.jpg)

.jpg)

.jpg)

Home Lending Explained for Today’s Buyers

For many buyers, home lending feels complicated because it combines money, timing, credit, contracts, property rules, and market movement all at once. But the basic idea is simple: a lender provides funds to help you buy a home, and you agree to repay that money over time under specific terms.

What matters most is understanding the moving parts before you are under pressure to make decisions. The right loan is not always the one with the lowest advertised rate. It is the one that fits your budget, your timeline, your savings, your income, and your long-term plans for the home.

Today’s buyers also have more tools than previous generations. Digital applications, secure uploads, e-signatures, faster approvals, and better educational resources can make the process more transparent. Still, technology does not replace good guidance. A smart home lending experience should combine convenience with a real person who can explain tradeoffs in plain English.

What home lending really means

Home lending is the process of borrowing money to buy, refinance, or access equity in residential real estate. For a buyer, it usually starts with a mortgage application and ends at closing, when the loan funds and ownership transfers.

A mortgage is different from most consumer loans because it is secured by the property. If the borrower does not repay the loan, the lender has legal rights tied to the home. That security is one reason mortgage rates are often lower than unsecured debt, but it also means the approval process is more detailed.

A lender is not just asking whether you can make the first payment. They are evaluating whether the loan makes sense over time, whether the home supports the loan amount, and whether the transaction meets program guidelines. That is why buyers are asked for income documents, asset statements, credit authorization, property details, and sometimes additional explanations.

