.jpg)

.jpg)

.jpg)

Home Loan Lending Rates: How to Compare Quotes

A mortgage quote can look simple at first glance: one interest rate, one monthly payment, and a few estimated costs. But when you are comparing home loan lending rates, the lowest number on the screen is not always the best deal.

Two lenders can quote the same interest rate with very different fees. One lender may offer a lower rate only because you are paying discount points upfront. Another may show a slightly higher rate but include a lender credit that lowers your cash to close. A third may quote a great rate with a short lock period that does not match your closing timeline.

The goal is not just to find the lowest advertised rate. The goal is to compare quotes on equal terms, understand the full cost, and choose the mortgage that fits your monthly budget, cash-to-close plan, and long-term goals.

Why home loan lending rates vary from quote to quote

Mortgage rates change for two broad reasons: the market and your individual loan profile.

Market conditions include inflation expectations, bond yields, investor demand for mortgage-backed securities, Federal Reserve policy signals, and economic data. These factors can move pricing daily, and sometimes more than once in the same day.

Your individual quote is shaped by details such as credit score, loan amount, down payment, property type, occupancy, loan program, term, debt-to-income ratio, and whether you are paying points or receiving lender credits. That is why a rate you see online may not match the rate you are personally offered.

It is also why advertised rates need context. Lenders and mortgage companies may promote rates through search ads, email campaigns, social media, or even automated direct mail campaigns designed to generate borrower interest. Those offers can be useful starting points, but they are not a substitute for a personalized quote based on your actual scenario.

For a deeper look at how mortgage pricing is built, see New Era Lending’s guide on how home mortgage lending rates are set.

Start by making every quote use the same assumptions

The most common mistake borrowers make is comparing quotes that are not actually comparable. A 6.75% quote with one point is not the same as a 6.875% quote with no points. A 30-day rate lock is not the same as a 60-day lock. A conventional quote is not the same as an FHA, VA, jumbo, or investment property quote.

Before you ask lenders for pricing, define the exact scenario you want them to quote. If you change the inputs, the offer changes.

Have these details ready:

- Purchase price or estimated home value

- Down payment amount or current loan balance if refinancing

- Estimated credit score range

- Property type, such as single-family home, condo, or multi-unit property

- Occupancy, such as primary residence, second home, or investment property

- Loan purpose, such as purchase, rate-and-term refinance, or cash-out refinance

- Desired loan program, if known

- Loan term, such as 30-year fixed or 15-year fixed

- Preferred rate lock period

- Whether you want to pay points, avoid points, or see both options

If you are early in the process, it is fine if some numbers are estimates. Just make sure each lender is quoting the same estimates. Once you have a signed purchase contract, property address, and more complete documentation, your quote can become more precise.

Do not compare interest rate alone

The interest rate matters because it affects your principal and interest payment. But the interest rate is only one part of the quote.

A mortgage quote should be reviewed through several lenses:

- Interest rate: The percentage used to calculate interest on the loan balance.

- APR: A broader cost measure that includes the interest rate and certain loan costs, expressed as a yearly percentage.

- Monthly payment: The estimated amount you pay each month, including principal and interest, and often taxes, insurance, mortgage insurance, and HOA dues when applicable.

- Cash to close: The estimated amount you need to bring to closing after down payment, costs, credits, and prepaids.

- Points or credits: Upfront cost or lender assistance that changes the rate and cash needed.

- Rate lock: The period during which the quoted rate is protected, assuming the loan closes on time and the loan details do not materially change.

The best quote depends on what you are optimizing for. A buyer with plenty of cash and a long ownership timeline may prefer paying points to reduce the rate. A buyer trying to preserve savings may prefer a slightly higher rate with a lender credit. A homeowner refinancing for a short expected timeframe may care more about break-even than the lowest possible rate.

Use the Loan Estimate as your comparison tool

The Loan Estimate is the standardized form lenders provide after you apply for a mortgage and give the required information. Because the format is consistent, it is one of the best tools for comparing lenders.

The Consumer Financial Protection Bureau offers a helpful Loan Estimate explainer that walks borrowers through the form. When reviewing quotes, focus especially on these areas.

Page 1: loan terms, payment, and cash to close

Page 1 gives you the headline numbers. This is where you can see the loan amount, interest rate, monthly principal and interest, whether the rate can change, estimated total monthly payment, and estimated cash to close.

