.jpg)

.jpg)

.jpg)

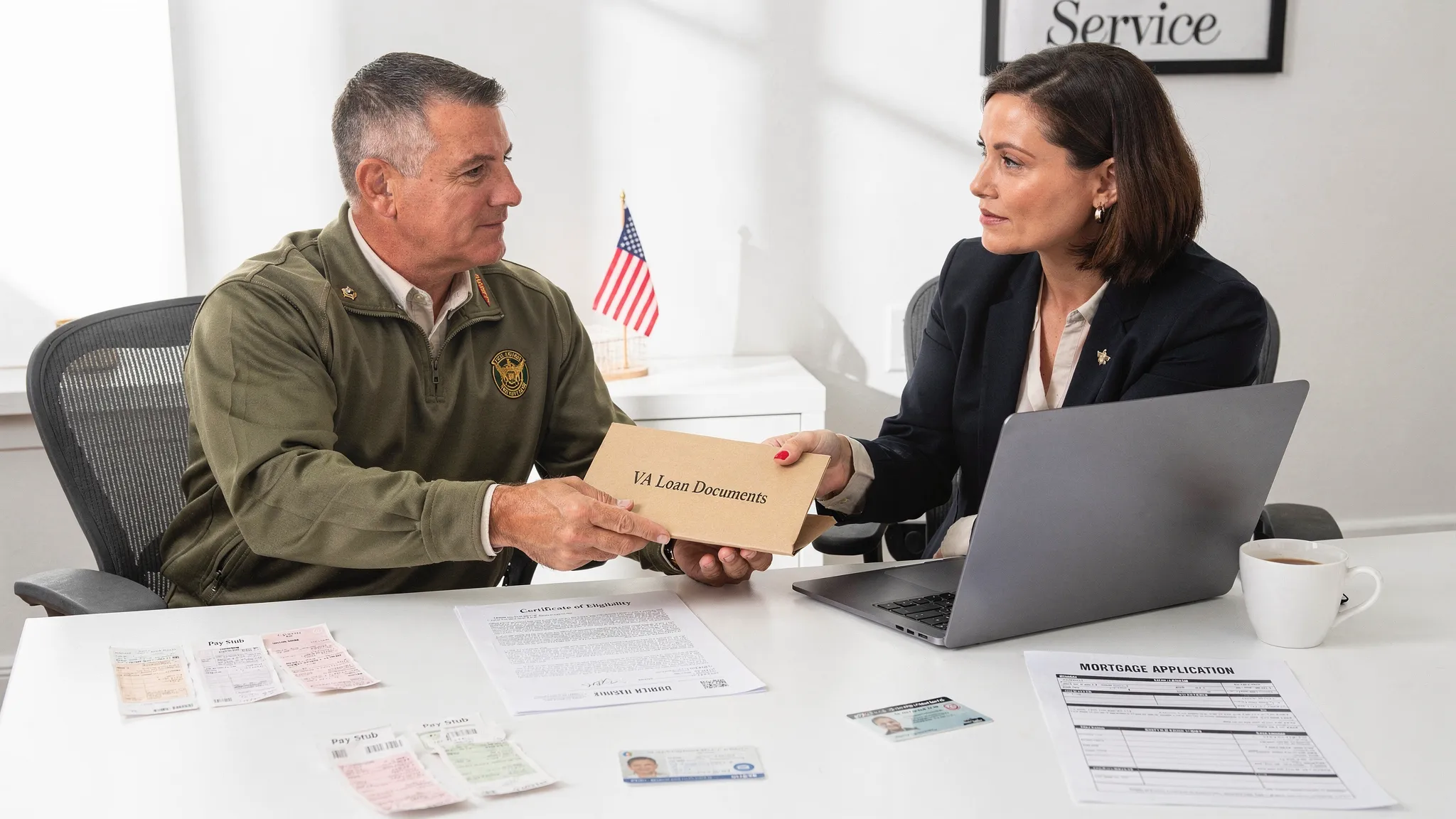

Veterans Mortgage Loans: Documents You’ll Need to Qualify

Getting a mortgage can feel like a paperwork test, especially when you are trying to use benefits you earned through service. The good news is that veterans mortgage loans (including VA loans and other options available to veterans) tend to follow a predictable documentation trail. If you gather the right items upfront, you can usually move faster through pre-approval, underwriting, and closing, with fewer last-minute “conditions” popping up.

