.jpg)

.jpg)

.jpg)

Mortgage Loan Requirements for 2026 Applications

Mortgage loan requirements in 2026 are not just about having a certain credit score or saving a down payment. Lenders look at the full picture: your income, debts, assets, property, loan program, and whether the file can be documented clearly enough to meet underwriting rules.

That can feel intimidating, especially if you are buying your first home, refinancing, self-employed, using a VA benefit, or trying to access equity. The good news is that most requirements fall into a few predictable categories. Once you understand what lenders need and why they need it, you can prepare a stronger application and avoid last-minute surprises.

This guide breaks down the main mortgage loan requirements for 2026 applications, including credit, income, debt-to-income ratio, down payment, documentation, property rules, and program-specific guidelines.

What lenders are really checking in 2026

A mortgage is a large, long-term loan secured by real estate. Because of that, lenders generally evaluate three things before approval.

First, they review your ability to repay. That means verifying income, employment, monthly debts, assets, and the stability of your financial picture. Second, they review your willingness to repay, which is usually reflected in your credit history, payment patterns, and overall debt management. Third, they review the property itself, because the home serves as collateral for the loan.

In 2026, many lenders use automated underwriting systems to evaluate conventional, FHA, VA, and USDA applications. These systems can return findings that approve, refer, or require additional documentation. But automated approval is not the same as final approval. A human underwriter still verifies the details, reviews documentation, and confirms that the property and loan file meet program and lender rules.

This is why two borrowers with similar credit scores can receive different outcomes. Loan type, down payment, debt ratio, reserves, employment type, property type, and documentation quality all matter.

Core mortgage loan requirements for most borrowers

Every loan program has its own rulebook, but most applications are built around the same core requirements. If you are preparing to apply in 2026, start with these areas.

1. Credit score and credit history

Your credit score helps lenders estimate risk, but it is not the only credit factor that matters. Underwriters also look at your payment history, open accounts, recent inquiries, collections, bankruptcies, foreclosures, and how much revolving credit you are using.

Common credit benchmarks include:

- Conventional loans often require a minimum credit score around 620, though stronger scores may qualify for better pricing.

- FHA loans may allow lower scores under FHA rules, including 580 with 3.5% down in many cases, but lender overlays can be stricter.

- VA loans do not set one universal minimum credit score, but lenders typically apply their own credit standards.

- USDA loans also rely on lender and automated underwriting standards, with credit history and repayment patterns playing an important role.

- Jumbo, investment property, and some non-QM loans often require stronger credit profiles.

Credit history can matter as much as the score itself. A borrower with a moderate score, clean recent payment history, and low debt may be easier to approve than a borrower with a slightly higher score but recent late payments or unstable debt patterns.

Before applying, review your credit reports, dispute clear errors, avoid opening unnecessary accounts, and keep credit card balances as low as practical. If you are already under contract or close to applying, ask your loan officer before making any major credit moves.

2. Stable and documentable income

Lenders need to verify that your income is likely to continue. For W-2 employees, that usually means recent pay stubs, W-2s, and possibly written or verbal employment verification. For salaried employees, the process can be straightforward. For hourly, commission, bonus, overtime, seasonal, or part-time income, lenders may need a longer history and may average the income.

Self-employed borrowers usually need more documentation. That can include personal and business tax returns, profit and loss statements, business bank statements, K-1s, 1099s, or year-to-date earnings information. Many programs prefer a two-year history of self-employment, although exceptions can sometimes apply when the borrower has related experience and strong documentation.

The main requirement is not just income amount. It is usable qualifying income. If your tax returns show lower net income because of business deductions, your qualifying income may be lower than your gross business revenue. That is one reason self-employed borrowers should prepare early and work with a lender who understands how underwriting calculates income.

3. Debt-to-income ratio

Your debt-to-income ratio, often called DTI, compares your monthly debt obligations to your gross monthly income. Lenders use DTI to evaluate whether the new housing payment fits your financial profile.

A typical DTI calculation includes the proposed mortgage payment, property taxes, homeowners insurance, mortgage insurance if applicable, HOA dues, credit card minimums, auto loans, student loans, personal loans, child support, and other required monthly debts.

