.jpg)

.jpg)

.jpg)

Loan Payment Terms That Can Raise or Lower Costs

A lower interest rate is helpful, but it is not the only thing that decides what a loan really costs. The payment terms written into your mortgage can change your monthly obligation, your cash needed at closing, how quickly you build equity, and the total interest you pay over time.

That is why two loans with the same loan amount can feel very different. One may offer a lower monthly payment but cost more over the life of the loan. Another may require a higher payment now but help you pay off the balance much faster.

If you are buying a home, refinancing, or accessing equity, understanding loan payment terms can help you compare offers with more confidence and avoid expensive surprises later.

What Are Loan Payment Terms?

Loan payment terms are the rules that determine how and when you repay borrowed money. For a mortgage, they usually include your repayment length, interest rate structure, amortization schedule, payment due date, escrow requirements, fees, and whether you can make extra principal payments without penalty.

In plain English, payment terms answer questions like:

- How many years will I be paying this loan?

- Is my interest rate fixed or adjustable?

- How much of my payment goes toward principal versus interest?

- Are taxes, insurance, or mortgage insurance included in the payment?

- What happens if I pay late or pay extra?

- Are there upfront costs that change my rate or monthly payment?

The payment of loans is not just about making one monthly transfer. It is about how every dollar is applied and how the structure of the loan affects your total cost.

The Consumer Financial Protection Bureau recommends using the Loan Estimate to compare mortgage offers because it shows key terms, projected payments, closing costs, and whether the loan has features such as a prepayment penalty or balloon payment.

