.jpg)

.jpg)

.jpg)

Down Payment for Home Loan: How Much You Really Need

The “you must put 20% down” rule is one of the biggest reasons buyers delay homeownership. In reality, the right down payment for a home loan depends on your loan program, your credit and income profile, the type of property you’re buying, and how competitive your market is.

This guide breaks down what you may need at minimum, what you might choose strategically, and how to decide on a number you can afford without draining your savings.

What a down payment is (and what it isn’t)

A down payment is the portion of the home price you pay upfront. The rest is financed with your mortgage.

It is not the same as:

- Closing costs (lender fees, title, escrow, appraisal, and other third-party costs)

- Prepaids (like homeowners insurance and property taxes you may pay upfront at closing)

- Cash reserves (money you keep available after closing, sometimes required, often recommended)

If you’ve been budgeting only for a down payment, you may be underestimating what you’ll need at the closing table. For a deeper breakdown, see New Era Lending’s explainer on closing costs.

Minimum down payment by loan type (common benchmarks)

Here are the down payment minimums many buyers qualify for, depending on the program. (Exact requirements vary by lender, scenario, and guidelines.)

Conventional loans

Many conventional loans allow low down payments, especially for primary residences.

- 3% down is a common minimum for some conforming conventional options for qualified buyers.

- 5% down is also common and can broaden eligibility depending on the file.

If you put less than 20% down on a conventional loan, you’ll typically pay private mortgage insurance (PMI) until you reach sufficient equity.

For background on conventional program options, Fannie Mae’s overview of low-down-payment products is a helpful reference: Fannie Mae HomeReady.

FHA loans

FHA loans are government-backed and are known for flexible qualification guidelines.

- 3.5% down is the widely cited minimum for many FHA borrowers who meet FHA requirements.

FHA loans include mortgage insurance (an upfront premium and monthly premium in many cases). You can confirm FHA basics via HUD’s FHA information.

New Era Lending also covers comparisons in FHA vs. Conventional Loans: Which One Is Right for You?.

VA loans

For eligible veterans, active-duty service members, and some surviving spouses:

- 0% down is possible with VA financing in many purchase scenarios.

VA loans can be a powerful path to homeownership because they may reduce or eliminate down payment requirements and do not require monthly PMI. Official program details are available at VA home loan benefits.

If you’re eligible, New Era Lending has a helpful veteran-focused guide: How Veterans Can Optimize Every Benefit They’ve Earned.

USDA loans

In designated rural and some suburban areas, USDA loans may allow:

- 0% down for eligible borrowers and properties.

Availability depends heavily on location and income requirements. You can learn more through the USDA Single Family Housing Guaranteed Loan Program.

Jumbo loans

For higher-priced homes that exceed conforming loan limits, down payment requirements are often higher.

- Many jumbo scenarios require 10% to 20% (or more), depending on credit, reserves, and the lender’s risk standards.

Because jumbo guidelines can vary widely, this is an area where a personalized pre-approval matters.

So how much down payment do you really need?

For most buyers, the real answer is this: you need enough down payment to get approved and win the home, while still keeping your overall finances healthy.

A practical way to choose a down payment is to balance four competing goals.

1) Get eligible for the loan program you want

Your minimum down payment depends on:

- Loan type (conventional, FHA, VA, USDA, jumbo)

- Occupancy (primary residence vs. second home vs. investment property)

- Property type (single-family, condo, multi-unit)

- Credit profile, income stability, and overall risk factors

For example, an investment property generally requires more down than a primary residence, and some condos can have additional restrictions.

