.jpg)

.jpg)

.jpg)

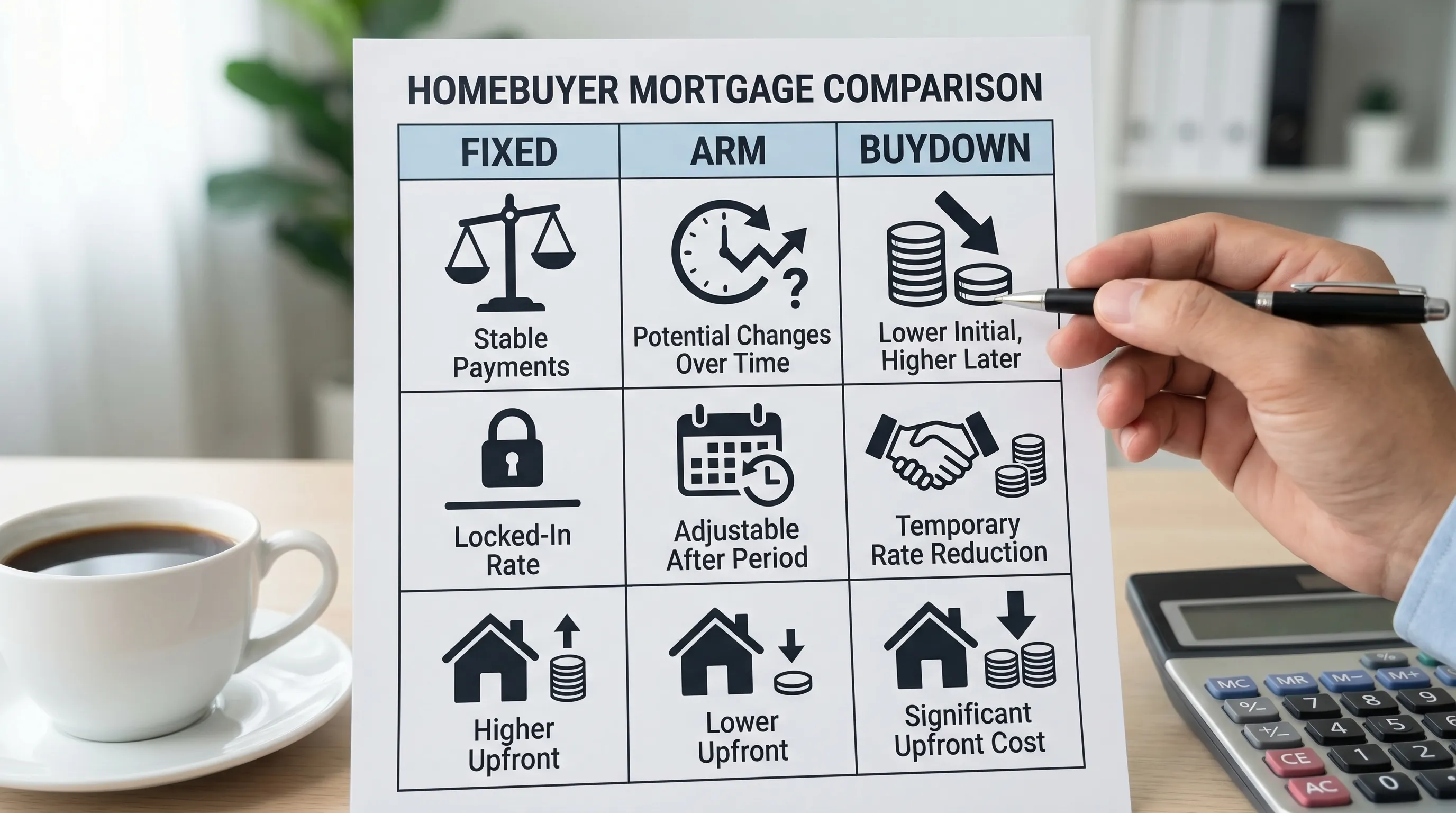

Mortgage Options Compared: Fixed vs ARM vs Buydowns

If you are shopping for a home or refinance in 2026, you are probably seeing three “paths” show up again and again in lender quotes: a traditional fixed-rate loan, an adjustable-rate mortgage (ARM), or a deal that includes a buydown (temporary or permanent). They can all be good mortgage options, but they solve different problems.

This guide compares fixed vs ARM vs buydowns in plain English, with the key math, the real risks to watch for, and a simple framework to help you choose.

The 30-second definitions (so you can compare apples to apples)

- Fixed-rate mortgage: Your interest rate (and principal and interest payment) stays the same for the entire term.

- ARM (adjustable-rate mortgage): Your rate is fixed for an introductory period (often 5, 7, or 10 years), then it can adjust on a schedule.

- Buydown: Someone pays extra upfront to reduce the rate. A temporary buydown lowers the rate for the first 1 to 3 years, while a permanent buydown (points) lowers it for the full term.

Option 1: Fixed-rate mortgages (predictability as the main benefit)

A fixed-rate mortgage is the “what you see is what you get” option. Your principal and interest payment is stable for the entire loan term, which is why many buyers default to it when budgets feel tight.