There is no single DTI limit for every mortgage. Conventional loans may allow higher ratios when other factors are strong. FHA loans can be flexible with compensating factors. VA loans also consider residual income, which measures how much money is left after major obligations. Jumbo and investment property loans may have tighter DTI expectations.

As a practical rule, a lower DTI can improve your approval strength and may help with loan options. If your DTI is tight, paying down revolving balances, reducing installment debts, increasing documented income, or choosing a lower purchase price may help.

4. Down payment and cash to close

Your down payment is the portion of the purchase price you pay upfront. Cash to close is broader. It includes the down payment, closing costs, prepaid taxes and insurance, escrow deposits, and any program-specific costs.

Common down payment paths include conventional loans with as little as 3% down for eligible borrowers, FHA loans with 3.5% down for qualifying credit profiles, and VA or USDA loans that may allow 0% down for eligible buyers and properties. Jumbo, second-home, and investment property loans usually require more.

Many buyers focus only on the down payment and forget closing costs. That can create stress late in the process. Closing costs vary by loan size, location, taxes, insurance, discount points, lender credits, and title or settlement fees. Your Loan Estimate is the key document for comparing these costs.

The Consumer Financial Protection Bureau explains the Loan Estimate as a standardized form that helps borrowers compare loan terms, estimated payments, and closing costs. Review it carefully, and ask questions about anything that is unclear.

If you are planning a home purchase while also paying for a major life event, keep your mortgage funds organized and traceable. For example, if you are budgeting for wedding expenses, from venue deposits to bridal appointments with a specialist such as Le Michel Bruidsmode, avoid draining your verified cash reserves or opening new credit before closing.

5. Verified assets and reserves

Lenders need to confirm where your funds come from. Bank statements, retirement account statements, investment account statements, and gift documentation may be required. Large deposits usually need to be explained and sourced, especially if they are outside your normal income pattern.

Reserves are funds left over after closing. Not every loan requires reserves, but they can strengthen an application. Reserves may be especially important for investment properties, multi-unit homes, jumbo loans, self-employed borrowers, or files with higher DTI.

Acceptable funds can include checking and savings accounts, vested retirement funds, investment accounts, documented gifts, eligible down payment assistance, and proceeds from the sale of another property. Cash that cannot be sourced is usually a problem, so avoid moving money around without a clear paper trail.

