.jpg)

.jpg)

.jpg)

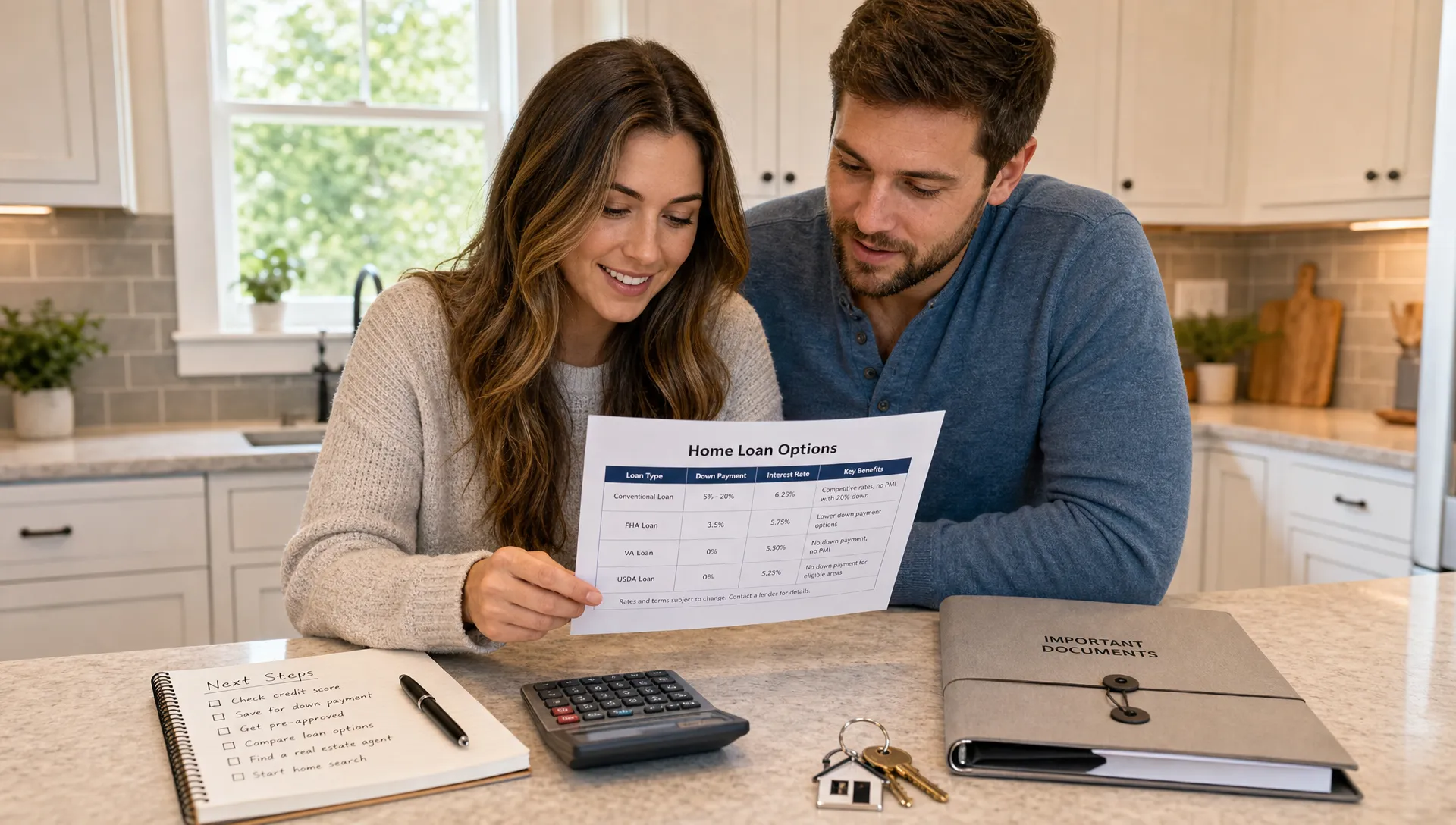

No Down Payment Options for First-Time Buyers

Saving for a down payment is one of the biggest reasons renters postpone buying. The good news is that 20% down is not a requirement, and for some buyers, the required down payment can be 0%.

