.jpg)

.jpg)

.jpg)

VA Loans for First-Time Home Buyers: Eligibility and Next Steps

If you’re a veteran, active-duty service member, or eligible surviving spouse, a VA home loan can be one of the most first-time-buyer-friendly paths to homeownership. The challenge is that “VA eligibility” and “first-time home buyer” rules get mixed together online, and that confusion can delay your pre-approval or lead you to plan for the wrong costs.

This guide breaks down VA loans for first-time home buyers, how eligibility works, what you should do next, and the most common mistakes to avoid so you can move from “thinking about buying” to a confident offer.

Do VA loans require you to be a first-time home buyer?

No. VA loans do not require you to be a first-time home buyer. VA home loan eligibility is tied to military service (or qualifying status as a surviving spouse), not whether you’ve owned a home before.

That said, you might still be considered a “first-time home buyer” for other programs, such as certain state or local down payment assistance programs, which often define “first-time” as not owning a home in the last 3 years. Those definitions vary by program.

If your plan is to combine a VA loan with other assistance, it’s worth confirming the specific first-time buyer definition early so you do not waste time pursuing a program you do not qualify for.

VA loan eligibility basics (what actually matters)

To use a VA loan, you generally need:

- Eligibility based on service (or qualifying surviving spouse status)

- A Certificate of Eligibility (COE)

- A property that meets VA occupancy and property standards

- Lender approval based on income, credit, and overall risk (the VA guarantees a portion of the loan, but lenders still underwrite the file)

The VA’s official starting point is its overview of the program on VA.gov.

Service eligibility (high level)

Service requirements can depend on whether you are active duty, a veteran, National Guard/Reserve, or another eligible category. Because rules can be specific and documentation varies, the most practical next step for most buyers is to request the COE rather than trying to self-diagnose eligibility from memory.

Eligible surviving spouses

Some surviving spouses may qualify, typically tied to circumstances around the service member’s death and benefit status. If this is your situation, your lender can help you identify the right documentation to request a COE.

Prior homeownership and VA entitlement

You can often use a VA loan even if you’ve owned a home before. What matters is whether you have available VA entitlement and whether you’ve restored entitlement after a previous VA loan. This is one reason the COE is so important: it clarifies your entitlement status so your lender can structure the right scenario.

