.jpg)

.jpg)

.jpg)

Veteran Loans: What Options Exist Beyond the VA Loan

A VA loan is often the headline benefit people associate with military service, and for good reason. But it is not the only path to homeownership or refinancing for eligible veterans, active duty service members, and many military families. In real life, borrowers compare options because the “best” loan depends on the property, your credit profile, your cash on hand, how competitive your local market is, and whether you want to preserve VA eligibility for later.

Below is a practical guide to veteran loans and mortgage options beyond the VA loan, including when each option tends to shine and what tradeoffs to watch.

Why a veteran might choose a non-VA mortgage

This is not about replacing VA loans. It is about understanding when another program can be a better fit.

Common reasons veterans explore non-VA options include:

- Not currently eligible for VA financing, or COE/entitlement issues that take time to resolve.

- Property type constraints, for example some condos or unique properties that are difficult to approve under certain guidelines.

- Seller perception in competitive markets, where some sellers prefer offers they believe will close faster or with fewer conditions (this varies by market and is not always justified).

- Preserving VA entitlement for a future move (especially for frequent relocations).

- Cost structure preferences, such as avoiding the VA funding fee when it applies, or comparing overall pricing based on credit score, down payment, and lender credits.

- Investment property plans, since VA is primarily for owner-occupied homes.

Conventional loans (conforming): a strong alternative for many veterans

A conventional loan is not government-insured (unlike FHA or USDA). For veterans with solid credit and stable income, conventional financing can be very competitive.

Where conventional loans can work especially well

- Low down payment options are often available for qualified borrowers (program minimums vary by guideline and borrower profile).

- Cancelable mortgage insurance can be a meaningful advantage. If you put less than 20% down, you typically pay private mortgage insurance (PMI), but it can often be removed later when equity requirements are met.

- Wider property flexibility in some scenarios, including certain condos.

- Second homes are generally possible with conventional financing (subject to guidelines), which matters for some military households planning a post-service location.

Key tradeoff to understand

If you put less than 20% down, PMI can increase the monthly payment, and PMI pricing is heavily influenced by credit score and down payment size. For some borrowers, VA’s no monthly mortgage insurance structure still wins long term. For others, conventional can be cheaper month to month, particularly with strong credit and a decent down payment.

If you want a deeper primer on how conventional compares to other common programs, New Era Lending has a useful overview: FHA vs. Conventional Loans: Which One Is Right for You?

FHA loans: flexible credit guidelines when life has happened

An FHA loan is insured by the Federal Housing Administration. It is often considered by buyers who need more flexibility on credit history, down payment sourcing, or debt-to-income tolerance.

Where FHA tends to help

- Lower minimum down payment is possible for many borrowers who qualify.

- More forgiving credit standards compared to many conventional scenarios.

- Gift funds are commonly used for down payment and closing costs (subject to documentation rules).

Key tradeoffs to understand

FHA includes mortgage insurance that works differently than PMI. Depending on your down payment and loan terms, FHA mortgage insurance can last a long time and may not be removable the same way PMI is. That does not make FHA “bad,” but it does mean you should compare total monthly payment, upfront costs, and how long you expect to keep the loan.

USDA loans: 0% down in eligible areas (not just “farmland”)

A USDA loan (USDA Rural Development) is designed to encourage homeownership in eligible areas and for households under certain income limits. Many people assume USDA is only for rural towns, but eligible zones can include suburban areas as well.

Where USDA can be a great fit

- No down payment for eligible borrowers.

- Often attractive for buyers who want to keep cash reserves for moving, repairs, or emergency savings.

What to watch

- Location eligibility is non-negotiable. The property must be in an eligible area.

- Household income limits apply.

For veterans who are not using VA financing (or who want to preserve entitlement), USDA can be one of the few true 0% down alternatives.

State and local veteran homebuyer programs (often overlooked)

Beyond federal loan types, many states, counties, and cities offer veteran-focused housing benefits that can pair with conventional or FHA financing, and in some cases may complement VA as well.

These programs vary widely, but may include:

- Down payment assistance (DPA) as a grant or a second mortgage with deferred payments

- Reduced interest rate programs through state housing finance agencies

- Closing cost assistance

- Property tax exemptions or reductions for qualifying disabled veterans (this is not a mortgage benefit, but it changes affordability)

Because these benefits depend on location, the best approach is to ask your loan officer what is available in your specific county and whether you can combine it with the mortgage type you want.