The important catch: no down payment does not always mean no money due at closing. A first-time buyer may still need funds for closing costs, prepaid taxes, homeowners insurance, inspections, moving expenses, and a small emergency cushion after closing. The right strategy is not just finding a zero-down loan, it is finding a payment, property, and cash-to-close plan that fits your life.

Below are the main no down payment options for first-time buyers, how they work, and how to decide which path is worth exploring before you start house hunting.

What no down payment really means

A down payment is the portion of the home price you pay upfront instead of financing. If you buy a $300,000 home with 3% down, your down payment is $9,000. A no down payment mortgage allows you to finance the full purchase price, or use approved assistance so your own required down payment is reduced to zero.

That does not erase every upfront cost. Depending on your loan and local market, cash to close can include:

- Lender fees, appraisal fees, title fees, and recording fees.

- Prepaid homeowners insurance, property taxes, and escrow deposits.

- Earnest money deposit, which may be credited back at closing.

- Inspection costs, moving costs, and immediate repairs or furnishings.

Some buyers reduce these costs through seller concessions, lender credits, gift funds, or down payment assistance. Each option has rules, and stacking them incorrectly can delay approval. That is why first-time buyers should talk through the whole file early, not just ask whether 0% down is possible.

VA loans: the strongest zero-down option for eligible buyers

For eligible service members, veterans, some surviving spouses, and certain National Guard or Reserve members, VA loans are often the most powerful no down payment program available. The U.S. Department of Veterans Affairs guarantees a portion of the loan, which allows approved lenders to offer qualified borrowers up to 100% financing.

VA loans are not limited to first-time buyers, but they can be especially helpful for first-time buyers because they typically do not require monthly mortgage insurance. Borrowers may pay a VA funding fee unless exempt, and that fee can often be financed into the loan. Eligibility, residual income, credit profile, and property requirements still matter.

A VA loan may be a strong fit if you have qualifying military service, plan to live in the home as your primary residence, and want to preserve cash instead of tying it all up in a down payment. The tradeoff is that the property must meet VA standards, and in competitive markets, your offer strategy should be prepared carefully so sellers understand the strength of your financing.

USDA loans: 0% down for eligible rural and suburban homes

USDA loans are another true no down payment option. Despite the name, they are not only for farms. Many small towns, outer suburbs, and less densely populated communities may fall within eligible areas. The USDA Single Family Housing Guaranteed Loan Program is designed to support homeownership for qualified buyers in approved locations.

USDA loans generally require the home to be your primary residence, the property to be in an eligible area, and your household income to fall within program limits for that location and household size. They also include guarantee fees, which can affect your monthly payment and total cost.

This option can be excellent for buyers who are open to where they live. If you are willing to look beyond the most central neighborhoods, a USDA-eligible area may give you more purchasing power with no required down payment.

Down payment assistance: turning a low-down loan into a no-down path

Down payment assistance is not always a mortgage by itself. Instead, it can help cover the required down payment on a loan that normally needs 3% or 3.5% down. That means a buyer using FHA, conventional, or another eligible loan may be able to purchase with little or none of their own money toward the down payment.

Assistance programs can come from state housing agencies, local governments, nonprofit organizations, or approved lenders. Common structures include grants, forgivable second mortgages, deferred-payment loans, and low-interest second loans. Some programs can also help with closing costs.

The details matter. Many assistance programs have income limits, purchase price caps, first-time buyer definitions, homebuyer education requirements, or rules about how long you must occupy the home. Some are forgivable over time, while others must be repaid when you sell, refinance, or pay off the first mortgage.

