.jpg)

.jpg)

.jpg)

How Your Home's Value Impacts Refinance Options

Most homeowners begin a refinance conversation by asking, “What rate can I get?” That matters, but it is only part of the picture. One of the first numbers a lender will look at is your home's value, because it helps determine how much equity you have, how much risk the new loan carries, and which refinance options are realistically available.

A higher value can improve your loan-to-value ratio, open the door to mortgage insurance removal, and increase how much cash you may be able to access. A lower value can limit cash-out proceeds, affect pricing, or make certain refinance paths harder to qualify for. Understanding this connection before you apply helps you compare offers with clearer expectations.

The refinance math starts with your home's value

When you refinance, the lender is not simply looking at what you paid for the property or what a real estate website estimates today. The value used for the refinance is typically based on an appraisal, an automated valuation, or another lender-approved valuation method. That value becomes the foundation for several important calculations.

The simplest way to think about it is this:

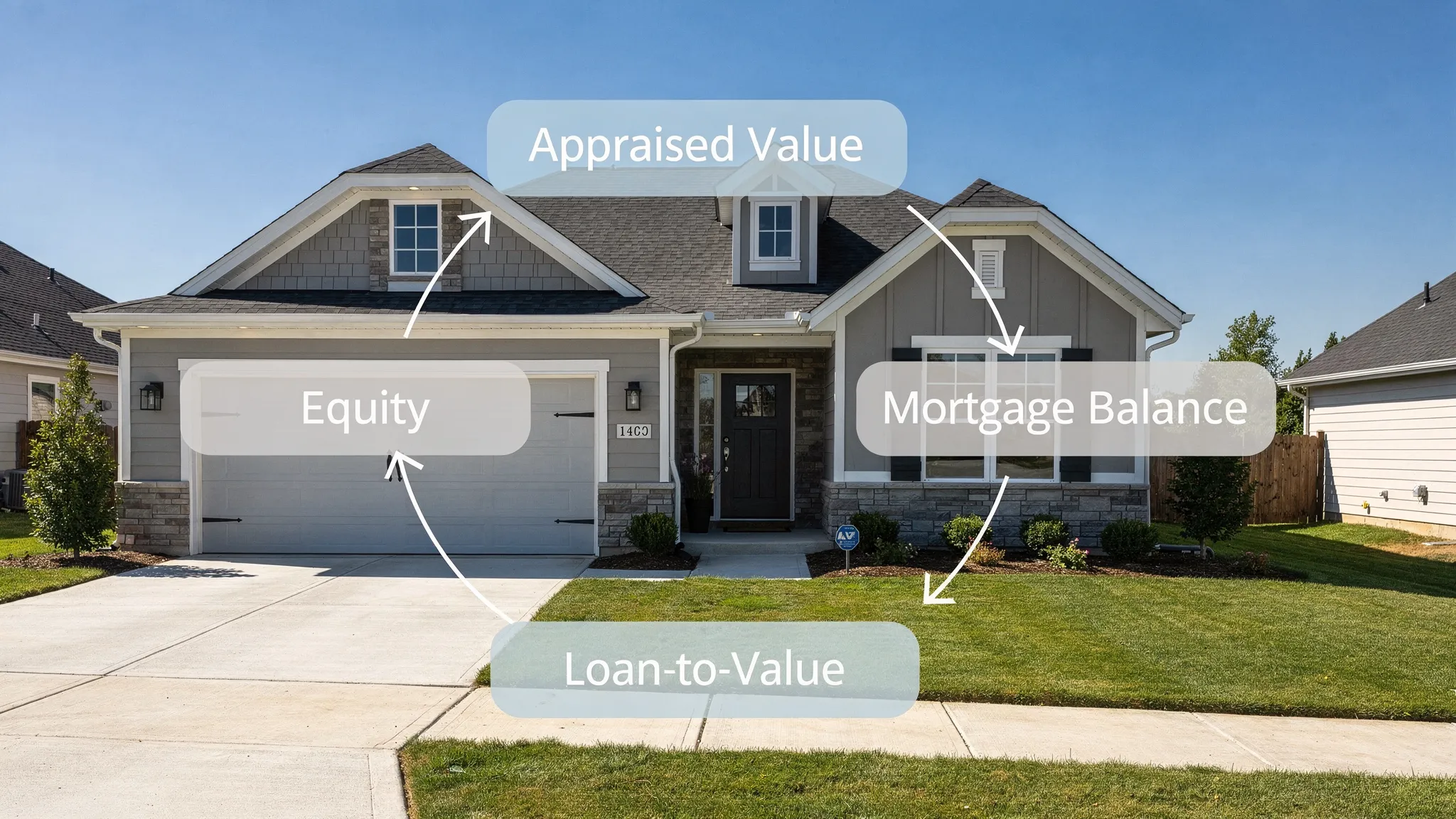

- Home equity is your home's current value minus the mortgage balances secured by the property.