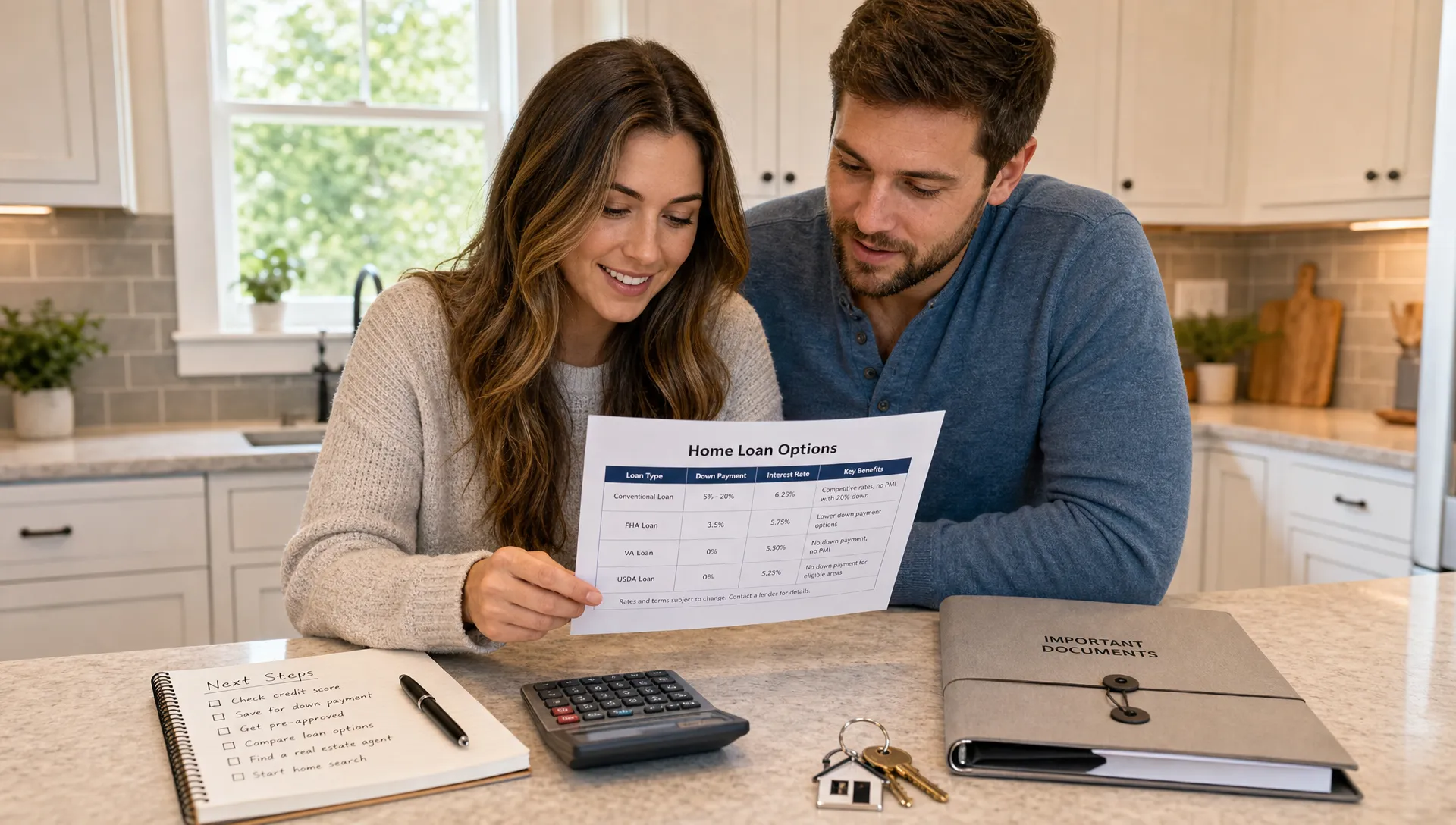

Why VA loans are especially strong for first-time buyers

First-time buyers usually have two big constraints: cash to close and monthly payment comfort. VA loans are designed to reduce friction in both areas.

Potential for $0 down (when eligible)

Qualified borrowers may be able to purchase with no down payment, which can preserve savings for reserves, moving costs, and early home maintenance.

No monthly mortgage insurance

VA loans do not have monthly private mortgage insurance (PMI). Many first-time buyers coming from FHA or low-down-payment conventional options are surprised how much this can impact the monthly payment.

More flexible real-world underwriting than many buyers expect

The VA program has guidelines, but the lender still determines approval based on the full file (income stability, debts, credit history, and assets). Many first-time buyers worry they need perfect credit, but VA loans can be workable for borrowers with less-than-perfect profiles, depending on the overall picture.

Assumable feature (in some cases)

VA loans can be assumable, meaning a qualified buyer may be able to take over the existing VA loan terms. This can be valuable in certain rate environments, but assumptions come with rules and timelines.

Costs first-time buyers should plan for with a VA loan

Even with $0 down, you should still plan for cash-to-close items and “day one” homeowner expenses.

Closing costs and prepaid items

VA loans still include typical closing costs (third-party fees, title, escrow, lender charges) plus prepaid items like homeowners insurance and property taxes (depending on timing). The VA also limits what veterans can be charged for certain fees.

For the VA’s current guidance on allowable costs, see the VA page on funding fees and closing costs.

The VA funding fee (and exemptions)

Many VA borrowers pay a VA funding fee, which helps keep the program running. The amount varies based on factors such as down payment and whether it’s your first time using the VA benefit.

Some borrowers are exempt from the funding fee, for example certain veterans receiving VA disability compensation. Your COE and supporting documentation help confirm this.

Inspection, appraisal, and “repair buffer”

A home inspection is usually optional (but strongly recommended) and paid by the buyer. VA appraisals are required and include Minimum Property Requirements (MPRs). A first-time buyer mistake is budgeting only for closing and forgetting:

- Inspection fees

- Earnest money deposit

- Minor repairs or updates after move-in

- Utility deposits, moving costs, and initial furnishings

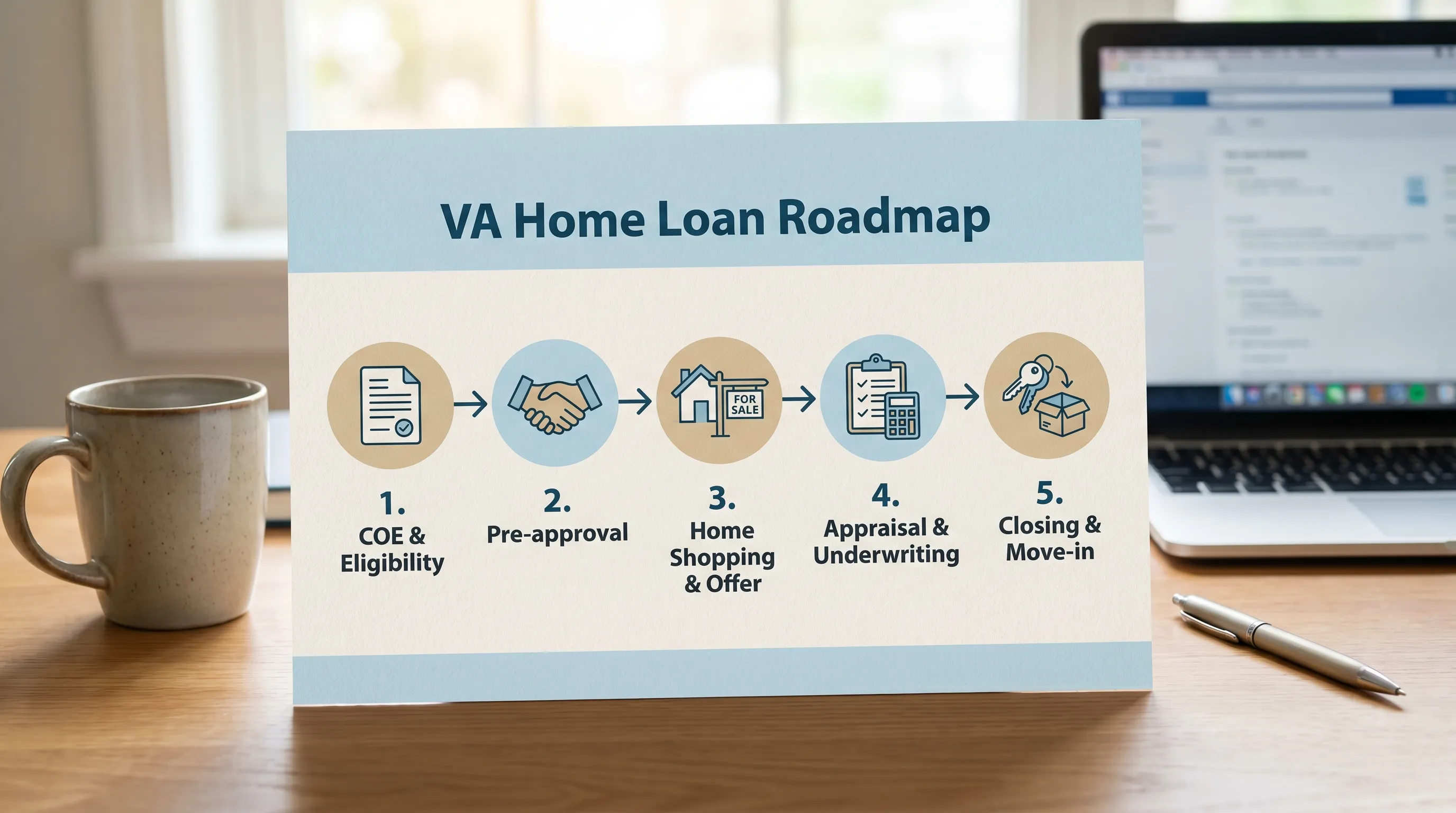

Next steps: how to buy a home with a VA loan (clear, first-time-buyer friendly)

Buying your first home is less stressful when you treat it like a simple workflow: confirm eligibility, get pre-approved, shop with the right guardrails, then move through underwriting with minimal surprises.

Step 1: Request your Certificate of Eligibility (COE)

Your COE confirms you meet VA eligibility requirements and shows your entitlement details. In many cases, a lender can help obtain it electronically, but some files require additional documentation.

If you want to understand the official process, the VA explains COEs on VA.gov.

Step 2: Get a true pre-approval (not just a quick pre-qualification)

First-time buyers often hear “pre-qualified” and assume they’re ready to make offers. In a competitive market, a stronger pre-approval typically means your lender has reviewed documentation and you have a clearer understanding of the numbers.

This is where you should decide:

- Target purchase price range

- Comfortable monthly payment range

- Down payment plan (even if it’s $0 down, you may choose to put money down)

- Whether you want a fixed rate, ARM, or a buydown strategy

If you want a deeper dive on loan structures, New Era Lending’s guide on fixed vs ARM vs buydowns is a helpful companion read.

Step 3: Prepare a simple “underwriting-ready” document set

A clean file shortens the time between offer acceptance and clear-to-close.