If this path interests you, review New Era Lending's guide to down payment assistance for first-time home buyers for a deeper look at how these programs are commonly structured.

100% financing and specialty lender programs

Some banks, credit unions, and mortgage companies offer 100% financing programs for qualified buyers. These programs vary widely. Some are tied to income limits, specific neighborhoods, first-time buyer status, profession, employer partnerships, or membership requirements.

A specialty 100% financing program can be a great solution, but it deserves careful comparison. Look at the full loan estimate, not just the down payment. A program with no down payment could still have a higher interest rate, higher fees, mortgage insurance, or stricter property rules.

When comparing options, ask how the monthly payment changes, whether assistance is repayable, whether the rate is fixed or adjustable, and what happens if you refinance or sell within a few years. You can also compare broader home loans with no down payment to understand where specialty programs fit beside VA, USDA, and assistance-based options.

Low-down loans that can still reduce your out-of-pocket costs

Not every first-time buyer qualifies for a true zero-down mortgage. That does not mean buying is out of reach. FHA loans can allow 3.5% down for eligible borrowers, and some conventional first-time buyer programs may allow as little as 3% down. With approved gift funds, employer assistance, or down payment assistance, your personal contribution can sometimes be reduced significantly.

Seller credits may also help with closing costs, although they usually cannot simply replace the buyer's required down payment. Lender credits can reduce upfront costs too, but they may come with a higher interest rate. These tools can be useful, but they should be evaluated alongside your monthly payment and long-term plans.

How to decide which no down payment option fits you

The best option depends on eligibility first. If you qualify for a VA loan, start there. If you are open to eligible rural or suburban areas, check USDA next. If neither applies, assistance programs or specialty lender options may be the next place to look.

Monthly payment matters just as much as cash due at closing. Putting less down means you borrow more, so your principal and interest payment may be higher. Depending on the program, you may also pay mortgage insurance, guarantee fees, or funding fees. A no down payment loan can still be the right choice if it preserves emergency savings, gets you into a stable home sooner, or helps you stop paying rising rent. It is not automatically the cheapest option.

Your timeline matters too. Some assistance programs take extra documentation, education courses, or approval steps. In a fast-moving market, you want this sorted out before you make an offer. Your lender should be able to explain what you qualify for, how strong your preapproval is, and what conditions could affect closing.

Finally, think about how long you expect to stay in the home. If you plan to sell quickly, a zero-down loan leaves you with less equity at the start, which can matter if home values flatten or selling costs are high. If you plan to stay longer and your payment is comfortable, preserving savings may be worth more than making a larger down payment.

Qualification factors first-time buyers should review early

Lenders look at more than whether a program allows 0% down. Before you rely on a no down payment option, review these areas:

- Credit history: Program guidelines vary, and lenders may have their own credit requirements.

- Income stability: W-2 income, self-employment income, overtime, bonuses, and variable income may be documented differently.

- Debt-to-income ratio: Student loans, car payments, credit cards, and personal loans can affect buying power.

- Cash reserves: Even with no down payment, reserves can help approval strength and protect you after closing.

- Property fit: Condos, manufactured homes, multi-unit properties, repairs, and appraisal issues may have special rules.

- Occupancy: Most no down payment purchase programs require the home to be your primary residence.

First-time buyers often focus on the purchase price first, but a lender will look at the whole picture. A slightly lower purchase price with a better tax profile, lower insurance cost, or stronger seller credit may be easier to afford than a more expensive home that technically fits your preapproval.

Common mistakes to avoid

One common mistake is assuming no down payment means no savings are needed. Even if your loan covers 100% of the purchase price, you may need money for inspections, appraisal gaps, moving, utility deposits, and repairs. Buying with no reserves can turn a successful closing into a stressful first year.

Another mistake is waiting until you find a house to ask about assistance. Many programs must be approved before closing, and some require specific lenders, education certificates, or property locations. If you wait too long, you may discover that a program you hoped to use cannot be paired with your loan or timeline.

