.jpg)

.jpg)

.jpg)

Mortgage Loan Refinance: Options to Lower Payment or Term

Most homeowners think of a refinance as “getting a lower rate.” That can be true, but a mortgage loan refinance can also change your loan term, remove mortgage insurance, stabilize an adjustable rate, or restructure payments to fit your budget and timeline.

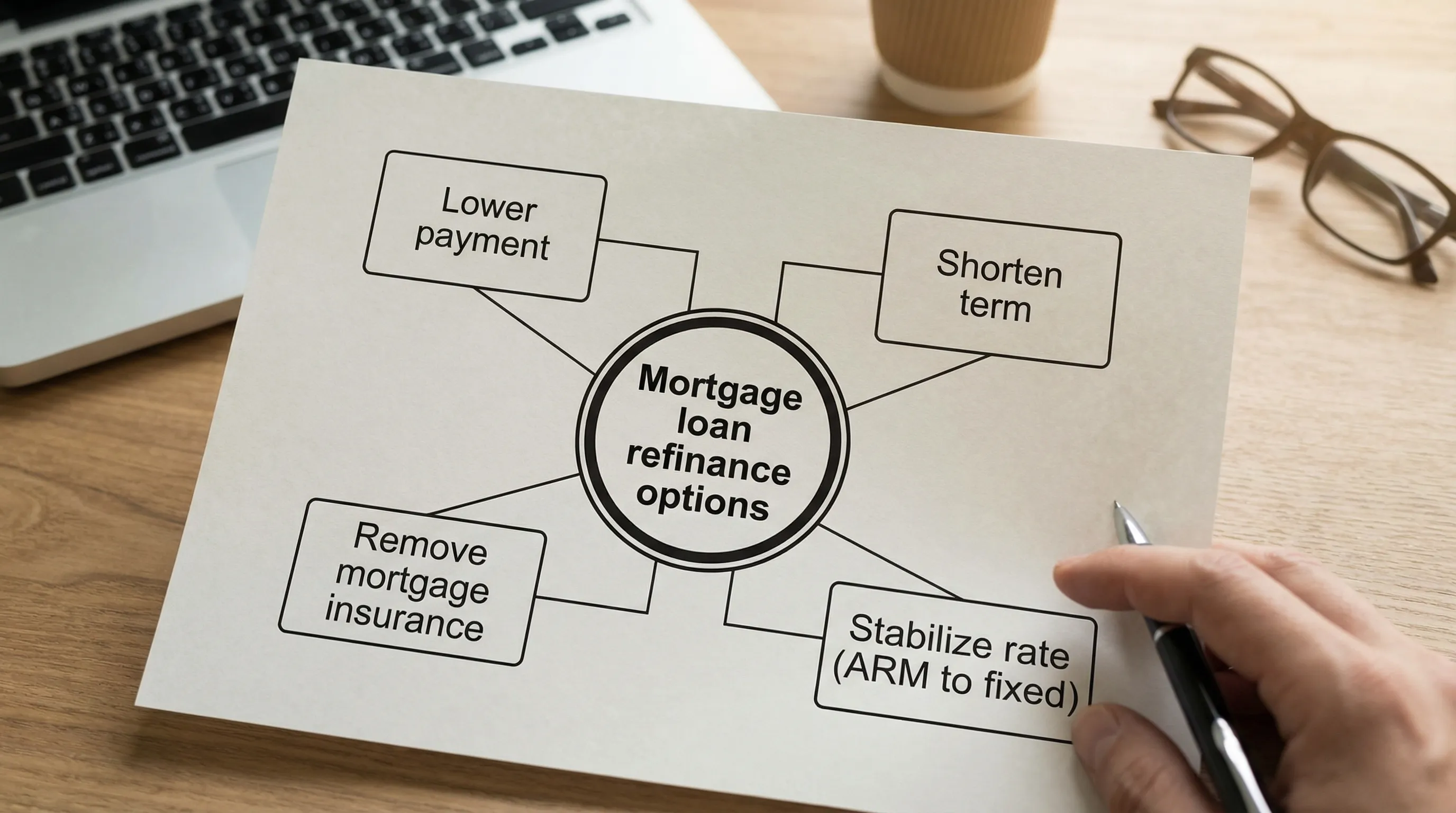

The key is matching the refinance type to your goal. “Lower payment” and “shorter term” are often competing outcomes, but with the right option, you can usually move closer to one without accidentally hurting the other.

