.jpg)

.jpg)

.jpg)

Veterans Loan Programs Beyond the Basic VA Loan

Most eligible service members and veterans first hear about the VA home loan as a 0% down purchase option. That benefit is powerful, but it is not the whole picture. Veterans loan programs can also help you refinance, access equity, adapt a home for disability needs, buy on tribal trust land, or choose a non-VA loan when the numbers make more sense.

The key is not asking, which veteran loan is best? The better question is, which program fits your service eligibility, property, timeline, cash position, and long-term plan?

This guide explains the options beyond the basic VA purchase loan, including specialized VA programs, grants, state assistance, refinance paths, and conventional alternatives that veterans should compare before making a decision.

What Beyond the Basic VA Loan Really Means

A standard VA purchase loan is often used to buy a primary residence with no required down payment, no monthly private mortgage insurance, and flexible underwriting for eligible borrowers. The U.S. Department of Veterans Affairs does not usually lend the money directly for this type of loan. Instead, it guarantees a portion of the loan made by an approved private lender, which can reduce lender risk and improve access for eligible borrowers.

But veteran financing does not stop at a traditional purchase mortgage. The broader category includes VA-backed refinance loans, direct VA programs for specific communities, grants for disabled veterans, state and local housing benefits, and non-VA mortgages that may better match certain goals.

For example, a veteran buying a move-in-ready primary residence may be well served by a standard VA loan. A veteran who already owns a home may need a VA cash-out refinance, a HELOC, or a home equity loan instead. A Native American veteran buying on federal trust land may need the Native American Direct Loan. A veteran with a qualifying service-connected disability may be eligible for housing adaptation grants that are not mortgages at all.

Specialized VA Programs Many Veterans Overlook

The VA purchase loan gets most of the attention, but several VA-related programs can be just as important depending on your situation. Some are widely available through VA-approved lenders, while others have more specific eligibility or lender participation requirements.

VA Interest Rate Reduction Refinance Loan

The VA Interest Rate Reduction Refinance Loan, commonly called an IRRRL or VA streamline refinance, is designed for borrowers who already have a VA-backed mortgage. Its main purpose is to help eligible homeowners lower their rate, reduce their payment, or move from an adjustable-rate mortgage to a fixed-rate loan.

An IRRRL may require less documentation than a full refinance, but it is not automatic. You still need to meet program and lender requirements, and the refinance must generally provide a tangible benefit. It is also not the right tool if your goal is to pull significant cash from home equity.

If you already have a VA loan and are monitoring refinance opportunities in 2026, compare the interest rate, APR, closing costs, funding fee, and break-even point. New Era Lending covers this in more detail in its guide to VA refinance rates.

VA Cash-Out Refinance

A VA cash-out refinance can help eligible veterans refinance an existing mortgage and access home equity. Unlike the IRRRL, this is a full refinance with more complete underwriting, income review, credit review, and typically an appraisal.

This option may be worth evaluating if you want to consolidate higher-interest debt, fund major home improvements, pay for education, or create liquidity for a specific plan. It can also be used in some cases to refinance a non-VA loan into a VA loan.

The caution is that a cash-out refinance replaces your current mortgage. If your existing rate is low, refinancing the entire balance into a new loan may be expensive even if the cash is useful. Compare it against a HELOC or home equity loan before deciding.

VA Energy Efficient Mortgage Add-On

Some VA borrowers may be able to finance eligible energy-efficient improvements as part of a VA loan when program and lender requirements are met. This may include improvements intended to reduce utility costs or improve home efficiency.

This is not a blank check for renovations. The work must meet applicable guidelines, and lenders may differ in how they handle these scenarios. If energy upgrades are part of your purchase or refinance plan, bring them up early so your loan officer can confirm whether the option is available and practical.

VA Renovation and Repair Options

A basic VA purchase loan is usually easiest when the home already meets VA Minimum Property Requirements. If the property needs repairs, financing can become more complicated.