Assumable mortgages: sometimes the most powerful “rate strategy”

In a market where rates can shift quickly, assumable mortgages deserve a mention. Some government-backed loans (commonly FHA, USDA, and VA) may be assumable, meaning a qualified buyer can take over the seller’s existing interest rate and terms rather than starting from scratch.

Veterans may run into assumable opportunities in two ways:

- Buying a home with an existing FHA or USDA loan and assuming that loan if the servicer and program allow it.

- Buying a home with an existing VA loan and pursuing a VA assumption (rules and entitlement implications can be more complex here).

Important reality check: even when a loan is assumable, you may need cash (or secondary financing) to cover the difference between the purchase price and the remaining loan balance. Still, when the assumed rate is meaningfully lower than current market rates, the math can be compelling.

Renovation loans (for veterans buying a fixer)

Not every home is move-in ready, and not every buyer wants turnkey. If you are purchasing a property that needs repairs or upgrades, you may consider a renovation-oriented loan.

Common non-VA renovation paths include:

- FHA 203(k) (often used for primary residences needing qualifying improvements)

- Conventional renovation programs offered through certain investors and lenders (availability varies)

Renovation loans add complexity, such as contractor bids, inspection requirements, and draw processes, but they can convert a “hard no” property into a financeable purchase.

Portfolio and non-QM loans: niche solutions when the standard boxes do not fit

Some veterans have strong overall finances but do not fit standard underwriting patterns. Examples include:

- Self-employed borrowers with heavy write-offs

- Retirees with significant assets but limited traditional income

- Buyers with recent major life transitions

In these cases, certain lenders offer portfolio or non-QM (non-qualified mortgage) options. These are not inherently risky, but they are typically more scenario-specific, and pricing can differ from mainstream loans. The right move is to compare these options carefully against conventional, FHA, USDA, and VA scenarios.

For self-employed borrowers who want to understand how lenders evaluate income, New Era Lending’s guide is a good starting point: How to Qualify For a Self-Employed Mortgage Loan

