.jpg)

.jpg)

.jpg)

Home Loans With No Down Payment: Your Best Options

Home loans with no down payment can make homeownership feel much closer, especially when saving tens of thousands of dollars is the biggest barrier standing between you and a set of keys. But zero down does not mean zero cost, and the best option depends on your eligibility, the property location, your credit profile, and how much monthly payment you can comfortably afford.

The good news: a 20% down payment is not the standard requirement many buyers think it is. In fact, if you qualify for the right program, you may be able to finance 100% of the purchase price. If you are still comparing the broader landscape, it helps to start with the basics of why you do not need 20% down to buy a home.

Below are the strongest home loans with no down payment, how they work, where they shine, and what to watch before you apply.

What no down payment really means

A no-down-payment mortgage means you are not required to put a percentage of the purchase price toward the home at closing. If you buy a $350,000 home with true 100% financing, the mortgage can cover the $350,000 purchase price.

That is different from having no cash due at closing. Even with a zero-down loan, buyers often need to plan for closing costs and prepaid expenses. These may include lender fees, title costs, escrow setup, homeowners insurance, property taxes, appraisal fees, inspections, and sometimes an upfront program fee.

In simple terms, there are three cash categories to understand:

- Down payment: The portion of the purchase price you pay upfront.

- Closing costs: Fees and third-party costs required to complete the loan.

- Cash to close: Your total amount due at closing after credits, deposits, gifts, and assistance are applied.

The right strategy is not always just finding a $0 down payment. It is finding the lowest practical cash-to-close structure without creating a payment that strains your monthly budget.