VA renovation or alteration and repair financing may be possible in certain cases, but availability varies by lender and the project must be carefully documented. Contractors, bids, appraisals, timelines, and inspection requirements can all affect the process.

For a veteran trying to buy a home that needs work, it is wise to compare multiple paths. A VA renovation option may fit, but FHA 203(k), conventional renovation financing, a seller repair agreement, or choosing a different property may be more practical.

Native American Direct Loan

The Native American Direct Loan, or NADL, is a VA direct loan program for eligible Native American veterans and certain spouses. It can be used to buy, build, or improve a home on federal trust land, or to refinance an existing NADL.

This is different from a standard VA-backed loan because the VA is the lender. It also requires that the tribal government or relevant authority have a memorandum of understanding with the VA. You can review official details on the VA page for the Native American Direct Loan program.

For eligible borrowers, this can be one of the most important veterans loan programs available, especially when trust land creates financing challenges that traditional lenders may not be equipped to solve.

VA Housing Grants That Are Not Traditional Loans

Some of the most valuable housing benefits for veterans are not mortgages. They are grants, which means they may not need to be repaid if you meet the rules.

The VA offers housing grant programs for veterans and service members with qualifying service-connected disabilities. These may help with building, buying, or adapting a home to support independent living. The primary programs include Specially Adapted Housing, Special Home Adaptation, and Temporary Residence Adaptation grants.

These grants are highly specific, and eligibility depends on disability status and the type of adaptation needed. They can sometimes work alongside a mortgage strategy, but they should be reviewed early because timing, documentation, and property plans matter. The VA provides official information on disability housing grants.

If you may qualify, do not treat the grant as an afterthought. It can change what type of property you target, how you budget for accessibility improvements, and how much mortgage financing you actually need.

State, Local, and Nonprofit Veteran Housing Programs

Many veterans focus only on federal VA benefits and miss state or local assistance. Depending on where you live, there may be veteran-focused down payment assistance, closing cost help, property tax relief, bond programs, or grants through housing finance agencies and nonprofit organizations.

These programs are not uniform. Some are limited to first-time buyers. Some require income limits, homebuyer education, purchase price caps, or specific loan programs. Others may be available to repeat buyers or disabled veterans.

Common forms of assistance include:

- Down payment grants or forgivable second mortgages

- Deferred-payment assistance for closing costs

- Reduced-rate mortgage programs through state housing agencies

- Property tax exemptions for qualifying disabled veterans

- Local nonprofit grants tied to military service or first-time homeownership

The important step is to check these benefits before you finalize your loan structure. Assistance programs may affect your cash to close, rate, underwriting timeline, or choice of first mortgage.