Below is a practical, lender-friendly breakdown of the documents you will typically need, why they matter, and how to avoid common delays.

First, a quick note on “veterans mortgage loans”

Many veterans use a VA home loan, but veteran borrowers can also qualify for conventional, FHA, USDA, and other programs depending on goals, property type, and eligibility. The documentation categories below are largely the same across programs.

VA loans do add a few service-specific items, mainly your Certificate of Eligibility (COE) and, if applicable, paperwork to confirm a VA funding fee exemption.

If you want to review the VA’s official overview of the process, start with the VA’s page on how to apply for a VA-backed home loan and request your COE: VA home loan application overview.

The document categories lenders look for (and what to gather)

Most mortgage document requests fit into six buckets:

- Service eligibility (VA specific)

- Identity and legal status

- Income and employment

- Assets and funds to close

- Debts and credit explanations

- Property and transaction paperwork

You do not always need every item in every bucket. Your exact list depends on whether you are buying vs refinancing, W-2 vs self-employed, active duty vs retired, and whether you have “special situations” like rental income, child support, or prior bankruptcy.

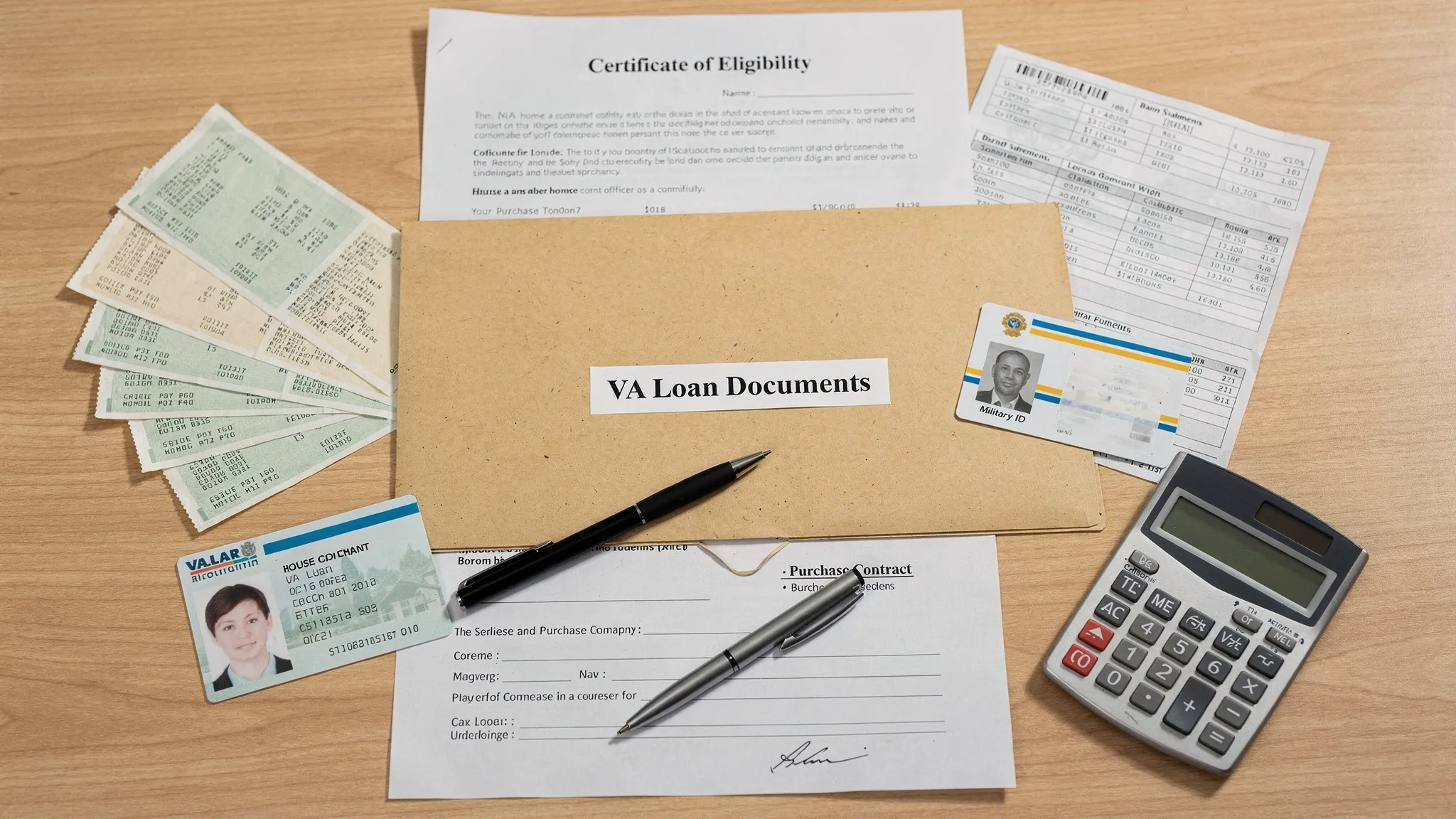

1) VA eligibility and service documents (VA loans)

If you are using a VA loan, this category is the big difference compared with other loan types.

Certificate of Eligibility (COE)

Your COE confirms to the lender that you meet VA service requirements and shows available entitlement. Many lenders can help obtain it electronically, but it is smart to be ready to provide supporting service documents if the system cannot instantly verify.

Proof of service (depending on your status)

Common examples include:

- Veterans: DD Form 214 (often the Member Copy)

- Active duty: Statement of Service (signed by your command) plus Leave and Earnings Statement (LES)

- National Guard or Reserves: NGB forms and/or points statements, plus evidence of qualifying service

- Surviving spouses (eligible cases): documentation supporting eligibility and benefit status

If you are not sure what applies to you, your loan officer can usually identify the minimum required items in minutes.

2) Identity and “life event” documents

Lenders must verify identity and ensure the file matches your legal name, obligations, and history.

Common requests include:

- Government-issued photo ID (driver’s license or passport)

- Social Security number verification (often just via the application and credit report, sometimes a card if needed)

- Proof of lawful residency, if applicable

And if your background includes any of the following, expect to provide supporting paperwork:

- Divorce decree, separation agreement, or child support order (especially if it affects qualifying income or monthly obligations)