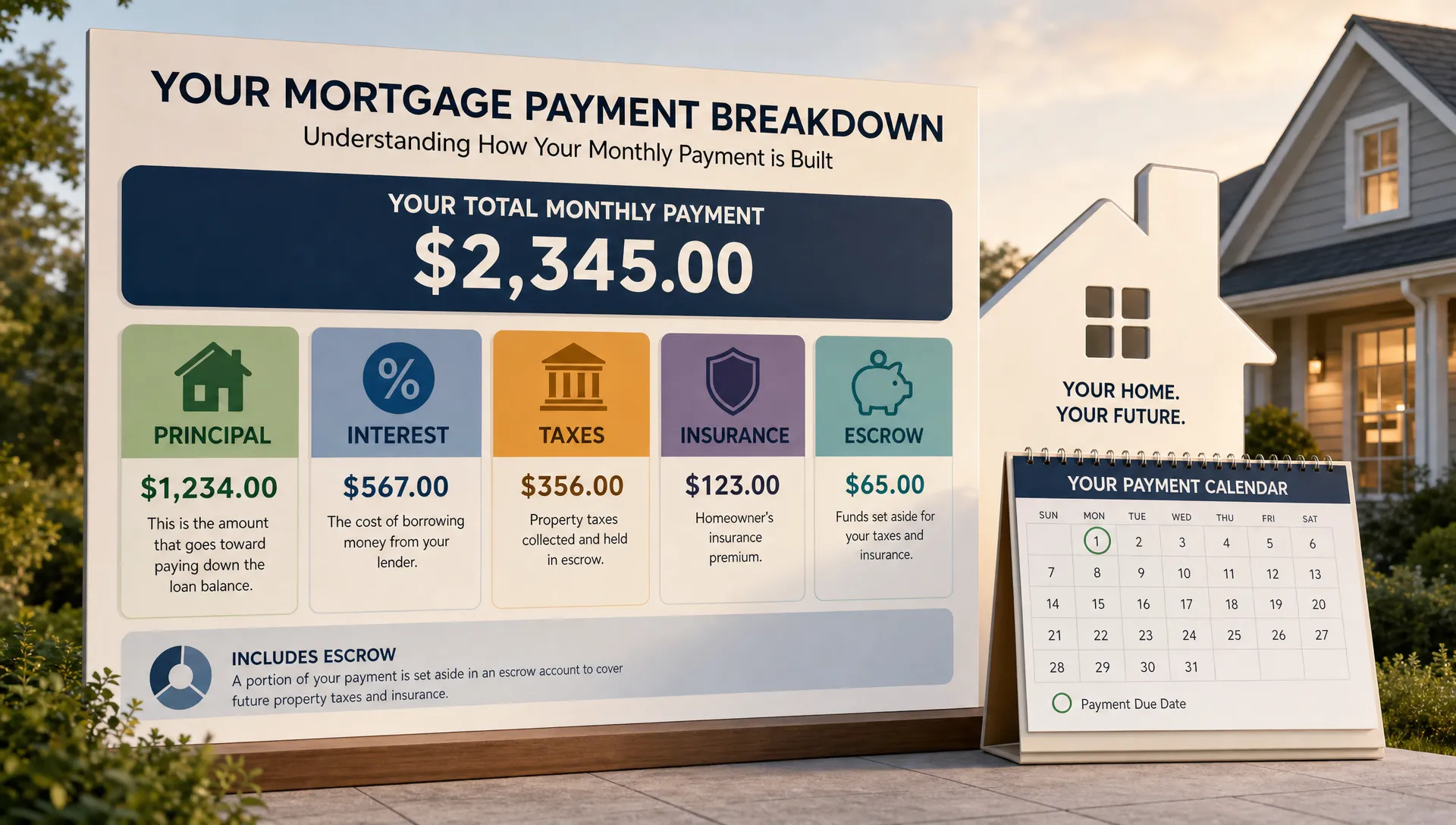

The core pieces of a home loan

Before comparing loan programs, it helps to know the major variables that shape your approval and monthly payment. These are the numbers that buyers should understand early, ideally before making an offer.

- Purchase price: The agreed-upon price of the home before credits, closing costs, or concessions are applied.

- Down payment: The amount you contribute upfront toward the purchase price, which affects your loan amount and sometimes mortgage insurance.

- Loan amount: The money you borrow from the lender after your down payment and any financed costs.

- Interest rate: The cost of borrowing expressed as a percentage, used to calculate your principal and interest payment.

- APR: A broader cost measure that includes the interest rate plus certain lender and loan costs.

- Loan term: The length of time used to repay the loan, commonly 15, 20, or 30 years.

- Cash to close: The total money needed at closing, including down payment, closing costs, prepaid taxes, insurance, and other required funds.

These numbers work together. A higher down payment may reduce the loan amount, but it may not always be the best move if it leaves you with too little cash after closing. A lower rate may look attractive, but it could come with discount points or fees that only make sense if you plan to stay in the home long enough.

If you are still getting comfortable with the vocabulary, New Era Lending’s guide to home loan basics every buyer should know is a helpful next step.

What lenders review before approval

A lender’s job is to determine whether the loan is likely to be repaid and whether it meets program requirements. That review is often called underwriting. While every buyer’s file is different, most approvals focus on five broad areas.

Credit history shows how you have handled past debt. Lenders often look at your credit score, payment history, balances, recent inquiries, and the types of accounts you have used. A few missed payments or high card balances do not automatically end the conversation, but they can affect eligibility, pricing, or documentation needs.

Income helps show whether the payment is sustainable. W-2 employees may provide pay stubs and tax forms, while self-employed buyers may need business returns, profit and loss statements, or additional year-to-date information. Stability matters, but so does the way income is documented.

Self-employed buyers and practice owners should be especially proactive. For example, a dentist, optometrist, chiropractor, or physician investing in growth through a healthcare practice marketing agency may see revenue rising while taxable income looks different because of business expenses. A lender will usually focus on documentable, qualifying income, not just gross receipts or projected growth.

Debt-to-income ratio, often called DTI, compares monthly debt obligations to qualifying monthly income. It can include housing payment, credit cards, auto loans, student loans, personal loans, and other recurring debts. DTI is not the only approval factor, but it is one of the most important affordability checks.

