.jpg)

.jpg)

.jpg)

Is a New Mortgage Rate Good Enough to Refinance?

A new mortgage rate can feel like a green light to refinance, especially if it is lower than the rate you have today. But the rate itself is only one part of the decision. A refinance is worth considering when the new loan improves your financial position after closing costs, fits your timeline, and supports a clear goal such as lowering your payment, shortening your term, removing mortgage insurance, or accessing equity responsibly.

The short answer: a lower rate is not automatically good enough to refinance. It becomes good enough when the savings, cost, and loan structure work together in your favor.

Start with what refinancing actually changes

When you refinance, you are replacing your current mortgage with a new one. That new mortgage may come with a different interest rate, loan term, payment, loan balance, program type, or mortgage insurance structure.

That means the question is not simply, “Is the new mortgage rate lower?” The better question is, “What does this refinance change, and is that change worth the cost?”

A refinance may affect:

- Your monthly principal and interest payment

- Your total interest cost over time

- Your remaining loan term

- Your mortgage insurance requirement

- Your cash reserves after closing

- Your access to home equity

- Your payment stability if you have an adjustable-rate mortgage

A lower rate can help, but it should be evaluated alongside the full picture. If the new loan saves $150 per month but costs $6,000 to complete, you need to know how long it will take to recover that cost. If the new loan lowers your payment only because it stretches your mortgage back to 30 years, you need to understand the long-term tradeoff.

Why a lower new mortgage rate can be misleading

Mortgage rates are often discussed as if every borrower receives the same number. In reality, your refinance rate depends on your credit profile, loan-to-value ratio, property type, occupancy, loan amount, loan program, term length, lock period, and whether the quote includes points or lender credits.

This is why a rate you see online may not match the rate you are actually offered. An advertised rate may assume excellent credit, a specific loan amount, a certain amount of equity, and upfront discount points. If your situation is different, your personalized quote may be different too.

It is also important to separate the interest rate from the APR. The interest rate helps determine the monthly principal and interest payment. The APR reflects certain loan costs and can help you compare offers more accurately. A refinance with a slightly lower interest rate but high points and fees may not be better than a refinance with a slightly higher rate and lower upfront cost.

Finally, be careful with term resets. If you have 22 years left on your current mortgage and refinance into a new 30-year loan, the monthly payment may fall partly because you are extending the repayment schedule. That can be useful if monthly cash flow is the goal, but it may increase total interest paid over the life of the loan if you do not make extra principal payments.

For a deeper look at comparing quotes, see New Era Lending’s guide on how to compare home refinance rates the right way.

The refinance test: payment, break-even, and timeline

A new mortgage rate is good enough to refinance when it passes three practical tests: the payment test, the break-even test, and the timeline test.

The payment test

Start with the full monthly payment, not just the interest rate. Your mortgage payment may include principal, interest, property taxes, homeowners insurance, mortgage insurance, HOA dues, or escrow adjustments. A rate reduction does not always mean every part of your housing payment will go down.

For example, your principal and interest payment might decrease, but your escrow payment could rise because property taxes or insurance premiums have increased. If your goal is monthly relief, compare the full projected payment to your current full payment.

Also ask where the savings are coming from. If the lower payment comes from a lower rate, that is different from a lower payment created mostly by restarting the loan term. Both may be valid, but they are not the same financial outcome.

The break-even test

The break-even point tells you how long it takes for monthly savings to recover the cost of refinancing.

Use this simple formula:

Total refinance costs divided by monthly savings equals break-even months.

If your refinance costs $5,000 and saves $250 per month, the break-even point is 20 months. If you expect to keep the home and loan for much longer than 20 months, the refinance may be worth exploring. If you may sell the home in a year, the math may not work.

Be sure to identify which costs are true costs and which are prepaids or escrow items. Lender fees, title fees, appraisal fees, recording charges, and discount points are typical refinance costs. Prepaid interest, property tax deposits, and insurance escrow funding may affect cash to close, but they are not always the same as permanent costs.

The timeline test

Even if the break-even math looks good, your personal timeline matters. If you plan to move, sell, refinance again, or pay off the loan soon, you may not benefit long enough to justify the refinance.

