.jpg)

.jpg)

.jpg)

How to Buy a First Home Without Costly Mistakes

Buying your first home is exciting, but it can also feel like a high-stakes test where every choice affects your savings, monthly budget, and future flexibility. The goal is not just to buy a first home. The goal is to buy the right home, with the right loan, on terms you understand before you sign.

Costly mistakes usually do not come from one bad decision. They come from small gaps: shopping before pre-approval, underestimating cash to close, focusing only on the interest rate, skipping inspections, or stretching the payment too far. A smarter approach is to slow down at the right moments, ask better questions, and make each decision with the full cost in view.

Start With the Payment, Not the Purchase Price

A home price can look affordable online while the actual monthly payment tells a different story. Your real payment may include principal, interest, property taxes, homeowners insurance, mortgage insurance, HOA dues, and sometimes flood insurance or special assessments.

Before touring homes, estimate a payment range that feels comfortable in real life. That means looking at your take-home pay, current debts, savings goals, childcare, transportation, retirement contributions, and the amount you want left over each month.

A common first-time buyer mistake is using the maximum pre-approval amount as a shopping budget. Pre-approval tells you what a lender may approve based on qualifying guidelines. It does not always tell you what will feel comfortable after utilities, maintenance, furniture, and life expenses are included.

If you want a clearer breakdown of what goes into the payment, New Era Lending’s guide on how to estimate your monthly mortgage payment is a helpful next step.

Know the Difference Between Down Payment and Cash to Close

Your down payment is only one part of the money you need to buy a home. Cash to close can also include lender fees, title fees, prepaid taxes and insurance, escrow reserves, appraisal fees, recording fees, and other closing costs.

Closing costs commonly range from about 2% to 5% of the loan amount, depending on location, loan type, property taxes, insurance costs, and transaction details. That means a buyer who saved for a down payment may still feel short if they did not plan for the full amount due at closing.

Before making offers, ask your lender for a realistic estimate of total cash to close based on your target price, loan program, and local taxes. Then keep a separate emergency reserve. Draining every dollar to close may make the purchase possible, but it can make the first year of ownership stressful.

A safer plan includes money for:

- Down payment and closing costs

- Moving expenses and utility deposits

- Basic repairs or maintenance after move-in

- A starter emergency fund

- Immediate household needs such as appliances, tools, or safety upgrades

For a deeper look at down payment planning, read Down Payment for Home Loan: How Much You Really Need.

Get Pre-Approved Before You Fall in Love With a Home

A strong pre-approval helps you understand your buying power, identify documentation issues early, and make more credible offers. It also gives your loan officer time to compare loan options before you are under contract and racing against deadlines.

Pre-approval is different from a quick online estimate. A more useful pre-approval typically reviews income, assets, credit, debts, employment, and the likely loan program. If you are self-employed, have variable income, receive bonuses, use gift funds, or recently changed jobs, early review matters even more.

Skipping this step can create expensive surprises. You might discover too late that your debt-to-income ratio is higher than expected, your bank deposits need explanation, your credit score changed, or your preferred loan program has property requirements that affect your offer.

The best time to solve these problems is before you are emotionally attached to a house.