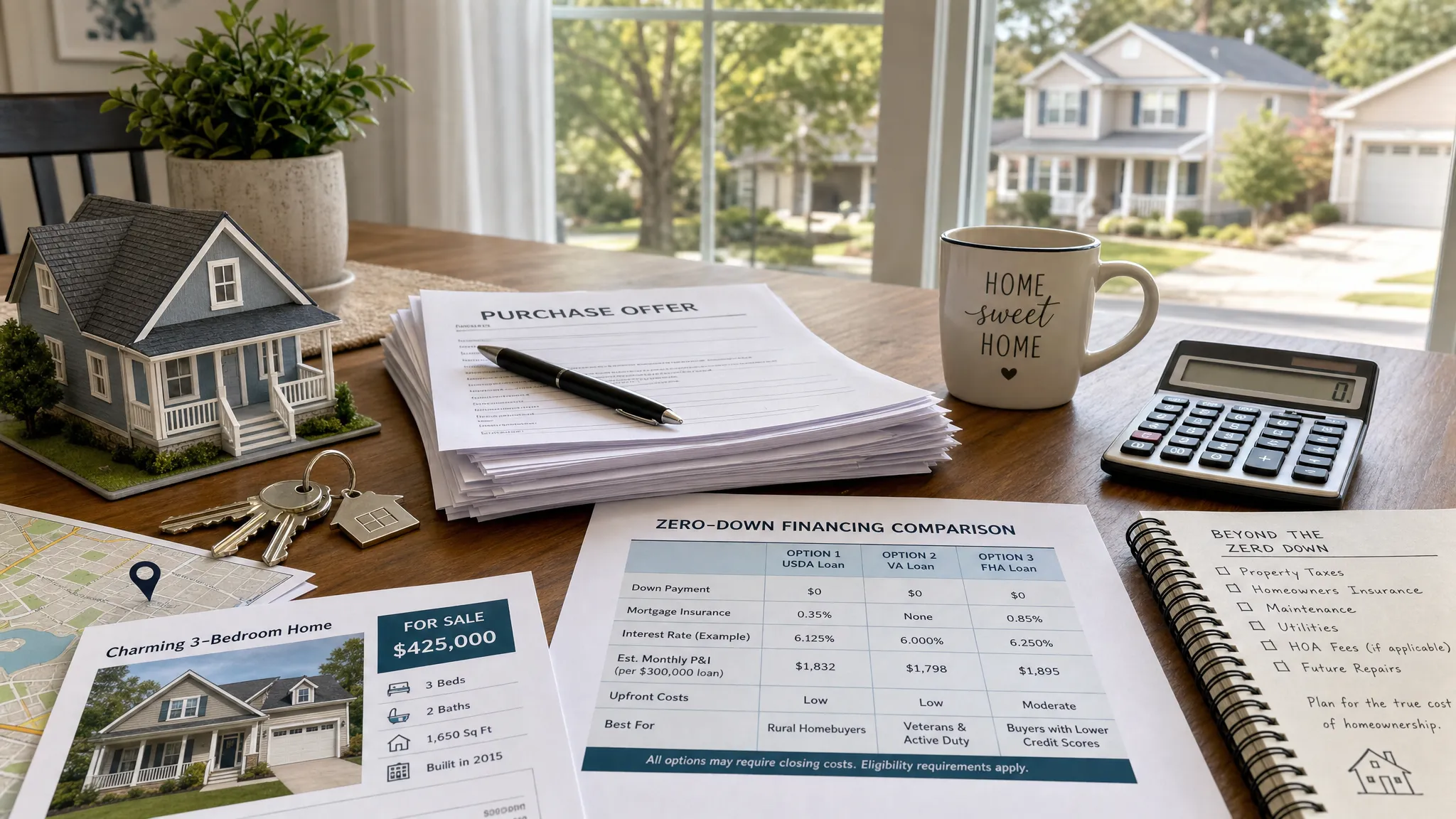

Best option 1: VA loans for eligible military borrowers

For eligible veterans, active-duty service members, certain National Guard and Reserve members, and qualifying surviving spouses, a VA loan is often the best no-down-payment mortgage available.

The VA purchase loan benefit is designed to help eligible borrowers buy a primary residence with favorable terms. In many cases, qualified borrowers can purchase with 0% down, and VA loans do not require monthly private mortgage insurance.

That combination can be powerful. Avoiding both a down payment and monthly PMI may help keep more cash available for moving, repairs, emergency savings, or future financial goals.

VA loans are especially strong if you:

- Have eligible military service or surviving spouse eligibility.

- Plan to buy a primary residence.

- Want to minimize upfront cash without automatically adding monthly PMI.

- Have enough income to support the payment, taxes, insurance, and other debts.

There are still important details to review. VA loans can include a funding fee unless the borrower is exempt, such as some veterans receiving VA disability compensation. The home must meet VA property standards, and if the appraised value is lower than the purchase price, you may need to renegotiate or cover the difference unless the seller adjusts.

If this path may apply to you, it is worth reviewing the specific VA loan down payment rules before you start shopping.

Best option 2: USDA loans for eligible rural and suburban homes

USDA loans are another major no-down-payment option, and they are not limited to farmland. Many eligible areas are small towns, outer suburbs, and communities outside dense urban centers.

The USDA Single Family Housing Guaranteed Loan Program supports low-to-moderate-income buyers purchasing eligible primary residences in approved areas. If you qualify, a USDA loan may allow 100% financing.

USDA loans can be a strong fit if you:

- Are buying in an eligible rural or suburban location.

- Meet household income limits for the area.

- Plan to occupy the property as your primary residence.

- Want a fixed-rate loan with no required down payment.

The biggest limitation is eligibility. Both the buyer and the property must qualify. Income limits vary by county and household size, and the home must be located in a USDA-eligible area. USDA loans also include guarantee fees, which can affect your total monthly payment.

For buyers who are flexible about location, USDA can be one of the most practical home loans with no down payment. For buyers locked into a city center or a higher-income household, it may not be available.

Best option 3: Down payment assistance paired with FHA or conventional loans

Some buyers do not qualify for VA or USDA, but can still get close to a no-down-payment outcome through down payment assistance, often called DPA.

Down payment assistance is usually offered through state housing agencies, local governments, nonprofits, or approved lending partners. It may come as a grant, forgivable second mortgage, deferred-payment loan, or low-interest second loan. When paired with an FHA or conventional mortgage, assistance may cover the required down payment and sometimes part of the closing costs.

This matters because FHA loans do not offer zero down by themselves. FHA typically requires a minimum down payment, and many conventional first-time buyer programs also require at least a small down payment. Assistance can be the bridge that reduces your out-of-pocket contribution.