When a fixed-rate mortgage tends to fit best

A fixed rate is often the strongest choice if:

- You expect to keep the home a long time.

- You want payment stability (especially if your income is steady but not rapidly rising).

- You do not want to rely on a refinance later.

- You would lose sleep if your payment could jump.

Tradeoffs to understand

- Higher starting rate (often): You may pay a premium for certainty compared to an ARM’s introductory rate.

- Opportunity cost: If rates fall later, you only benefit if you refinance (and refinancing has costs).

Fixed-rate “gotchas” that surprise borrowers

- Your total payment still changes if taxes and insurance rise. Even with a fixed rate, escrow changes can raise the monthly bill.

- APR matters if you are paying points or lender fees. Two “same-rate” quotes can have different APRs because costs differ.

Option 2: ARMs (lower upfront payment, with rules you must verify)

An ARM is not automatically “risky,” but it is more complex. You must understand the adjustment mechanics and your worst-case payment.

The CFPB’s Consumer Handbook on Adjustable-Rate Mortgages is one of the best plain-language resources for learning how ARMs work.

How an ARM is structured

Most ARMs are described with two numbers, like 5/6 ARM or 7/1 ARM:

- The first number is the initial fixed period (5 years, 7 years, 10 years, etc.).

- The second number is how often it adjusts after that (every 6 months, every year).

Your new rate after the fixed period is typically based on:

- Index (a market rate the loan follows)

- Margin (a fixed number added by the lender)

Your loan also includes rate caps that limit how much the rate can rise:

- Initial adjustment cap: Max increase at the first adjustment.

- Periodic cap: Max change each adjustment period.

- Lifetime cap: Max increase over the life of the loan.

When an ARM can be a smart move

An ARM can make sense if:

- You are confident you will sell or refinance before the first adjustment (with a realistic backup plan).

- You are buying more home than a fixed-rate payment allows, but you have strong future income growth and reserves.

- You want lower initial payments to free up cash for renovations or debt payoff.

The real ARM risk (it is not the label, it is the payment shock)

The main risk is payment shock when the rate adjusts. Before you choose an ARM, you should be able to answer:

- What is my payment at today’s rate?

- What is my payment at the fully indexed rate (index + margin) if it were calculated today?

- What is my payment at the lifetime cap (worst case)?

- Could my budget handle that payment if I had to keep the loan?

If you cannot comfortably handle the worst-case payment, the ARM is a bet you may not want to make.

Option 3: Buydowns (lower rate, but you need to know who pays and what you give up)

A buydown reduces your interest rate by paying extra costs upfront. There are two broad types.

Temporary buydown (common examples: 2-1 and 1-0)

A temporary buydown reduces the rate for a limited time, then returns to the “note rate” for the remainder of the loan.

- A 2-1 buydown lowers the rate by 2% in year one, 1% in year two, then returns to the note rate in year three.

- A 1-0 buydown lowers the rate by 1% for the first year only.

These are often funded by:

- Seller concessions (the seller pays closing costs and funds the buydown)

- Builder incentives in new construction

- Lender credits (sometimes paired with a slightly higher note rate)

Key point: a temporary buydown is usually about early-payment relief, not long-term interest savings.

Permanent buydown (discount points)

A permanent buydown means paying discount points to lower the rate for the entire term. This is more straightforward: you pay more upfront, you get a lower rate, and you keep it as long as you keep the loan.

When a buydown tends to make sense

A buydown can be a good fit if:

- You expect to keep the loan long enough to break even on the upfront cost (especially for permanent points).

- You are qualifying close to your maximum payment and a lower rate meaningfully helps approval.

- You negotiated seller concessions and would rather apply them to interest savings than other closing costs.

The most common buydown mistakes

- Assuming you will refinance before the buydown ends. If refinancing does not happen, the payment step-up can still hurt.

- Comparing only the first-year payment. Temporary buydowns can look amazing in year one, but you must compare year three onward.

- Ignoring the opportunity cost. Money used for points might be more valuable as reserves, repairs, or paying down higher-interest debt.

Fixed vs ARM vs Buydowns: a decision framework that works in real life

Instead of asking “Which is cheapest today?” ask the five questions below. This gets you to the right mortgage option faster.

1) How long will you keep the home (and how sure are you)?

- 7+ years and you are confident: fixed-rate often wins on simplicity, and permanent points may pencil if you stay long enough.

- 3 to 7 years: an ARM or a temporary buydown can be worth modeling.

- Under 3 years: focus on total cost over your likely timeline, not a 30-year snapshot.

2) Is your budget sensitive to a future payment increase?

If a higher payment would force lifestyle cuts or put you at risk of missing payments, lean toward:

- Fixed-rate, or

- A buydown that lowers payment without introducing future uncertainty (permanent points, not an ARM).

If you can tolerate variability and have strong reserves, an ARM may be reasonable.

3) Do you need lower payment now, or lower cost over time?

- Need lower payment now (cash flow): temporary buydown or ARM can help, but verify the step-up plan.

- Need lower total interest over time: fixed rate with permanent points might be better than a temporary buydown.