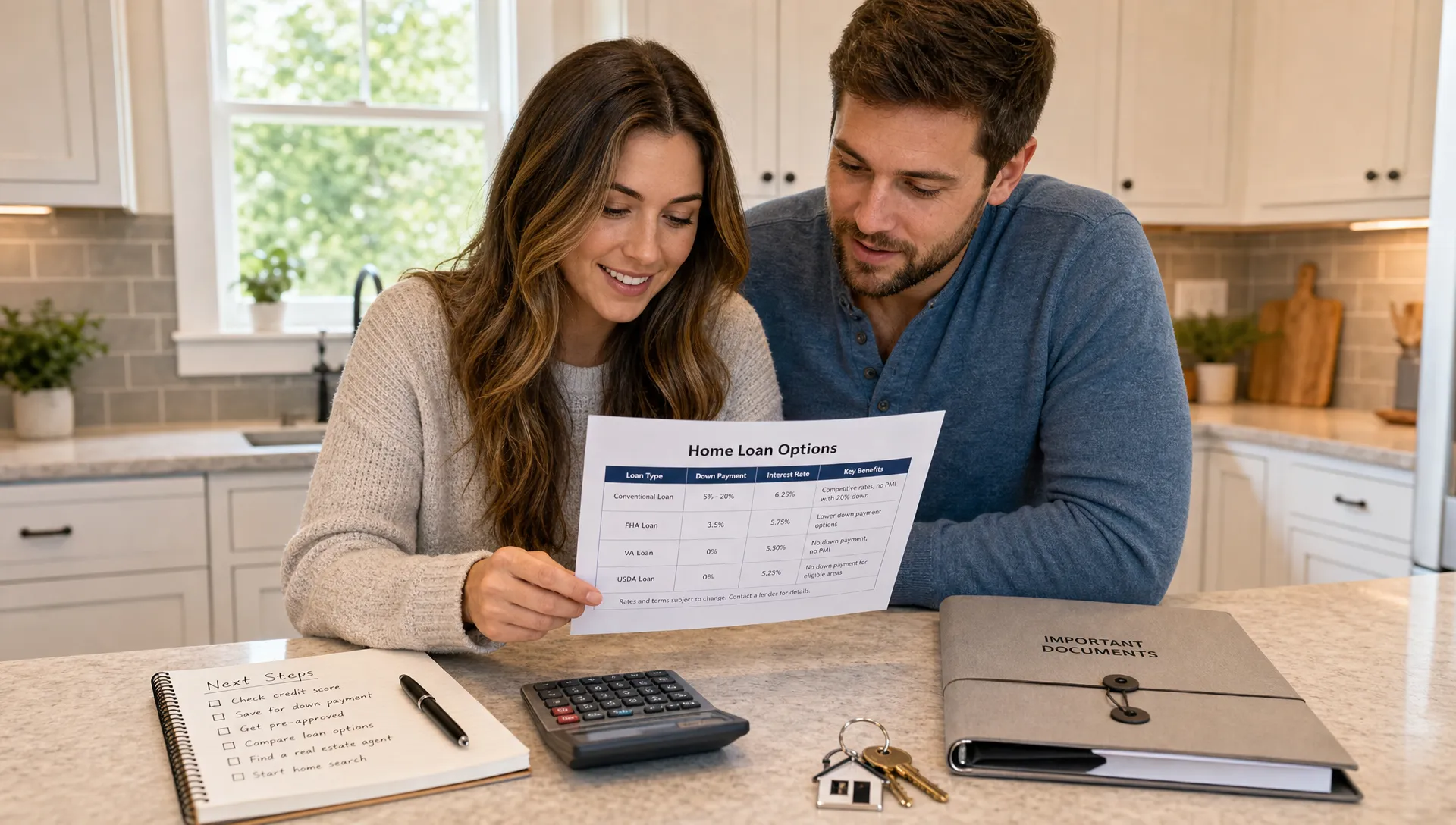

Non-VA Loans Veterans Should Still Compare

A VA loan is often a strong option, but it is not automatically the best answer in every scenario. Veterans should compare VA financing against conventional, FHA, USDA, jumbo, and equity-based options when their situation calls for it.

Conventional Loans

A conventional mortgage can be useful for veterans with strong credit, sufficient down payment or equity, and a desire to avoid the VA funding fee. It may also be the better fit for second homes, investment properties, or certain condos that do not work well with VA guidelines.

Conventional loans may require private mortgage insurance when the down payment is below 20%, but that insurance can often be removed later if requirements are met. VA loans do not have monthly PMI, but they may include a funding fee unless the borrower is exempt. That tradeoff should be modeled, not guessed.

FHA Loans

FHA loans are not veteran-specific, but they can help borrowers with lower credit scores or limited savings. They may be useful if a veteran does not have VA eligibility, has entitlement complications, or is buying a property where FHA is easier to execute.

The tradeoff is mortgage insurance. FHA loans typically include upfront and annual mortgage insurance premiums, and the long-term cost can be higher than a VA loan for many eligible veterans. Still, FHA can be a legitimate backup strategy.

USDA Loans

For eligible rural and suburban properties, USDA loans may allow no down payment for borrowers who meet income and location requirements. Veterans buying outside major metro areas should not ignore this option.

USDA loans are property-location and income dependent, so they are not as broadly available as VA or conventional financing. However, they can be useful when the property qualifies and the borrower wants to preserve cash.