What a mortgage loan refinance can (and can’t) change

Refinancing replaces your current mortgage with a new one. Depending on the program and your finances, a refinance may let you change:

- Interest rate (lower, or sometimes higher if you’re trading for a different benefit)

- Loan term (for example, 30-year to 20-year, or 30-year to 15-year)

- Rate structure (ARM to fixed, or fixed to ARM)

- Mortgage insurance (remove PMI by moving to a new conventional loan if equity supports it)

- Monthly payment (down or up, depending on the choices you make)

In most cases, refinances fall into two buckets:

- Rate-and-term refinance: You’re primarily changing rate and/or term, not taking significant cash out.

- Cash-out refinance: You increase the loan amount and receive cash at closing (useful sometimes, but it can work against the goal of paying less overall).

If your headline goal is “lower payment or term,” you’re usually looking at rate-and-term options first.

Options to lower your monthly payment

Lowering payment is not just “wait for rates to drop.” There are several levers, and the best one depends on how long you plan to keep the home and what tradeoffs you can accept.

1) Lower the rate (classic payment-focused refinance)

When you reduce the interest rate and keep a similar term length, your monthly principal-and-interest payment often drops.

Two details matter in real life:

- Your break-even point: If closing costs are $X, how many months of savings does it take to recoup them?

- APR vs. interest rate: APR includes many upfront costs, which helps you compare offers that use points or lender credits. The Consumer Financial Protection Bureau (CFPB) has a clear explainer on how to read a Loan Estimate.

2) Extend the term (payment drops, total interest usually rises)

If you refinance from a remaining 22 years back into a new 30-year term, your payment can drop even if the rate reduction is modest.

This option is most helpful when:

- Cash flow is tight and you need breathing room.

- You plan to pay extra principal once you stabilize, to avoid staying in a 30-year payoff track.

The common pitfall is forgetting that “lower payment” can mean paying interest for longer. If you extend the term, consider setting an automatic extra-principal amount so you keep momentum.

3) Remove monthly mortgage insurance (PMI or FHA MIP impact)

Mortgage insurance can be a major part of your payment.

- Conventional PMI: Many borrowers can remove PMI without refinancing once they reach the required equity threshold, but a refinance can help if your home value increased and you want to reset the loan based on a new appraisal.

- FHA MIP: FHA mortgage insurance often lasts much longer than people expect, sometimes for the life of the loan depending on the original down payment and term. In those cases, refinancing from FHA to conventional (if you qualify) can be a meaningful payment reduction.

If mortgage insurance is part of your refinance math, it’s worth reading the details carefully and comparing scenarios rather than guessing. If you want a quick refresher on loan program differences, New Era Lending also covers the basics in their FHA vs. conventional overview.

4) Switch from an ARM to a fixed rate (stability can be the “savings”)

If you have an adjustable-rate mortgage and the rate is about to reset, refinancing into a fixed rate may protect you from payment shock. Even if the new fixed rate isn’t dramatically lower than today’s ARM rate, locking the payment can be the biggest win.

This is less about “lowest possible payment this month” and more about predictability, especially if your budget cannot absorb future increases.

5) Consider a “no-cost” refinance (often lender-credit structured)

A “no-cost refinance” usually means you’re not paying closing costs out of pocket. In exchange, you may accept a slightly higher rate and receive a lender credit that covers some or most fees.

This can make sense when:

- You expect to sell or refinance again sooner.

- You want payment relief without writing a large check at closing.

The right way to evaluate this is to compare two scenarios side by side (lower rate with costs vs. higher rate with lender credit) and calculate how long you’d need to keep the loan for the lower-rate option to win.

Options to shorten your term (and usually cut total interest)

If your priority is paying the home off sooner, the “best” refinance is the one that shortens the payoff timeline without creating an unsustainable payment.

1) Refinance into a shorter term (15-year or 20-year)

A 15-year fixed mortgage often comes with a lower interest rate than a 30-year, but the payment can be significantly higher because you’re repaying principal faster.

A middle-ground option is often a 20-year term, or even a 25-year term (depending on what’s available), which can reduce total interest without the jump of a 15-year payment.

2) Keep a 30-year term, but pay it like a 15-year

Sometimes the best “term refinance” is actually a rate refinance.

If you lower your rate but keep a 30-year term, you can:

- Keep the required payment manageable.

- Make an additional principal payment monthly to mimic a shorter amortization.

This approach offers flexibility. If life changes (job transition, medical expense, childcare costs), you can temporarily fall back to the required payment without risking late payments.

3) Use a recast (not a refinance) when the rate is already great

If you already have a low rate and you make a large principal payment (for example, after a bonus or selling another property), some servicers allow a mortgage recast. A recast keeps your existing interest rate and term, but reduces the monthly payment by re-amortizing the balance.

