.jpg)

.jpg)

.jpg)

Home Loan Options for 2026: What to Consider Before You Apply

If you plan to buy a home or refinance this year, you have more home loan options than most people realize. The hard part in 2026 is not finding a loan product, it is choosing the one that fits your timeline, cash-to-close, risk tolerance, and long-term plan.

This guide focuses on what to consider before you apply, so you can walk into pre-approval prepared, compare offers correctly, and avoid surprises late in underwriting.

Step 1: Get clear on your goal (because it changes the “best” loan)

Before you compare rates, decide what success looks like:

- Buying a primary home: The priority is usually approval strength, predictable payment, and cash-to-close.

- Refinancing to lower payment or change term: Break-even time and total cost matter as much as rate.

- Accessing equity (cash-out, home equity loan, HELOC): Your priority is often liquidity and payment flexibility.

If you are still comparing purchase vs refinance decisions, you will get better pricing discussions once your lender can run side-by-side scenarios based on the same assumptions.

Step 2: In 2026, think “payment strategy,” not just interest rate

Mortgage rates can move quickly, and the best option is often the one that keeps your payment stable across different outcomes. Before applying, choose a strategy you can defend.

Fixed-rate mortgage

A fixed-rate loan is straightforward: your principal and interest payment stays the same over the term.

Fixed tends to fit borrowers who:

- Want payment stability

- Plan to keep the home for a long time

- Do not want to depend on refinancing later

Adjustable-rate mortgage (ARM)

An ARM can lower the initial rate for a period, then adjust based on the loan’s terms.

An ARM tends to fit borrowers who:

- Expect to sell or refinance before the first adjustment

- Have high income visibility and can handle payment changes

- Want a lower starting payment and understand the caps and worst-case payment

If you are considering an ARM, ask for the fully indexed and worst-case payment scenario, not just the teaser period.

Temporary buydowns and discount points

Buydowns and points can reduce your rate, but they only “win” if the math works for your timeline.

Before you apply, be ready to answer:

- Who is paying for the buydown or points (you or the seller)?

- How long do you expect to keep the loan?

- What is your break-even point versus taking a higher rate with lower fees?

For a deeper explanation of these structures, see New Era Lending’s guide on fixed vs ARM vs buydowns.

Step 3: Know the underwriting “big levers” that shape your options

Most borrowers think approval is primarily about income and credit score. In practice, lenders look at a combination of factors that can expand or shrink your options.

Credit profile (score is not the whole story)

Your credit score matters, but so do:

- Recent late payments or collections

- Credit utilization (how much of your available credit you are using)

- New accounts opened before applying

If you are within a few months of applying, focus on stability. Big changes can cause re-underwriting and delays.

Debt-to-income ratio (DTI)

DTI helps determine what payment level is reasonable. Before you apply, review recurring monthly obligations such as auto loans, student loans, credit card minimums, and other installment debt.

A practical pre-application move is to avoid taking on new monthly payments until after closing.

Cash-to-close (down payment is only one piece)

Your total cash needs often include:

- Down payment

- Closing costs

- Prepaid items (like homeowners insurance and property taxes, depending on escrow)

- Reserves (extra funds in the bank that some programs require)

If you want a quick refresher on closing cost expectations, New Era Lending breaks it down here: Closing Costs: The Fees Nobody Tells You About.

Property type and occupancy

Some loan programs and pricing depend heavily on what you are buying:

- Primary residence vs second home vs investment property

- Condo vs single-family vs 2–4 unit

- Condition and appraisal requirements

If you are shopping condos or multi-unit properties, it is smart to mention that early, because your “home loan options” can narrow based on eligibility rules.

Step 4: Match yourself to the right home loan options (high level)

You do not need to memorize every program, but you should know which bucket you likely fall into so your application is targeted.