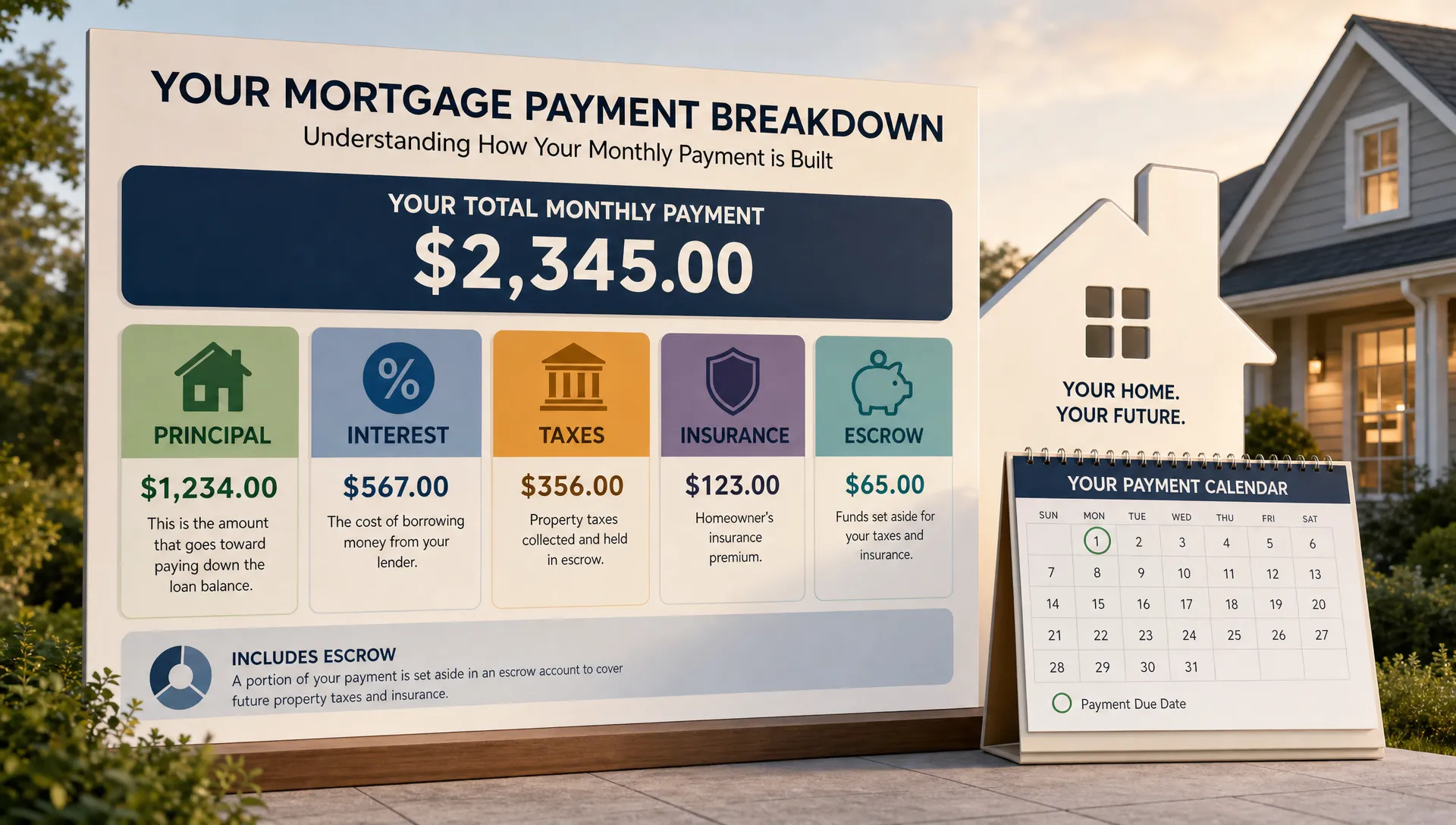

2) Keep the monthly payment comfortable (not just the loan amount)

A bigger down payment reduces the amount you borrow, which can reduce:

- Your monthly principal and interest payment

- Your mortgage insurance cost (or eliminate PMI at 20% down on conventional)

But it’s important to look at the whole payment, not just the down payment. Taxes, homeowners insurance, HOA dues, and mortgage insurance can matter as much as rate.

If you want a neutral reference for understanding what goes into a mortgage payment, the CFPB mortgage resources are a solid starting point.

3) Stay competitive in your local market

In some markets, sellers care less about your down payment and more about certainty of closing (strong pre-approval, clean offer, reasonable timelines). In other markets, a higher down payment can signal financial strength and reduce worries about appraisal or financing issues.

That said, a large down payment is not the only way to strengthen an offer. A great loan officer, clean documentation, and fast underwriting can also help.

4) Avoid becoming “house poor”

Putting every dollar into the down payment can backfire if you have no cushion for:

- Repairs and maintenance after move-in

- A job or income change

- A surprise medical bill

- Higher-than-expected utility costs

Many buyers feel safest keeping some cash reserves even if it means putting less than 20% down.

Common down payment targets (and why buyers choose them)

These are not rules, just common decision points.

3% to 5% down: “Get in sooner”

This range is popular with first-time buyers and buyers prioritizing liquidity.