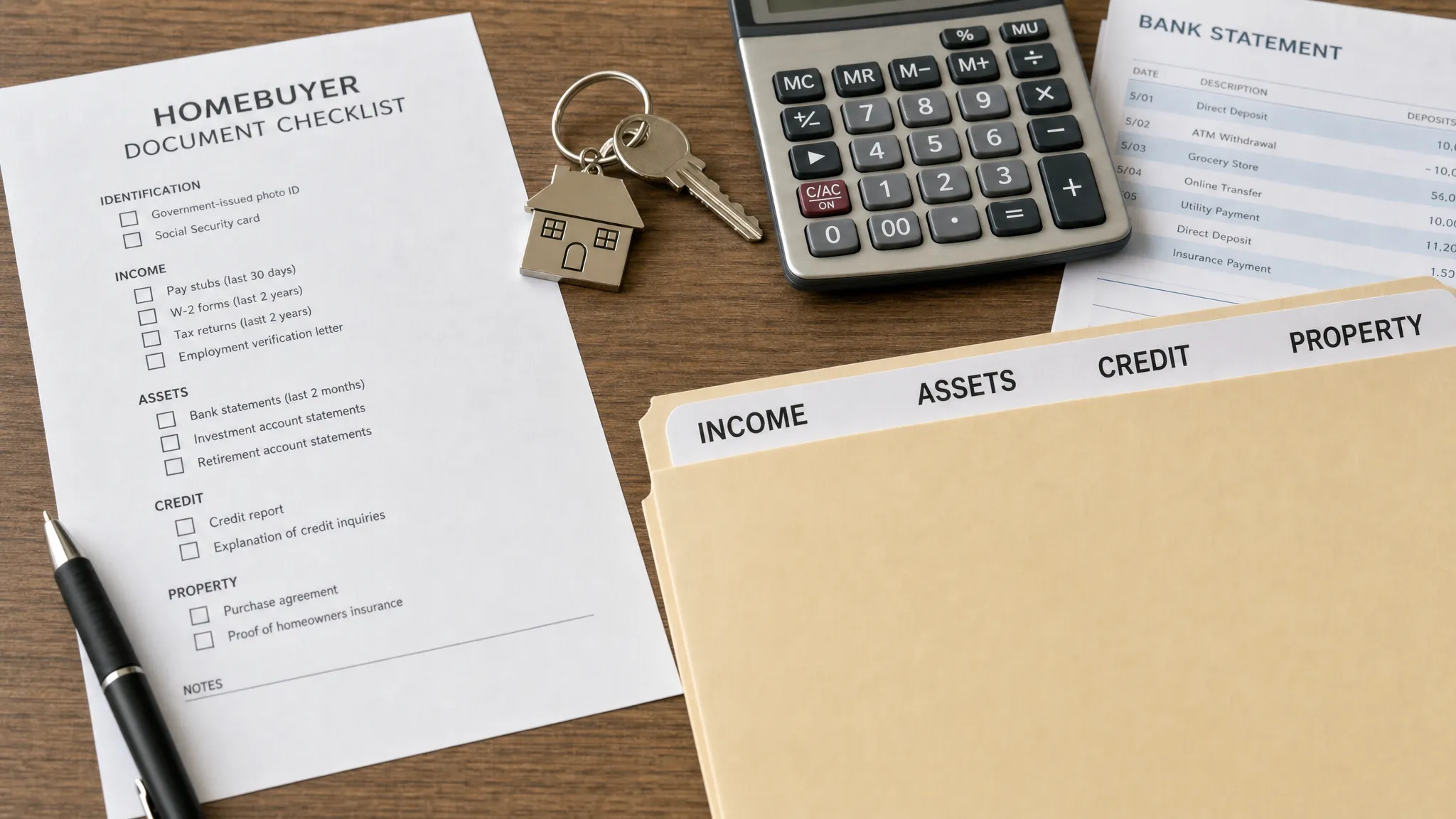

Documents you may need for a 2026 mortgage application

Documentation requirements vary by borrower and loan type, but most lenders will ask for a standard set of records. Having these ready can speed up pre-approval and reduce underwriting conditions.

Typical mortgage documents include:

- Government-issued photo ID and Social Security number or tax identification information.

- Recent pay stubs, usually covering the most recent 30 days.

- W-2 forms, often for the past two years.

- Personal tax returns if self-employed, commissioned, or using complex income.

- Business tax returns if you own a qualifying percentage of a business.

- Recent bank statements for checking, savings, and other asset accounts.

- Retirement or investment statements if used for reserves or funds to close.

- Gift letters and proof of transfer if using gift funds.

- Statements for debts not fully reflected on credit reports.

- Divorce decrees, child support orders, or alimony documentation if applicable.

- Purchase contract for a home purchase.

- Homeowners insurance quote or declarations page before closing.

For refinances, you may also need your current mortgage statement, homeowners insurance information, property tax bill, payoff details, and documentation for any liens on the property.

For VA loans, eligible borrowers typically need a Certificate of Eligibility. The Department of Veterans Affairs provides guidance on how to request a COE. For USDA loans, property location and household income eligibility are key factors, and the USDA provides information about its single family housing guaranteed loan program.

Property requirements lenders review

Mortgage approval is not only about the borrower. The property must also meet loan program requirements.

The appraisal is central to this review. An appraiser estimates the home’s market value and may identify property condition concerns. The appraised value helps determine loan-to-value ratio, which affects eligibility, mortgage insurance, down payment requirements, and sometimes pricing.

Property requirements can include:

- The home must be acceptable collateral for the loan program.

- The appraised value must support the loan amount and required LTV.

- Title must be clear enough for the lender to secure its lien.

- The property must have adequate homeowners insurance.

- Condo projects may need to meet program-specific approval standards.

- FHA and VA loans may require repairs for certain safety, soundness, or habitability issues.

- Occupancy must match the loan application, such as primary residence, second home, or investment property.

