.jpg)

.jpg)

.jpg)

How to Find the Right Loan Without Guesswork

Finding the right loan should feel less like guessing and more like narrowing a set of choices with clear criteria. The challenge is that mortgage options can sound similar on the surface. One loan has a lower rate, another has lower cash to close, another promises speed, and another may fit a specific borrower profile better.

The best way to choose is not to ask, “What is the cheapest loan?” It is to ask, “Which loan best fits my budget, timeline, cash position, risk tolerance, and long-term plan?” That shift turns a confusing search into a structured decision.

Below is a practical framework you can use whether you are buying a home, refinancing, or looking to access home equity.

Start with the job the loan needs to do

Before comparing rates or loan names, define the purpose of the loan. A purchase loan, refinance, cash-out refinance, and home equity solution are not judged by the exact same standard.

If you are buying a home, the loan needs to support your offer strategy, fit your monthly budget, and close on time. If you are refinancing, the loan should improve your financial position in a measurable way, such as lowering your payment, shortening your term, changing loan type, removing mortgage insurance, or accessing equity. If you are using home equity, the right loan should be evaluated against the purpose of the funds, the repayment plan, and the cost of replacing or adding debt.

This first step matters because a loan that looks “best” for one goal may be wrong for another. A borrower planning to stay in a home for 20 years may value long-term stability. A borrower planning to sell in three years may care more about upfront costs and break-even timing.

Define your real payment comfort zone

Many borrowers begin with the maximum amount they can qualify for. That is understandable, but it is not the same as the amount they will feel comfortable paying every month.

Your real housing payment may include more than principal and interest. Depending on the home and loan structure, it can include property taxes, homeowners insurance, mortgage insurance, HOA dues, flood insurance, and other recurring housing costs. A payment that looks manageable before these items are included can feel very different once the full picture is clear.

A strong loan search starts with three numbers:

- Your ideal monthly payment

- Your maximum comfortable monthly payment

- The amount of cash you want to keep after closing

Keeping cash reserves is especially important. A loan that uses nearly all available savings may create stress after move-in, even if the interest rate looks attractive. For a deeper look at building a realistic homebuying budget, New Era Lending’s guide on how to find a mortgage that fits your budget is a useful next step.