- Loan-to-value ratio, or LTV, is the new loan amount divided by the home's value.

For example, if your home is valued at $400,000 and your current mortgage payoff is $300,000, you have about $100,000 in equity before closing costs and other adjustments. If you refinance into a new $300,000 loan, your LTV is 75 percent.

But if the same home appraises for $360,000 instead of $400,000, that same $300,000 loan would be about 83 percent LTV. Nothing changed about your income or credit, but your refinance profile looks different because the value changed.

Why loan-to-value matters so much

Lenders use LTV to measure how much of the property is financed compared with how much equity remains. Generally, a lower LTV means the borrower has more equity in the property, which can reduce the lender's risk. A higher LTV means less equity, which may affect eligibility, pricing, mortgage insurance, and approval conditions.

Your LTV can influence:

- Whether a refinance program is available to you

- Whether mortgage insurance is required

- How much cash you can take out

- The interest rate and cost structure you are offered

- Whether an appraisal waiver or alternative valuation might be possible

- How much flexibility you have if the appraisal comes in lower than expected

LTV is not the only factor. Your credit profile, debt-to-income ratio, income documentation, property type, occupancy, and loan program all matter too. Still, your home's value is one of the biggest pieces of the refinance puzzle.

How value affects a rate-and-term refinance

A rate-and-term refinance replaces your current mortgage with a new loan, usually to lower the interest rate, change the loan term, switch from an adjustable-rate mortgage to a fixed-rate mortgage, or adjust the payment structure. You are not primarily taking cash out, although closing costs may be included depending on the scenario and program rules.

Your home's value matters because it determines the LTV of the new loan. If the value has increased since you bought the home, your LTV may be lower than it was originally. That can help you qualify for more favorable terms, reduce risk-based pricing adjustments, or avoid mortgage insurance in certain conventional refinance scenarios.

If the value is lower than expected, a rate-and-term refinance may still be possible, but the benefits could shrink. For example, you might still qualify for a lower interest rate, but if the higher LTV requires mortgage insurance or changes pricing, the monthly savings may not be as strong as they looked in an early estimate.

If your main goal is to lower payment or adjust your loan term, it is worth comparing multiple scenarios. New Era Lending's guide to mortgage loan refinance options explains how different refinance structures can affect payment, term, and long-term cost.

How value affects a cash-out refinance

A cash-out refinance is more directly tied to your home's value because you are replacing your current mortgage with a larger loan and receiving part of your equity back as cash. The lender will set a maximum LTV based on the loan program, occupancy, property type, credit profile, and underwriting requirements.

Here is a simplified example:

- Appraised value: $500,000

- Example maximum LTV: 80 percent

- Maximum new loan amount: $400,000

- Current mortgage payoff: $310,000

- Estimated closing costs and prepaid items: $8,000

- Estimated cash available before final adjustments: $82,000

If the home appraises for $460,000 instead, the math changes. At the same example 80 percent LTV, the maximum new loan amount would be $368,000. After the same $310,000 payoff and $8,000 in estimated costs, the available cash could drop to about $50,000.

That is why cash-out refinance estimates should always be treated as value-sensitive until the property's valuation is complete. A small difference in appraised value can make a big difference in available proceeds.

Cash-out refinancing can be useful for home improvements, debt consolidation, education costs, emergency reserves, or other major financial goals, but it also increases the loan balance secured by your home. If you are comparing a cash-out refinance with a home equity line of credit, this guide on cash-out mortgage loans vs HELOCs can help you think through the tradeoffs.

How value can help you remove mortgage insurance

If you bought your home with a smaller down payment, your current loan may include mortgage insurance. A higher home value can sometimes help you remove or avoid mortgage insurance when refinancing, especially with a conventional loan.