Pros:

- Lower upfront cash requirement

- You keep more savings for reserves, furnishing, repairs, and life

Tradeoffs:

- You will likely pay mortgage insurance (PMI or FHA mortgage insurance)

- Loan approval may be more sensitive to credit score, DTI, and appraisal details

10% down: “Lower risk without draining savings”

This is a common middle ground.

Pros:

- Smaller loan balance than a minimum-down option

- Often lower mortgage insurance cost than 3% to 5% down (especially on conventional)

Tradeoffs:

- Still not enough to eliminate PMI on conventional

- May reduce your cash buffer if you overextend

20% down: “Eliminate PMI on conventional”

The biggest reason 20% is famous is that it can remove PMI on most conventional loans.

Pros:

- No PMI (in many conventional cases)

- Lower monthly payment from a smaller loan amount

Tradeoffs:

- Could delay buying by years while you save

- May leave you with less cash for repairs, reserves, and other priorities

Important note: FHA mortgage insurance rules work differently than conventional PMI, so “20% down” does not automatically mean “no mortgage insurance” with FHA.

A quick example: how down payment changes your loan size

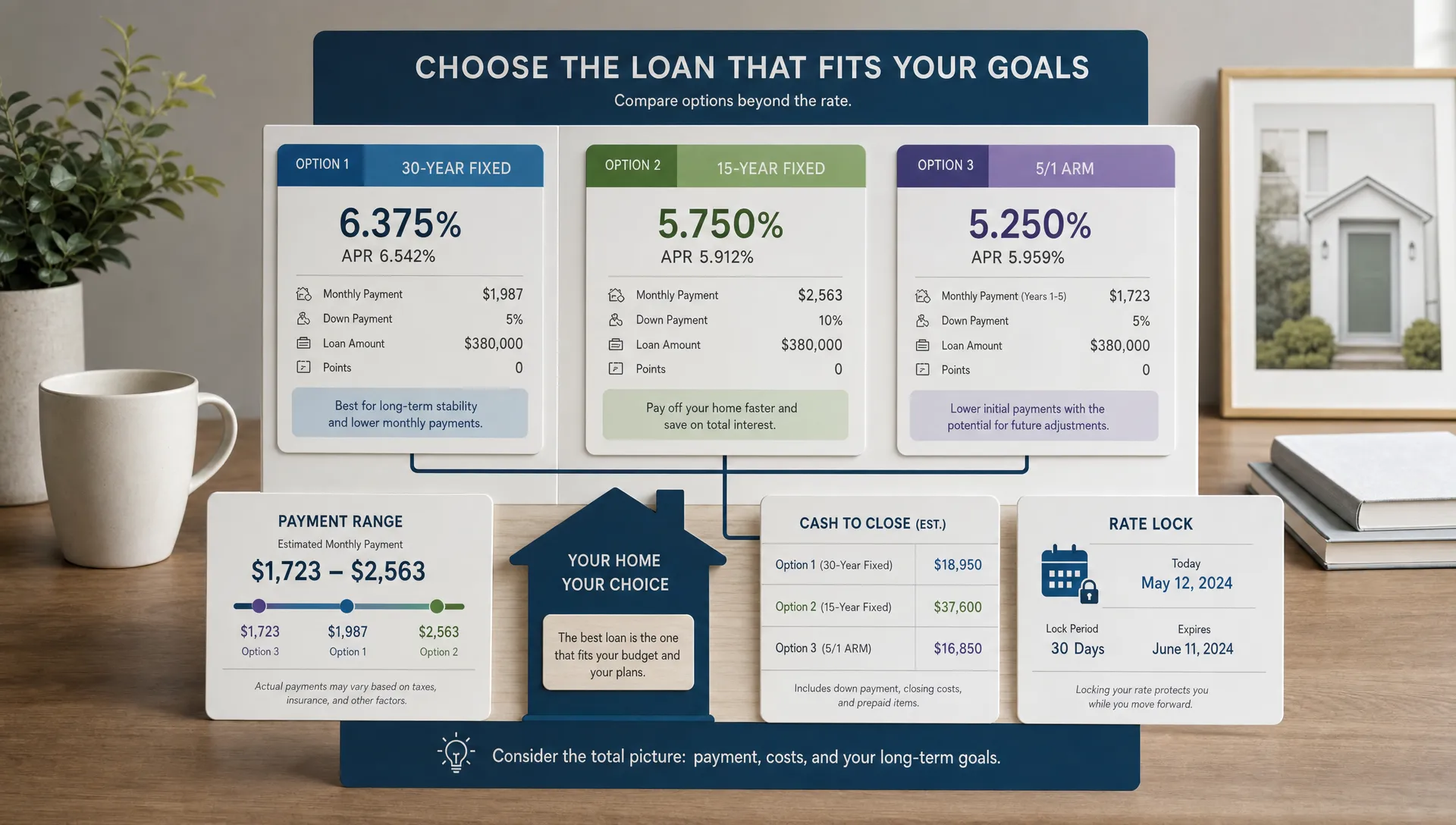

Let’s use a simple home price example to make the math tangible.