This page is useful because it helps you answer three practical questions:

Is the payment comfortable? Is the cash to close realistic? Is the loan structure what you expected?

Be careful with the monthly payment line. Some quotes may show only principal and interest, while others estimate the full housing payment. For real budgeting, you want to understand the complete payment, including property taxes, homeowners insurance, mortgage insurance, and HOA dues when applicable.

Page 2: origination charges and closing costs

Page 2 is where many quote differences become clear. Pay close attention to lender fees, discount points, processing or underwriting charges, appraisal costs, title fees, recording fees, prepaids, escrow deposits, and lender credits.

Not every cost is controlled by the lender. For example, property taxes, homeowners insurance, and some government recording charges may be similar no matter which lender you choose. But lender fees, points, and credits can vary significantly.

When comparing lenders, separate the costs into categories:

- Costs controlled by the lender, such as origination charges and points

- Third-party costs, such as appraisal and title services

- Prepaid items, such as interest, insurance, and escrow deposits

- Credits, including lender credits and seller credits

This helps you avoid being distracted by differences that may not represent a true lender pricing advantage.

Page 3: APR and long-term cost context

Page 3 includes the APR, total interest percentage, and other comparison details. APR is useful, but it is not perfect. It assumes you keep the loan for the full term and it can be affected by how certain fees are calculated.

For borrowers who expect to sell, refinance, or pay off the loan early, the APR may not tell the whole story. In that case, you also need to look at break-even, cash to close, and monthly savings.

For a plain-English review of APR, points, and amortization, read New Era Lending’s guide to loan terms explained.

Understand points, lender credits, and the rate tradeoff

Discount points are optional upfront fees paid to reduce the interest rate. One point equals 1% of the loan amount. For example, one point on a $400,000 loan equals $4,000.

A lender credit works in the opposite direction. You accept a higher interest rate, and the lender provides a credit that can help offset closing costs. This can reduce cash needed at closing, but it may increase the monthly payment.

Neither choice is automatically good or bad. It depends on your timeline and cash strategy.

Paying points may make sense if you expect to keep the loan long enough for monthly savings to outweigh the upfront cost. Taking a lender credit may make sense if you want to preserve cash, expect to move or refinance soon, or need help managing closing costs.

A simple break-even test can help. If paying $3,000 in points saves $75 per month, the break-even period is 40 months. If you expect to keep the loan beyond that point, paying points may be worth considering. If not, a no-point or credit-based option may be more practical.

