.jpg)

.jpg)

.jpg)

Mortgage Refinance Options That Could Fit Your Goals

Refinancing can be a smart financial move, but only when the new loan solves a real problem or helps you reach a specific goal. A lower rate may be helpful, but it is not the only reason homeowners refinance. The right choice depends on what you want to change, how long you plan to keep the home, how much equity you have, and what the new loan costs.

That is why it helps to compare mortgage refinance options by goal instead of starting with a single question like, “What is today’s rate?” A refinance can lower your monthly payment, shorten your payoff timeline, access home equity, remove mortgage insurance, replace an adjustable-rate loan, or simplify your overall debt picture.

Below is a practical guide to the most common refinance paths and the goals they may fit.

Start With the Goal Before Choosing the Loan

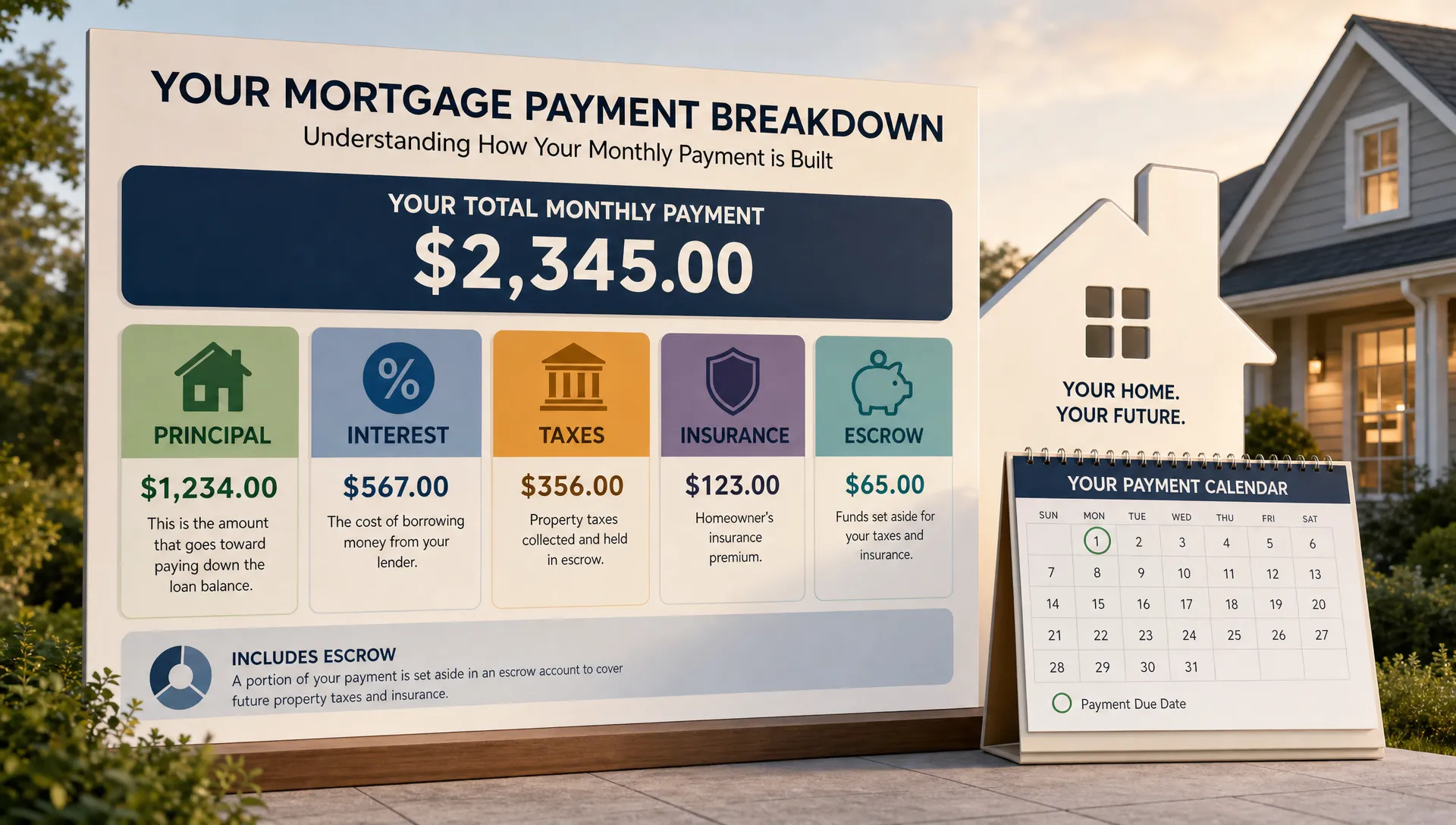

A refinance replaces your current mortgage with a new one. That new mortgage may have a different interest rate, loan term, loan type, balance, or monthly payment. In many cases, it also comes with closing costs, which can be paid upfront or rolled into the new loan if the program allows it.