This is why pre-approval is only one part of the process. A borrower can be financially qualified, but a property issue can still delay or change the loan approval. If you are buying a condo, manufactured home, multi-unit property, or fixer-upper, discuss the property type with your lender before making an offer.

Mortgage loan requirements by program

Choosing the right program can make a major difference in how your application is reviewed. The best option depends on your credit, cash to close, military eligibility, income, property location, and long-term goals.

Conventional loans

Conventional loans are not insured by the federal government. They are common for primary residences, second homes, and investment properties. Many conventional loans follow Fannie Mae or Freddie Mac guidelines, though lenders may have additional requirements.

A conventional loan may be a strong fit if you have a solid credit profile, stable income, and enough down payment to meet program rules. Some eligible buyers may qualify with a low down payment, while borrowers with 20% down can often avoid monthly private mortgage insurance.

Conventional loan requirements often focus heavily on credit score, DTI, LTV, property type, reserves, and whether the loan amount falls within conforming loan limits. The Federal Housing Finance Agency publishes conforming loan limit information, and limits can change annually.

FHA loans

FHA loans are insured by the Federal Housing Administration and are often used by buyers who need more flexible credit or down payment requirements. FHA loans generally require owner occupancy, mortgage insurance premiums, and an appraisal that meets FHA property standards.

FHA can be helpful for first-time buyers, borrowers rebuilding credit, or buyers with limited cash to close. However, mortgage insurance rules and property standards should be reviewed carefully. A lower entry requirement does not automatically mean the lowest long-term cost.

VA loans

VA loans are available to eligible veterans, active-duty service members, certain National Guard and Reserve members, and eligible surviving spouses. VA loans may offer 0% down, no monthly private mortgage insurance, and flexible underwriting, but borrowers must meet service eligibility, occupancy, lender, and property requirements.

VA underwriting also considers residual income. This can be helpful because it looks beyond a simple DTI percentage and evaluates whether the borrower has enough remaining income after major obligations. VA loans may include a funding fee unless the borrower is exempt.

USDA loans

USDA loans are designed for eligible rural and some suburban areas. They may allow 0% down for qualified borrowers, but both the property and household income must meet USDA requirements. USDA loans are generally for primary residences, not investment properties or second homes.

USDA can be an excellent option when the location, income, and property rules line up. Because eligibility is location-specific, buyers should confirm the property area early.

Jumbo, non-QM, and specialty loans

Jumbo loans exceed conforming loan limits and usually have stricter requirements. Borrowers may need higher credit scores, larger down payments, lower DTI, and significant reserves.

Non-QM and specialty loans may help borrowers who do not fit standard guidelines, such as certain self-employed borrowers, real estate investors, or applicants with alternative documentation. These programs vary widely, so it is important to compare not only the rate, but also fees, prepayment terms, documentation rules, and long-term fit.

Requirements for refinance and cash-out applications

Refinance applications share many requirements with purchase loans, but the focus shifts toward your current mortgage, property value, equity, and refinance goal.

For a rate-and-term refinance, lenders typically review your credit, income, DTI, assets, property value, current loan, and whether the new loan provides a clear benefit. For a cash-out refinance, lenders also review how much equity you have and how much cash you want to access. Cash-out loans often have stricter LTV limits and pricing adjustments than simple rate-and-term refinances.

Some FHA and VA refinance programs may offer streamlined documentation in specific cases, but streamlined does not mean no requirements. You may still need to meet payment history, seasoning, benefit, occupancy, and program rules.

Before refinancing in 2026, compare the full picture: rate, APR, closing costs, new loan term, monthly payment, break-even period, and how long you expect to keep the loan. A lower payment can be useful, but extending the term or rolling in costs may increase total interest over time.

What can hurt approval in 2026

Many mortgage delays happen because of changes made after pre-approval. Once you apply, your financial profile should stay as steady as possible until closing.

Common issues that can hurt approval include:

- Opening new credit cards, auto loans, personal loans, or buy-now-pay-later accounts.

- Making large unexplained deposits or moving funds between accounts without documentation.

- Changing jobs, income structure, or employment type without telling your lender.

- Missing payments or increasing credit card balances.

- Spending down funds needed for closing or reserves.

- Co-signing for someone else’s loan.