This is where “good enough” becomes personal. A homeowner planning to stay for 10 years may accept a longer break-even period than someone who expects to relocate within 18 months. A homeowner who needs immediate payment relief may prioritize monthly cash flow more than long-term interest savings. A homeowner nearing retirement may prefer payment stability or a shorter term.

How much lower does the rate need to be?

You may have heard that refinancing only makes sense if the new rate is at least 1 percentage point lower than your current rate. That rule of thumb is too simple.

A smaller rate drop can be worthwhile if your loan balance is high, your closing costs are low, or you plan to keep the home for a long time. A larger rate drop may still fail the test if your loan balance is small, your costs are high, or you expect to sell soon.

Instead of looking for a universal rate drop, evaluate the actual dollars. Ask how much the refinance saves each month, how much it costs, how long it takes to break even, and how it changes your total interest over the period you expect to keep the loan.

A rate that is “good enough” for one homeowner may not be good enough for another. The right answer depends on the loan size, current rate, available equity, credit profile, closing costs, and goals.

When a small rate improvement can be good enough

A modest rate reduction may still be worth considering in certain situations. For example, if you have a large loan balance, even a small change in rate can create meaningful monthly savings. If the refinance has low closing costs, the break-even period may be short. If you are staying in the home long term, you may have enough time to benefit from the savings.

A small rate improvement can also be valuable if it helps you remove mortgage insurance. For a conventional loan, reaching the right equity position may allow you to refinance into a loan without PMI. In that case, your savings may come from both the lower rate and the elimination of mortgage insurance.

A lower rate may also be helpful if you currently have an adjustable-rate mortgage and want a fixed payment. Even if the payment savings are not dramatic, the value may come from reducing future payment uncertainty.

When even a lower rate may not be enough

A refinance can look attractive at first and still be the wrong move. This often happens when homeowners focus on the interest rate while overlooking costs, timing, or the long-term loan structure.

A lower rate may not be enough if you are likely to sell soon. In that situation, it may be smarter to compare the cost of refinancing with the cost and potential savings of selling. If you are already leaning toward a move, reviewing listing options, including flat-fee MLS options such as NetRealtyNow, can help you think through the sell-versus-refinance decision more clearly.

A refinance may also be less attractive if the closing costs are high, the break-even period is too long, or the new loan restarts your mortgage in a way that increases lifetime interest. It may not make sense if you are using a cash-out refinance without a disciplined plan for the funds, or if the new loan would leave you with too little emergency savings.

There are also cases where the existing loan has benefits worth preserving. For example, some homeowners have unusually favorable older rates, unique loan terms, or assumptions tied to their current financing. Before replacing your loan, make sure you understand what you are giving up.

Do not ignore the loan term

The loan term can change the answer completely. A lower rate on a new 30-year loan may reduce the payment, but it can extend the amount of time you are in debt. A 15-year or 20-year refinance may increase the monthly payment compared with a 30-year option, but it can reduce total interest and help you build equity faster.

If your goal is monthly breathing room, a new 30-year term may be reasonable. If your goal is to pay off the home faster, a shorter term may be better. If your goal is both lower payment and faster payoff, you may compare a lower-rate refinance while continuing to make your old payment amount as an extra principal strategy.

The key is to compare options over the same time horizon. Do not only compare the old payment to the new payment. Compare the interest cost, remaining balance, and flexibility after five, seven, or 10 years, depending on your expected ownership timeline.