- Marriage certificate or legal name change document (if your credit, ID, and pay documents do not match)

- Bankruptcy discharge and schedules (if you have a bankruptcy history)

- Foreclosure or short sale documentation (if applicable)

These are not “red flags” by themselves, but missing pages and missing signatures are common reasons underwriting has to re-request documents.

3) Income documents (the core of qualifying)

Underwriting is largely about answering one question: can you reasonably repay the loan? That is why income paperwork is usually the most detailed.

If you are W-2 (most borrowers)

Typically requested:

- Recent pay stubs (often covering the most recent 30 days)

- W-2s for the last 2 years

- Federal tax returns for the last 2 years (sometimes not required, but often requested if you have variable income, deductions that impact qualifying, or other complexities)

If you earn overtime, bonuses, commissions, or shift differentials, a lender may look for a history of receiving that income (often a two-year pattern) and confirmation it is likely to continue.

If you are active duty

You will commonly provide:

- Leave and Earnings Statement (LES)

- A Statement of Service (if needed)

- Documentation for housing allowances or special pay, if you want it considered

Some allowances can be used for qualifying if they are stable and properly documented. Your lender will calculate this under program rules.

If you are retired or receive fixed benefits

Common items:

- Award letter(s) for retirement income, disability income, or other recurring benefits

- Proof of receipt (bank statements showing deposits)

If you receive VA disability compensation and want to confirm a VA funding fee exemption, you may need a VA document showing disability status. The VA explains funding fees and exemptions here: VA funding fee and closing costs.

If you are self-employed or a 1099 contractor

Plan on more documentation because the lender must verify both income and business stability. Common requests include:

- Personal federal tax returns (often the last 2 years)

- Business tax returns (often the last 2 years, if applicable)

- Year-to-date profit and loss statement (and sometimes a balance sheet)

- Business bank statements (sometimes requested to support cash flow)

- K-1s (if you are in an S-corp or partnership)

Practical tip: if your income is tied to contracts, invoices, or production cycles, keep records organized by month. For example, a veteran launching a consumer brand may work with an apparel development and manufacturing partner to produce inventory, those invoices and contracts can help clarify revenue timing when underwriting asks about large deposits or business expenses.

4) Asset documents (how you will fund the purchase and reserves)

Even with a VA loan (often associated with low or no down payment), lenders still verify that you can cover cash-to-close and that your funds are sourced properly.