For conventional loans, mortgage insurance is often connected to whether your LTV is above or below key thresholds. If your home's value has increased and your new loan amount would be at or below 80 percent LTV, you may be able to refinance into a loan without monthly private mortgage insurance, assuming you meet the other requirements.

If you currently have an FHA loan with mortgage insurance premiums, refinancing into a conventional loan may be one possible path to removing monthly mortgage insurance, but only if your credit, income, value, and equity position support it. This is not automatic, and closing costs matter, so the savings should be compared against the cost of the refinance.

Also, refinancing is not always the only way to address mortgage insurance. Some homeowners may be able to request PMI cancellation through their current loan servicer if they meet the requirements. For a deeper breakdown, read New Era Lending's guide to property mortgage insurance costs, rules, and ways to avoid it.

How value affects VA and FHA refinance options

Government-backed refinance programs can treat home value differently depending on the type of refinance.

For eligible veterans, service members, and qualifying surviving spouses, a VA Interest Rate Reduction Refinance Loan, often called an IRRRL, may have a more streamlined process when refinancing an existing VA loan. In some cases, the valuation requirements may be different from a full cash-out refinance. However, lender requirements and individual circumstances still matter, so it is important to confirm details before making assumptions.

A VA cash-out refinance is different. Because you are accessing equity or refinancing a non-VA loan into a VA-backed loan, the home's value plays a major role in determining the maximum loan amount and whether the transaction meets program guidelines.

FHA refinance options can also vary. An FHA streamline refinance may have reduced documentation or valuation requirements in some cases, while an FHA cash-out refinance depends more heavily on the appraised value, LTV, credit, and income profile.

The key point is simple: streamline refinances may focus less on current value than cash-out refinances, but your home's value still matters for many refinance paths.

What if your home's value has increased?

If your property has appreciated, you may have more refinance flexibility than you had when you first bought the home. That can be especially helpful if you purchased with a low down payment, made significant improvements, or live in a market where values have grown.

A higher value may help you:

- Lower your LTV and potentially improve pricing

- Remove or reduce mortgage insurance

- Access more equity through a cash-out refinance

- Refinance from FHA to conventional if you qualify

- Combine a first mortgage and certain secondary financing into one new loan

- Improve your approval profile if LTV was previously a limiting factor

That said, higher value does not automatically mean refinancing is the right move. If your current mortgage rate is much lower than today's available rates, replacing the entire loan could increase your payment even if you have more equity. In that case, a HELOC or home equity loan might be worth comparing, depending on your goals.

In 2026, many homeowners are balancing strong equity positions with rate environments that vary week to week. The right decision depends on your current loan, the new offer, your timeline, and what you want the refinance to accomplish.

What if the appraisal comes in lower than expected?

A low appraisal does not always end the refinance, but it can change the numbers. If the appraised value is lower than the estimate used in your initial quote, your LTV rises. That may reduce cash-out proceeds, add mortgage insurance, change pricing, or require a different loan structure.

Common options after a lower-than-expected valuation include:

- Reducing the new loan amount

- Taking less cash out

- Bringing cash to closing to keep the desired LTV

- Switching loan programs if another option fits better

- Requesting a reconsideration of value if there are factual errors or stronger comparable sales

- Waiting to refinance until market conditions or your equity position improve

A reconsideration of value is not a guaranteed fix. You typically need specific evidence, such as incorrect property details, overlooked comparable sales, or documented improvements that were not considered. A lender or loan officer can explain whether a reconsideration is appropriate for your situation.

What appraisers look at when valuing your home

An appraisal is not the same as a home inspection. The appraiser's job is to provide an opinion of market value based on the property and comparable sales. They may consider the home's size, condition, location, lot, age, layout, updates, and recent sales of similar homes nearby.

Some improvements may support a higher value, but not every dollar spent on a project translates into a dollar of appraised value. A kitchen renovation, finished basement, new roof, or energy-efficient upgrade may help, but the impact depends on your market and how similar homes are selling.

Condition also matters. Safety issues, deferred maintenance, damaged flooring, peeling paint in certain loan programs, or incomplete repairs can create appraisal conditions or underwriting questions. Before refinancing, it is smart to fix obvious issues and gather records for major improvements.

How to estimate your value before applying

You do not need to know your exact appraised value before starting a refinance conversation, but having a realistic estimate helps. Online home value tools can be a starting point, but they can miss recent renovations, unusual property features, local market shifts, or differences between nearby neighborhoods.