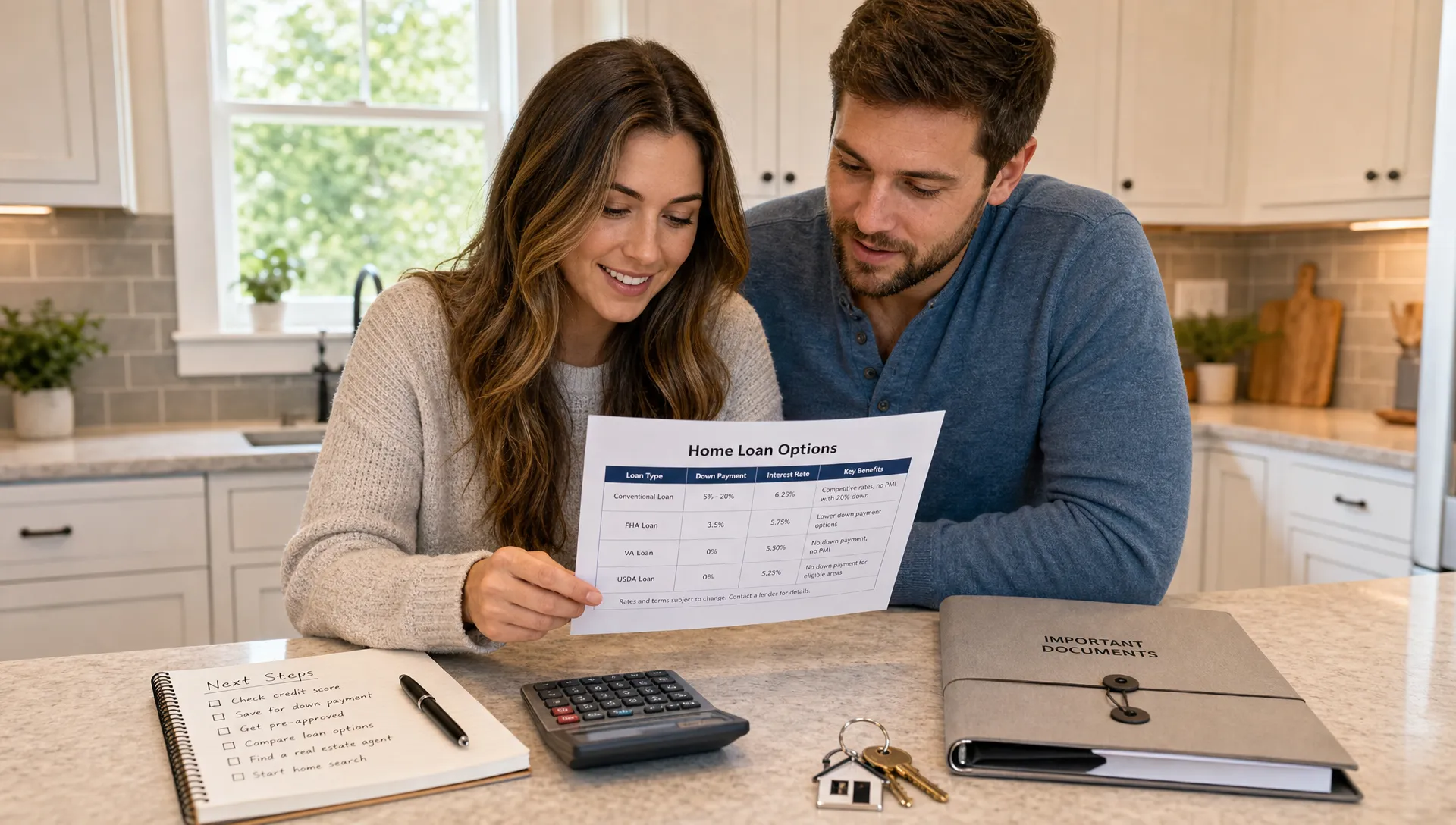

Match the loan type to your borrower profile

Loan programs are tools. The right tool depends on your financial profile, property type, location, and goals.

A conventional loan may be a strong fit for borrowers with solid credit, stable income, and enough down payment to meet program requirements. FHA loans may be useful for buyers who need more flexible credit or down payment guidelines. VA loans can offer major advantages for eligible veterans, service members, and qualifying spouses. USDA loans may help eligible borrowers in qualifying rural or suburban areas. Jumbo loans are designed for loan amounts above conforming loan limits. Non-QM or portfolio options may serve borrowers with more complex income or documentation needs.

The point is not to memorize every guideline. The point is to avoid assuming that the most familiar loan is automatically the best one. A borrower with excellent credit and strong savings may compare options differently than a first-time buyer with limited cash to close. A self-employed borrower may need a different documentation path than a W-2 employee.

If you want a broader overview of common programs, this simple guide to mortgage loan options explains the main categories and when each may make sense.

Compare total cost, not just the interest rate

The interest rate matters, but it is not the whole loan. A lower rate can come with higher upfront costs. A higher rate can sometimes come with lender credits that reduce cash due at closing. Points, credits, fees, mortgage insurance, taxes, and escrow setup can all change the true cost of the loan.

The most reliable way to compare offers is to review the Loan Estimate, a standardized form lenders provide after you apply. The Consumer Financial Protection Bureau’s Loan Estimate explainer breaks down the major sections and helps borrowers understand what they are seeing.

When comparing loans, focus on the same scenario. That means the same loan amount, loan term, down payment, lock period, property type, and credit assumptions. If one quote assumes points and another does not, they are not equal comparisons. If one quote includes estimated taxes and insurance and another excludes them, the monthly payment comparison can be misleading.

APR can help show the cost of credit over time, but it should not be used alone. Cash to close, monthly payment, break-even point, and how long you expect to keep the loan all matter.