DPA may be a fit if you:

- Are a first-time buyer or have not owned a home recently.

- Meet income and purchase price limits.

- Are buying in an eligible area.

- Can complete any required homebuyer education.

- Understand the repayment or forgiveness rules before closing.

The terms matter. A grant that never has to be repaid is very different from a second mortgage that becomes due when you sell or refinance. Some programs require you to live in the home for a set number of years before the assistance is forgiven.

If this route sounds relevant, New Era Lending has a deeper guide to down payment assistance for first-time home buyers that explains how these programs are commonly structured.

Best option 4: 100% financing from lenders, credit unions, or community programs

Some lenders and credit unions offer 100% financing programs outside the major VA and USDA paths. These may be designed for first-time buyers, moderate-income households, certain professions, or properties in specific communities.

These programs can be helpful, but the details vary widely. One lender might use a primary mortgage plus a second loan. Another might offer lender-paid mortgage insurance in exchange for a different rate structure. Some programs are only available in certain counties, for certain income levels, or to borrowers with stronger credit.

A 100% financing program may be worth exploring if you:

- Do not qualify for VA or USDA.

- Have stable income and manageable debts.

- Have good credit but limited cash saved.

- Are comfortable comparing rate, APR, mortgage insurance, and second-lien terms carefully.

The key is not to assume that every zero-down structure is automatically cheaper. A loan with no down payment can still cost more over time if it comes with a higher rate, higher fees, mortgage insurance, or restrictive repayment terms. Ask your lender to compare it side by side with a low-down-payment option so you can see the true monthly and long-term cost.

Best option 5: Credits, gifts, and incentives that reduce cash to close

Seller credits, builder incentives, lender credits, and gift funds are not always home loans with no down payment by themselves, but they can help reduce how much money you need to bring to closing.

A seller credit can often be used toward closing costs and prepaid expenses, subject to program limits. A builder incentive may help cover closing costs or buy down the interest rate on new construction. A lender credit may reduce upfront costs in exchange for a different rate. Gift funds from an eligible donor may help cover some or all of the required down payment, depending on the loan program.

These tools are especially useful when combined with a low-down-payment or assistance program. For example, if assistance covers the down payment and a seller credit covers closing costs, your cash to close may be significantly reduced.

Just be careful with assumptions. Credits usually have limits, and not every type of credit can be used for every purpose. Your lender should confirm what is allowed before you write an offer.

Why zero down can be a liquidity strategy

No-down-payment mortgages are often framed as a solution for buyers without savings. That is true in many cases, but it is not the only reason buyers use them. Some borrowers have cash, but prefer to keep it available for emergency reserves, renovations, moving costs, childcare, business needs, or investments.

For example, if a buyer has funds tied up in a business venture or an alternative asset class, such as someone researching crypto mining in UAE, they may not want to liquidate a large amount of cash solely to make a down payment. In that situation, a no-down-payment mortgage can preserve flexibility, as long as the borrower still qualifies and the monthly payment remains sustainable.

That last point is critical. Liquidity is valuable, but it should not come at the cost of becoming house poor. A strong mortgage plan leaves room for repairs, higher utility bills, insurance changes, and the normal surprises that come with homeownership.

Which no-down-payment option is best for you?

There is no single best zero-down mortgage for every buyer. The right choice depends on your profile.

- Eligible veteran, active-duty service member, or surviving spouse: Start with VA. It is often the strongest combination of no down payment and no monthly PMI.

- Buyer in a USDA-eligible area with qualifying income: Compare USDA early, especially if you are open to rural or outer-suburban locations.

- First-time buyer with limited savings: Look at down payment assistance paired with FHA or conventional financing.

- Buyer with good credit but no VA or USDA eligibility: Ask about 100% financing through lender, credit union, or community programs.

- New construction buyer: Review builder incentives, but compare the home price and interest rate carefully.

The best loan is not always the one with the lowest upfront cost. It is the one that balances upfront cash, monthly payment, long-term interest, mortgage insurance, flexibility, and your comfort level.

How to compare home loans with no down payment

When you receive options, do not compare them only by down payment. Ask your lender to show the complete picture.

Focus on these factors:

- Total cash to close: This is the number that matters most for your upfront budget.

