.jpg)

.jpg)

.jpg)

Refinance Lending: How to Compare Lenders and Terms

Refinancing can be a smart move, but the best offer is rarely the one with the lowest number in a headline ad. In refinance lending, your true cost depends on the lender, the loan structure, the term, the fees, the rate lock, and how long you plan to keep the new loan.

That is why comparing refinance offers takes more than checking today’s rate online. You need a consistent way to evaluate lenders and terms side by side, so you can see which option actually supports your goal, whether that goal is lowering your payment, shortening your payoff timeline, removing mortgage insurance, switching loan types, or accessing equity.

Below is a practical framework for comparing refinance lenders and loan terms with more confidence.

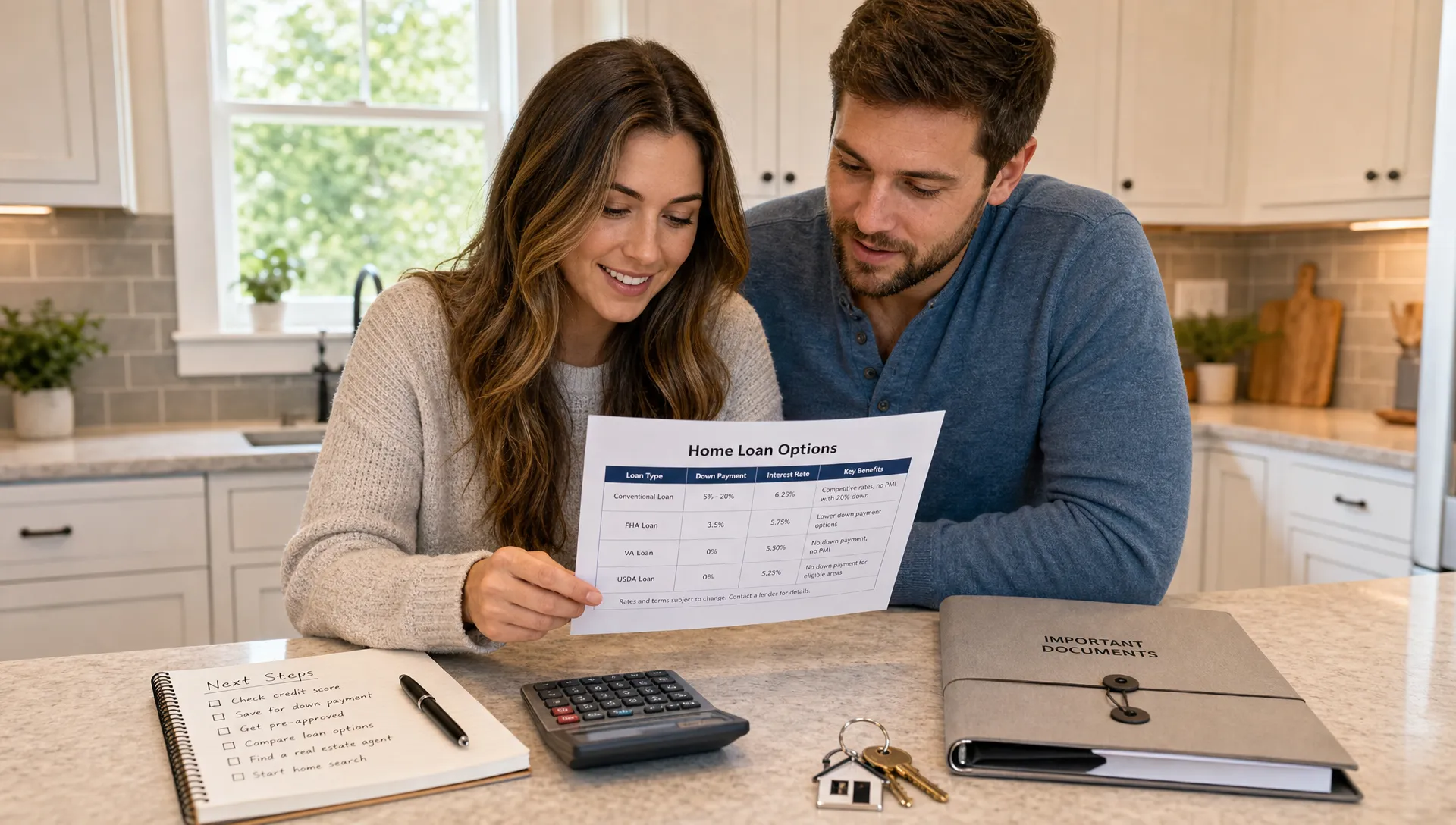

Start With the Reason You Want to Refinance

Before you compare lenders, define what a successful refinance looks like. A lender can only structure the right scenario if your goal is clear.

Common refinance goals include:

- Lowering the monthly payment

- Reducing the interest rate

- Shortening the loan term

- Moving from an adjustable-rate mortgage to a fixed-rate loan

- Removing mortgage insurance

- Accessing home equity through a cash-out refinance

- Consolidating higher-interest debt with a clear repayment plan

- Changing loan programs, such as FHA to conventional or conventional to VA if eligible

The right refinance lending option changes depending on your goal. For example, a 30-year refinance may lower your payment, but it can extend your payoff timeline. A 15-year refinance may save interest over time, but it can raise the monthly payment. A cash-out refinance may provide useful funds, but it increases the loan balance and should be weighed carefully.

If you are still deciding whether refinancing makes sense, it helps to review the broader signs that it may be time to refinance your home before you start collecting quotes.