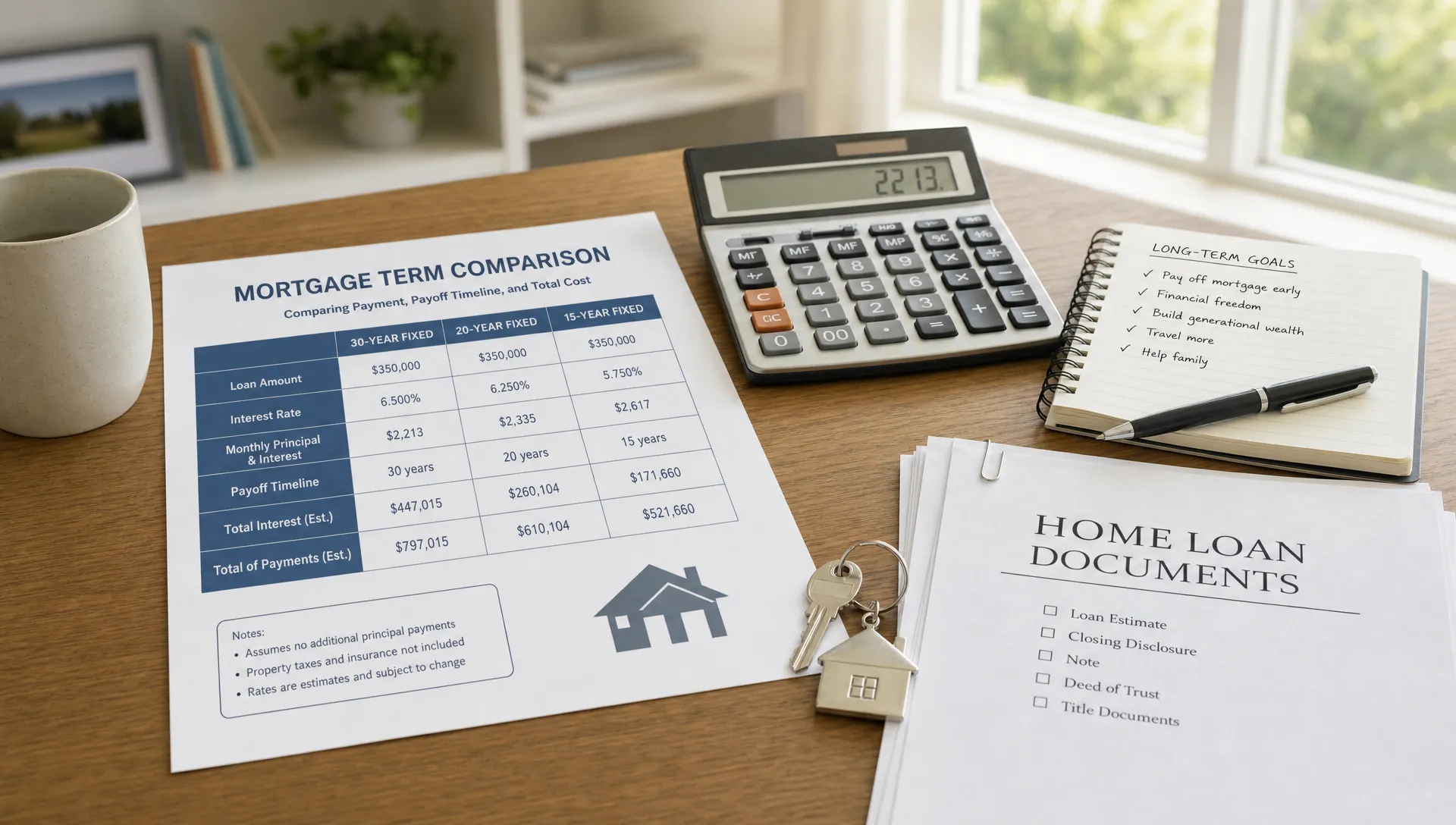

Look at the tradeoffs behind each loan option

Every mortgage decision includes tradeoffs. The right loan is rarely the one that wins every category. It is the one that balances the categories that matter most to you.

For example, paying discount points may lower your rate and monthly payment, but it increases your upfront cost. That can make sense if you plan to keep the loan long enough to recover the cost through monthly savings. It may make less sense if you expect to move, refinance, or pay off the loan soon.

A smaller down payment may help you buy sooner and keep more savings available, but it can increase your monthly payment or require mortgage insurance. A larger down payment may lower the payment, but it can reduce liquidity. A shorter loan term may save interest over time, but the monthly payment will usually be higher. A longer term can improve monthly affordability, but total interest paid over the life of the loan may increase.

This is where guesswork often enters the process. Borrowers compare one visible benefit, like a low rate, while missing the hidden compromise. A good loan comparison makes the tradeoff visible before you commit.

Use a simple decision framework

If you are trying to find the right loan, use the same set of questions for every option. This keeps the decision objective and makes lender conversations more productive.

Ask yourself:

- Does this loan keep the full monthly housing payment within my comfort zone?