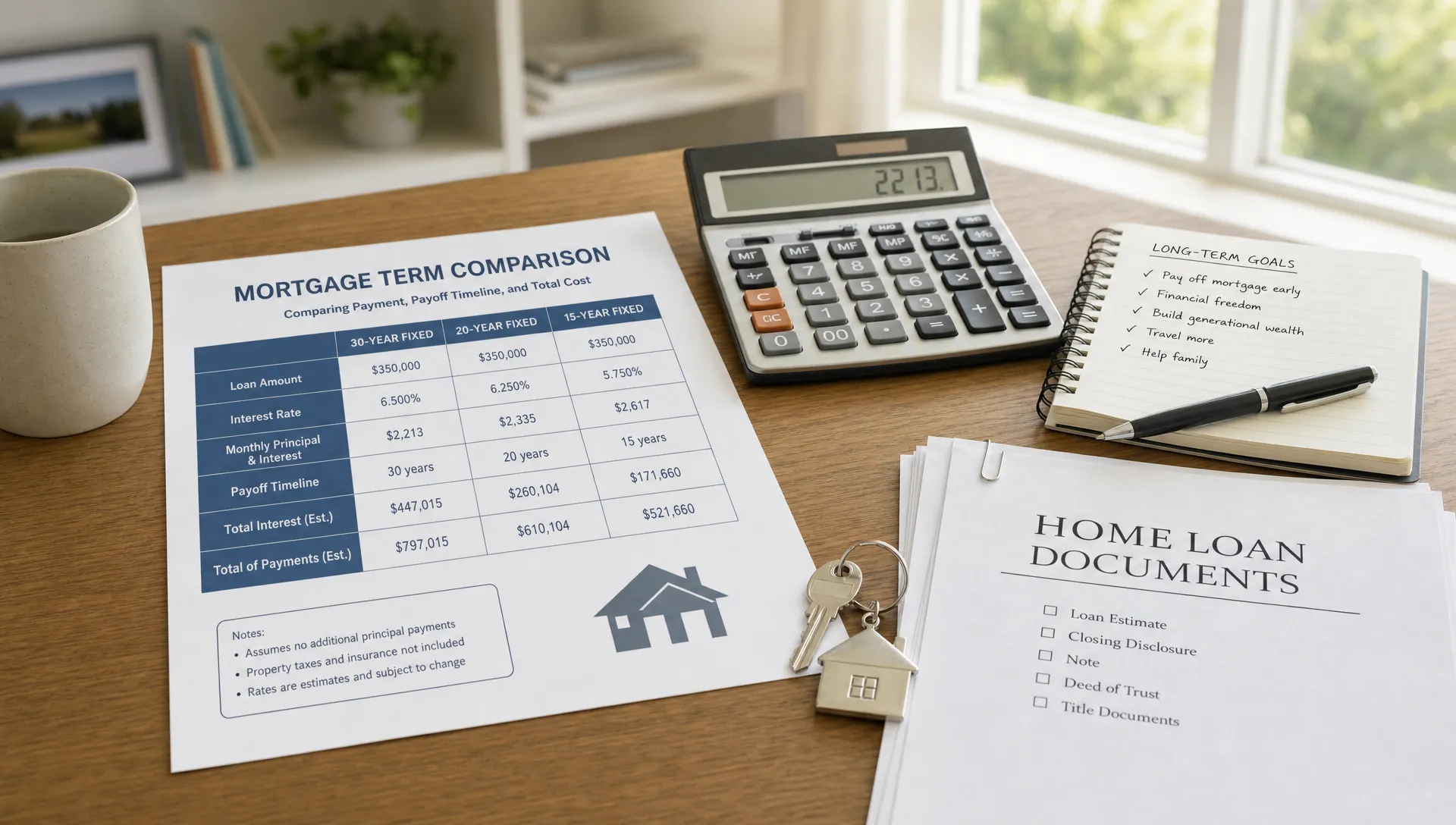

Choose the Loan Program Around Your Real Constraint

There is no single best mortgage for every first-time buyer. The right loan depends on what is limiting you most: cash to close, credit profile, monthly payment, property type, timeline, or long-term cost.

For example, a conventional loan may work well for a buyer with strong credit and enough down payment to manage mortgage insurance costs. FHA may help buyers with lower credit scores or limited savings. VA loans can be powerful for eligible veterans, active-duty service members, and certain surviving spouses. USDA may be an option for qualifying buyers in eligible rural or suburban areas.

A costly mistake is choosing a loan based only on the lowest advertised rate or the lowest down payment. A lower down payment may preserve cash, but it can increase mortgage insurance or monthly payment. A lower rate may require discount points that only pay off if you keep the loan long enough. A loan that looks cheaper upfront may not be the best fit over time.

Ask your lender to compare realistic scenarios side by side. Review cash to close, monthly payment, mortgage insurance, rate, APR, and how long you expect to own the home. You can also explore New Era Lending’s overview of mortgage loan programs to understand common options before you apply.