Before comparing options, define the outcome you want. A refinance meant to free up monthly cash flow will look different from one designed to build equity faster. A homeowner planning to move in two years should evaluate costs differently from someone planning to stay for another decade.

The most common refinance goals include:

- Lowering the monthly mortgage payment

- Paying off the loan faster

- Accessing cash from home equity

- Removing mortgage insurance

- Switching from an adjustable rate to a fixed rate

- Changing from one loan type to another

- Consolidating higher-interest debt

- Financing home improvements

Once the goal is clear, you can compare the tradeoffs more effectively.

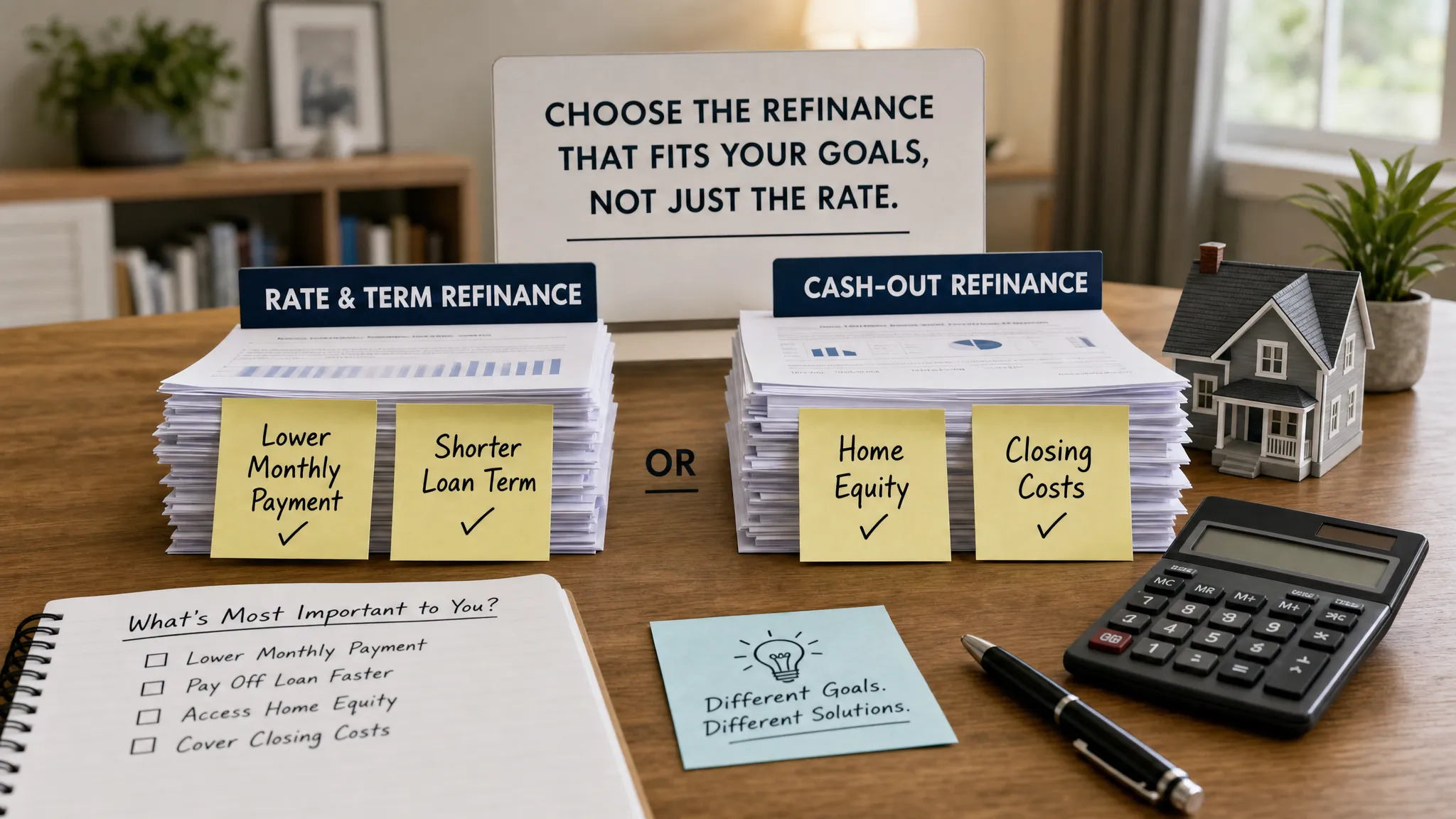

Rate-and-Term Refinance: For Lower Payments or a Better Loan Structure

A rate-and-term refinance is one of the most common mortgage refinance options. It changes the interest rate, loan term, or both, without taking significant cash out of the home.