- Does it preserve enough cash after closing for emergencies and move-in costs?

- Does it fit how long I realistically expect to keep the home or loan?

- Are the rate, fees, points, credits, and cash to close clear enough to compare?

- Does the loan program match my credit, income, down payment, property, and timeline?

The answer does not need to be perfect in every category. It does need to be clear. If you cannot explain why one option is better than another, you probably need more information before choosing.

Get pre-approved with real documentation

Online calculators are helpful for early planning, but they cannot replace a real review of your income, assets, credit, debts, and property goals. Pre-approval can help turn rough estimates into a more reliable borrowing range.

A stronger pre-approval usually involves documentation, not just a quick estimate. Lenders may review pay stubs, W-2s, tax returns, bank statements, identification, credit history, and other items depending on your situation. For self-employed borrowers, investors, veterans, or borrowers with complex income, documentation can be especially important.

This step reduces surprises. It can also help you identify issues early, such as credit report errors, debt-to-income concerns, reserve requirements, or documentation gaps. Fixing those before you are under contract can make the process smoother.

New Era Lending combines smart mortgage technology with personalized human guidance, including secure document uploads and e-signature support, so borrowers can move through the process with more clarity and less friction.

Know the warning signs of a poor fit

A loan may be wrong for you even if it is technically available. Watch for signs that an option does not match your goals or comfort level.

Common red flags include:

- The payment only works if everything else in your budget goes perfectly

- You do not understand why the rate is lower than another offer

- The cash to close is higher than expected and not clearly explained

- You are being rushed without enough time to review the Loan Estimate

- The loan structure depends on assumptions that may not happen, such as a future refinance

- The lender cannot clearly explain fees, points, credits, mortgage insurance, or escrow items

A good loan should be understandable. Mortgage details can be complex, but your lender should be able to explain the reason behind each major cost and term in plain language.

Ask better questions before you choose

The quality of your loan decision often depends on the quality of your questions. Instead of asking only, “What is your rate?” ask questions that reveal the full cost and fit.

Useful questions include:

- What assumptions are used for this rate quote?

- Are there discount points or lender credits?

- What is the estimated cash to close?

- How long is the rate lock?

- What could cause the payment or closing costs to change?

- How does this option compare with another program I may qualify for?

- What documents should I prepare now to avoid delays?

These questions can quickly separate a surface-level quote from a meaningful loan comparison. If you are evaluating lenders as well as loan options, this article on questions to ask a home loan mortgage lender can help you prepare.

Do not choose a loan in isolation

Your mortgage is one part of your larger financial life. The right loan should support your broader goals, not compete with them.

Think about how the loan affects your emergency fund, retirement contributions, education savings, debt payoff plan, and ability to handle repairs. A home can build long-term stability, but only if the financing remains manageable after closing.

Also consider how life could change. Will your income fluctuate? Are you planning to grow your family? Could you relocate for work? Do you expect major repairs or renovations? The more realistic your assumptions, the less likely you are to choose a loan that only works on paper.

Frequently Asked Questions

What is the best way to find the right loan? Start by defining your goal, budget, cash to close, timeline, and risk tolerance. Then compare loan options using the same assumptions, including rate, APR, fees, points, credits, monthly payment, and total cash required.

Should I choose the loan with the lowest interest rate? Not always. A lower rate may come with higher upfront costs or points. The better choice depends on how long you expect to keep the loan, your cash reserves, and the total cost compared with other options.

How early should I start comparing mortgage options? Ideally, start before you make an offer or begin a refinance application. Early comparison gives you time to review your credit, gather documents, understand your budget, and choose a loan strategy without pressure.

Can I compare loans before I know the exact property? Yes. You can compare estimated scenarios based on target price, down payment, location, credit profile, and loan amount. Final numbers may change once the property, taxes, insurance, and underwriting details are known.

What makes a loan the “right” loan? The right loan is the one that fits your full financial picture. It should be affordable, clearly explained, aligned with your goals, and structured around realistic assumptions.

Find your loan with more clarity

You do not have to choose a mortgage by guessing. When you compare options through the lens of payment, cash to close, program fit, total cost, and long-term goals, the right path becomes easier to see.

New Era Lending helps borrowers explore purchase, refinance, and equity access options with modern tools and expert guidance. If you want a clearer way to evaluate your next mortgage decision, start with New Era Lending and move forward with a loan strategy built around your needs.