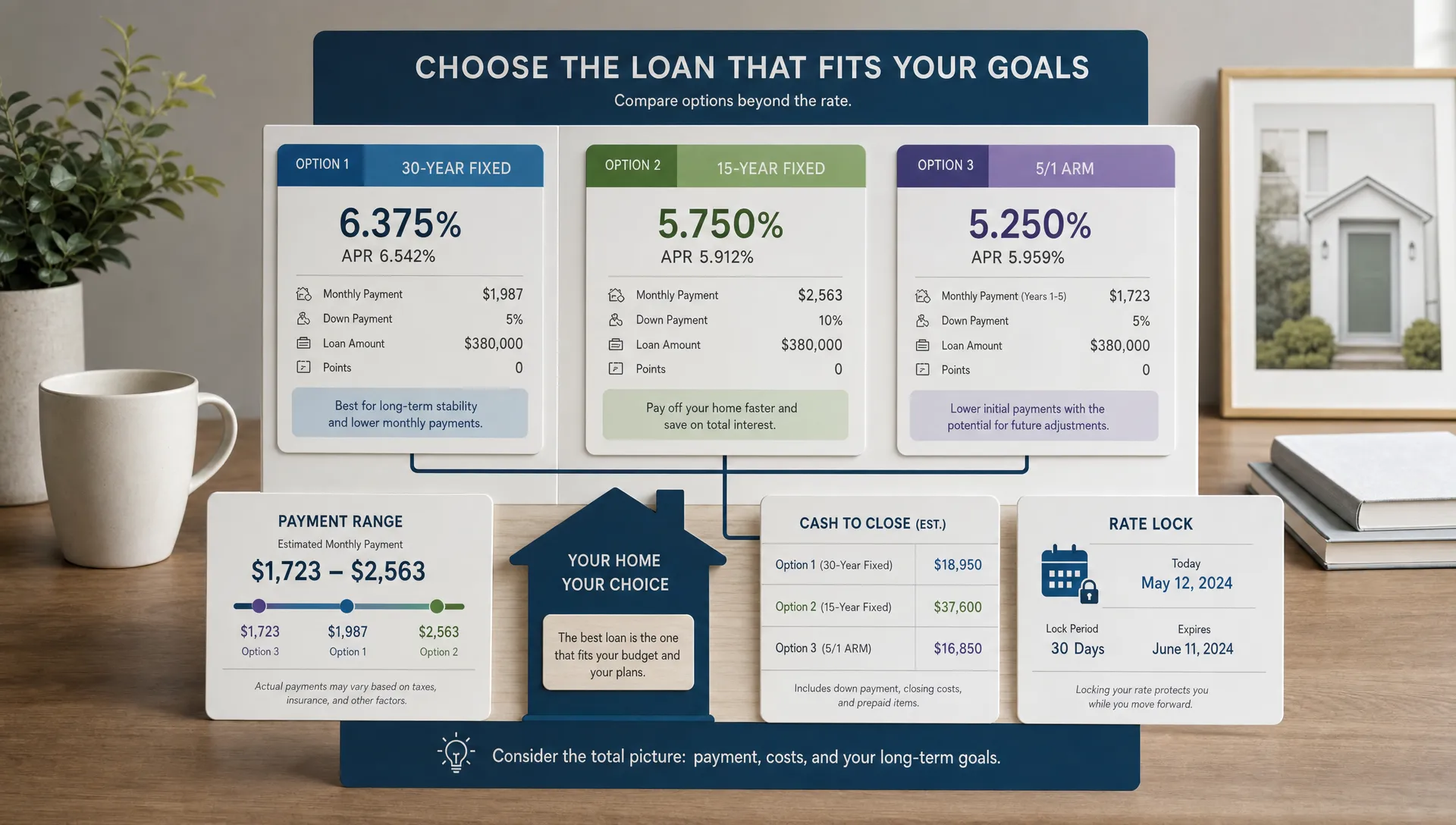

Loan Term Length: Lower Payment or Lower Total Interest

The loan term is one of the biggest cost drivers. Most homebuyers compare 30-year and 15-year mortgages, but other terms may be available depending on the loan program and lender.

A longer term usually lowers the monthly principal and interest payment because the balance is spread across more months. The tradeoff is that you typically pay interest for a longer period.

A shorter term usually increases the monthly payment but can reduce total interest dramatically because the loan is paid down faster.

For example, using a hypothetical $350,000 mortgage at a fixed 6.75% interest rate:

- A 30-year term would have a principal and interest payment of about $2,270 per month and roughly $467,000 in total interest over the full term.

- A 15-year term would have a principal and interest payment of about $3,098 per month and roughly $208,000 in total interest over the full term.

The shorter term costs more each month, but the long-term interest savings can be significant. The right choice depends on your income stability, savings, emergency fund, other debts, and how long you expect to keep the home.

If a 15-year payment feels too tight, a 30-year loan with optional extra principal payments may provide flexibility while still helping you reduce interest over time.

Fixed vs Adjustable Payment Terms

Your rate structure also changes your payment risk. With a fixed-rate mortgage, the principal and interest portion of your payment stays the same for the life of the loan. Taxes, insurance, HOA dues, or mortgage insurance can still change, but the core loan payment is predictable.

With an adjustable-rate mortgage, often called an ARM, the initial rate is fixed for a set period. After that, the rate can adjust based on the loan’s index, margin, and adjustment caps. ARMs can sometimes offer a lower starting payment than a comparable fixed-rate loan, but the payment may rise later.

An ARM may make sense if you have a shorter ownership timeline, expect to refinance, or have enough budget flexibility to handle future adjustments. It may be risky if you are stretching to qualify or need long-term payment certainty.

Before choosing an ARM, ask about:

- The initial fixed period

- The first adjustment date

- The index and margin

- The maximum increase at the first adjustment

- The lifetime rate cap

- The highest possible payment

Do not compare only the starting payment. Compare the payment you can afford if the loan adjusts upward.

Amortization: How Your Payment Is Applied

Amortization is the schedule that determines how each payment is divided between interest and principal. In the early years of a standard mortgage, more of your payment goes toward interest. Over time, more goes toward principal.

This matters because two loans can have the same monthly payment but build equity at different speeds depending on the term, rate, and amortization structure.

Most traditional mortgages are fully amortizing, meaning that if you make every required payment, the loan is paid off by the end of the term. Some loans may have nontraditional features, such as interest-only periods or balloon payments. These can reduce the payment at first, but they may increase risk later.

An interest-only payment may look attractive because it does not require principal reduction during the interest-only period. However, once principal repayment begins, the payment may rise significantly. A balloon payment can create an even larger challenge because a remaining balance may come due all at once.

For most borrowers, a fully amortizing loan is easier to plan around because the payoff path is built into the monthly payment.

