.jpg)

.jpg)

.jpg)

Monthly Mortgage Costs: What Buyers Often Miss

A mortgage calculator can make home shopping feel deceptively simple: enter the price, down payment, interest rate, and loan term, then look at the result. But the number on the screen is not always the full story.

For many buyers, monthly mortgage costs start with principal and interest, then grow once taxes, insurance, mortgage insurance, HOA dues, utilities, maintenance, and lifestyle changes enter the picture. Some of these are included in the payment you send to your mortgage servicer. Others arrive as separate bills. Either way, they affect the same household budget.

The goal is not to scare you away from buying. It is to help you shop with clearer numbers, so your home feels comfortable after closing, not just affordable on paper.

Why the monthly mortgage number is easy to underestimate

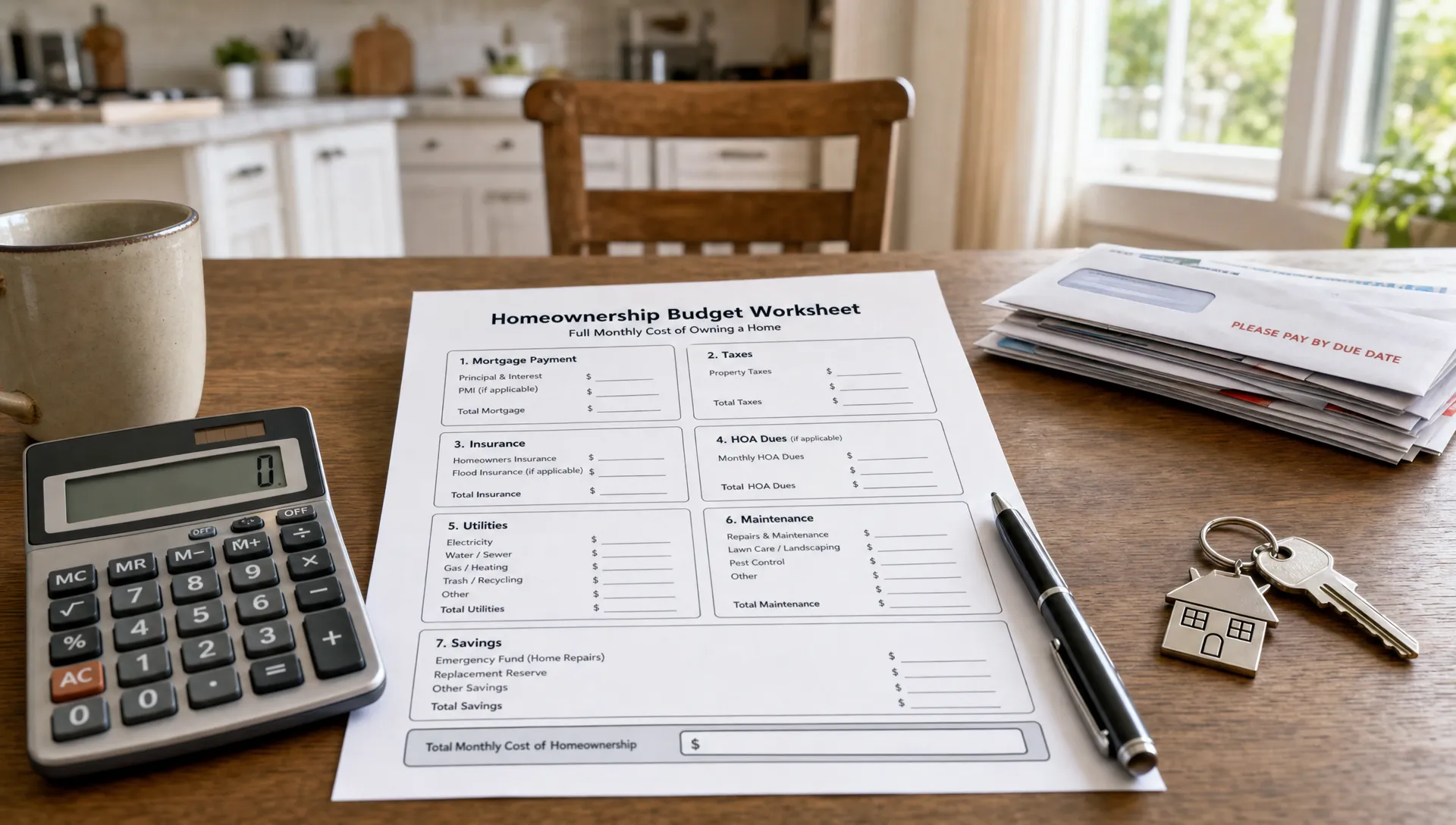

When people say monthly mortgage, they often mean the loan payment. In practice, homeownership includes several layers of cost. The base loan payment is usually made up of principal and interest, while escrow may add property taxes and homeowners insurance. Depending on your loan, it may also include mortgage insurance.