Expect requests such as:

- Bank statements (commonly the most recent 2 months for checking and savings)

- Retirement account statements (if you plan to use them for reserves or funds)

- Documentation for any large deposits (a common underwriting condition)

Gift funds (if applicable)

If a family member is helping, you will likely need:

- A gift letter (lender will provide the template)

- Evidence the donor had the funds and transferred them

- Evidence you received the funds

Earnest money

If you wrote an earnest money check or wire, lenders typically want to see:

- Proof the funds cleared your account

- A copy of the check or wire confirmation

Avoid sending screenshots unless your lender confirms they are acceptable. Underwriting often needs full statements with your name, account number (usually partially masked), and all pages.

5) Debts, credit, and explanation letters (yes, they matter)

Your credit report will show most monthly liabilities, but underwriters may ask for clarification.

Common examples:

- Letters of explanation for recent credit inquiries

- Documentation for disputed accounts (some disputes must be removed before closing)

- Student loan documentation if repayment terms are unclear

- Proof of payoff if you are paying off a loan to qualify

If you have had recent job changes, gaps in employment, or irregular income, expect a brief written explanation. A clean, honest, one-paragraph explanation can prevent a week of back-and-forth.

6) Property and transaction documents

Your lender also has to verify the details of the home and transaction, not just your finances.

For a home purchase

Common items include:

- Fully executed purchase agreement (all pages and addenda)

- Contact information for your real estate agents (both sides)

- Homeowners insurance quote and agent contact (often required before closing)

- If applicable, HOA documentation (especially for condos and planned communities)

Your lender will typically order the appraisal and coordinate title work, but you may be asked to review or sign disclosures promptly.

For a refinance

You may be asked for:

- Current mortgage statement

- Current homeowners insurance declarations page

- Property tax information (sometimes collected through escrow documents)

If you are doing a VA streamline refinance (IRRRL), documentation can be lighter, but exact requirements still vary by lender and file complexity.

VA-specific “nice to have” documents that prevent delays

Even if they are not required on day one, these items often become important later.

Funding fee exemption documentation

Some veterans are exempt from the VA funding fee. If you think you qualify, ask early what proof is needed so it does not become a last-minute condition.

Disability income paperwork (if used for qualifying)

If disability compensation is part of your qualifying income, be ready with the award letter and proof of receipt.

Prior VA loan information (if you have used the benefit before)

If you have an existing VA loan or you have used entitlement in the past, your lender may need details to confirm remaining entitlement and how it will be applied.

Common document mistakes that slow veterans down

Most delays are avoidable. The biggest issues are not “bad numbers,” they are missing or unclear documentation.

- Uploading partial statements (underwriting often needs every page, even blank ones)

- Unexplained large deposits (prepare to show where the money came from)

- Out-of-date pay stubs or expired IDs

- Blurry photos where names, dates, or account numbers cannot be read

- Big changes during the process (opening new credit, switching jobs, moving money between accounts without a paper trail)

If you are planning a purchase, try to keep your finances steady until after closing.

A simple way to get organized before pre-approval

You will usually move fastest if you assemble a “starter packet” that covers eligibility, income, and assets. If you want a practical starting point, gather:

- Photo ID

- COE (or DD-214 / Statement of Service so your lender can help obtain COE)

- Pay stubs or LES

- W-2s (last 2 years)

- Bank statements (last 2 months)

From there, your loan officer can tailor the remaining document requests to your scenario.

How New Era Lending supports a smoother document process

Document collection should not feel like guesswork. New Era Lending’s approach combines smart technology with real human guidance, which is especially helpful for veteran borrowers who want clarity and speed. Based on the services described by New Era Lending, you can expect support such as:

- Secure document uploads

- E-signature support

- Transparent rates and terms

- Guidance from a loan professional who can explain what is needed and why

If you want to reduce surprises, ask for a document checklist customized to your specific profile (active duty, retired, self-employed, using a VA loan vs another program, and buying vs refinancing). That one step can shave days off your timeline.

For more context on using VA benefits strategically, you can also read New Era Lending’s veteran-focused guide: How Veterans Can Optimize Every Benefit They’ve Earned.

When you are ready, the best next step is a pre-approval conversation that confirms which program fits and exactly which documents you will need to qualify, before you fall in love with a house.