.jpg)

.jpg)

.jpg)

How to Apply for a Mortgage Loan in 2026

Applying for a mortgage in 2026 can feel faster than it used to, but it is not automatic. Digital applications, secure uploads, and e-signatures have made the process more convenient. Still, lenders must verify your credit, income, assets, debts, property details, and ability to repay before they can issue a final approval.

The best way to apply for a mortgage loan is to treat the application as a decision process, not just a form. You are choosing a loan structure, proving your financial readiness, comparing official disclosures, and coordinating a property review, all while keeping your home purchase or refinance timeline on track.

This guide walks through the mortgage application process in 2026, step by step, so you know what to prepare, what lenders look for, and how to avoid the most common delays.

Before You Apply: Understand What Counts as a Mortgage Application

A mortgage application is more formal than a quick online quote. You may start with a pre-qualification, which is often based on self-reported information, or a pre-approval, where the lender may review credit and documents more closely. A full mortgage application typically begins once you provide key details about yourself, your income, the loan amount, and the property.

In many cases, once a lender has enough required information, federal rules require the lender to provide a Loan Estimate within three business days. The Consumer Financial Protection Bureau explains the Loan Estimate as a standardized form that helps borrowers compare loan terms, projected payments, and closing costs.

That means your application is not just about getting a yes or no. It starts a regulated process with deadlines, disclosures, document requests, and underwriting steps. Knowing that upfront helps you respond quickly and make better comparisons.

Step 1: Define Your Mortgage Goal

Before you apply, get clear on what you want the loan to accomplish. A first-time buyer, move-up buyer, homeowner refinancing for a lower payment, and borrower using home equity all have different priorities. Your goal affects the loan type, documentation, timeline, and cash needed to close.

For a home purchase, focus on your target price range, down payment, monthly payment comfort zone, and expected closing timeline. For a refinance, clarify whether you want a lower rate, shorter term, debt consolidation, cash-out funds, or a more stable loan structure. For an investment property, consider rental income assumptions, maintenance costs, reserves, and property management expenses.

If you are buying a rental property in Northeast Florida, for example, reviewing local leasing support such as property management in Jacksonville and St. Augustine can help you estimate operating costs and rental logistics before you finalize your loan strategy.

If you are still comparing programs, New Era Lending has a helpful guide to home loan options for 2026 that explains what to consider before choosing a mortgage path.

Step 2: Check Your Credit, Income, Debts, and Cash to Close

Lenders look at your full financial picture. Credit score matters, but it is only one part of the application. Your income stability, debt-to-income ratio, assets, down payment, and documentation quality can all affect approval and pricing.

Start by reviewing your credit reports for errors, late payments, high balances, or unfamiliar accounts. If you find something inaccurate, address it before applying when possible. Also avoid making major credit changes right before or during the application, such as financing a vehicle, opening new cards, or increasing balances.

Next, calculate your recurring debts. This may include credit cards, auto loans, student loans, personal loans, alimony, child support, and other obligations. Lenders compare those debts with your qualifying income to estimate whether the proposed mortgage payment is sustainable.

Finally, confirm your cash to close. Your down payment is not the only upfront cost. You may also need funds for closing costs, prepaid taxes, homeowners insurance, escrow deposits, appraisal fees, inspections, and reserves. For a deeper look at what lenders review, see New Era Lending's guide to mortgage loan requirements for 2026 applications.

Step 3: Gather Documents Before You Start

One of the easiest ways to speed up your mortgage application is to gather documents early. Missing or incomplete paperwork is a common reason applications slow down.

Most borrowers should be ready to provide:

- Government-issued identification and Social Security number

- Recent pay stubs, W-2s, 1099s, or other income records

- Federal tax returns, especially for self-employed income, rental income, or complex compensation

- Recent bank, retirement, and investment account statements

- Documentation for large deposits, gift funds, or asset transfers

- Current mortgage statements if refinancing or keeping another property

- Purchase contract once you are under contract on a home

- Homeowners insurance information before closing

Self-employed borrowers often need extra documentation because income may fluctuate or include business deductions. Be prepared for profit and loss statements, business bank statements, K-1s, or additional tax schedules if they apply to your situation.