Do Not Make Big Financial Changes During the Process

Once you begin pre-approval or go under contract, keep your finances steady. Lenders may re-check credit, employment, assets, and debts before closing. A new car loan, large credit card purchase, job change, undocumented deposit, or missed payment can affect approval.

This does not mean you cannot live your life. It means you should check with your loan officer before making financial moves that could change your file.

Avoid these actions unless your lender confirms they are safe:

- Opening or closing credit accounts

- Financing furniture, appliances, or a vehicle

- Moving large sums of money between accounts without documentation

- Making unexplained cash deposits

- Changing jobs, pay structure, or work hours

- Co-signing for someone else’s loan

For small business owners, freelancers, and side-hustle earners, clean records are especially important. Keep business and personal funds organized, document deposits, and use tools that make income easier to track. For example, a service-based business owner who accepts in-person payments may benefit from a simple Tap-to-Phone solution like nashi for contactless card payments so sales activity is easier to document and reconcile.

Compare Loan Estimates, Not Verbal Promises

A quoted interest rate is not enough to compare mortgage offers. You need the full cost picture. The Loan Estimate shows key details such as interest rate, APR, monthly payment, estimated cash to close, loan costs, lender credits, and whether the loan has features like prepayment penalties or balloon payments.

The Consumer Financial Protection Bureau explains the Loan Estimate as a tool borrowers can use to compare offers more clearly. To make that comparison fair, request quotes using the same purchase price, down payment, loan type, lock period, and credit assumptions.

Pay close attention to:

- Interest rate and APR

- Points or lender credits

- Total loan costs

- Estimated cash to close

- Mortgage insurance

- Escrowed taxes and insurance

- Rate lock period and expiration date

One offer may show a lower rate because it includes more upfront points. Another may show lower cash to close because it uses lender credits, but that can come with a higher interest rate. Neither is automatically wrong. The right choice depends on your budget, timeline, and how long you plan to keep the loan.

Protect Yourself With Inspections and Smart Contingencies

First-time buyers sometimes feel pressure to waive protections in a competitive market. While every market is different, giving up inspections or contingencies can create major risk, especially if you do not have extra cash for repairs.

A home inspection does not guarantee the house is perfect, but it can reveal safety issues, roof concerns, plumbing problems, electrical defects, HVAC age, drainage concerns, and signs of deferred maintenance. These findings can help you renegotiate, request repairs, plan future costs, or walk away if the contract allows.

The appraisal is different from the inspection. The appraisal helps the lender assess value and certain property standards. It is not a full condition review for your benefit. You should understand both steps before making an offer.

If the appraisal comes in lower than the purchase price, you may need to renegotiate, bring more cash, change the loan terms, or cancel if your contract provides that option. If the home has condition issues, certain loan programs may require repairs before closing.

Your real estate agent and loan officer should help you understand the risks before you waive any protection.