Jumbo and Portfolio Loans

Veterans buying higher-priced homes may need to compare VA jumbo options with conventional jumbo or portfolio loans. This is especially true in high-cost markets or for borrowers with complex income.

A VA loan can still be competitive for eligible borrowers, but jumbo pricing, down payment strategy, reserve requirements, and funding fee treatment can change the final comparison. A side-by-side review is essential.

HELOCs and Home Equity Loans

For veterans who already own a home, a refinance is not always the best way to access equity. A HELOC or home equity loan may let you borrow against your home while keeping your existing first mortgage intact.

This can be attractive if your current mortgage rate is much lower than today’s rates. The tradeoff is that HELOCs often have variable rates, and home equity loans add a second monthly payment. Compare the full repayment plan before using home equity for any purpose.

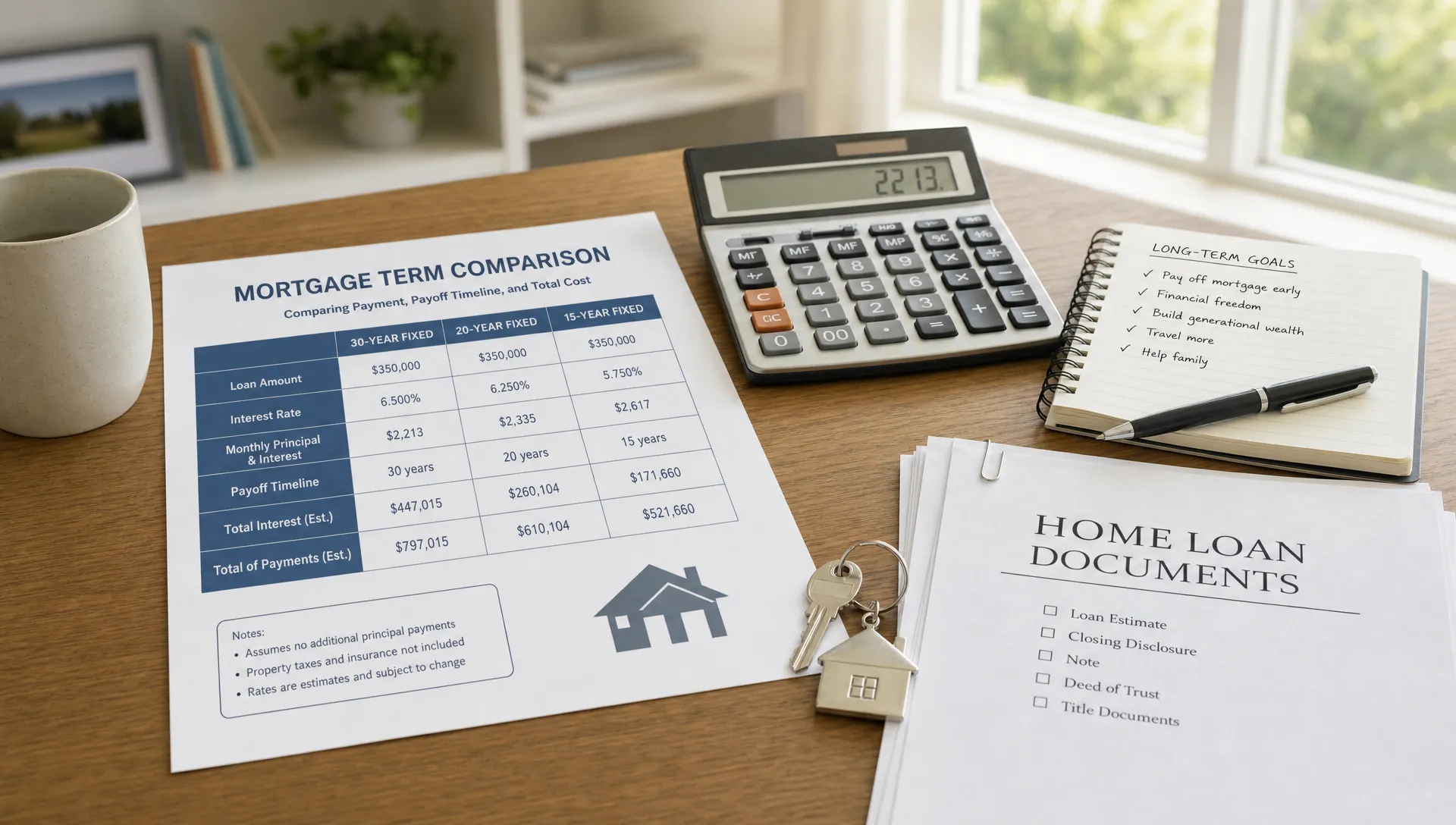

How to Compare Veterans Loan Programs the Smart Way

The right program is the one that fits your full financial picture, not just the one with the lowest advertised rate. When comparing veteran loan programs, focus on the numbers that affect real life.

Start with total cash to close. A VA loan may allow no down payment, but closing costs, prepaid taxes, insurance, escrows, inspections, and the funding fee still matter. State assistance, seller credits, or lender credits may reduce upfront cash, but each can affect the structure of the deal.

Next, compare the full monthly payment. Principal and interest are only part of the payment. Taxes, homeowners insurance, HOA dues, mortgage insurance, and escrow changes can alter affordability.

Then review long-term cost. A lower payment may come from a longer term or higher upfront fees. A lower interest rate may require discount points. A no-cost refinance may simply move costs into the rate. Your Loan Estimate is the best tool for comparing these tradeoffs.

Finally, consider execution risk. VA loans have property standards and appraisal requirements. Down payment assistance can add approval steps. Renovation loans can require contractor documentation. In a competitive purchase market, speed and certainty can matter almost as much as rate.

A strong comparison should answer these questions:

- Which option has the lowest realistic cash to close?

- Which option has the most comfortable full monthly payment?

- Which option is most likely to close on time for this property?

