rate. Evaluate with breakeven math.

- Temporary buydowns (like 2-1 buydowns): A short-term payment reduction that steps up later. Make sure the future payment fits your budget.

For refinancing decisions and breakeven thinking, New Era Lending’s Refinance Rates for Mortgages: When to Refi in 2026 is a helpful companion.

How to choose the right mortgage loan program (a decision framework)

Instead of asking “What’s the best loan?” ask “What’s the best loan for my constraint?” Most borrowers have one primary constraint and one secondary constraint.

Start with your constraint

- Lowest cash to close: VA or USDA (if eligible) often lead, conventional low-down options can be next, FHA may be competitive depending on credit.

- Credit is the main issue: FHA often provides a clearer path, but compare the full mortgage insurance cost.

- Lowest long-term total cost: Conventional can win with strong credit and enough down payment to reduce or remove PMI.

- Property type is the issue (condo, multi-unit, fixer-upper): Program/property rules may narrow your choices quickly.

- Income is complex (self-employed, variable, multiple streams): Underwriting approach matters as much as the rate.

Then sanity-check the “real monthly payment”

Your payment is more than principal and interest:

- Property taxes

- Homeowners insurance

- Mortgage insurance (PMI or FHA MIP)

- HOA dues (if applicable)

A program that looks cheaper on rate can be more expensive after mortgage insurance is added.

How to compare lenders and offers correctly

When you apply, you’ll receive a Loan Estimate that standardizes key terms and costs. The Consumer Financial Protection Bureau (CFPB) provides a clear explainer of the Loan Estimate and how to use it for comparison.

When comparing two offers, focus on:

- APR vs interest rate: APR includes many financing costs, so it’s useful for comparison.

- Total cash to close: Not just down payment, also lender fees, title, escrows, and prepaid items.

- Mortgage insurance details: How much per month, and whether it can be removed later.

- Credits and points: Confirm whether a lower rate requires points, and whether lender credits are offsetting higher rates.

- Lock period: A great quote that expires in 7 days is not the same as a 30 or 45 day lock.

Don’t forget insurance and other “non-loan” costs

Mortgage approval is only one part of the affordability picture. Homeowners insurance (and sometimes flood insurance) is typically required by the lender, and it affects your monthly payment.

If you’re comparing coverage in other markets, it can help to use a platform designed for fast plan comparisons. For example, compare and buy insurance online if you need to shop home, life, or health coverage in the UAE.

How New Era Lending helps you navigate programs without the overwhelm

The fastest way to pick the right program is to narrow options based on your goals, then validate the numbers with a real pre-approval and a Loan Estimate review.

New Era Lending’s approach is built around making that process simpler, combining modern tools with personalized guidance. That means you can move through a tech-enabled mortgage process (including secure document uploads and e-signature support) while still having a human expert to help you:

- Match you to the right mortgage loan program for your credit, down payment, and property

- Run “what if” scenarios (payment, cash to close, mortgage insurance)

- Prepare clean documentation for smoother underwriting

If you’re ready to compare FHA, VA, conventional, USDA, jumbo, or renovation options based on your specific numbers, start with a pre-approval conversation through New Era Lending.