That is why two homes with the same purchase price can have very different monthly costs. One may sit in a higher tax district. Another may require flood insurance. A condo may have lower exterior maintenance but higher monthly HOA dues. A newer home may cost more upfront but need fewer repairs in the first few years.

If you want a deeper breakdown of the standard payment formula, New Era Lending has a helpful guide on how to estimate your monthly mortgage payment. This article goes one step further by focusing on the costs buyers often forget to include when deciding what they can comfortably afford.

Cost component | What it covers | Why buyers miss it

Principal | The portion that repays the loan balance | It is usually visible in every calculator

Interest | The cost of borrowing money | It changes based on rate, loan size, and term

Property taxes | Local taxes based on assessed value and tax rules | They may change after purchase or reassessment

Homeowners insurance | Coverage for the home and certain risks | Premiums vary widely by location and property type

Mortgage insurance | Protection for the lender on certain low down payment loans | It may be overlooked until the loan estimate stage

HOA dues | Community fees for condos, townhomes, or planned communities | They may be paid separately from the mortgage Property taxes can change after you buy

Property taxes are one of the biggest surprises for buyers because they are not always stable from year to year. A listing may show the previous owner’s tax bill, but that number may reflect exemptions, a lower assessed value, or a valuation from before the sale.

After closing, your local tax authority may reassess the property. If the assessed value rises, your monthly escrow payment can rise too. Even if your mortgage payment was affordable at closing, an escrow adjustment can make the next year feel tighter.

A practical step is to look up the county or city tax assessor’s information before making an offer. Ask your mortgage professional how taxes are being estimated, especially if the seller has owned the home for a long time or if the home is new construction.

Homeowners insurance is not one-size-fits-all

Homeowners insurance can vary based on the home’s age, roof condition, construction type, claims history, location, coverage limits, and deductible. Buyers sometimes use a rough estimate early in the process, then feel surprised when the real quote comes in higher.

Location matters. A home in an area with hurricane, wildfire, hail, or flood exposure may require more careful insurance planning. Flood insurance, for example, is separate from standard homeowners insurance and may be required by the lender if the property is in a designated flood zone.

Insurance also changes over time. Premiums can increase at renewal, and coverage needs may change after renovations or personal property upgrades. Before you commit to a home, get an actual insurance quote rather than relying only on a generic estimate.

Mortgage insurance may apply even if the payment looks manageable

If you put less than 20% down on many conventional loans, private mortgage insurance may be required. FHA loans generally have mortgage insurance premiums, and other loan programs have their own fee structures. These costs can affect either the monthly payment, the upfront cost, or both.

Mortgage insurance is not necessarily bad. It can help buyers purchase sooner with a smaller down payment. The key is understanding how it affects your monthly budget and whether it can eventually be reduced or removed based on the loan type and equity position.

For a more detailed explanation, review New Era Lending’s guide to property mortgage insurance costs, rules, and ways to avoid it.

HOA dues can change the affordability equation

HOA dues are common with condos, townhomes, and some single-family communities. They may cover amenities, exterior maintenance, landscaping, insurance for common areas, reserves, or community management. But they are usually not optional, and lenders often factor them into qualification.

A lower-priced condo with a high HOA fee may have a higher total monthly housing cost than a more expensive property with no HOA. Buyers should also review whether the HOA has reserve funds, pending repairs, special assessments, or planned increases.

The monthly dues are only one part of the picture. Special assessments can create large one-time costs, while underfunded reserves may increase the risk of future fee hikes.

Utilities and services often grow with the home

Moving from an apartment to a house can change utility costs dramatically. Electricity, gas, water, sewer, trash, internet, and security services can all cost more in a larger space. Older homes may be less energy efficient. Homes with pools, large lawns, irrigation systems, or multiple HVAC units may have higher routine costs.

Buyers often focus on the mortgage because it is the largest bill, but utilities are part of real affordability. If possible, ask the seller for average utility costs. If that is not available, research local utility rates and consider the home’s size, insulation, windows, and heating or cooling systems.

Maintenance is not monthly, but your budget should treat it that way

A home does not need a new water heater, roof, appliance, or HVAC repair every month. But when those costs arrive, they can be expensive. That is why many homeowners create a monthly maintenance fund even if no repair is currently needed.

A common starting point is to set aside around 1% of the home’s value per year for maintenance, then adjust based on the property’s age, condition, climate, and features. A newer home may need less at first. An older home with mature trees, aging systems, or deferred maintenance may need more.

The key is to avoid treating maintenance as an emergency every time. Saving monthly turns irregular expenses into a planned part of homeownership.

Lifestyle costs still matter after closing

Your mortgage approval does not know everything about your life. It may not fully reflect childcare, healthcare, family support, hobbies, dining out, travel, or the cost of a longer commute.

A home should leave room for the life you want to keep living. If annual travel is important to your household, for example, compare your new housing budget against that goal before planning experiences like handpicked Mexico tours. The same logic applies to weddings, school tuition, car replacement, or building a cash reserve.