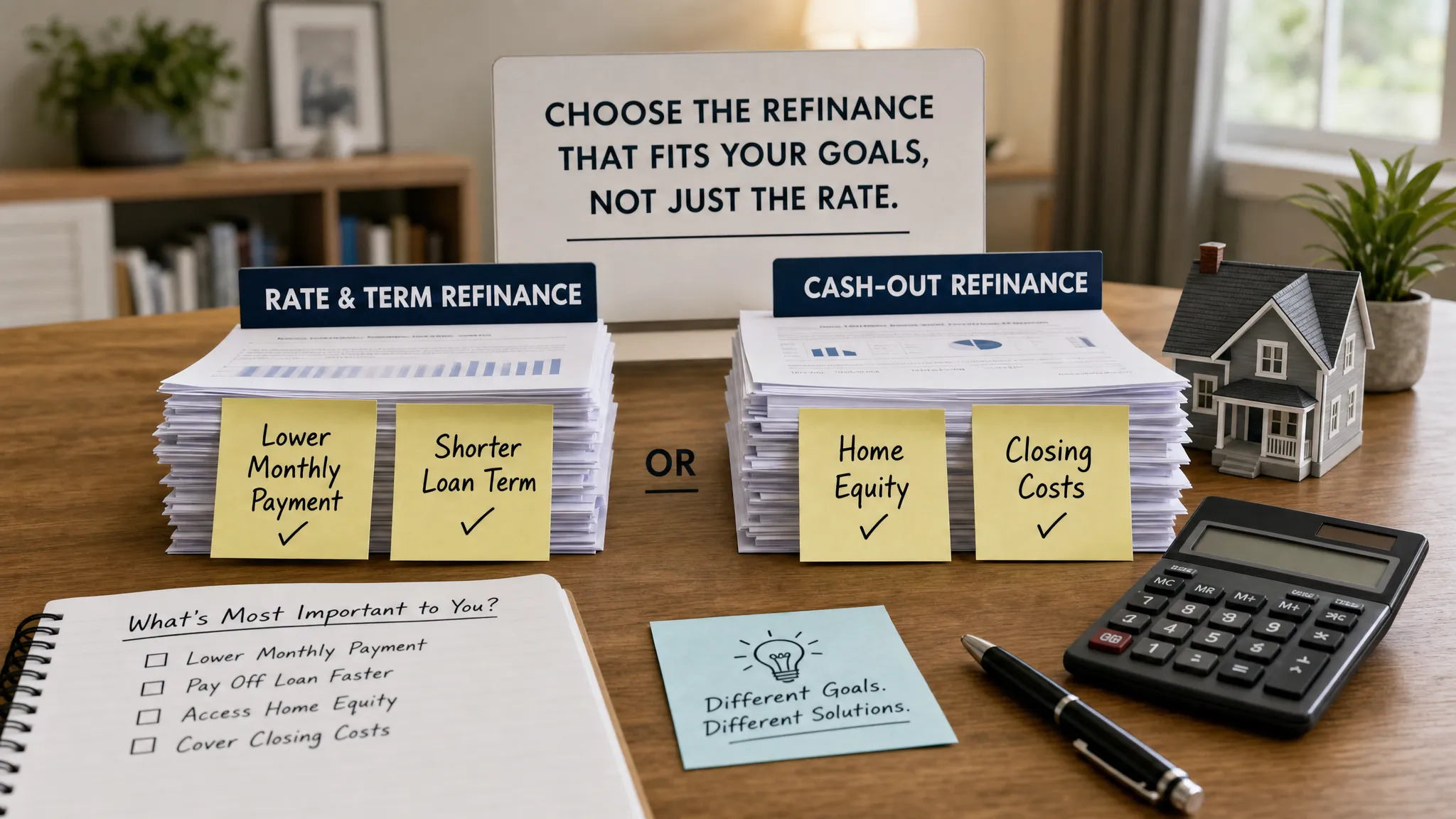

Consider the type of refinance you are choosing

Not all refinances are designed to accomplish the same thing. A rate-and-term refinance focuses on changing the rate, term, or loan structure without taking significant cash out. This is the most common path when the main goal is lowering the payment, shortening the loan, or moving from an ARM to a fixed-rate loan.

A cash-out refinance is different. It allows you to convert home equity into funds, but it also increases the loan balance. In this case, a new mortgage rate is not the only decision point. You should also evaluate how the money will be used, how much equity remains, and whether a HELOC or home equity loan would be a better fit.

A streamline refinance, such as certain VA or FHA refinance options, may involve less documentation or a simplified process for eligible borrowers. These programs often focus on a clear borrower benefit, but costs still matter. Veterans and FHA borrowers should look carefully at funding fees, mortgage insurance, payment changes, and the break-even period.

If you are comparing multiple refinance goals, New Era Lending’s guide to mortgage loan refinance options to lower payment or term can help you frame the decision.