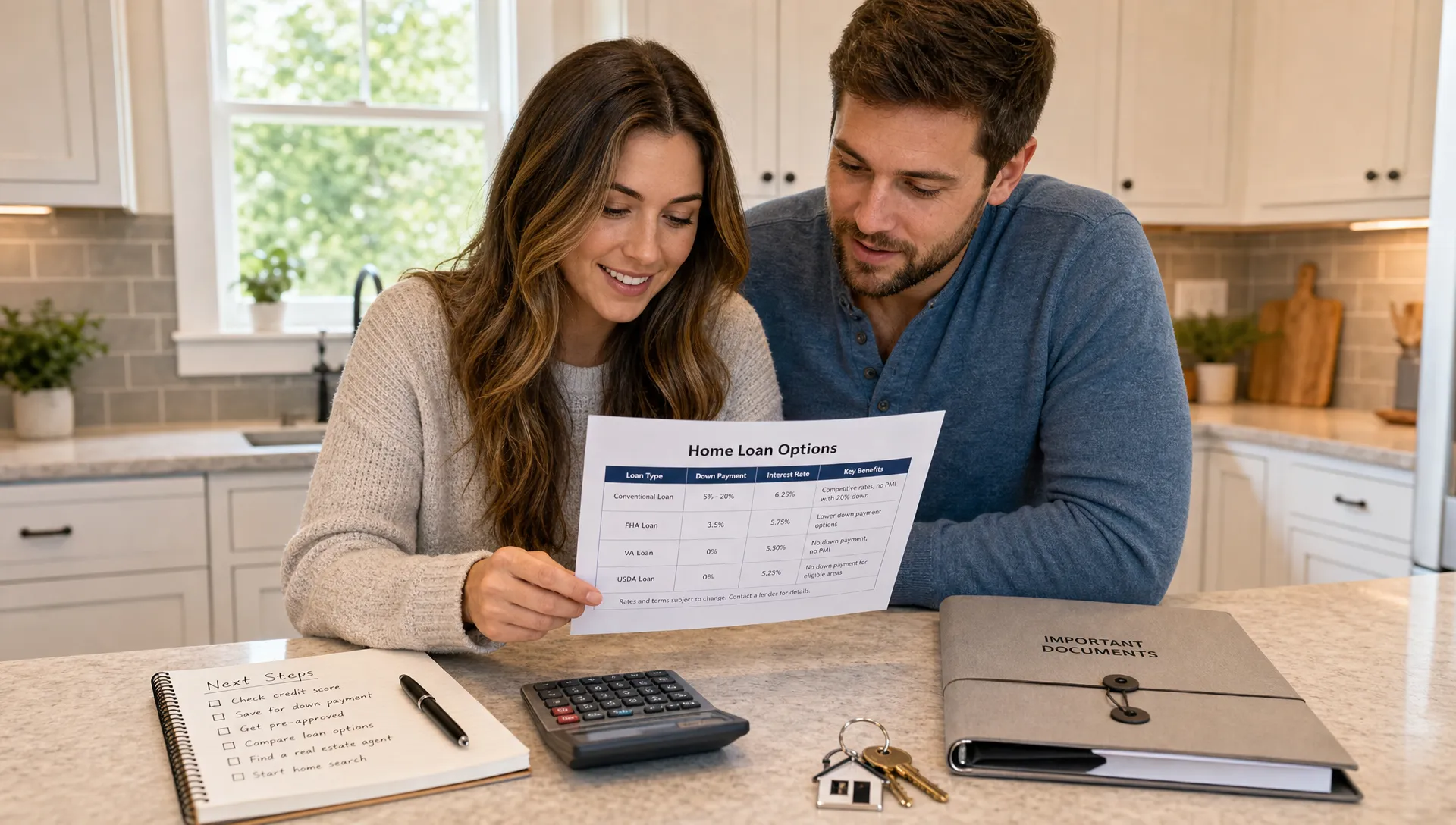

Common home loan options in 2026 include:

- Conventional loans: Often a strong fit for borrowers with solid credit and stable income.

- FHA loans: Often helpful for lower down payments and more flexible credit guidelines, with mortgage insurance considerations.