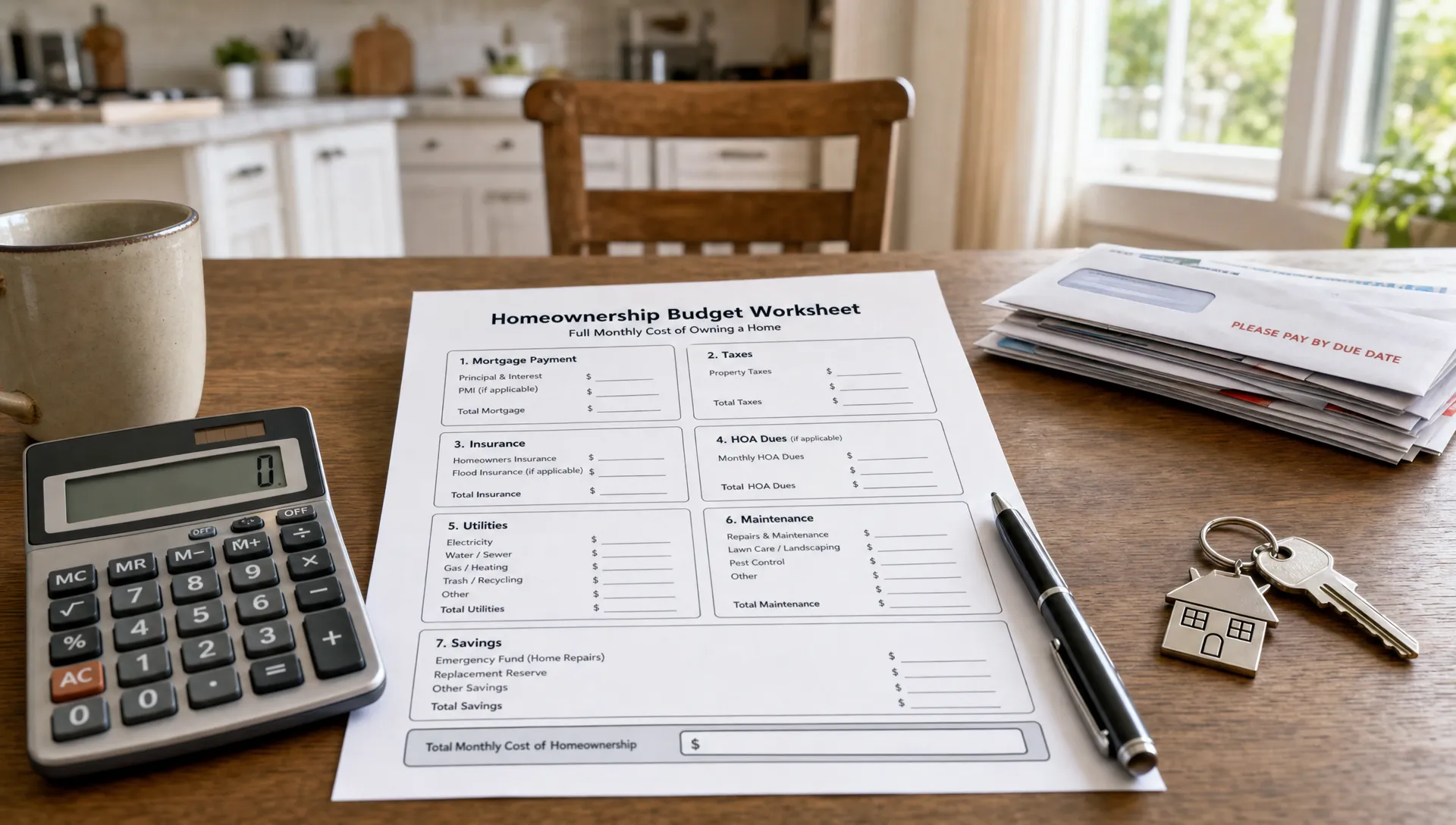

Compare the full monthly payment, not just principal and interest

A quote that lowers your principal and interest payment may still produce a higher total monthly housing payment if taxes, insurance, mortgage insurance, or HOA dues are estimated differently.

Your full payment may include:

- Principal and interest

- Property taxes

- Homeowners insurance

- Mortgage insurance, if required

- HOA dues, if applicable

- Flood insurance, if required

For purchase loans, tax estimates can be especially important. Some homes are reassessed after sale, and the prior owner’s tax bill may not reflect your future bill. Insurance can also vary widely by location, property age, coverage level, and risk factors.

When comparing quotes, ask each lender whether the payment includes the same tax and insurance assumptions. If one quote looks lower because taxes or insurance are understated, it may not be the better mortgage.

Check the rate lock period and lock terms

A great rate is only useful if it can be protected through closing. Rate locks commonly run for periods such as 30, 45, or 60 days, although available options vary by lender and scenario.

Longer locks may cost more or come with slightly different pricing. Shorter locks may offer better pricing but create risk if your closing timeline is uncertain. If your purchase contract gives you 45 days to close, comparing a 30-day lock from one lender to a 45-day lock from another is not an equal comparison.

Ask each lender:

- How long is the rate locked?

- What happens if closing is delayed?

- Is there a lock extension fee?

- Does the lock include a float-down option?

- What loan changes could affect the locked pricing?

This is especially important in a rate environment where pricing can move quickly. A quote without a clear lock strategy may leave you exposed to changes later.