It’s not available on every loan, and it typically requires a fee and a minimum principal reduction. But it can be a strong alternative when your rate is a “keeper” and you simply want a lower payment.

Streamline refinance programs (VA and FHA)

For eligible homeowners, streamline programs can reduce paperwork and speed up the process.

VA IRRRL (Interest Rate Reduction Refinance Loan)

If you have a VA loan, the VA IRRRL is designed to refinance into another VA loan with less friction. In many cases it’s used to lower the rate and payment, or move from an ARM to a fixed rate. The VA also applies a “net tangible benefit” concept, meaning the refinance should generally improve the borrower’s position.

New Era Lending has veteran-focused resources if you want to go deeper into VA strategy, including refinance options like IRRRL and cash-out: How Veterans Can Optimize Every Benefit They’ve Earned.

FHA Streamline Refinance

If you have an FHA loan, an FHA Streamline may reduce the rate and payment with fewer documentation requirements than a full refinance, depending on your specific file and the lender’s overlays.

Even when streamline options exist, it’s still smart to compare them against a conventional refinance, especially if your credit and equity improved and you’re trying to eliminate FHA mortgage insurance.

Cost, break-even, and the math that prevents refinance regret

Refinancing is rarely “free.” Common costs can include lender fees, title services, appraisal, recording charges, and prepaid items (like escrow setup).

A simple break-even approach:

- Estimate your monthly savings (new payment minus old payment).

- Estimate your total refinance costs (from the Loan Estimate).

- Break-even (months) = costs ÷ monthly savings.

Example:

If your refinance costs are $4,500 and you save $150 per month, break-even is 30 months. If you’ll likely sell in 18 months, the refinance may not pencil unless you use a lender-credit structure or there’s another strong reason (like removing PMI or stabilizing an ARM).

For rate context, many borrowers track baseline market movement using Freddie Mac’s Primary Mortgage Market Survey as a reference point, but your exact pricing still depends on credit, equity, occupancy, loan type, and other factors.

How to compare refinance offers without getting tricked by the headline rate

When you’re shopping a mortgage loan refinance, make sure you compare apples to apples:

- Same loan term and type (30-year fixed vs 30-year fixed, not 30-year vs 15-year)

- Same points and lender credits assumptions

- APR and total loan costs side by side

- Mortgage insurance changes (PMI removal, FHA MIP changes, VA funding fee considerations)

- Cash to close and whether you are rolling costs into the loan balance

If two offers show similar payments, the one with dramatically higher upfront costs might only “win” if you keep the loan long enough.

Documentation and qualification: how to prepare (especially if self-employed)

Most refinances still verify the fundamentals: equity, credit, income stability, and acceptable debt-to-income.

Before you apply, it helps to:

- Pull your credit and correct obvious errors.

- Avoid opening new debt right before or during the process.

- Gather recent pay stubs, W-2s, tax returns, and asset statements (requirements vary by program).

- Make sure homeowners insurance and property tax information is current.

If you’re self-employed, expect added focus on tax returns and business documentation. If your business has specialized tax filings, keeping them organized can prevent last-minute underwriting delays. For example, businesses that owe federal excise taxes may need to stay current with Form 720, and using an IRS-authorized Form 720 e-filing service can simplify that recordkeeping when you’re juggling a refinance timeline (see eFileExcise720).

Choosing the right refinance option for your goal

A good decision framework is to pick your primary objective first:

- If you need breathing room now: focus on payment reduction, then decide whether you’re comfortable extending term or prefer lowering rate without resetting the clock too much.

- If you want to be mortgage-free sooner: price out a 15-year or 20-year, and also ask what happens if you keep a 30-year and pay extra principal.

- If you’re paying mortgage insurance: prioritize scenarios that remove or reduce it, because it can outperform a small rate drop.

- If you’re in an ARM: weigh stability as a form of savings, especially before a reset.

How New Era Lending supports refinance decisions

Refinancing is full of tradeoffs, and the “best” offer is the one that matches your timeline, risk tolerance, and monthly budget.

New Era Lending’s approach combines smart tools and personalized human guidance to help you compare realistic scenarios, understand your Loan Estimate, and move through the process with clarity. If you’re looking to lower your payment, shorten your term, or both, you can explore refinance options with a team that emphasizes transparent terms, secure document uploads, and support across 39 states.

If you want to sanity-check the numbers first, their in-depth guide on timing and break-even math is also a helpful companion read: Refinance Rates for Mortgages: When to Refi in 2026.