- Applying for a property type that does not fit the loan program.

- Submitting incomplete or inconsistent documentation.

If something changes, communicate quickly. A good loan team would rather know early than discover an issue during final underwriting.

How to strengthen your mortgage application before applying

You do not need a perfect financial profile to qualify for a mortgage. But preparation can improve your options, reduce stress, and help your loan officer identify the right program.

Start by checking your credit and correcting obvious errors. Pay all accounts on time and try to reduce revolving balances if possible. Avoid new debt before and during the mortgage process.

Next, organize income and asset documents. If you are self-employed, review your tax returns with a mortgage professional before assuming your gross revenue will qualify. If you receive bonus, overtime, commission, rental, retirement, or support income, ask how that income will be calculated.

Then, estimate your full monthly housing payment, not just principal and interest. Property taxes, homeowners insurance, mortgage insurance, HOA dues, and escrow adjustments can materially affect affordability.

Finally, get a real pre-approval before shopping seriously. A strong pre-approval reviews credit, income, assets, and loan fit in more detail than a quick estimate. It can help you shop with confidence and make a more credible offer.

A practical 2026 application checklist

Before you submit a full mortgage application, use this checklist to spot gaps.

- Confirm your target loan purpose: purchase, refinance, cash-out, or equity access.

- Review your credit report and avoid new credit activity.

- Estimate your comfortable monthly payment and cash-to-close range.

- Gather income, asset, ID, and debt documentation.

- Identify your likely loan programs, such as conventional, FHA, VA, USDA, jumbo, or specialty options.

- Verify whether your property type or location creates special requirements.

- Ask how your DTI, reserves, credit score, and down payment affect approval.

- Review your Loan Estimate when issued and compare APR, fees, payment, and cash to close.

- Keep your finances stable from application through closing.

This checklist is simple, but it reflects how underwriting works. The clearer your file is, the easier it is to identify solutions early.

Frequently Asked Questions

What are the basic mortgage loan requirements in 2026? Most borrowers need acceptable credit, verifiable income, a manageable debt-to-income ratio, enough funds for down payment and closing costs, documented assets, and a property that meets loan program standards. Exact requirements depend on the loan type and lender.

What credit score do I need for a mortgage in 2026? Conventional loans often require around 620 or higher, while FHA loans may allow lower scores under certain conditions. VA and USDA programs do not have one universal score requirement, but lenders set their own standards. A higher score can improve approval options and pricing.

How much income do I need to qualify for a mortgage? There is no single income number. Lenders compare your qualifying income to your monthly debts and proposed housing payment. Your required income depends on the loan amount, interest rate, taxes, insurance, debts, and loan program.

Can I get a mortgage with student loans or credit card debt? Yes, but those payments are included in your debt-to-income ratio. High monthly obligations can reduce your qualifying loan amount. Paying down revolving debt or choosing a lower payment target may help.

Do I need 20% down to qualify? No. Many borrowers qualify with less than 20% down, depending on the program. Conventional loans may allow low down payment options, FHA can allow 3.5% down for qualifying borrowers, and VA or USDA loans may allow 0% down for eligible buyers. Less than 20% down may involve mortgage insurance or program fees.

What is the difference between pre-qualification and pre-approval? Pre-qualification is usually an early estimate based on limited information. Pre-approval typically involves a deeper review of credit, income, assets, and loan options. A stronger pre-approval can make the homebuying process smoother.

Can mortgage requirements change during 2026? Yes. Loan limits, program guidelines, investor rules, insurance costs, and lender overlays can change. Always verify current requirements with a licensed mortgage professional before making decisions.

Get clear on your 2026 mortgage options

Mortgage loan requirements do not have to be confusing. The key is knowing which rules apply to your situation and preparing your file before you are under pressure.

New Era Lending combines smart mortgage technology with personalized human guidance to help borrowers purchase, refinance, or access equity with more confidence. With secure document uploads, e-signature support, transparent rate and term discussions, and a wide range of loan options, the process is designed to be simpler without losing the personal support that matters.

If you are planning a 2026 application, start with a personalized review. Visit New Era Lending to explore your options and connect with a team that can help you understand what you need to qualify.