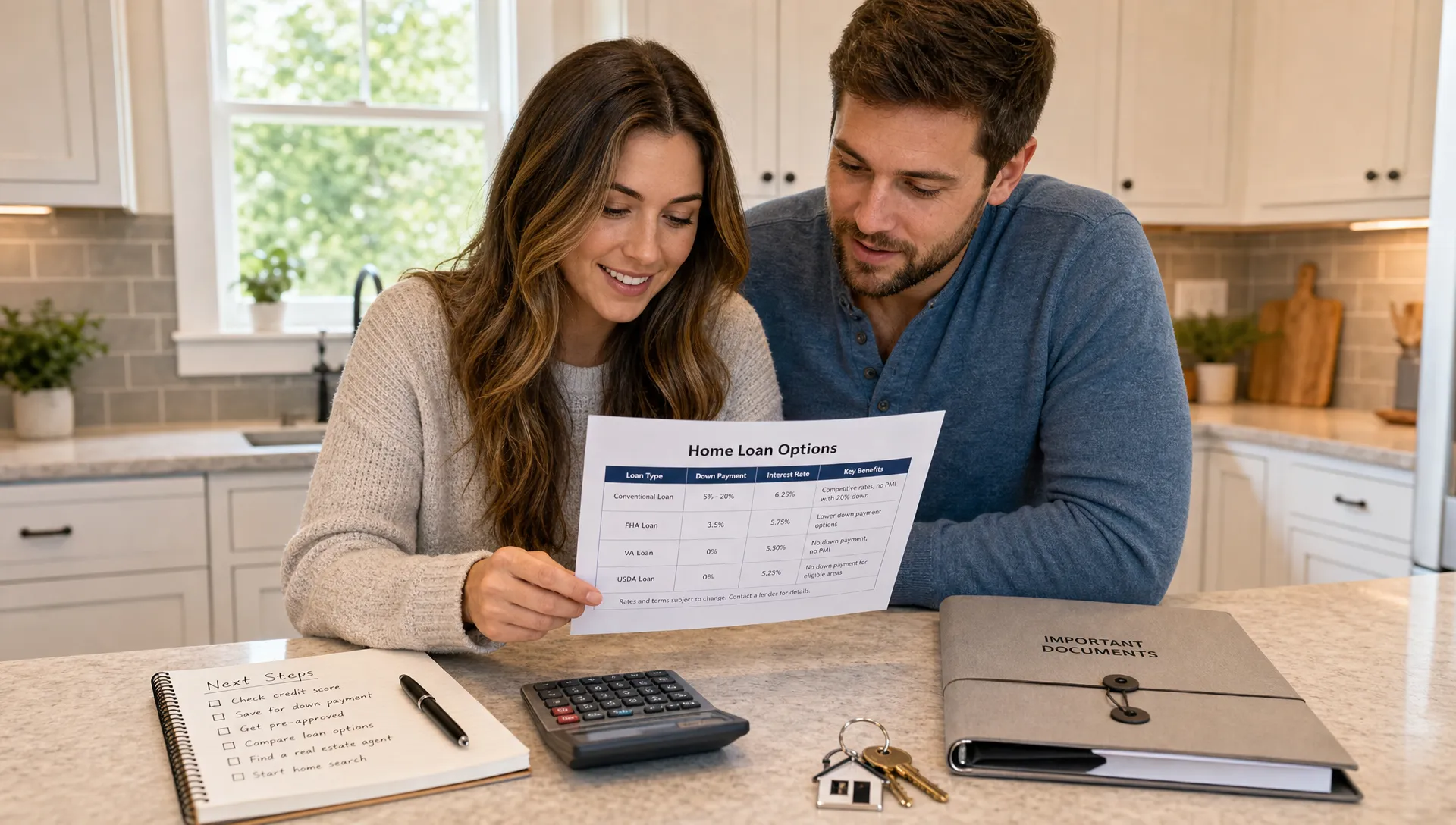

Compare loan programs carefully

Different loan programs can produce different rates, fees, mortgage insurance rules, and underwriting requirements. The best home loan lending rates for one borrower may not be tied to the same program that works best for another borrower.

Common options include conventional loans, FHA loans, VA loans, USDA loans, jumbo loans, and specialized programs for unique borrower profiles. Each can serve a different purpose.

For example, a conventional loan may be attractive for a borrower with strong credit and enough down payment to reduce or avoid mortgage insurance. An FHA loan may help a buyer with a smaller down payment or more flexible credit needs. A VA loan may be a powerful option for eligible veterans, active-duty service members, and certain surviving spouses because it can offer 0% down and no monthly private mortgage insurance, subject to eligibility and program requirements.

The key is to compare programs by total cost and approval fit, not just the rate. A lower interest rate can be offset by higher mortgage insurance, funding fees, or cash-to-close requirements.

If you are still deciding among loan types, New Era Lending’s guide to mortgage loan programs can help you understand the main differences.

Watch for quote red flags

Most mortgage professionals want to help borrowers make informed decisions, but not every quote is presented clearly. Slow down if something feels vague or too good to be true.