Points and Lender Credits: Upfront Cost vs Monthly Savings

Discount points and lender credits are payment terms that shift cost between closing and the monthly payment.

A discount point is an upfront fee paid to reduce the interest rate. One point equals 1% of the loan amount. Paying points may lower your monthly payment and total interest if you keep the loan long enough to reach the break-even point.

A lender credit works in the opposite direction. You may accept a higher interest rate in exchange for reduced closing costs. This can help preserve cash at closing, but it may increase your monthly payment and long-term cost.

Neither option is automatically good or bad. It depends on your cash position and timeline.

If paying points saves $120 per month but costs $5,000 upfront, the simple break-even point is about 42 months. If you plan to sell or refinance before then, paying points may not make sense. If you expect to keep the loan much longer, it may be worth considering.

This is where APR can help, but APR is not perfect. APR blends the interest rate with certain loan costs, making it useful for comparing similar loans. However, it assumes you keep the loan for the full term, which may not match your actual plans.

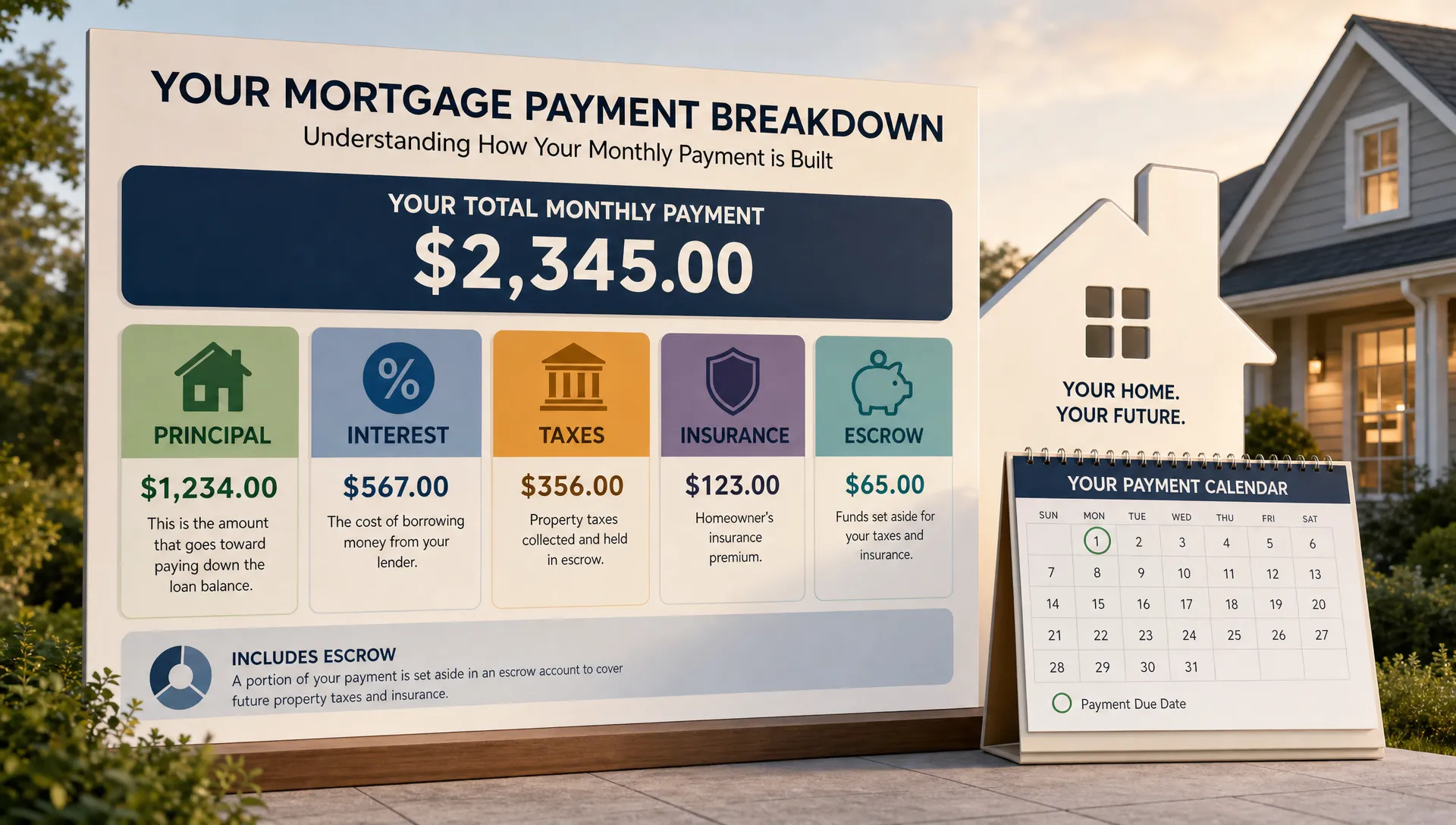

Escrow Terms: Convenient, but Not Fixed Forever

Many mortgage payments include escrow for property taxes and homeowners insurance. Instead of paying those bills separately, you pay a monthly amount into an escrow account, and the servicer pays the bills when due.

Escrow can make budgeting easier, but it can also cause your total monthly payment to change. If property taxes rise or insurance premiums increase, your escrow payment may increase after the annual escrow analysis.

This often surprises borrowers who thought their payment was completely fixed. The principal and interest portion may be fixed, but escrowed items can change.

When comparing loan payments, make sure you know whether the quote includes:

- Principal and interest

- Property taxes

- Homeowners insurance

- Mortgage insurance

- HOA dues, if applicable

A quote that shows principal and interest only may look much lower than your real housing payment.

Mortgage Insurance and Funding Fees

Mortgage insurance terms can raise or lower costs depending on your loan type, down payment, and equity.

Conventional loans may require private mortgage insurance, commonly called PMI, when the down payment is less than 20%. PMI is often paid monthly, though other structures may be available. FHA loans typically include mortgage insurance premiums, which have different rules. VA loans do not require monthly mortgage insurance, but they may include a VA funding fee unless the borrower is exempt.

These costs can affect both monthly payment and total loan cost. The important question is not just “What is my rate?” but “What is my total monthly payment including insurance and loan-specific fees?”