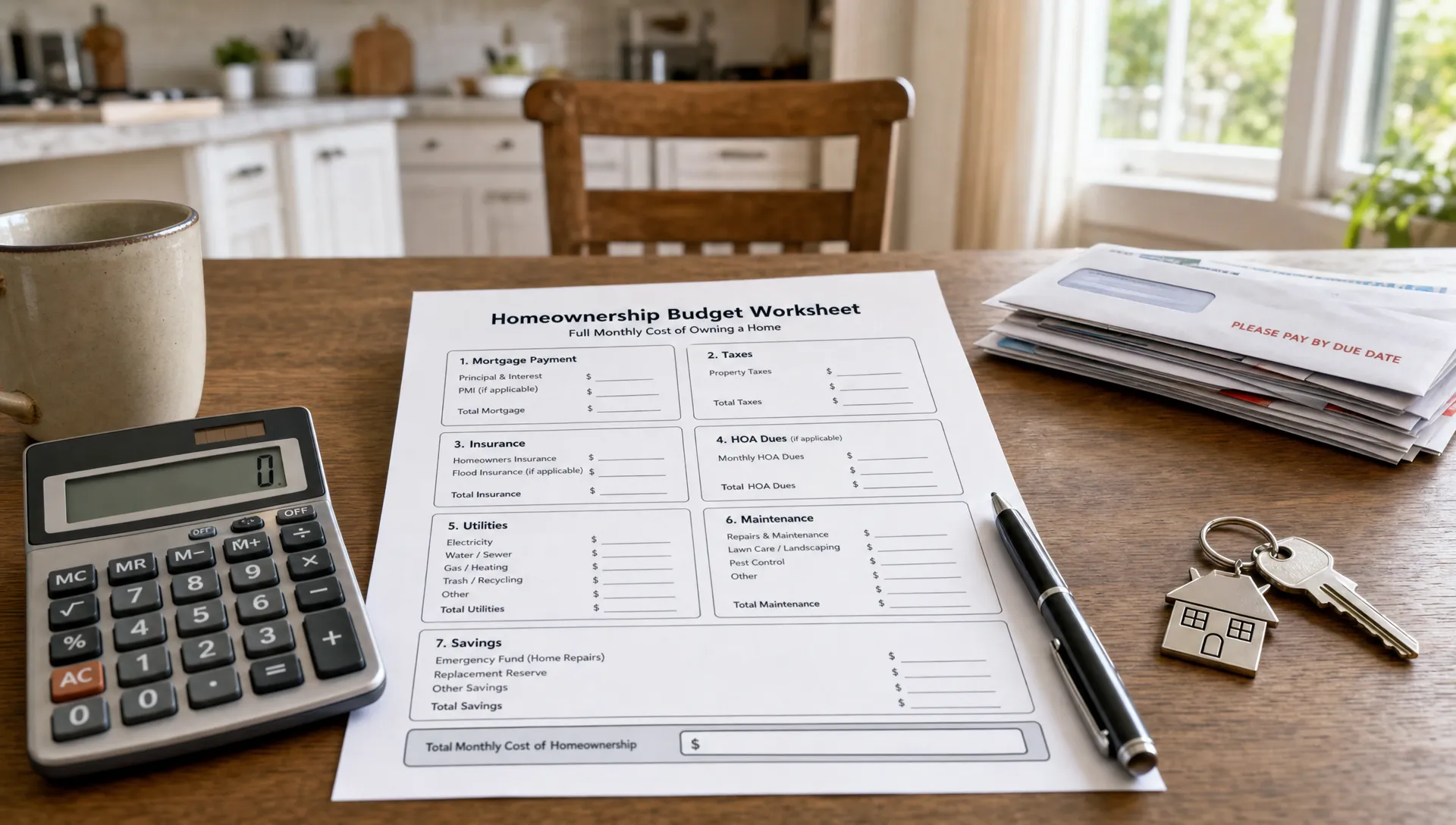

Budget for the First Year of Ownership

The first year in a home often costs more than buyers expect. Even a move-in-ready property may need locks changed, filters replaced, minor repairs, lawn equipment, window coverings, paint, pest service, or appliance upgrades.

Homeownership also changes your risk profile. If a water heater fails, the landlord is not coming. If property taxes or insurance increase, your escrow payment can rise. If the HOA announces a special assessment, you may need to pay it.

A good rule is to avoid turning your closing into a financial finish line. Closing day is the start of ownership, not the end of expenses.

Before you buy, ask yourself:

- If the payment rose by $150 to $300 per month later, could I still manage it?

- If a $2,000 repair happened in the first six months, would I have options?

- Do I understand whether taxes and insurance are escrowed?

- Does the HOA have healthy reserves and clear rules?

- Am I still saving for emergencies after closing?

This is where a slightly lower purchase price can create much more peace of mind than stretching to the top of your approval.

Understand the Neighborhood, Not Just the House

A home can look perfect in photos and still be a poor fit. Research commute times, schools if relevant, property tax trends, insurance costs, parking rules, noise, flood zones, HOA restrictions, future development, and resale demand.

Visit the area at different times if possible. A quiet street on a weekday morning may feel different during rush hour or on weekends. Check whether the home’s layout, lot, and location fit your life for more than the next six months.

You do not need to predict the future perfectly. But you should avoid buying based only on cosmetic appeal. Paint colors can change. Location, lot size, traffic patterns, and neighborhood restrictions are harder to fix.