Potential red flags include:

- A rate quote that does not disclose points or lender fees

- A payment estimate that excludes taxes, insurance, or mortgage insurance without saying so

- Pressure to lock before you understand the offer

- A quote based on a credit score, down payment, or loan amount that does not match your situation

- Missing information about the lock period

- Large lender credits that are not explained

- Verbal promises that do not appear on the Loan Estimate

You do not need to become a mortgage expert, but you should feel comfortable asking questions. A lender should be willing to explain how the quote was built and what could cause it to change.

How many mortgage quotes should you compare?

Many borrowers benefit from comparing at least two or three personalized quotes. The point is not to collect endless offers. The point is to understand whether the pricing, fees, and service match your needs.

When timing your rate shopping, try to request quotes within the same short window. Mortgage pricing can change daily, so comparing one quote from Monday with another from the following week may not be a fair test.

Credit scoring models generally allow a shopping window for mortgage inquiries, meaning multiple mortgage credit checks within a defined period are typically treated as one inquiry for scoring purposes. The exact treatment depends on the scoring model, but the broader point is simple: concentrated shopping is usually better than spreading applications out over months.

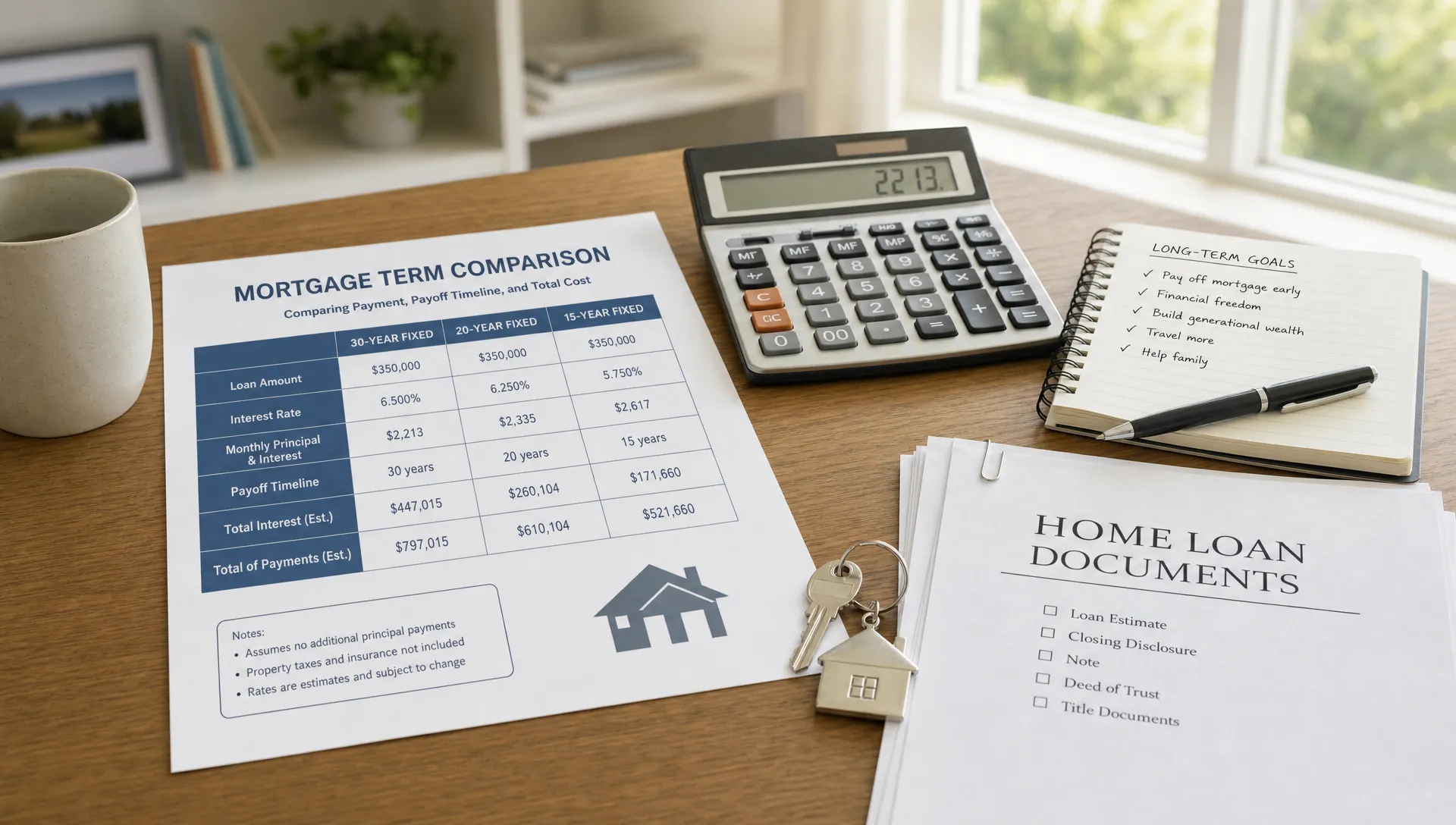

A simple example of comparing two quotes

Imagine two lenders quote a $350,000, 30-year fixed loan.