If the home price is $400,000:

- 3% down is $12,000, loan amount is about $388,000

- 5% down is $20,000, loan amount is about $380,000

- 10% down is $40,000, loan amount is about $360,000

- 20% down is $80,000, loan amount is about $320,000

Your monthly payment impact depends on your interest rate, term, and mortgage insurance. As a rough illustration only, a $68,000 smaller loan balance (the difference between 3% down and 20% down in this example) can reduce principal and interest noticeably, but you should run a personalized scenario that includes PMI, taxes, and insurance.

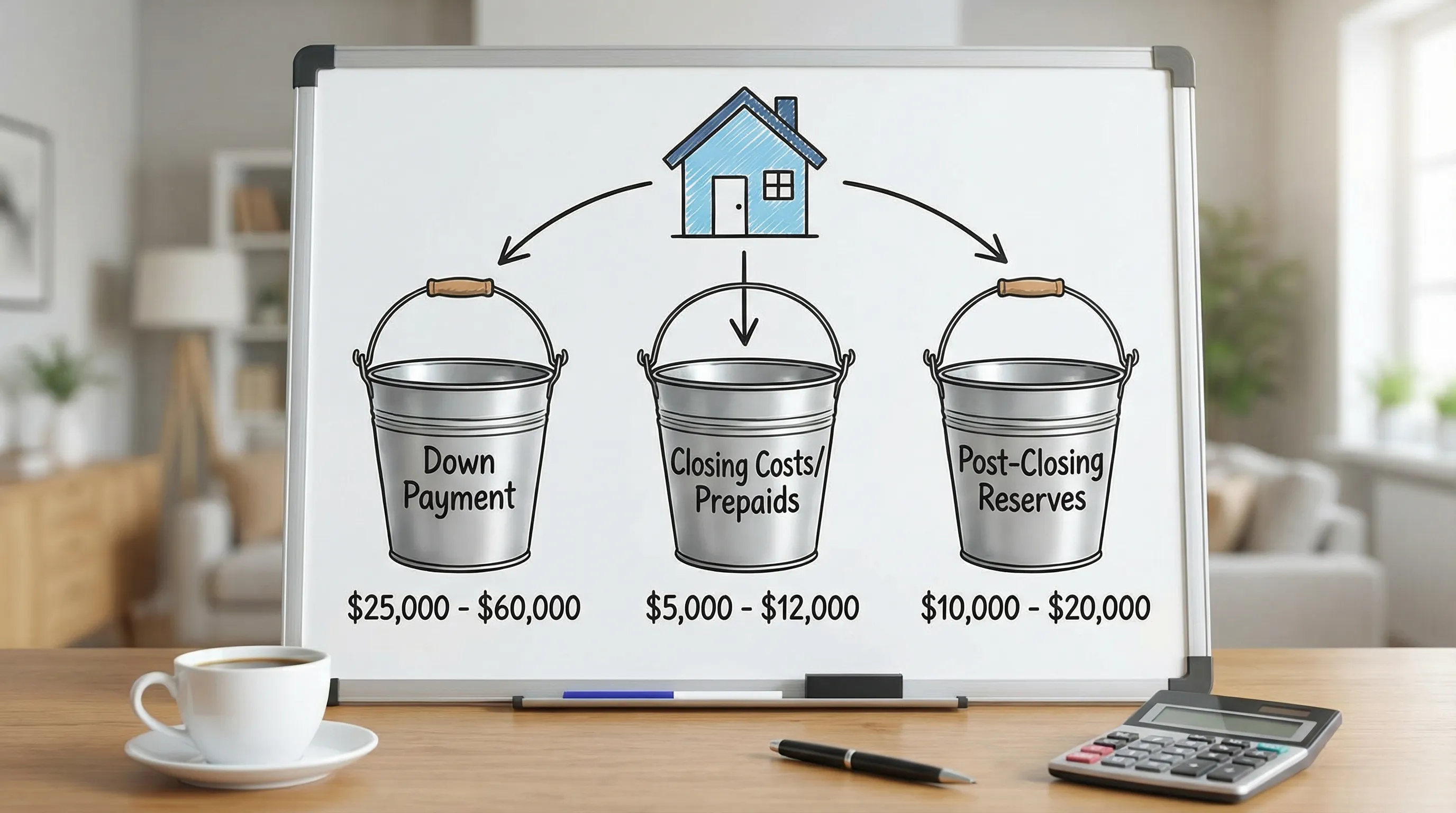

Don’t forget closing costs and prepaids

Even with a low down payment, you still need to plan for closing-related cash.