Assets show whether you have enough verified funds for closing and reserves. Lenders may review checking, savings, retirement accounts, gift funds, or proceeds from the sale of another property. Large deposits may need explanation because lenders must verify acceptable sources of funds.

The property is also part of the approval. An appraisal, property type, occupancy, title review, insurance, and any required repairs can all affect the transaction. Even a strong borrower can run into delays if the property has issues that must be resolved before closing.

Pre-qualification, pre-approval, and final approval

Buyers often hear these terms used interchangeably, but they are not the same.

Pre-qualification is usually an early estimate based on information you provide. It can be useful for planning, but it may not involve a full document review. Pre-approval is stronger because the lender typically reviews credit, income, assets, and other documentation before issuing a letter.

Final approval comes later, after the property is under contract and underwriting has reviewed the full loan file. Even then, the approval may come with conditions. Conditions are requests for missing documents, clarifications, updated statements, appraisal items, insurance evidence, or final verifications.

A strong pre-approval can help you shop with more confidence. It also helps your real estate agent understand your price range and structure offers that align with financing requirements. In competitive markets, sellers often take pre-approved buyers more seriously because the financing has already been reviewed at a deeper level.

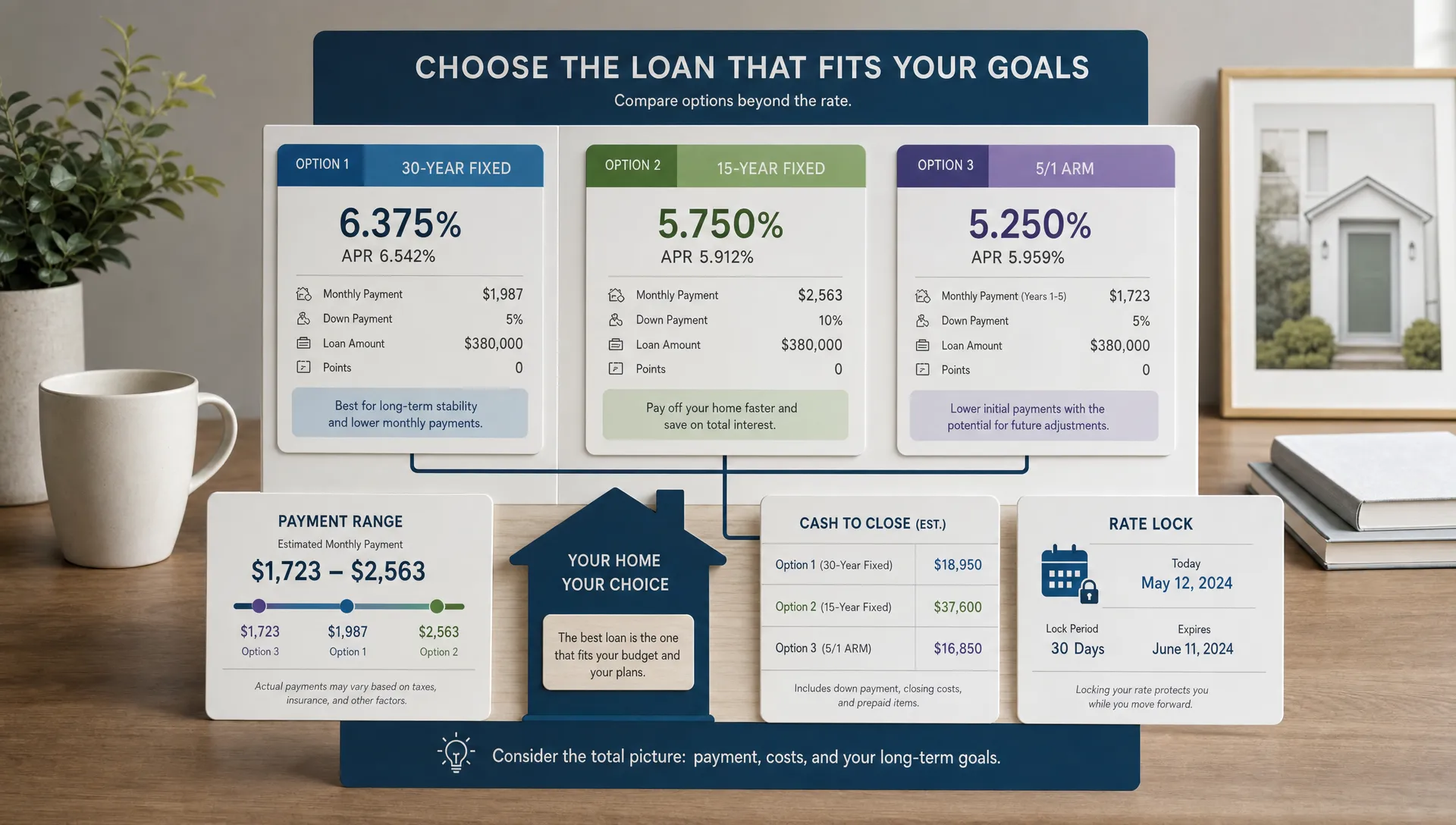

Choosing the right loan option

There is no universal best mortgage program. The right choice depends on your credit profile, down payment, military service, location, income type, property type, and financial goals.

Conventional loans are common for buyers with solid credit and stable income. They can work for first-time buyers and repeat buyers, and they may offer flexibility with property types and down payment levels. FHA loans may be helpful for buyers who need more flexible credit or down payment guidelines. VA loans can be powerful for eligible veterans, active-duty service members, and certain surviving spouses, often with favorable terms and no required down payment.

USDA loans may support eligible buyers in qualifying rural and suburban areas, while jumbo loans are designed for amounts above conforming loan limits. Some buyers may also explore renovation loans, construction loans, non-QM options, or portfolio products when their situation does not fit standard guidelines.