- VA loans: A major benefit for eligible veterans and service members, often with $0 down options and no monthly PMI.

- USDA loans: Can be a $0 down option for eligible rural areas and qualified borrowers.

- Jumbo loans: For loan amounts above conforming limits, often with stricter underwriting.

- Non-QM / portfolio options: For borrowers who do not fit standard documentation or income patterns.

- Renovation / construction loans: Useful when buying a property that needs work, or building.

If you want a program-by-program explainer, start with New Era Lending’s overview: Mortgage Loan Programs: Compare FHA, VA, Conventional and More.

Step 5: Prepare like an underwriter (so your approval is faster and cleaner)

The easiest way to reduce stress is to assume everything will be verified and document it upfront.

Pre-application document checklist

Most borrowers should gather:

- Last 2 years W-2s (or 1099s if applicable)

- Recent pay stubs (most recent 30 days is common)

- Last 2 years tax returns (often needed for self-employed, variable income, or complex scenarios)

- 2–3 months bank statements for accounts used for funds to close

- Photo ID

- A list of monthly debts not shown clearly on credit (child support, alimony, private loans)

Two practical tips that prevent delays:

- Avoid unexplained large deposits right before applying. If it happens, keep a paper trail.

- Keep your funds-to-close in accounts that are easy to document.

Step 6: Compare lenders using the right tool (Loan Estimate, not marketing)

When you have real offers in hand, compare them using the Loan Estimate. The Consumer Financial Protection Bureau provides a helpful explainer of the form and what each section means: the Loan Estimate and Closing Disclosure resources.

When comparing, pay attention to:

- Rate vs APR: APR attempts to reflect the cost of the loan including certain fees.

- Discount points and lender credits: Lower rate often means higher upfront cost.

- Mortgage insurance details: How much, and under what conditions it can be removed.

- Lock terms: How long is your rate locked, and what happens if closing is delayed?

Also remember that averages are not your rate. Public surveys can help you understand the broader rate environment, but your pricing depends on your profile. For context on market averages, see Freddie Mac’s Primary Mortgage Market Survey.

Step 7: Ask better questions before you hit “submit”

A strong loan officer will happily run scenarios. Before you apply, ask questions that reveal whether you are getting real guidance or just a quote.

Consider asking:

- “Can you show me the payment for a higher rate scenario, so I know my comfort zone?”

- “What is the cash-to-close estimate, and what could make it change?”

- “If I choose an ARM, what is the worst-case payment and when could it happen?”

- “What documentation tends to slow underwriting for borrowers like me?”

Service quality matters because mortgages are communication-heavy. Some teams invest in structured training to improve clarity and objection handling, including tools like AI roleplay training with Scenario IQ to help professionals practice high-stakes conversations.

Frequently Asked Questions

What are the best home loan options for 2026? The best option depends on your credit, down payment, property type, and timeline. Conventional, FHA, VA, and USDA remain the most common starting points, with jumbo and non-QM for specific cases.

Should I choose a fixed-rate mortgage or an ARM in 2026? A fixed rate prioritizes payment stability. An ARM can reduce the initial rate, but you should understand caps and be comfortable with the worst-case payment if rates rise.

How much money should I have saved before applying? Plan for down payment plus closing costs (often discussed as 2–5% of the loan amount in many transactions) plus a buffer for reserves and moving or repair costs.

Will shopping lenders hurt my credit? Multiple mortgage credit checks made in a short window are generally treated as one inquiry for scoring purposes, but timing rules vary by model. Ask your lender about the best way to shop within a focused period.

What’s the biggest mistake people make before applying? Choosing a loan based on a headline rate without comparing total cost, cash-to-close, and payment risk under realistic scenarios.

Ready to compare your home loan options with a clear plan?

New Era Lending helps buyers and homeowners evaluate home loan options with a tech-forward process and real human guidance. If you want a clean pre-approval, transparent scenarios, and a smoother path from application to closing, start here: New Era Lending.