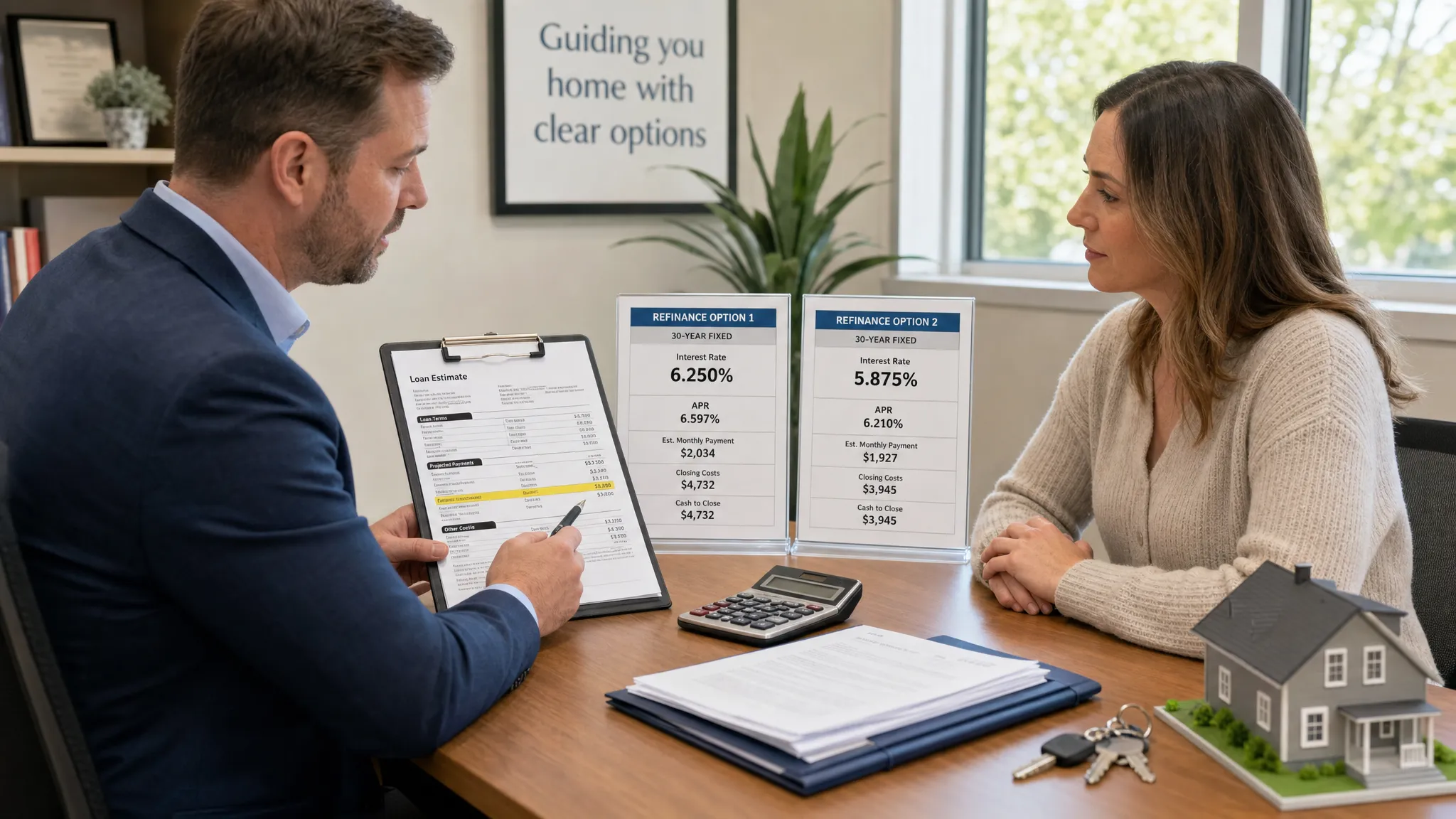

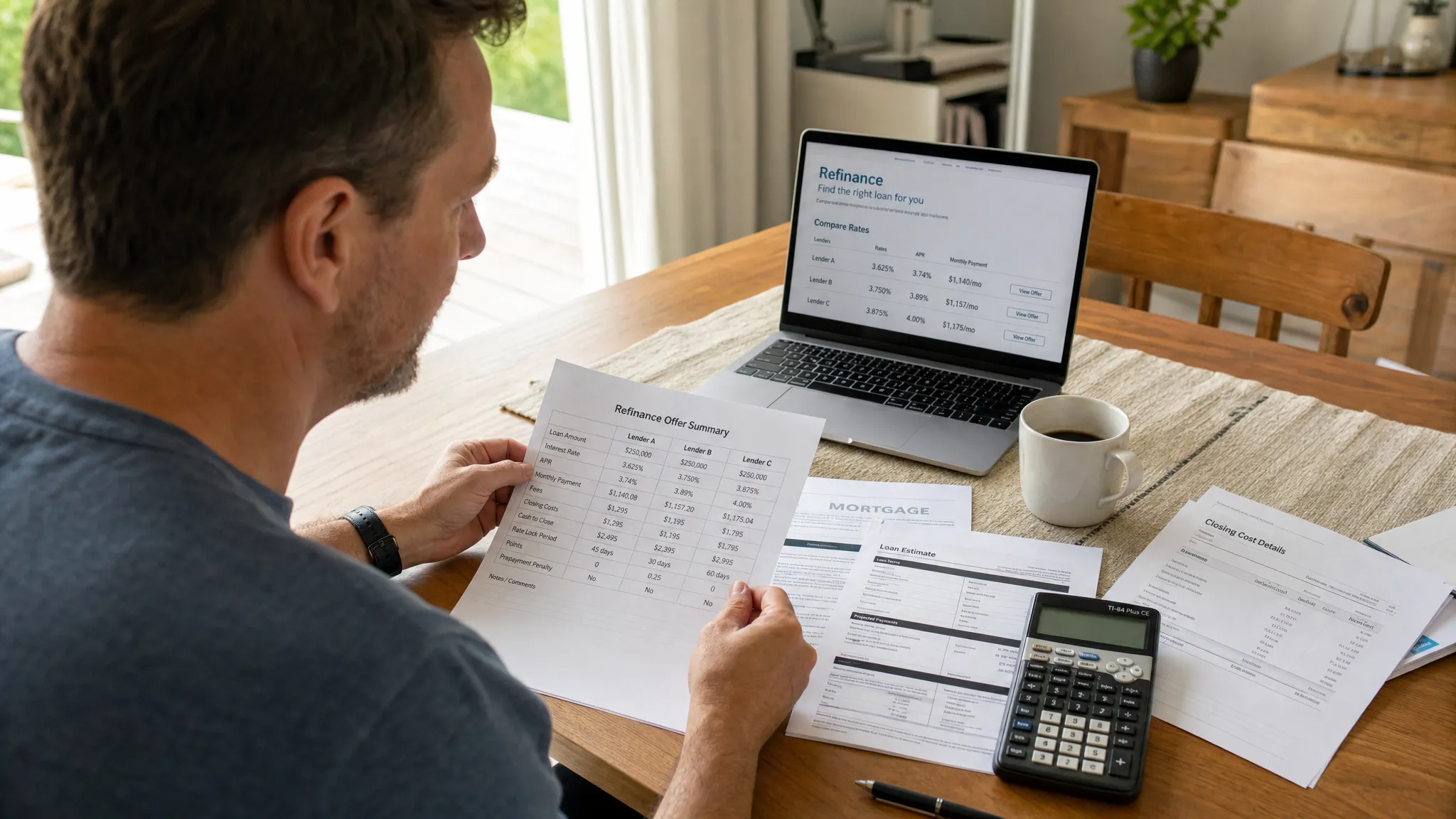

Compare Lenders Using the Same Loan Scenario

One of the biggest mistakes homeowners make is comparing quotes that are based on different assumptions. A lender quoting a 30-year fixed loan with points is not giving you the same offer as a lender quoting a 30-year fixed loan with lender credits. A quote with a 15-day lock is not the same as one with a 45-day lock.

To make the comparison fair, give each lender the same information and request the same scenario. Be ready to share your estimated home value, current loan balance, desired loan amount, property type, occupancy, credit profile, income type, target loan term, and whether you want cash out.

You should also ask each lender to quote the same lock period and to clearly state whether the offer includes discount points, lender credits, or both. Even small differences in these assumptions can change the rate, APR, closing costs, and monthly payment.