Keep Your Timeline Realistic

A smooth purchase requires coordination between the buyer, seller, agents, lender, title company, appraiser, inspector, insurance provider, and sometimes the HOA. Delays can happen when documents are missing, appraisal turn times run long, title issues appear, insurance is hard to obtain, or repair negotiations take extra time.

Ask your lender what timeline is realistic for your loan type and market. Fast approvals are valuable, but only when the full file is ready and the transaction details support the closing date.

You can reduce delays by responding quickly, uploading complete documents, avoiding blurry screenshots, and keeping your loan officer updated on contract changes. New Era Lending’s technology-driven process includes secure document uploads and e-signature support, which can help simplify the paperwork side while still giving you access to human guidance.

For a full overview of what happens from application to closing, see The Mortgage Loan Process From Start to Closing.

Ask Better Questions Before You Commit

The most expensive mistakes often happen when buyers are too embarrassed to ask basic questions. Mortgage terms can be confusing, and a good lender should be willing to explain them clearly.

Before choosing a loan, ask:

- What is my estimated total monthly payment, including taxes and insurance?

- How much cash do I need to close?

- What loan programs do I qualify for, and why are you recommending this one?

- Am I paying points, receiving lender credits, or neither?

- How long is my rate locked, and what happens if closing is delayed?

- Can my mortgage insurance be removed later?

- What could still change before closing?

- What documents should I avoid delaying?

You can also review 10 questions to ask a home loan mortgage lender before you apply.

A Simple First-Home Buying Roadmap

Buying a first home becomes easier when you follow a clear sequence. The exact order can vary, but this structure helps reduce surprises.

- Set your comfort budget: Decide the monthly payment and cash-to-close range that fits your life, not just lender limits.

- Review credit and debts: Check for errors, avoid new debt, and understand how monthly obligations affect approval.

- Get pre-approved: Let a lender review your income, assets, credit, and loan options before you shop seriously.

- Compare loan scenarios: Look at cash to close, payment, APR, mortgage insurance, and long-term flexibility.

- Shop with discipline: Stay within your comfort range and research neighborhoods carefully.

- Make informed offers: Understand contingencies, inspection rights, appraisal risk, and seller concessions.

- Respond quickly during underwriting: Provide complete documents and avoid financial changes.

- Review closing documents: Compare final terms to expectations and ask questions before signing.

This process does not remove every risk, but it gives you more control over the biggest decisions.

Frequently Asked Questions

How much money should I save before buying my first home? It depends on your loan program, location, price range, and comfort level. Plan for the down payment, closing costs, moving expenses, immediate home needs, and an emergency reserve. Some buyers may qualify with a low down payment, but cash to close is more than the down payment alone.

Should I get pre-approved before looking at houses? Yes. Pre-approval helps you understand your budget, identify loan options, and make stronger offers. It also gives you time to fix documentation, credit, or income issues before contract deadlines matter.

Is the lowest mortgage rate always the best deal? Not always. A lower rate may come with points, higher upfront costs, or tradeoffs that do not fit your timeline. Compare the Loan Estimate, APR, monthly payment, cash to close, and rate lock terms before choosing.

Can I buy a first home with less than 20% down? Yes. Many buyers purchase with less than 20% down through conventional, FHA, VA, USDA, or assistance programs, depending on eligibility. The tradeoff may include mortgage insurance, funding fees, or program-specific requirements.

What is the biggest mistake first-time buyers make? One of the biggest mistakes is focusing on the house before understanding the full financing picture. A beautiful home can become stressful if the payment, cash to close, repairs, taxes, or insurance costs are higher than expected.

Buy With Clarity, Not Guesswork

The best way to buy a first home without costly mistakes is to prepare before emotions take over. Know your payment comfort zone, compare real loan scenarios, protect your cash reserves, and ask questions until the terms make sense.

New Era Lending helps buyers move through the mortgage process with smart technology, transparent guidance, secure document uploads, e-signature support, and personalized human help across a wide range of loan options. If you are preparing to buy your first home, getting pre-approved early can help you shop with confidence and avoid surprises before closing.