- How long do you expect to keep the home or loan?

- Are you paying a funding fee, mortgage insurance, discount points, or second-lien costs?

- What happens if you refinance, sell, rent the home later, or need to access equity?

Match the Program to the Veteran’s Real-World Goal

Different goals call for different financing strategies. Here are common scenarios where looking beyond the basic VA loan can help.

You are buying your first home with limited cash

A standard VA purchase loan may be the strongest starting point because it can reduce the down payment barrier and avoid monthly PMI. Still, you should check state veteran assistance, seller credit options, and closing cost strategies before you write an offer.

You have a service-connected disability

Confirm whether you are exempt from the VA funding fee, and explore housing grants if accessibility modifications are needed. A funding fee exemption can meaningfully change the VA versus conventional comparison. Official funding fee rules are available through the VA’s funding fee and closing cost guidance.

You already have a VA loan and want a lower payment

An IRRRL may be worth reviewing if market conditions have improved or if you want to move from an adjustable rate to a fixed rate. Do not focus only on the rate. Look at APR, closing costs, escrow changes, and how long it takes to break even.

You want to renovate or buy a fixer-upper

Ask about VA renovation availability, but also compare FHA 203(k), conventional renovation loans, seller-funded repairs, or buying a home that already meets required standards. The best choice may depend on contractor readiness and appraisal risk.

You want to access home equity

Compare a VA cash-out refinance against a HELOC, home equity loan, or conventional cash-out refinance. If your current mortgage has a favorable rate, replacing the entire loan may not be the cheapest way to borrow.

You are buying outside a major metro area

If the home is in an eligible location and your income fits the rules, USDA financing may be worth comparing. Veterans sometimes overlook USDA because they assume VA is the only low-down-payment path.

Do Not Skip the Human Network Around the Loan

Veteran home financing often works best when the right people are involved early: a loan officer who understands VA guidelines, a real estate agent who knows how to structure VA offers, an insurance professional, an inspector, and sometimes a veteran service officer or housing counselor.