What to compare before you say yes

Before deciding that the new rate is good enough, gather your current loan details and compare them with the proposed refinance. Your loan officer can help you run these numbers, but it helps to know what to look for.

Review these items side by side:

- Current unpaid principal balance, interest rate, payment, and remaining term

- New interest rate, APR, loan amount, payment, and term

- Closing costs, points, lender credits, and cash to close

- Break-even period based on realistic monthly savings

- Total interest over the period you expect to keep the loan

- Mortgage insurance changes, if any

- Whether costs are paid upfront, rolled into the loan, or offset with a lender credit

- How much emergency savings you will keep after closing

This comparison is especially important with “no-closing-cost” refinance offers. These can be useful, but the costs do not disappear. They are usually covered through a higher rate, lender credit, or a higher loan balance. Sometimes that tradeoff makes sense, especially if you want a short break-even period. Sometimes paying some costs upfront creates a better long-term result.

Timing matters, but do not chase rates blindly

Mortgage rates can move quickly, and 2026 has continued to remind borrowers that the market can change based on inflation data, bond yields, economic news, and lender pricing adjustments. Waiting for the perfect rate can backfire if rates rise, but rushing into a refinance without checking the math can be just as costly.

A practical approach is to get prepared before the rate you want appears. Know your current loan balance, credit profile, home value estimate, income documentation, and refinance goal. That way, when pricing becomes favorable, you can move quickly and compare real options rather than guessing from headlines.

Also ask about the rate lock. A quote is not the same as a locked rate. Confirm the lock period, whether there are lock fees, what happens if closing is delayed, and whether a float-down option is available.

A simple decision framework

If you are unsure whether to refinance, use this plain-English framework.

Refinancing may make sense if the new loan gives you a meaningful monthly benefit, the break-even period fits your expected timeline, and the refinance supports a clear financial goal. It is stronger when you can preserve cash reserves, avoid unnecessary debt extension, and understand all costs before closing.

Refinancing may not make sense if the savings are too small, the costs are too high, you plan to sell soon, or the new loan only looks better because it hides costs in the balance or stretches the term. It may also be worth waiting if improving your credit, paying down debt, or building more equity could unlock better pricing soon.

The best refinance decisions are not based on one number. They are based on a full comparison that shows what changes now, what changes over time, and what tradeoffs you are accepting.

Frequently Asked Questions

Is a 1% lower mortgage rate always enough to refinance? No. A 1% rate drop can be helpful, but it is not automatically enough. Closing costs, loan balance, remaining term, break-even period, and how long you plan to keep the home all matter.

Can a smaller rate drop still make refinancing worthwhile? Yes. A smaller rate drop can make sense if your loan balance is large, your refinance costs are low, you plan to stay in the home long term, or the refinance also removes mortgage insurance.

What is a good break-even period for refinancing? A good break-even period is one that is comfortably shorter than the time you expect to keep the loan. If your break-even point is 24 months and you expect to stay for five years, the math may work. If you expect to sell in a year, it probably does not.

Should I refinance if the payment is lower but the loan restarts at 30 years? Maybe. Restarting at 30 years can improve monthly cash flow, but it may increase long-term interest if you make only the minimum payment. Ask for a comparison that shows total cost and remaining balance over your expected timeline.

Are no-closing-cost refinances really free? Usually, no. The costs are often covered through a higher rate, lender credit, or by rolling costs into the loan. That can still be a smart option in some cases, but you should compare it with paying costs upfront.

Should I wait for rates to drop more before refinancing? It depends on your current numbers and risk tolerance. If today’s refinance meets your goals and has a strong break-even period, waiting may not be necessary. If the savings are marginal, improving your credit or watching the market may be reasonable.

Make the new rate work for your real goals

A new mortgage rate is only good enough if the full refinance makes sense. Before you commit, compare the monthly savings, closing costs, break-even point, loan term, and long-term impact.

New Era Lending helps homeowners evaluate refinance options with smart technology, transparent loan comparisons, secure document uploads, e-signature support, and personalized guidance from experienced mortgage professionals. If you are considering a refinance, request a personalized scenario review so you can decide with confidence, not guesswork.