4) Who is funding the “deal sweetener”?

This question is huge. The best buydown is often one funded by negotiated credits (seller or builder), not one that drains your cash reserves.

If you are choosing between:

- Paying points out of pocket, or

- Keeping cash for emergencies,

remember that homeownership includes non-mortgage expenses. A single repair can change your comfort level quickly. Even something as basic as a sewer backup or a failed water heater can be expensive, so it is wise to keep a realistic maintenance buffer and know who you would call for urgent issues (for example, licensed plumbing and drain cleaning services if you own a home in the Kingston, Ontario area).

5) Are you trying to “time” a refinance?

Plenty of borrowers plan to refinance, but the plan needs guardrails:

- What if rates are flat for 3 to 5 years?

- What if home values dip and refinancing is harder?

- What if your income changes?

If the loan only works if refinancing happens, it is not a plan, it is a gamble.

How to compare quotes properly (the checklist most people skip)

Whether you are comparing a fixed rate, an ARM, or a buydown, ask your lender for side-by-side scenarios and verify these items in the Loan Estimate.

For any mortgage option

- Interest rate vs APR: APR helps you see how fees and points change the true cost.

- Cash to close: verify what is actually due at closing after credits.

- Monthly payment breakdown: principal and interest vs taxes, insurance, HOA, mortgage insurance.

The CFPB’s Loan Estimate explainer is a helpful reference when you are reviewing fees.

Extra checks for ARMs

- What are the index and margin?

- What are the initial, periodic, and lifetime caps?

- What is the lender’s estimate of the highest possible payment and where is it documented?

Extra checks for buydowns

- Is it a temporary or permanent buydown?

- What is the payment schedule by year?

- Who funds it (seller, builder, lender credit, you)?

- If it is temporary, what happens to your payment when it resets (and can your budget handle it)?

Real-world scenarios (who usually chooses what)

Scenario A: First-time buyer prioritizing stability

If you want the simplest path and plan to stay put, a fixed-rate mortgage is often the best “set it and forget it” structure. If the payment is slightly too high, you might explore a seller-funded temporary buydown, but only if you are confident year-three payment is affordable.

Scenario B: High-income-growth household with a shorter timeline

If you expect to move within 5 to 7 years (job relocation, growing family) and you want a lower initial payment, an ARM might be worth considering. The key is to underwrite yourself conservatively: make sure you can handle the payment at the fully indexed rate or lifetime cap if plans change.

Scenario C: Buyer negotiating strong seller concessions

When you have meaningful seller credits, you can often choose between:

- Applying credits to reduce cash to close, or

- Funding a temporary buydown for payment relief, or

- Paying discount points for a permanent lower rate (if allowed and if you plan to keep the loan long enough).

The “best” choice depends on your time horizon and how tight your monthly budget is.

Scenario D: Refinance borrower deciding between fixed vs ARM

If your goal is long-term certainty, fixed is usually the cleanest refinance structure. If you are refinancing mainly to bridge a near-term period (for example, expecting to sell), an ARM could reduce the payment now, but you should still stress-test the future adjustments.

Where New Era Lending fits in

Most borrowers do not need more options, they need fewer, clearer choices backed by real numbers.

New Era Lending’s approach is built around comparing scenarios with modern tools (secure document uploads, e-signatures, transparent comparisons) plus human guidance to help you choose a structure you can live with. If you are deciding between a fixed rate, an ARM, or a buydown, ask for a side-by-side review using the same loan amount, same closing date assumptions, and a clear breakdown of cash-to-close and payment changes over time.

Frequently Asked Questions

Is a fixed-rate mortgage always safer than an ARM? A fixed rate is usually safer for budgeting because principal and interest do not change. An ARM can still be a responsible choice if you understand the caps, have reserves, and can afford the payment if rates rise.

What is the main risk of an ARM? Payment shock after the introductory fixed period ends. You should evaluate your payment at the fully indexed rate and at the lifetime cap before choosing an ARM.

Are temporary buydowns worth it? They can be, especially when funded by seller or builder credits and when the year-three payment fits your budget. They are less attractive when you pay for them out of pocket and do not keep enough cash reserves.

Is a permanent buydown (points) better than a temporary buydown? Not always. Permanent points can save more over time, but only if you keep the loan long enough to break even. Temporary buydowns mainly help early payments and can be useful for short-term cash flow.

Should I choose based on the lowest rate advertised? Not by itself. Compare cash to close, APR, and the full payment timeline. The lowest rate sometimes comes with higher fees or points.

How do I compare mortgage options quickly without getting overwhelmed? Start with your time horizon, your maximum comfortable payment (including worst-case ARM adjustments), and your available cash. Then ask for side-by-side Loan Estimates showing fixed vs ARM vs buydown using the same assumptions.

Get a side-by-side comparison that matches your budget

If you are ready to choose between a fixed rate, an ARM, and a buydown, the fastest way to get clarity is to run real scenarios (not generic averages) based on your purchase price, down payment, credit profile, and timeline.

Explore your options with New Era Lending at neweralendingllc.com and request a personalized comparison so you can lock the structure that fits your payment comfort zone, not just today’s headline rate.