A better pre-application estimate may come from reviewing recent comparable sales, speaking with a local real estate professional, checking your current mortgage payoff, and asking a lender to model a few value scenarios. For example, you might compare what happens if the home is valued at $425,000, $400,000, or $375,000. That way, you know where the refinance still works and where it becomes less attractive.

Try not to make the decision under pressure. Refinancing involves numbers, deadlines, and personal goals, so it helps to step away and review the offer with a clear head. Take a walk, sleep on the decision, or if you happen to be traveling in Spain, reset with something restorative like a relaxing massage in Valencia before you commit to a major financial move.

How to prepare your home and finances for a refinance

You cannot control every part of the valuation process, but you can make sure the property and your loan file are presented clearly.

Before applying, consider these steps:

- Gather records for major improvements, including dates, costs, permits, and contractor invoices when available.

- Complete small repairs that could raise condition concerns, such as damaged trim, leaks, broken fixtures, or missing safety items.

- Make sure the appraiser can access key areas, including the attic, basement, garage, mechanical systems, and exterior.

- Review your mortgage payoff and any second liens, HELOCs, or other loans secured by the property.

- Avoid taking on new debts before or during the refinance process.

- Decide your main goal before comparing offers, such as lower payment, shorter term, cash out, or mortgage insurance removal.

The clearer your goal, the easier it is to know whether the valuation supports the refinance. A loan that looks good for cash-out purposes may not be the best option for lowering payment. A loan that removes mortgage insurance may still need a break-even review to make sure the closing costs are worth it.

Questions to ask your lender about home value

A good refinance conversation should include more than a rate quote. Ask how your value affects the full loan structure.

Helpful questions include:

- What estimated property value are you using for this quote?

- What LTV thresholds affect my pricing or eligibility?

- Is an appraisal required, or could an appraisal waiver be possible?

- How would my payment change if the appraisal is 5 percent lower?

- Would this refinance remove, reduce, or add mortgage insurance?

- For a cash-out refinance, how much cash would I receive after payoff and estimated costs?

- Are there other refinance or equity options that fit my goal better?

These questions help you avoid surprises and compare offers more accurately. They also make it easier to see whether the refinance still makes sense if the value changes.

Your home's value is important, but it is not the whole decision

A strong home value can open refinance options, but it does not replace the rest of the underwriting picture. Lenders still review credit, income, employment, assets, debts, property type, occupancy, and the details of the loan program.

You also need to compare the refinance cost against the benefit. A lower payment may be helpful, but how long will it take to recover closing costs? A cash-out refinance may provide funds now, but how much interest will you pay over time? Removing mortgage insurance may be valuable, but would your current servicer allow cancellation without a full refinance?

The best refinance decision is not based on value alone. It is based on value, loan structure, costs, payment, timeline, and your reason for refinancing.

Frequently Asked Questions

Does my home need to appraise for the amount I think it is worth? Not necessarily, but the lender will use the approved valuation for refinance calculations. If the appraised value is lower than expected, your LTV may increase, which can affect pricing, mortgage insurance, cash-out proceeds, or eligibility.

Can I refinance if my home value dropped? Yes, it may still be possible, depending on your loan type, LTV, credit, income, and refinance goal. Some streamline refinance programs may be less value-sensitive, while cash-out refinances usually depend heavily on current value.

How much equity do I need for a cash-out refinance? It depends on the loan program, occupancy, property type, credit profile, and lender guidelines. You generally need enough equity to pay off the current mortgage, cover costs if financed, and stay within the program's maximum LTV.

Can a higher home value help remove PMI? It can. If your value has increased enough that your conventional loan balance is at or below key LTV thresholds, you may be able to remove PMI through refinancing or, in some cases, by requesting cancellation from your current servicer.

Should I order my own appraisal before refinancing? Usually, the lender must order the appraisal or valuation through approved channels. A private appraisal may help you understand value, but it may not be usable for the refinance itself.

Refinance with clearer numbers and guidance

Your home's value can change your refinance options in a big way, but you do not have to figure out the math alone. New Era Lending helps homeowners compare refinance scenarios with smart technology, secure document uploads, transparent rates and terms, and personalized human guidance.

Whether your goal is to lower your payment, adjust your term, remove mortgage insurance, or access equity, a personalized review can show how your home's value affects the options available to you. If you are ready to explore your next move, connect with New Era Lending and get a refinance comparison built around your goals.