Also ask whether mortgage insurance can be removed later. Conventional PMI may be cancellable once certain equity requirements are met, while FHA mortgage insurance rules can vary depending on down payment, loan term, and when the loan was originated.

Extra Principal Payments: A Flexible Way to Reduce Interest

Some borrowers want to lower total cost without committing to a shorter loan term. Extra principal payments can help.

When you pay extra toward principal, you reduce the balance that interest is calculated on. Over time, this can shorten the payoff schedule and lower total interest.

The key is to make sure extra payments are applied correctly. Your payment instructions should clearly state that the extra amount is for principal reduction, not a future payment.

Common strategies include paying a little extra each month, making one additional principal payment per year, or applying bonuses and tax refunds toward the balance.

Before doing this, confirm that your loan has no prepayment penalty. Many standard residential mortgages do not have prepayment penalties, but you should still verify the terms on your Loan Estimate and closing documents.

Biweekly Payments: Helpful Only If Structured Correctly

Biweekly payment plans are often marketed as a way to pay off a mortgage faster. The idea is simple: instead of making 12 monthly payments per year, you make half a payment every two weeks. Since there are 52 weeks in a year, this creates 26 half-payments, equal to 13 full monthly payments.

That extra annual payment can reduce total interest and shorten the loan term. However, not all biweekly plans are equal.

Some third-party services charge fees for something you may be able to do yourself. Others may hold payments before sending them to the servicer, which can create timing issues.

A simpler approach may be to divide one monthly payment by 12 and add that amount as extra principal each month. You get a similar effect while keeping direct control over the payment.

Late Fees, Grace Periods, and Payment Timing

Payment timing terms may not seem important when everything goes smoothly, but they matter if your income timing changes or an unexpected expense hits.

Most mortgages have a due date and a grace period. For example, a payment may be due on the first of the month, with a late fee after a certain date. The exact timing and fee should be listed in your loan documents.

A late fee increases cost directly. More importantly, payments that become seriously late can affect credit and create servicing issues. Since credit history can influence future refinance options, a late payment can have costs beyond the fee itself.

If your pay schedule makes the due date difficult, ask your servicer what options are available after closing. Some servicers may allow changes to draft dates, but do not assume that is guaranteed before you sign.