Use the Loan Estimate as Your Main Comparison Tool

A verbal quote is useful for an initial conversation, but the Loan Estimate is where the real comparison begins. The Consumer Financial Protection Bureau explains that the Loan Estimate is designed to help borrowers understand key loan terms, projected payments, closing costs, and other important details.

When comparing Loan Estimates, focus on the full picture, not just the interest rate. Review these sections carefully:

- Loan terms: Check the loan amount, interest rate, monthly principal and interest, and whether the loan has a prepayment penalty or balloon payment.

- Projected payments: Look at the full estimated payment, including taxes, insurance, and mortgage insurance if applicable.

- Costs at closing: Compare closing costs, cash to close, lender fees, third-party fees, and prepaid items.

- APR: Use APR as a helpful cost comparison, but remember that it may not capture your personal timeline perfectly.

- Services you can shop for: Some third-party costs may vary, and shopping can sometimes reduce your total closing costs.

The Loan Estimate helps prevent apples-to-oranges comparisons. If two lenders quote similar rates but one has much higher origination fees or points, the cheaper-looking rate may not be the better deal.

For a deeper look at rate comparison, see this guide on how to compare home refinance rates the right way.

Understand the Terms That Change Your True Cost

Refinance terms can affect your finances for years. Before choosing a lender, make sure you understand how each major term works.

Interest Rate

The interest rate determines the cost of borrowing before certain fees and other charges. A lower rate can reduce your payment, but it may come with higher upfront costs if you are paying discount points.