The goal is not to upload every financial document you have. It is to provide what the lender needs in a clear, complete, and secure way. A lender that offers secure document uploads can make this part of the process easier and safer.

Step 4: Choose the Right Loan Type

You do not need to become a mortgage expert before you apply, but you should understand the major categories. Common options include conventional loans, FHA loans, VA loans, USDA loans, jumbo loans, fixed-rate mortgages, adjustable-rate mortgages, and refinance or cash-out refinance loans.

The right fit depends on your credit profile, down payment, military service history, property location, income, occupancy, and tolerance for payment changes. For example, a borrower with strong credit and a larger down payment may compare conventional options. A qualified veteran may want to evaluate VA benefits. A buyer with limited down payment funds may need to look at programs with more flexible upfront cash requirements.

This is where personalized guidance matters. The lowest advertised rate is not automatically the best loan if the closing costs, points, mortgage insurance, or payment structure do not match your goals. If you want a broader explanation of the process from application to closing, New Era Lending's guide to how a home mortgage loan works from start to close is a useful companion resource.

Step 5: Submit the Mortgage Application

Once you have a goal, documents, and a likely loan direction, it is time to apply. A mortgage application usually asks for personal information, employment history, income, assets, liabilities, property details, declarations, and permission to verify information.

Be accurate and consistent. If your legal name, address history, employment dates, or income details differ across documents, it may create extra questions. That does not mean you will be denied, but it can slow the file while the lender reconciles the differences.

In 2026, many borrowers expect a digital application experience. That can be a real advantage when it is paired with human support. Technology helps with speed, uploads, e-signatures, and organization. A knowledgeable mortgage professional helps interpret guidelines, explain tradeoffs, and guide you through conditions.