This option may fit if your main goal is to reduce your monthly payment, move into a more stable loan, or improve the long-term cost of your mortgage. For example, a homeowner with a higher-rate loan may refinance into a lower-rate loan to reduce interest costs. Another homeowner may keep a similar rate but extend the loan term to lower the monthly payment.

The key is understanding what changes and what resets. If you refinance from a mortgage you have paid for 8 years into a new 30-year loan, your payment may fall, but the payoff clock starts over. That does not automatically make it a bad decision, especially if monthly cash flow is the priority, but it should be measured against total interest over time.

If your main question is whether a lower rate is enough to justify refinancing, New Era Lending has a deeper guide on how to decide if a new mortgage rate is good enough to refinance.

Shorter-Term Refinance: For Paying Off the Mortgage Faster

A shorter-term refinance, such as moving from a 30-year mortgage to a 20-year or 15-year mortgage, is usually designed for homeowners who want to pay less interest over the life of the loan and build equity faster.

This route can make sense when your income has increased, your financial obligations have decreased, or you are preparing for retirement and want the home paid off sooner. Shorter terms often come with lower interest rates than longer terms, although the monthly payment can be higher because the balance is repaid over fewer years.

This option is not just about the rate. It is about whether the higher payment fits comfortably into your budget. A shorter-term refinance can be powerful, but it should not leave you without emergency savings or force you to rely on credit cards for routine expenses.

If the payment feels too tight, you might compare a formal shorter-term refinance with another strategy: refinancing into a more favorable loan and making extra principal payments voluntarily. The second approach may offer more flexibility, but it requires discipline.

Cash-Out Refinance: For Using Home Equity Strategically

A cash-out refinance replaces your current mortgage with a larger new loan. The difference between the old payoff balance and the new loan amount is returned to you as cash, minus eligible costs and any required reserves.

This option may fit goals such as home improvements, debt consolidation, education expenses, or creating liquidity for a major life event. For example, if you have built substantial equity and want to renovate a kitchen, replace a roof, or add usable living space, a cash-out refinance may allow you to fund those improvements through your mortgage.

The tradeoff is that you are increasing your mortgage balance and using your home as collateral. If you use cash-out funds to pay off credit cards, the monthly savings may look attractive, but it is important to avoid rebuilding the same card balances afterward. If you plan to use home equity for investing, take time to understand risk and diversification. Independent financial education resources such as Greek Shares’ investing guides can help you think more carefully before putting borrowed funds into the market.

Your home value plays a major role here. Lenders look at equity and loan-to-value ratio when determining how much cash may be available and what terms you may qualify for. For more context, see how your home’s value impacts refinance options.

FHA Refinance Options: For Certain Current FHA Borrowers or Flexible Qualification Needs

FHA refinance options can be useful for homeowners who currently have an FHA loan or who need a refinance path with more flexible credit or equity requirements than some conventional programs.

One common FHA option is the FHA Streamline Refinance, which is designed for eligible homeowners who already have an FHA mortgage. It may involve less documentation than a full refinance and is generally focused on creating a tangible benefit, such as a lower payment or more stable loan terms. However, mortgage insurance rules still matter, and not every FHA borrower will save money by refinancing.

There are also FHA cash-out and FHA rate-and-term refinance options. These may fit certain borrowers, but it is important to compare them against conventional alternatives, especially if your credit, income, and equity have improved since you first bought the home.

A homeowner who once needed FHA financing may now qualify for a conventional refinance that could reduce or remove mortgage insurance, depending on equity and program requirements. That shift can be meaningful, but it depends on the full loan estimate, not just the headline rate.

VA Refinance Options: For Eligible Veterans, Service Members, and Surviving Spouses

For eligible borrowers, VA refinance options can be especially valuable. VA loans are designed for qualifying veterans, active-duty service members, certain members of the National Guard and Reserves, and eligible surviving spouses.