Affordability is not only whether you can make the payment. It is whether the payment allows you to stay financially flexible.

Approval is not the same as comfort

A mortgage pre-approval is an important step, but it is not the same as a personal budget. Lenders evaluate income, credit, debts, assets, loan program requirements, and estimated housing costs. That helps determine what you may qualify to borrow.

Your comfort number may be lower than your approval number. That is normal. A lender may not fully account for your grocery preferences, savings goals, family obligations, future car purchase, medical costs, or how much breathing room helps you sleep at night.

The Consumer Financial Protection Bureau explains that a Loan Estimate helps borrowers compare loan terms, projected payments, and closing costs. Use that document as a starting point, then add your own real-life costs before deciding on an offer price.

Qualification view | Personal affordability view

Income and employment | Income stability and comfort with risk

Credit profile and existing debts | Savings goals, retirement contributions, and family priorities

Estimated taxes and insurance | Possible tax increases, insurance renewals, and utility changes

Required down payment and cash to close | Emergency fund after closing

Loan program guidelines | Lifestyle flexibility after moving Even with a fixed-rate mortgage, your total monthly housing cost can change. Buyers sometimes assume fixed rate means fixed payment forever. In reality, the principal and interest portion may stay fixed, but escrowed items can move.

Property taxes may rise. Insurance premiums may renew at a higher amount. HOA dues may increase. If your servicer paid more from escrow than expected, you may have an escrow shortage that is spread across future payments.

Loan structure matters too. Adjustable-rate mortgages, temporary buydowns, interest-only periods, and certain loan features can change payment expectations over time. These options can be useful in the right situation, but they require careful planning.

If you are comparing loan structures, New Era Lending’s article on loan payment terms that can raise or lower costs can help you understand how term length, rate type, points, credits, escrow, and mortgage insurance may affect the total cost.

A simple way to build a realistic monthly mortgage budget

Before making an offer, create a housing budget that includes both the lender’s estimate and your own homeowner costs. You do not need a complicated spreadsheet, but you do need to be honest.

- Start with the estimated principal and interest payment.

- Add property taxes, homeowners insurance, and any mortgage insurance.

- Add HOA dues, condo fees, or community assessments if they apply.

- Estimate utilities, internet, trash, lawn care, pest control, and other recurring services.

- Create a monthly maintenance reserve for repairs and future replacements.

- Add a lifestyle buffer for savings, transportation, childcare, healthcare, and personal priorities.

- Stress-test the total by asking whether you could handle higher taxes, insurance, or one surprise repair.

The final number may be higher than the mortgage calculator result. That is useful information, not bad news. It helps you choose the right price range, compare homes more accurately, and avoid stretching into a payment that limits your options later.

Questions to ask before choosing a home

A good mortgage conversation should go beyond the interest rate. The rate matters, but the payment is only one part of the decision. Ask questions that reveal what the home will really cost month after month.

Consider asking your loan professional, insurance agent, real estate agent, or the HOA for clarity on these items:

- What tax estimate is being used, and could it change after purchase?

- Is the insurance estimate based on a real quote or a rough assumption?

- Will mortgage insurance apply, and how long might it last?

- Are there HOA dues, special assessments, or planned increases?

- Which costs are escrowed, and which will I pay separately?

- What would the payment look like if taxes or insurance increased next year?

These questions help you move from a basic payment estimate to a more complete ownership plan.

Frequently Asked Questions

What are monthly mortgage costs? Monthly mortgage costs usually include principal and interest, and may also include property taxes, homeowners insurance, mortgage insurance, and escrow items. Buyers should also budget for separate costs like HOA dues, utilities, maintenance, and services.

Why did my monthly mortgage payment increase if I have a fixed rate? With a fixed-rate mortgage, the principal and interest portion generally stays the same, but taxes, insurance, HOA dues, or escrow shortages can increase your total monthly payment.

Should I include utilities in my mortgage budget? Yes. Utilities are not usually part of the mortgage payment, but they are part of the cost of owning the home. Electricity, gas, water, sewer, trash, and internet can meaningfully affect affordability.

How much should I save each month for home maintenance? A common starting point is to save around 1% of the home’s value per year, divided monthly. Adjust higher or lower based on the home’s age, condition, systems, location, and your emergency fund.

Is the lowest monthly mortgage payment always the best choice? Not always. A lower payment may come from a longer term, upfront points, an adjustable rate, or a structure that changes later. Compare the full loan terms, cash needed at closing, and long-term cost before deciding.

Make your monthly mortgage clearer before you commit

The best homebuying decisions are made with the full monthly picture in view. Principal and interest matter, but so do taxes, insurance, maintenance, HOA dues, utilities, and the life you want after moving in.

New Era Lending combines smart mortgage technology with personalized human guidance to help buyers, homeowners, and refinancers understand their options with more confidence. If you are planning a purchase, refinance, or equity strategy, explore personalized mortgage solutions from New Era Lending and get clearer about what your monthly costs could really look like.