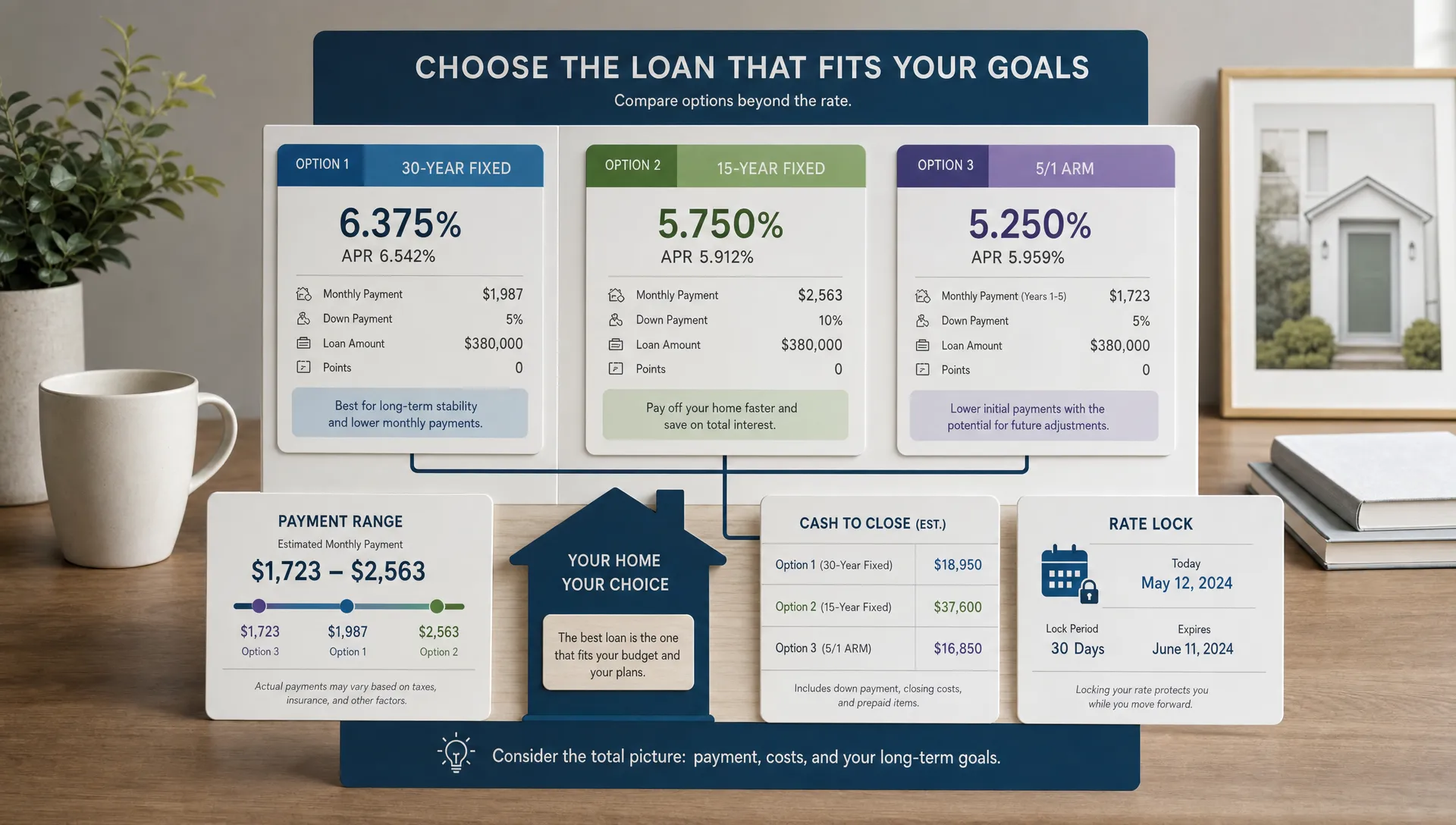

Step 6: Review and Compare Your Loan Estimate

After you apply, review your Loan Estimate carefully. This is one of the most important documents in the mortgage process because it gives you a structured way to compare offers.

Do not look only at the interest rate. Review the annual percentage rate, monthly principal and interest, estimated taxes and insurance, mortgage insurance if applicable, points, lender credits, origination charges, third-party costs, and total cash to close.

Pay close attention to whether the rate is locked. If it is not locked, the rate and costs may change with market conditions. If it is locked, ask how long the lock lasts and whether it covers your expected closing date.

Also compare the loan purpose and structure. A lower payment may come from a longer loan term, upfront points, an adjustable rate, or escrow assumptions. Make sure the offer fits your real goals, not just the lowest first-month number.

Step 7: Move Through Processing and Underwriting

Once you choose a loan offer and move forward, your file usually enters processing. A processor organizes your documentation, verifies details, orders required services, and prepares the file for underwriting.

Underwriting is where the lender evaluates whether the loan meets program guidelines and investor requirements. The underwriter may issue a conditional approval, which means the loan appears approvable if specific conditions are satisfied.

Conditions are normal. They may ask for an updated bank statement, a letter explaining a large deposit, proof a debt was paid, clarification on employment, or an updated insurance binder. Respond quickly and provide exactly what is requested. Sending partial information can create more follow-up.

The key is to keep your financial life steady while the loan is under review. Continue paying bills on time. Avoid new debt. Do not move large sums of money between accounts without a clear paper trail. If your income, employment, or purchase terms change, tell your lender right away.

Step 8: Complete the Property Review

For a purchase loan, the property matters almost as much as the borrower. The lender needs to confirm that the home supports the loan amount and meets program requirements. This often includes an appraisal, title review, hazard insurance verification, and sometimes flood certification or additional inspections depending on the property and loan type.

An appraisal is not the same as a home inspection. The appraisal is primarily for the lender and evaluates value and certain property conditions. A home inspection is for the buyer and focuses on the condition of systems, structure, and potential repairs. Many buyers choose an inspection even when it is not required by the lender.

For condos, the lender may also review the condominium project, insurance coverage, budget, litigation status, or owner-occupancy details. For refinances, the lender may use a full appraisal, desktop review, property data report, or automated valuation process depending on the loan and eligibility.

Step 9: Prepare for Final Approval and Closing

As closing approaches, the lender clears final conditions and prepares closing documents. You will receive a Closing Disclosure that outlines the final loan terms, projected payment, closing costs, and cash needed to close. The CFPB notes that borrowers generally must receive the Closing Disclosure at least three business days before closing.

Compare the Closing Disclosure with your most recent Loan Estimate. Some changes are expected, such as prepaid interest based on the actual closing date. Other changes should be reviewed carefully, especially if loan terms, cash to close, or fees differ from what you expected.