The key is not memorizing every program. The key is knowing what questions to ask. How much cash will you need? What is the estimated payment? Is mortgage insurance required? Are there property restrictions? How long do you plan to keep the home? How sensitive is your budget to rate movement?

For a broader overview, compare common mortgage loan options for different buyer situations before deciding which path fits you best.

How mortgage rates fit into home lending

Mortgage rates are important, but they are only one part of the decision. A rate is shaped by market conditions, lender pricing, loan program, credit profile, down payment, property type, occupancy, lock period, and whether you pay points.

That is why two buyers can receive different rate quotes on the same day. A buyer purchasing a primary residence with excellent credit and a larger down payment may see different pricing than a buyer with a smaller down payment, a different property type, or a longer lock period.

The Consumer Financial Protection Bureau recommends comparing Loan Estimates when shopping for a mortgage because they show key costs in a standardized format. This helps buyers look beyond the rate and evaluate lender fees, third-party costs, prepaid items, and total cash to close.

Rates also move with the broader bond market and investor demand for mortgage-backed securities. If you want a plain-English explanation, New Era Lending’s article on how home mortgage lending rates are set explains the pricing chain in more detail.

The home lending process from start to finish

While every transaction has its own timing, most purchase loans follow a similar path.

- Prepare your financial picture: Review credit, estimate your budget, gather income documents, and think through how much cash you want to use.

- Apply and get pre-approved: Submit your application, authorize credit, provide documents, and review your estimated price range and loan options.

- Shop for a home: Work with your real estate agent to find homes that fit your budget, needs, and financing structure.

- Make an offer: Once the seller accepts, the lender receives the contract and begins the property-specific loan process.

- Complete underwriting: The lender reviews your full file, orders or reviews the appraisal, verifies title and insurance, and clears conditions.

- Review closing documents: You receive final figures, confirm your cash to close, and sign required disclosures.

- Close and fund: You sign final documents, funds are disbursed, and the home purchase is completed.