Closing costs and prepaids often include:

- Lender and third-party fees (appraisal, title, escrow)

- Prepaid homeowners insurance

- Prepaid property taxes (depending on timing)

These can be significant, which is why it’s smart to budget for both buckets from day one. New Era Lending’s closing costs guide is a good companion piece when you’re estimating cash to close.

Ways buyers cover the down payment (without breaking the rules)

Many buyers assume their only option is personal savings. In practice, there are several common, legitimate paths.

Gift funds

Some loan programs allow gift funds from qualified donors (often family). Rules vary by loan type and documentation requirements, so you want to confirm what’s acceptable before you move money.

Down payment assistance (DPA)

State, county, and city programs may offer grants or favorable second loans for eligible buyers. Availability and rules vary by location, and funding can be limited.

Seller concessions (where allowed)

In some transactions, the seller may contribute toward closing costs, which can reduce the amount of cash you need at closing, even if it doesn’t technically increase your down payment.

Strategic saving and account planning

If you’re building your down payment over time, consistency usually beats intensity. Automating transfers, limiting large new debt, and keeping your funds “easy to source” (well-documented) can help when underwriting begins.

New Era Lending’s Down Payments 101 goes deeper on assistance programs and other options, if you want a broader menu of strategies.

A simple framework to choose your down payment amount

If you want a clear decision process, use this checklist.

Start with the program you’re most likely to use

- Eligible for VA? Start with that path.

- Need FHA flexibility? Build around 3.5% down plus mortgage insurance.

- Strong credit and stable income? Compare conventional 3% to 5% options against higher-down scenarios.

If you’re not sure, New Era Lending’s FHA vs. conventional comparison can help you narrow it down.

Decide how much cash you want to keep after closing

A good down payment is one that still leaves you breathing room. Think about your:

- Emergency fund

- Expected first-year home expenses

- Job or income variability

Run scenarios based on monthly payment, not just down payment

Two buyers can put the same amount down and end up with very different monthly payments due to:

- Interest rate

- PMI or FHA mortgage insurance

- Property taxes and insurance

- HOA dues

Get pre-approved early

Pre-approval turns “I think I can” into “Here is what the numbers support.” It also helps you move quickly when the right home appears.

If you’re a first-time buyer, you may also like New Era Lending’s practical overview: 5 Things Every First-Time Buyer Should Know Before They Start.

Frequently Asked Questions

Is 20% down required for a home loan? No. Many borrowers buy with less than 20% down using conventional, FHA, VA, or USDA programs. The best amount depends on eligibility, monthly payment goals, and cash reserves.

What is the minimum down payment for a conventional loan? Many conventional options start at 3% down for qualified buyers on primary residences, but requirements vary by scenario, property type, and lender guidelines.

Is FHA always 3.5% down? 3.5% is a common minimum benchmark, but eligibility depends on meeting FHA requirements. Some borrowers may need a higher down payment depending on their profile.

Can I buy a home with 0% down? Potentially, yes. VA and USDA loans can allow 0% down for eligible borrowers and properties. Not everyone qualifies, and other costs (like closing costs) still apply.

Should I use my savings for a bigger down payment or keep cash reserves? It depends on your comfort level and financial stability. A larger down payment can reduce your loan size and mortgage insurance, but keeping reserves can protect you from surprise expenses after closing.

Do I need cash for closing costs in addition to the down payment? Usually, yes. Closing costs and prepaids are separate from your down payment. In some cases, seller concessions or assistance programs can reduce the cash you bring to closing.

Get a clear down payment plan with New Era Lending

If you want to know exactly how much down payment you’ll need for a home loan based on your credit, income, location, and goals, New Era Lending can help you model real scenarios and pick the smartest path.

Explore your options at New Era Lending and request a personalized pre-approval. With smart tools, secure document uploads, and expert guidance, you can move forward with clarity and confidence.