- Monthly payment: Include principal, interest, taxes, insurance, HOA dues, mortgage insurance, and program fees.

- APR and rate structure: A lower cash-to-close option may carry a higher long-term cost.

- Mortgage insurance or guarantee fees: VA, USDA, FHA, and conventional programs handle these differently.

- Assistance repayment rules: Know whether aid is a grant, forgivable loan, deferred loan, or repayable second mortgage.

- Property restrictions: Some programs limit location, occupancy, property type, or condition.

- Timeline: Assistance programs and certain property approvals may add steps, so plan ahead.

A good loan comparison should make the tradeoffs easy to see. If two options both allow you to buy with little or no money down, the better one is usually the option that gives you the most stable payment and the least restrictive terms for your goals.

Steps to take before you apply

Getting ready early can help you avoid surprises and strengthen your offer when you find the right home.

- Check your eligibility first: Confirm whether VA, USDA, DPA, or special 100% financing programs may apply before you focus on homes.

- Review your credit and debts: Zero-down loans still require the lender to verify that the payment is affordable.

- Get a realistic preapproval: A preapproval should include estimated taxes, insurance, mortgage insurance or fees, and likely cash to close.

- Ask about combining programs: Some buyers can combine assistance, credits, and gifts, but the rules must be checked in advance.

- Confirm property eligibility before making an offer: This is especially important for USDA, condo approvals, and homes needing repairs.

- Keep reserves if possible: Even if reserves are not required, having money left after closing can make homeownership much less stressful.

This is where a guided mortgage process helps. Technology can make document uploads, e-signatures, and approval steps faster, but human guidance is what helps you understand which option actually fits your life.

Common mistakes to avoid

The biggest mistake is assuming no down payment means no money needed. Inspections, earnest money, appraisal gaps, and closing costs can still matter. Even if credits or assistance cover much of the cost, you should know the numbers before you make an offer.

Another mistake is focusing only on getting approved. Approval is not the same as affordability. A loan may technically fit underwriting guidelines but still leave you with a payment that feels uncomfortable after utilities, maintenance, groceries, transportation, and savings.

Finally, do not ignore the exit rules on assistance programs. If a second mortgage must be repaid when you sell or refinance, that can affect your future flexibility. The program may still be worth it, but you should understand the tradeoff before closing.

Frequently Asked Questions

Are there truly home loans with no down payment? Yes. VA and USDA loans are the two most common major mortgage programs that may allow eligible borrowers to finance 100% of the purchase price. Some lender, credit union, and assistance programs may also create a zero-down structure.

Do FHA loans offer no down payment? Not by themselves. FHA loans generally require a minimum down payment, but eligible down payment assistance or gift funds may be used to cover that requirement if program rules allow.

Can closing costs be rolled into a no-down-payment mortgage? Sometimes certain upfront program fees can be financed, such as some VA and USDA fees, but typical purchase closing costs usually need to be paid through borrower funds, seller credits, lender credits, gifts, or assistance.

Is a no-down-payment mortgage more expensive? It can be. With less equity upfront, you may have a higher loan balance and potentially more interest over time. Some programs also include mortgage insurance or guarantee fees. The right comparison should include monthly payment, APR, cash to close, and long-term cost.

Can first-time buyers get a home loan with no down payment? Yes, depending on eligibility. First-time buyers may qualify through USDA, VA if eligible, down payment assistance, or certain 100% financing programs. Program rules vary by location, income, credit, and property type.

What credit score do I need for a zero-down home loan? Requirements vary by loan program and lender. VA does not set one universal minimum credit score, but lenders may apply their own guidelines. USDA, DPA, and 100% financing programs also vary, so it is best to review your full profile with a mortgage professional.

Find your best no-down-payment path

Home loans with no down payment can open the door to buying sooner, but the right choice depends on more than the down payment line. You need to know your eligibility, your true cash to close, your monthly payment, and the tradeoffs behind each program.

New Era Lending helps buyers compare personalized mortgage solutions with smart technology and human guidance across 39 states. If you are considering a no-down-payment loan, start by reviewing your options, confirming eligibility, and building a mortgage plan that supports both your purchase and your long-term financial confidence.