Trusted referrals can help you find that team, especially through military communities, local veteran organizations, and homeowners who have recently used VA financing. In the business world, tools like AI-powered referral intelligence show how valuable warm introductions can be when people need trusted professionals. The same principle applies to home buying, but every referral should still be backed by licensing, transparent terms, and a Loan Estimate you can compare.

The best team will not simply tell you that VA is good or conventional is faster. They will explain how each option affects your offer, approval, cash to close, monthly payment, and future flexibility.

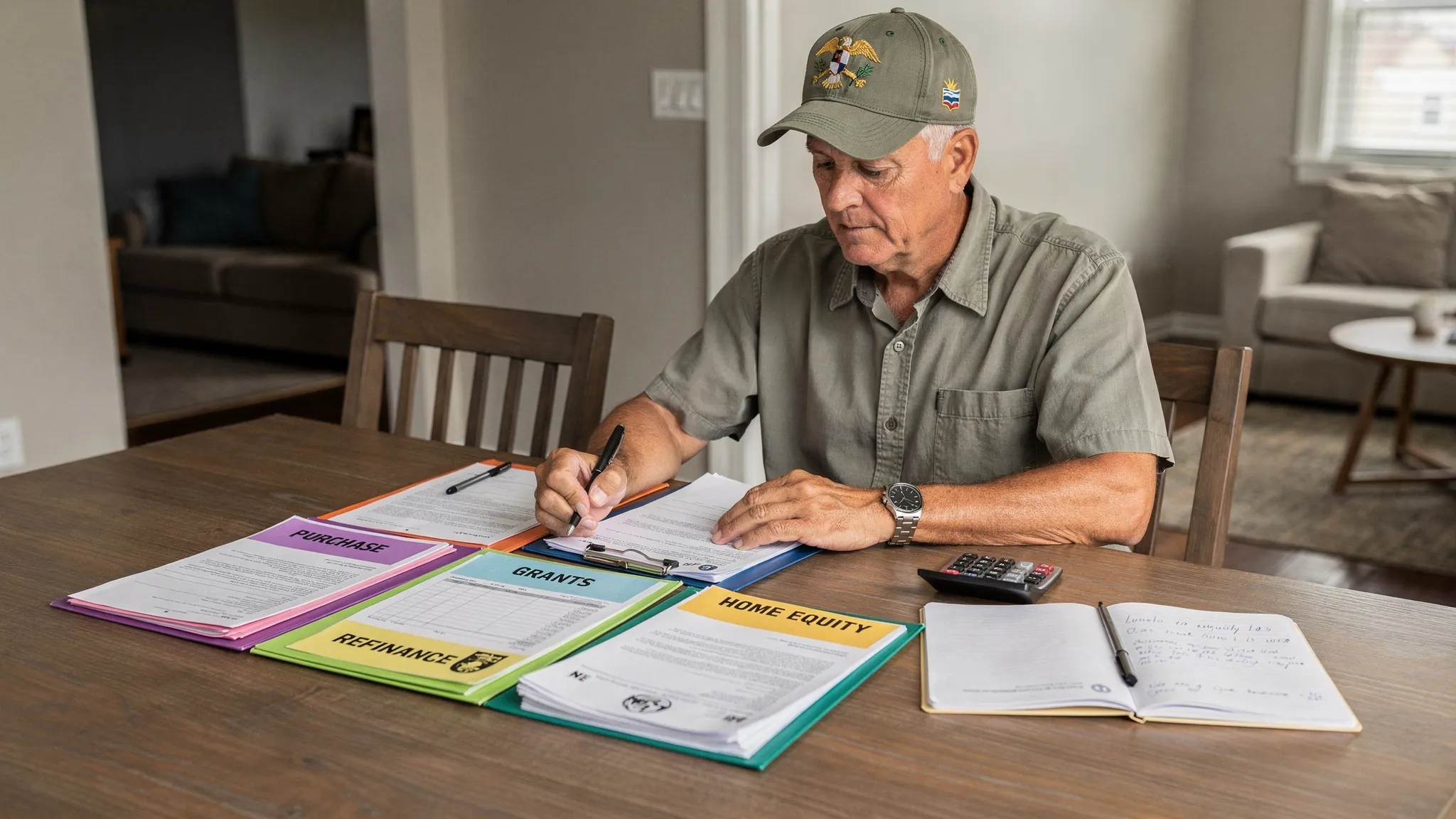

Documents to Gather Before You Compare Programs

You do not need every document on day one, but getting organized early can prevent delays. Veterans should be ready to provide service, income, asset, credit, and property information.