The best way to reduce stress is to respond quickly to document requests and avoid major financial changes during the process. Do not open new credit, make large unexplained deposits, change jobs, or move money between accounts without first asking your lending team how it could affect your file.

Where smart technology helps buyers

Modern home lending should feel less like chasing paperwork and more like following a clear path. Secure document uploads can make it easier to provide pay stubs, bank statements, tax forms, and other required files. E-signature support can reduce delays when disclosures need to be reviewed quickly. Digital updates can help buyers understand what is done, what is pending, and what needs attention.

But technology is most valuable when it supports communication. A mortgage platform can collect documents, but it cannot always explain whether a buydown makes sense, whether to use gift funds, or how a job change might affect approval. That is where human guidance matters.

New Era Lending combines smart mortgage technology with personalized support across 39 states, helping buyers navigate purchase loans, refinancing, equity access, and specialized veteran loan programs. The goal is a process that feels efficient without becoming impersonal.

Common mistakes today’s buyers should avoid

Many lending issues are preventable. The earlier you understand potential pitfalls, the easier they are to avoid.

- Shopping homes before knowing your numbers: A beautiful listing can create pressure, but a pre-approval helps ground the search in reality.

- Focusing only on the rate: A lower rate may come with higher upfront costs, and the best choice depends on your break-even timeline.

- Underestimating cash to close: Buyers sometimes plan for the down payment but forget taxes, insurance, prepaid interest, title fees, and reserves.

- Making financial changes mid-process: New debt, job changes, large transfers, and unexplained deposits can create underwriting delays.

- Skipping questions: If you do not understand a fee, document request, or loan term, ask before moving forward.

A good lender should welcome questions. Clear explanations are not a bonus, they are part of a responsible lending experience.

What to do before you talk to a lender

You do not need to have everything perfect before starting a conversation. In fact, speaking with a lender early can help you build a better plan. Still, a little preparation goes a long way.

Start by checking your credit report for errors or outdated information. Review your monthly debts and estimate a payment range that feels comfortable, not just one that might be technically approved. Look at your savings and decide how much you want to keep after closing for emergencies, repairs, moving costs, and furniture.

Gather basic documents such as pay stubs, W-2s, tax returns if self-employed, bank statements, photo ID, and information about existing debts or properties. If you expect to use gift funds, sale proceeds, bonus income, overtime, commission, or business income, mention it early so the lender can explain what documentation may be needed.

Most importantly, be honest about your goals. A first-time buyer trying to minimize cash to close may need a different strategy than a move-up buyer focused on payment stability. A veteran buyer may want to explore VA benefits. A buyer expecting to relocate in a few years may evaluate costs differently than someone planning to stay for decades.

Frequently Asked Questions

What is home lending? Home lending is the process of borrowing money to buy, refinance, or access equity in a home. For buyers, it usually involves applying for a mortgage, getting approved, and closing on a property.

How early should I get pre-approved before buying a home? Many buyers benefit from getting pre-approved before they start touring homes seriously. This helps define a realistic price range and gives time to address credit, income, or cash-to-close questions.

Does the lowest mortgage rate always mean the best loan? Not always. A low rate can be valuable, but you also need to compare fees, points, APR, monthly payment, cash to close, and how long you expect to keep the loan.

Can I buy a home if I am self-employed? Yes, many self-employed buyers qualify for home loans. The key is documenting stable, eligible income through tax returns, business records, bank statements, or other documentation required by the loan program.

What should I avoid after applying for a mortgage? Avoid opening new credit, taking on new debt, making large unexplained deposits, changing jobs, or moving funds without guidance. These changes can affect underwriting and may delay closing.

Make home lending easier to understand

Home lending does not have to feel overwhelming. When you know what lenders review, how loan options differ, and which numbers matter most, you can make decisions with more confidence.

If you are preparing to buy, refinance, or explore your equity options, connect with New Era Lending for smart mortgage tools, transparent guidance, and personalized support designed to make the lending process simpler from the start.