A third mistake is comparing only the interest rate. Two loans with the same rate can have very different upfront costs, mortgage insurance, assistance repayment terms, or seller credit limits. Ask for a clear cash-to-close estimate and a monthly payment breakdown that includes principal, interest, taxes, insurance, mortgage insurance if applicable, and HOA dues if relevant.

A practical plan for buying with little or no down

Use a structured process before you tour homes:

- Get preapproved early: A preapproval helps confirm your budget, documents, and likely loan options before you fall in love with a property.

- Check VA and USDA eligibility first: These are the most common true zero-down programs, but eligibility is specific.

- Ask about assistance before making offers: Down payment assistance can be powerful, but program rules can affect timing and property choice.

- Build a complete cash-to-close estimate: Include closing costs, prepaid items, inspections, moving, reserves, and any funds already paid as earnest money.

- Compare the full cost, not just the down payment: Review rate, APR, fees, mortgage insurance, assistance repayment, and monthly payment.

- Keep your finances steady until closing: Avoid new debt, large unexplained deposits, job changes, or major purchases unless your loan team confirms they are acceptable.

If you are tightening your budget to prepare for homeownership, keep the approach realistic. You do not have to cancel every enjoyable purchase, but you should make each one intentional. A small entertainment budget for local shows, streaming, or digital music from an independent artist's official online music shop is easier to manage than untracked impulse spending. The goal is to protect your homebuying funds without making the process feel impossible.

When no down payment is a smart move

A no down payment mortgage can be smart when it helps you buy a home you can comfortably afford while keeping cash available for emergencies. It may be especially useful if rents are rising, you have stable income, your credit is in good shape, and your expected payment leaves room for maintenance and savings.

It may be less ideal if the only way the numbers work is by stretching your monthly budget. Homeownership includes costs that do not appear in a rent payment, such as repairs, lawn care, appliances, higher utilities, and future tax or insurance changes. A sustainable payment is more valuable than the lowest possible upfront cost.

The best first step is a personalized comparison. Ask your lender to show you a side-by-side view of zero-down, low-down, and assistance-based options so you can see the difference in cash to close, monthly payment, and long-term cost.

Frequently Asked Questions

Can first-time buyers really buy a house with no down payment? Yes, some can. VA loans and USDA loans may allow 0% down for eligible buyers, and down payment assistance may cover the required down payment on certain low-down-payment loans. Qualification depends on eligibility, income, credit, property type, and location.

Does no down payment mean I need no money at all? Usually, no. You may still need money for closing costs, prepaid taxes and insurance, inspections, moving, and reserves. Seller credits, lender credits, gift funds, or assistance may reduce the amount you need at closing.

Is a USDA loan only for farms? No. USDA eligibility is based on property location and income rules, and many eligible homes are in small towns or suburban areas. You must check the property address and household income against current USDA guidelines.

Do VA loans require mortgage insurance? VA loans typically do not require monthly mortgage insurance, which can be a major benefit. However, many borrowers pay a VA funding fee unless exempt, and that fee may often be financed.

What credit score do I need for no down payment options? Requirements vary by program and lender. VA, USDA, assistance programs, and specialty 100% financing options may all use different credit standards. A lender can review your full profile and explain which programs may fit.

Should I wait until I have a bigger down payment? It depends on your payment comfort, savings, market conditions, and available programs. Waiting can give you more cash and equity, but it may also mean paying rent longer or facing higher home prices. Compare both scenarios before deciding.

Explore your first-time buyer options with guidance

No down payment options for first-time buyers can open the door to homeownership, but the best choice depends on more than one program name. Eligibility, closing costs, monthly payment, property location, and long-term affordability all need to work together.

New Era Lending combines smart mortgage technology with personalized human guidance to help buyers compare purchase options with clarity. If you are ready to understand what you may qualify for, start with New Era Lending and review your path before you begin making offers.