Helpful documents may include:

- Certificate of Eligibility or information needed to request it

- DD Form 214, statement of service, or applicable service records

- Recent pay stubs, W-2s, tax returns, retirement income, or disability income documentation

- Bank statements and proof of funds for closing

- Photo ID and basic personal information

- Current mortgage statement if refinancing or accessing equity

- Disability award documentation if requesting a funding fee exemption review

- Contractor bids or repair details for renovation scenarios

For a deeper preparation checklist, see New Era Lending’s guide to veterans mortgage loan documents.

Common Mistakes Veterans Should Avoid

The first mistake is assuming the VA loan is always cheapest. It often is, but the funding fee, property type, loan size, ownership timeline, and competing loan offers can change the result.

The second mistake is ignoring grants and local assistance. These benefits can reduce cash pressure, but they may require extra steps and should be built into the plan early.

The third mistake is choosing a property before checking program rules. VA, FHA, USDA, condo, manufactured home, and renovation guidelines can all affect approval. A beautiful home is not enough if the loan program cannot support it.

The fourth mistake is comparing rates without comparing APR, points, credits, fees, and lock terms. Two lenders can quote the same rate with very different upfront costs.

The fifth mistake is waiting too long to involve a lender. Pre-approval is not just paperwork. It helps you understand your buying power, identify issues early, and choose the right loan path before you are under contract.

Frequently Asked Questions

Are veterans loan programs only for buying a home? No. Veteran-focused programs can support purchases, refinances, cash-out equity access, home adaptations, and in some cases construction or improvements. Some benefits are mortgages, while others are grants or local assistance programs.

Is a VA loan always better than a conventional loan? Not always. VA loans are often highly competitive for eligible borrowers, especially because they do not require monthly PMI. However, a conventional loan may be better for certain high-equity borrowers, second homes, investment properties, or cases where avoiding the VA funding fee changes the math.

Can I use a VA loan more than once? Yes, VA entitlement can often be reused if eligibility and entitlement requirements are met. Some veterans may even have remaining entitlement while still owning another property. The exact answer depends on your prior VA loan use and current entitlement.

What is the difference between an IRRRL and a VA cash-out refinance? An IRRRL is generally for refinancing an existing VA loan to improve the rate or terms, usually with a more streamlined process. A VA cash-out refinance is a full refinance that may allow equity access and can sometimes refinance a non-VA loan into a VA loan.

Can veteran grants be combined with a mortgage? Sometimes. Housing grants, down payment assistance, and tax benefits may work alongside a mortgage, but each program has its own rules. Confirm eligibility, timing, and documentation before assuming funds can be used.

Do all lenders offer every VA or veteran-focused program? No. Lender participation varies, especially for renovation loans, certain assistance programs, manufactured homes, construction scenarios, or specialized products. Ask early which programs the lender can actually originate.

Compare Your Veteran Loan Options With New Era Lending

Veterans deserve more than a one-size-fits-all mortgage answer. The right financing path may be a standard VA loan, an IRRRL, a VA cash-out refinance, a state assistance program, a conventional loan, or a combination of benefits that lowers your total cost.

New Era Lending helps eligible veterans compare options with smart technology, secure document uploads, e-signature support, transparent rates and terms, and personalized human guidance. With mortgage solutions available across 39 states, the goal is to make the process clearer, faster, and easier to understand.

If you are exploring veterans loan programs for a purchase, refinance, or equity strategy, start with a personalized review. Visit New Era Lending to discuss your goals and compare the loan paths that fit your service, home, and budget.