Common documents include:

- Government-issued ID

- COE (or permission for your lender to pull it)

- Recent pay stubs and W-2s (or other income documentation)

- Bank statements (checking, savings, retirement if needed for reserves)

- Current debts and minimum monthly obligations

If you’re self-employed, documentation is usually more involved. New Era Lending has a dedicated guide on self-employed mortgage qualification.

Step 4: Shop for a home that fits VA occupancy and property rules

VA loans are intended for primary residences, not vacation homes or pure investment properties. Typically, you’ll need to occupy the home within a required timeframe (often discussed as around 60 days, depending on circumstances).

Also, certain property types (condos, multi-units, manufactured homes) can be eligible, but there are extra rule checks. If you’re unsure what’s allowed, see New Era Lending’s overview of VA property types, occupancy, and rules.

A practical first-time-buyer tip: ask your lender early if a condo is VA-approved, or if the property condition is likely to raise appraisal issues.

Step 5: Make an offer with the right expectations about VA appraisals

Some sellers worry VA deals take longer or require excessive repairs. In reality, the biggest delays usually come from preventable issues like missing documents, unclear income, or property problems discovered late.

You can reduce friction by using:

- A strong pre-approval letter

- An agent who understands VA transactions

- Realistic timelines for appraisal and underwriting

Step 6: Move through appraisal and underwriting (and respond fast)

Once you’re under contract, your lender will order the appraisal and underwriting begins. You may be asked for “conditions,” which are follow-up documents or clarifications. Responding quickly is one of the easiest ways to keep your closing on track.

Step 7: Review your Closing Disclosure and cash to close

Before closing, you’ll receive a Closing Disclosure showing your final loan terms and the amount due at closing. Compare it to your Loan Estimate and ask questions about changes.

How to strengthen your offer when using a VA loan

VA buyers can absolutely win in competitive markets. The goal is to reduce uncertainty for the seller while staying within VA guidelines.

Consider these offer-strengthening moves:

- Choose a lender known for clear communication and reliable timelines

- Keep documentation ready so underwriting can move quickly

- Understand what seller concessions can and cannot cover, and structure your request accordingly

- Focus on homes that are likely to meet VA Minimum Property Requirements to avoid last-minute repair disputes

When a VA loan might not be the best fit

VA loans are powerful, but there are situations where another route could make sense, for example if you’re buying a non-primary residence, you need a very specific property type, or the economics of the VA funding fee versus alternatives do not work in your favor.

If you want a broader comparison framework, New Era Lending also outlines veteran loan options beyond the VA loan.

A quick note if you’re thinking about investing (not buying a primary residence)

Many first-time buyers start with a primary residence, then think about investing later. Just remember: VA loans are built for owner-occupancy, so they are not a fit for a purely investment-focused purchase.

If you’re exploring international real estate investing separate from your primary home purchase, you might find it useful to research specialized partners in that space, such as UAE off-plan investment opportunities with Azimira. That’s a different lane than VA financing, but it can help you keep your goals and tools aligned.

Frequently Asked Questions

Can I use a VA loan if I’ve never bought a home before? Yes. VA eligibility is based on military service (or qualifying surviving spouse status), not prior homeownership.

What credit score do I need for a VA loan as a first-time buyer? The VA does not set a minimum credit score in its program guidelines, but lenders may have their own requirements. Your income, debts, and overall profile also matter.

Do VA loans really have no down payment? Many eligible borrowers can buy with $0 down, but you may still have closing costs and prepaid items. Some buyers also choose to put money down to reduce the funding fee or monthly payment.

How do I get my VA Certificate of Eligibility (COE)? You can apply through VA.gov, by mail, or often through a lender who can request it electronically when you start the pre-approval process.

Are VA loans only for single-family homes? No. VA loans can work for several property types, but there are occupancy rules and property standards. Condos and multi-unit properties may require extra checks.

Ready for the next step? Get a VA purchase plan you can trust

If you’re a first-time home buyer using a VA loan, the fastest way to reduce stress is to get a clear, numbers-based plan before you shop: price range, monthly payment target, estimated cash to close, and a timeline you can actually execute.

New Era Lending combines smart technology with personalized human guidance to help you move from COE to pre-approval to closing with less confusion. If you’re buying in one of the 39 states where New Era Lending operates, you can start the process with secure document uploads and e-signature support, and get transparent scenarios tailored to your goals.

Explore your options and start a VA pre-approval at New Era Lending.