APR

APR reflects the interest rate plus certain loan costs, expressed as an annual percentage. It is helpful when comparing similar loan types with similar terms. However, APR can be less useful if you are comparing a short-term ownership plan against a long-term one, because upfront costs are spread over the life of the loan.

Loan Term

The term is the length of time used to repay the loan, often 15, 20, or 30 years. A shorter term usually means a higher payment but lower total interest if you keep the loan. A longer term can improve monthly cash flow but may increase long-term interest, especially if you restart the clock after already paying down your current mortgage for several years.

Discount Points and Lender Credits

Discount points are upfront fees paid to lower the rate. Lender credits work the opposite way, giving you help with closing costs in exchange for a higher rate. Neither is automatically good or bad. The right choice depends on cash flow, savings, and how long you expect to keep the loan.

Closing Costs

Closing costs may include lender fees, title fees, recording fees, appraisal costs, credit report fees, prepaid interest, escrow deposits, and other transaction costs. Some costs are negotiable or shop-able, while others are set by third parties or local requirements.

Rate Lock

A rate lock protects your quoted rate for a specific period. Compare the lock length, extension cost, and whether the lender offers any float-down option. A low quote with an unrealistic lock period may create problems if the loan takes longer to close.

Escrow Setup

If your new loan includes an escrow account for property taxes and homeowners insurance, your cash to close and monthly payment may change. Make sure you understand whether the quote includes escrow deposits and how those deposits compare across offers.

Run the Break-Even Math

Break-even is one of the simplest ways to test whether a refinance is worth the cost. The basic formula is:

Total refinance costs divided by monthly savings equals months to break even.

For example, if your refinance costs $4,000 and saves you $200 per month, the break-even period is 20 months. If you expect to stay in the home and keep the loan longer than that, the refinance may be worth considering. If you may sell or refinance again before then, the savings may not justify the cost.

Break-even is not the only factor, though. It does not fully capture cash-out goals, term changes, mortgage insurance removal, tax considerations, or long-term interest savings. A refinance that raises your payment may still make sense if it shortens your term and saves substantial interest. A refinance that lowers your payment may be less attractive if it extends your debt far longer than you want.

If your primary goal is changing payment or term, compare your options with this guide to mortgage loan refinance choices.

Compare the Lender, Not Just the Loan

The lender matters as much as the quote. A refinance often involves deadlines, documentation, appraisal requirements, title work, underwriting questions, and rate lock timing. A low-cost offer can become frustrating or expensive if the process is unclear or delayed.

When comparing refinance lenders, consider:

- How clearly they explain rates, APR, points, credits, and fees

- Whether they provide a written Loan Estimate promptly when appropriate

- How familiar they are with your refinance type, such as VA, FHA, conventional, jumbo, cash-out, or self-employed income scenarios

- How they handle secure document uploads and e-signatures

- How responsive they are when you ask detailed questions

- Whether they explain rate lock risks and timeline expectations upfront

- Whether they help you compare multiple structures instead of pushing one option

Modern refinance lending is increasingly digital, but technology should support clarity rather than replace guidance. Secure uploads, e-signatures, and streamlined workflows can make the process faster and easier, especially when paired with experienced human support. The same principle applies across technical industries: reliable systems matter behind the scenes, whether in mortgage platforms or specialized engineering fields where power electronics and embedded system specialists build the infrastructure that helps complex products work reliably.

In other words, do not choose a refinance lender only because the online experience looks convenient. Choose one that combines digital efficiency with accurate explanations, realistic timelines, and transparent terms.

Watch for Red Flags When Shopping Refinance Offers

Most lenders want to help borrowers make informed decisions, but you should still know what warning signs look like.

Be cautious if a lender advertises a very low rate without showing assumptions, avoids discussing APR, will not explain points or credits, pressures you to lock before reviewing costs, or discourages you from comparing Loan Estimates. You should also be careful if the numbers change repeatedly without a clear reason.