Recast Terms: Lowering the Payment Without Refinancing

A mortgage recast allows you to make a large principal payment and have the lender recalculate the monthly payment based on the lower balance and remaining term. Unlike refinancing, a recast typically keeps the same interest rate and loan maturity date.

This can be useful if you buy before selling another home, receive a large bonus, or want to lower your required monthly payment after paying down principal.

Not all loans are eligible for recasting, and lenders may charge a fee. Government-backed loans may have different restrictions. If recasting is part of your strategy, ask about it before choosing the loan.

Recasting is different from making extra principal payments. Extra payments can reduce interest and shorten the payoff period, but they usually do not lower the required monthly payment unless the loan is recast.

HELOC and Home Equity Payment Terms

If you are accessing home equity, payment terms deserve special attention. A home equity loan, HELOC, and cash-out refinance can each create different payment patterns.

A home equity loan usually provides a lump sum with a fixed repayment schedule. A HELOC usually works like a revolving line of credit with a draw period and a repayment period. During the draw period, payments may be interest-only or based on the amount borrowed. During repayment, the payment can rise because principal repayment begins.

Many HELOCs also have variable rates, which means payment can change as market rates change. That flexibility can be useful, but it requires careful budgeting.

A cash-out refinance replaces your existing mortgage with a new one, often changing the rate, term, and payment. It can simplify debt into one mortgage payment, but it may also restart the repayment clock or increase total interest if the new term is much longer.

Before using home equity, compare not only the starting payment but also the highest realistic payment, total fees, and how long you will be paying.

How to Compare Loan Payment Terms Before You Commit

The best way to compare loan terms is to use the same loan scenario across each quote. That means the same purchase price or home value, down payment or equity amount, credit assumptions, loan type, term, lock period, and occupancy.

Then review the Loan Estimate carefully. Pay special attention to projected payments, estimated taxes and insurance, closing costs, cash to close, APR, points, lender credits, prepayment penalties, balloon payments, and whether the payment can increase.

Ask your lender questions that connect the payment to your real life:

- What is my full estimated monthly payment, including escrow and mortgage insurance?

- Which parts of the payment can change over time?

- How much total interest would I pay if I keep the loan for the full term?

- What happens if I pay extra principal?

- Is there any prepayment penalty, balloon payment, or interest-only period?

- What is the break-even point if I pay points?

- How would the payment change if I choose a shorter or longer term?

A trustworthy comparison should make tradeoffs clear. The goal is not always the lowest monthly payment or the lowest upfront cost. The goal is the payment structure that fits your budget, risk tolerance, and long-term plans.

Frequently Asked Questions

Which loan payment term has the biggest impact on cost? The repayment length and interest rate structure usually have the biggest impact. A longer term can lower the monthly payment but increase total interest, while a shorter term usually costs more each month but reduces long-term interest.

Can I lower my mortgage cost without refinancing? Sometimes, yes. Extra principal payments, removing eligible mortgage insurance, shopping homeowners insurance, or requesting a recast after a large principal payment may help lower costs. The right option depends on your loan type and servicer rules.

Are lower monthly payments always better? Not always. A lower payment can improve monthly cash flow, but it may come from a longer term, higher rate, lender credit, interest-only structure, or delayed principal repayment. Always compare total cost and future payment risk.

What should I check before signing loan documents? Review the Loan Estimate and Closing Disclosure for rate, APR, projected payments, escrow items, closing costs, points, lender credits, mortgage insurance, prepayment penalties, balloon payments, and whether the payment can increase.

Do extra principal payments automatically lower my monthly payment? Usually no. Extra principal payments can reduce total interest and shorten the payoff timeline, but the required monthly payment often stays the same unless the loan is recast or refinanced.

Get Clear on the Payment Terms Before You Choose a Loan

Loan payment terms can make a mortgage more affordable, more expensive, more flexible, or more predictable. The details matter, especially when you are comparing loan options that look similar at first glance.

New Era Lending helps borrowers review mortgage scenarios with smart technology and personalized human guidance, including home purchase, refinance, and equity access options. If you want a clearer view of your monthly payment, cash to close, and long-term cost, connect with New Era Lending to compare options before you commit.