Lender A offers 6.75% with $4,000 in discount points and estimated cash to close of $22,000. Lender B offers 6.95% with no points and estimated cash to close of $18,000.

At first, Lender A looks better because the rate is lower. But if the monthly savings are $45 and you pay $4,000 more upfront, the break-even period is about 89 months. If you plan to stay in the home and keep the loan for 10 years or more, Lender A may be worth considering. If you may move or refinance within five years, Lender B may preserve cash and offer a better practical fit.

Now imagine Lender B’s quote includes a 45-day lock while Lender A’s quote includes only a 30-day lock, and your contract closing date is 42 days away. That makes the comparison even more important. The cheaper quote may not be cheaper if it requires an extension.

This is why comparing quotes is less about finding one magic number and more about understanding the full structure.

Questions to ask before choosing a lender

Once you have quotes in hand, ask direct questions before you commit.

- Is this quote based on my actual credit, income, property type, and loan amount?

- Does this rate include discount points?

- Are there lender credits, and what rate tradeoff creates them?

- What is included in the monthly payment estimate?

- What is the estimated cash to close?

- How long is the rate lock?

- What fees are controlled by the lender?

- Which costs are third-party estimates?

- What could cause this quote to change?

- How quickly can the loan move from application to closing?

The answers should be clear and consistent with the Loan Estimate. If the explanation is confusing, ask for a side-by-side comparison in writing.

The service side of comparing quotes

Rates and fees matter, but service matters too. A lender that communicates clearly, processes documents securely, and helps you solve issues early can make a major difference, especially in a competitive purchase market.

A very low quote may not help if the lender cannot meet your closing deadline, explain underwriting conditions, or support your real estate timeline. On the other hand, you should not overpay simply because a lender is friendly. The strongest choice usually combines competitive pricing, transparent terms, reliable execution, and guidance you trust.

This is where New Era Lending’s model is designed to help. Borrowers can use smart technology, secure document uploads, e-signature support, and personalized human guidance to compare mortgage options with more confidence. New Era Lending supports home purchase, refinance, and equity access solutions across 39 states, with specialized support for veterans and a focus on clear rates and terms.

Frequently Asked Questions

What is the best way to compare home loan lending rates? Compare quotes using the same loan amount, down payment, property type, loan program, lock period, and points structure. Then review the Loan Estimate for interest rate, APR, lender fees, credits, monthly payment, and cash to close.

Is the lowest mortgage rate always the best deal? Not always. A lower rate may require discount points or higher upfront costs. The better deal depends on your break-even period, how long you expect to keep the loan, your cash reserves, and your monthly budget.

What is more important, interest rate or APR? Both matter. The interest rate affects your monthly principal and interest payment. APR helps show certain financing costs over time. You should also compare cash to close, lender fees, points, and the full monthly payment.

Can mortgage quotes change after I receive them? Yes. Quotes can change if market rates move, your credit or loan details change, the property information changes, or the rate is not locked. Once locked, the rate is generally protected for the lock period as long as the loan still matches the lock terms.

How many mortgage quotes should I get? Many borrowers compare two or three personalized quotes. Request them within a short timeframe so market movement does not distort the comparison.

Compare your mortgage quotes with confidence

Home loan lending rates are important, but the best mortgage decision comes from comparing the whole offer: rate, APR, points, fees, credits, lock terms, monthly payment, and cash to close.

If you want help reviewing your options, New Era Lending can walk you through personalized mortgage scenarios and explain the tradeoffs in plain English. Whether you are buying a home, refinancing, or accessing equity, you can compare options with smart tools and human guidance built around your goals.

Start by reviewing your numbers, gathering consistent quotes, and asking the right questions. A clearer comparison today can help you choose a mortgage with more confidence tomorrow.