Before closing, confirm how to send funds. Wire fraud remains a serious risk in real estate transactions, so always verify wiring instructions through a trusted phone number before sending money. Do not rely only on email instructions.

At closing, you will sign loan and property documents. For a purchase, ownership usually transfers after documents are signed, funds are received, and the transaction is recorded according to local practice. For many primary residence refinances, a three-business-day right of rescission may apply before the loan funds.

Common Mistakes to Avoid When You Apply

Many mortgage problems are preventable. The application process goes more smoothly when you avoid surprises and communicate early.

Common mistakes include:

- Applying before you know your realistic monthly payment comfort zone

- Comparing only interest rates instead of full Loan Estimates

- Making large undocumented deposits into your bank account

- Opening new credit or increasing credit card balances during underwriting

- Changing jobs, pay structure, or employment status without discussing it first

- Waiting too long to provide requested documents

- Assuming pre-approval means the property is automatically approved

A strong mortgage application is not about perfection. It is about clarity, documentation, and consistency. If something unusual appears in your file, such as a job gap, bonus-heavy income, gift funds, or recent credit event, explain it early so your lender can guide you.

How Long Does It Take to Apply for a Mortgage Loan in 2026?

The application itself can often be completed quickly, especially with a digital process. The full timeline depends on your readiness, the property, loan program, appraisal timing, title work, and how fast conditions are cleared.

A well-prepared borrower may move from application to approval faster than someone who starts without documents or has unresolved credit, income, or asset questions. Purchase timelines are also influenced by the contract closing date and local market conditions. Refinances may depend more on valuation, payoff information, and title review.

If speed matters, ask your lender what could delay your specific file. The answer may be different for a salaried borrower buying a single-family home than for a self-employed borrower purchasing a condo or a homeowner requesting cash-out funds.

How New Era Lending Helps Simplify the Application

New Era Lending offers technology-driven, personalized mortgage solutions for home purchases, refinancing, and equity access. The goal is to combine modern tools with expert human guidance, so borrowers can move through the process with more clarity and confidence.

That combination is important in 2026. Borrowers want secure document uploads, efficient communication, e-signature support where available, transparent rates and terms, and educational resources. But they also need a person who can explain options, answer questions, and help align the mortgage with the bigger financial picture.

New Era Lending serves borrowers across 39 states and offers a wide range of loan options, including specialized veteran loan programs. If you are preparing to apply, working with a team that blends smart technology and personal guidance can help you avoid confusion and stay organized from application to closing.

Frequently Asked Questions

What do I need to apply for a mortgage loan in 2026? Most borrowers need identification, income documents, asset statements, debt information, credit authorization, and property details if a home has been selected. Self-employed borrowers, investors, and borrowers using gift funds may need additional documentation.

Can I apply for a mortgage before I find a house? Yes. Many buyers apply for pre-approval before shopping so they understand their budget and can make stronger offers. A full property review happens after you have a specific home under contract.

Does applying for a mortgage affect my credit score? A lender usually pulls your credit when you apply or seek pre-approval, and that inquiry may affect your score. Many scoring models treat multiple mortgage inquiries within a limited shopping window as one inquiry, but the exact impact depends on your credit profile and scoring model.

Should I compare mortgage offers from more than one lender? Comparing offers can help you evaluate rates, fees, points, lender credits, and closing costs. Use official Loan Estimates when possible because they present key terms in a standardized format.

What happens after I submit my mortgage application? The lender reviews your file, provides disclosures, verifies documents, orders property-related services, sends the loan to underwriting, clears conditions, issues final approval, and prepares closing documents.

Can I apply if I am self-employed? Yes, but be prepared for more documentation. Lenders may review tax returns, business income trends, deductions, profit and loss statements, and bank statements to determine qualifying income.

Ready to Apply With More Confidence?

Applying for a mortgage loan in 2026 does not have to feel overwhelming. When you prepare your documents, understand your loan options, compare disclosures carefully, and work with the right guidance, the process becomes much more manageable.

If you are planning to buy, refinance, or access home equity, New Era Lending can help you explore personalized mortgage solutions supported by smart technology and human guidance.