Another red flag is a quote that ignores your actual goal. If you want to lower your monthly payment, the lender should show the full payment impact, including taxes, insurance, and mortgage insurance. If you want to shorten your term, the lender should compare total interest and monthly affordability. If you want cash out, the lender should help you understand new loan balance, equity position, and repayment risk.

A good lender should be willing to slow down and explain the tradeoffs.

Ask These Questions Before Choosing a Refinance Lender

Once you have narrowed your options, ask direct questions before making a decision:

- What assumptions are used in this quote? Confirm loan amount, home value, credit score range, term, property type, occupancy, lock period, points, and credits.

- What is the total monthly payment? Ask for principal, interest, taxes, insurance, mortgage insurance, and HOA dues if applicable.

- What are my total closing costs and cash to close? Make sure you understand the difference between lender fees, third-party fees, prepaids, and escrow deposits.

- How long is the rate locked? Ask what happens if closing is delayed and whether extension fees apply.

- What is my break-even point? Ask the lender to walk through the math using your actual costs and payment savings.

- How does this refinance affect my long-term interest? This is especially important if you are restarting a 30-year term.

- What could change before closing? Ask about appraisal results, income verification, title issues, insurance updates, and escrow adjustments.

- What documents should I prepare now? A complete file can reduce delays and improve your ability to lock confidently.

These questions help you compare lenders based on transparency and fit, not just pricing.

A Simple Workflow for Comparing Refinance Lending Offers

A structured process can make refinance shopping much less overwhelming.

First, define your goal and decide what matters most: lower payment, shorter term, equity access, payment stability, or reduced long-term cost. Second, request quotes from multiple lenders using the same loan scenario. Third, compare written Loan Estimates side by side. Fourth, calculate break-even and total interest impact. Fifth, evaluate the lender’s process, communication, timeline, and rate lock policy. Finally, choose the offer that best matches your financial goal and comfort level.

This approach helps you avoid chasing a headline rate that does not actually serve your needs.

How New Era Lending Helps Homeowners Compare Refinance Options

New Era Lending combines smart mortgage technology with personalized human guidance to make refinance decisions clearer. Homeowners can compare loan options, review rates and terms, use secure document uploads, and move through the process with support from experienced mortgage professionals.

Because refinance decisions are personal, the right answer depends on your loan balance, equity, credit profile, income, timeline, and long-term plans. A side-by-side scenario review can help you see whether refinancing truly improves your situation, or whether waiting makes more sense.

Frequently Asked Questions

How many refinance lenders should I compare? Comparing at least a few lenders can help you understand the range of rates, fees, and terms available for your scenario. Make sure every quote uses the same assumptions so the comparison is fair.

Is the lowest refinance rate always the best choice? Not always. A lower rate may require higher upfront costs, discount points, or a longer break-even period. Compare APR, closing costs, cash to close, loan term, and how long you expect to keep the loan.

What is the most important document when comparing refinance offers? The Loan Estimate is the key document. It shows the loan terms, projected payments, closing costs, APR, and cash to close in a standardized format.

Should I pay points on a refinance? Paying points can make sense if the monthly savings justify the upfront cost and you plan to keep the loan long enough to pass the break-even point. If you may sell or refinance again soon, points may not be worth it.

Can I compare lenders without hurting my credit too much? Credit scoring models often treat multiple mortgage inquiries within a limited shopping window as one inquiry, but rules can vary by model. It is still smart to shop within a focused period and ask lenders what type of credit pull they use.

Ready to Compare Refinance Lending Options?

The right refinance is not just about finding a lower rate. It is about choosing the lender, term, cost structure, and timeline that support your financial goals.

If you want a clearer side-by-side review, New Era Lending can help you compare refinance scenarios with modern tools, transparent guidance, and a process designed to simplify the decision. Reach out to explore your options before you lock in your next loan.