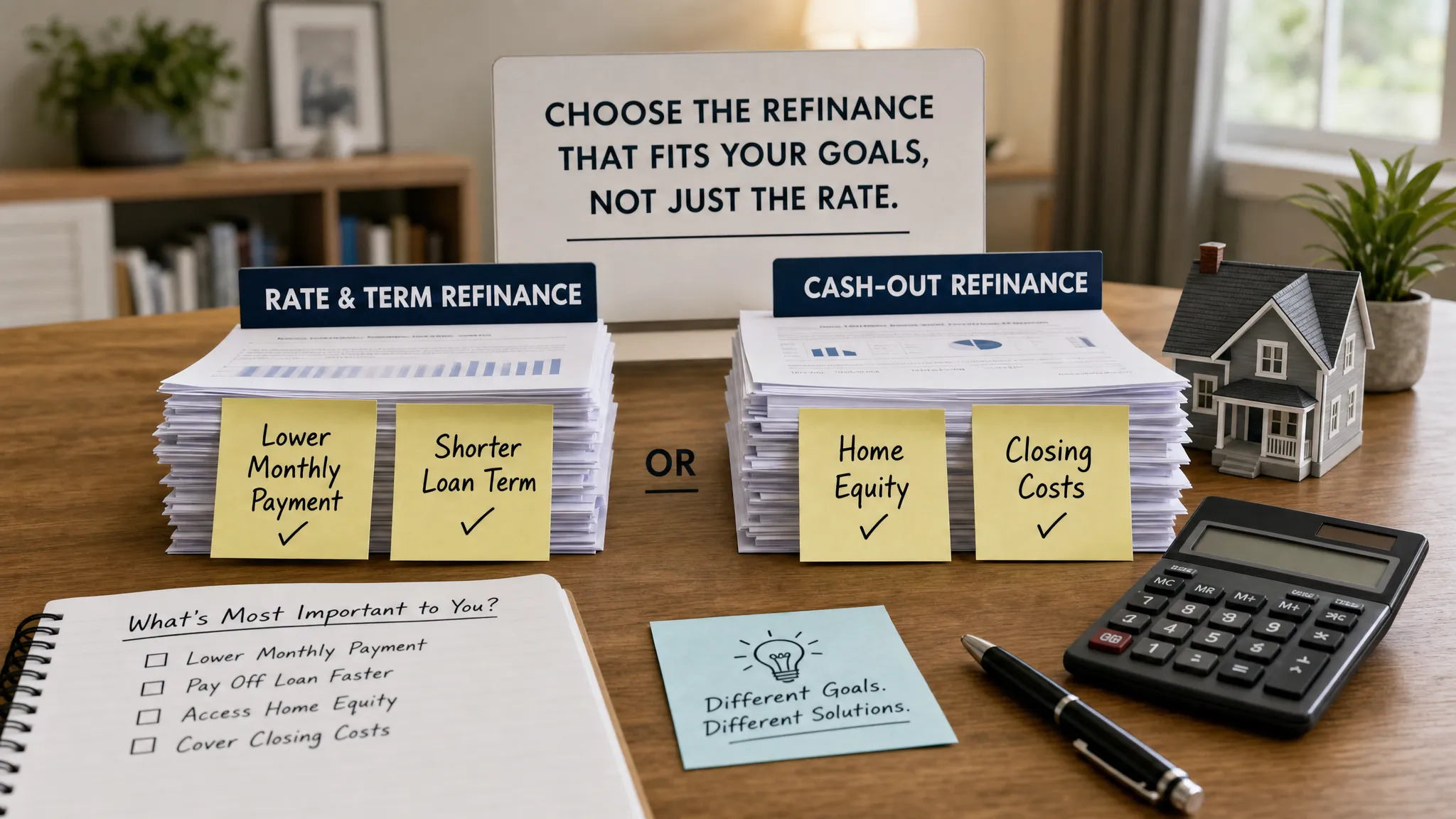

Equity access beyond VA: cash-out refinance vs HELOC

“Veteran loans” is not only about buying. Many veterans also explore equity access after they have owned for a few years.

Two common routes:

- Cash-out refinance: Replace your current mortgage with a larger one and take the difference as cash.

- HELOC (home equity line of credit): Keep your existing mortgage and add a revolving line of credit secured by your home.

The better choice depends on your current rate, how much cash you need, whether you want a fixed payment, and how quickly you plan to repay. A HELOC can be useful for flexible projects and staged expenses, while a cash-out refi can make sense when it also improves the primary mortgage structure.

A simple decision framework: which non-VA option is most likely to fit?

If you are comparing loans beyond VA, start with a few “anchor” questions. Your answers narrow the field quickly.

- Do you need (or strongly prefer) 0% down? USDA might be worth checking if the property is eligible.

- Is credit or recent credit history the main constraint? FHA may be more forgiving.

- Do you have strong credit and at least some down payment available? Conventional often competes well on total cost.

- Is the home a fixer-upper? Consider FHA 203(k) or conventional renovation products.

- Are you buying in a highly competitive market? Discuss closing timelines, appraisal strategy, and documentation readiness with your loan officer. Sometimes execution matters as much as program choice.

Do not forget the “full monthly budget” beyond the mortgage

When you move, your payment is only one part of the monthly picture. Utilities can swing affordability more than buyers expect, especially for larger homes, older construction, or properties with inefficient heating and cooling.

If you are buying a mixed-use property or planning to operate a business out of a building where energy costs are material, it can help to learn how commercial energy users manage procurement and consumption. One example resource (Germany-focused) is energy procurement guidance for businesses, which highlights how organizations approach energy sourcing and management when costs are a major operating line item.

How New Era Lending can help you compare veteran loan options confidently

The hardest part of choosing “the best” loan is that you cannot judge it by the interest rate alone. You need to compare:

- Total monthly payment (including mortgage insurance when applicable)

- Cash needed to close (down payment, closing costs, reserves)

- How long you expect to keep the loan

- Property eligibility and condition

- The probability of a smooth, on-time closing

New Era Lending’s approach combines modern tools with human guidance, so you can evaluate multiple paths (VA and beyond) without guessing. If you are buying, refinancing, or exploring equity access, a clear side-by-side comparison and a solid pre-approval game plan usually makes the decision straightforward.