The VA Interest Rate Reduction Refinance Loan, often called an IRRRL, may help eligible VA borrowers refinance an existing VA loan into a new VA loan with a lower rate, a more stable payment, or a different structure. There is also a VA cash-out refinance, which may allow eligible borrowers to access home equity or refinance from a non-VA loan into a VA loan.

VA refinances can offer important benefits, but they are not automatic wins. Funding fees, closing costs, loan size, occupancy rules, and long-term plans should all be reviewed. Eligible borrowers should compare the VA option with conventional and other available refinance paths before choosing.

If this applies to you, New Era Lending’s guide to veterans mortgage options for purchase and refinance explains the broader landscape.

Refinancing to Remove Mortgage Insurance

Mortgage insurance can add a noticeable amount to your monthly housing cost. Homeowners may look into refinancing when their equity has grown enough to qualify for a loan without mortgage insurance, or with a more favorable structure.

This is common for borrowers who bought with a low down payment and have since gained equity through payments, home appreciation, or improvements. It may also apply to FHA borrowers who want to evaluate whether refinancing into a conventional loan could reduce long-term mortgage insurance costs.

However, removing mortgage insurance is not the only number that matters. You still need to compare the new rate, closing costs, term length, and total monthly payment. A refinance that removes mortgage insurance but increases the interest rate or resets the loan for too long may not be the best fit.

A good review should answer one simple question: after all costs and changes are included, does the new loan improve your situation within the time you expect to keep the home?

Adjustable-Rate to Fixed-Rate Refinance: For Payment Stability

If you currently have an adjustable-rate mortgage, refinancing into a fixed-rate mortgage may be worth exploring before or after the adjustable period changes. The goal here is usually stability, not necessarily the lowest possible payment.

An adjustable-rate mortgage may start with a lower initial rate, but the payment can change later based on the loan’s terms and market conditions. A fixed-rate refinance can make budgeting easier because the principal and interest payment remains consistent for the life of the loan.

This option may fit if you plan to stay in the home long term, prefer predictable payments, or are concerned about future rate adjustments. Even if the new fixed payment is slightly higher at first, the added certainty may be valuable.

On the other hand, if you plan to sell soon, refinancing out of an ARM may not provide enough time to recover closing costs. This is where a break-even calculation becomes important.

Cash-In Refinance: For Better Pricing or Lower Loan-to-Value

A cash-in refinance is the opposite of a cash-out refinance. Instead of taking money out, you bring money to closing to reduce the loan balance. This can help some homeowners qualify for better terms, lower their loan-to-value ratio, remove mortgage insurance, or fit within a specific loan program limit.

This option is less common than a cash-out refinance, but it can be useful for homeowners with strong savings who want to reduce long-term interest costs or improve loan eligibility.

The main question is opportunity cost. Money used to reduce the mortgage balance cannot be used for emergency savings, retirement contributions, business needs, or other investments. For some homeowners, the guaranteed reduction in debt is worth it. For others, keeping liquidity may be more important.

No-Closing-Cost Refinance: For Reducing Upfront Cash Needs

A no-closing-cost refinance does not mean the refinance is free. It usually means the costs are paid through a lender credit in exchange for a higher interest rate, or the costs are rolled into the new loan balance when allowed.

This can be helpful if you want to refinance but prefer not to bring cash to closing. It may also make sense if you do not expect to keep the loan long enough for upfront closing costs to pay off.

The tradeoff is that you may pay more over time through a higher rate or larger loan balance. A no-closing-cost structure can be a practical tool, but it should be compared against paying costs upfront. Ask to see both versions so you can evaluate the monthly payment, APR, cash to close, and long-term cost.

The Consumer Financial Protection Bureau explains that the Loan Estimate is designed to help borrowers compare loan costs and terms more clearly. Reviewing that document carefully is one of the best ways to avoid surprises.

How to Compare Refinance Options Without Getting Overwhelmed

A refinance decision becomes easier when you compare each option against the same set of questions. Instead of focusing only on the interest rate, look at the complete picture.

Ask these questions before choosing a refinance path:

- What is my primary goal for refinancing?

- How much will my monthly payment change?

- What are the total closing costs?

- How long will it take to break even?

- Will the loan term restart or shorten?

- How much interest could I pay over the life of the loan?

- Does the new loan add or remove mortgage insurance?

- Am I taking cash out, bringing cash in, or keeping the balance similar?

- How long do I realistically expect to keep the home?

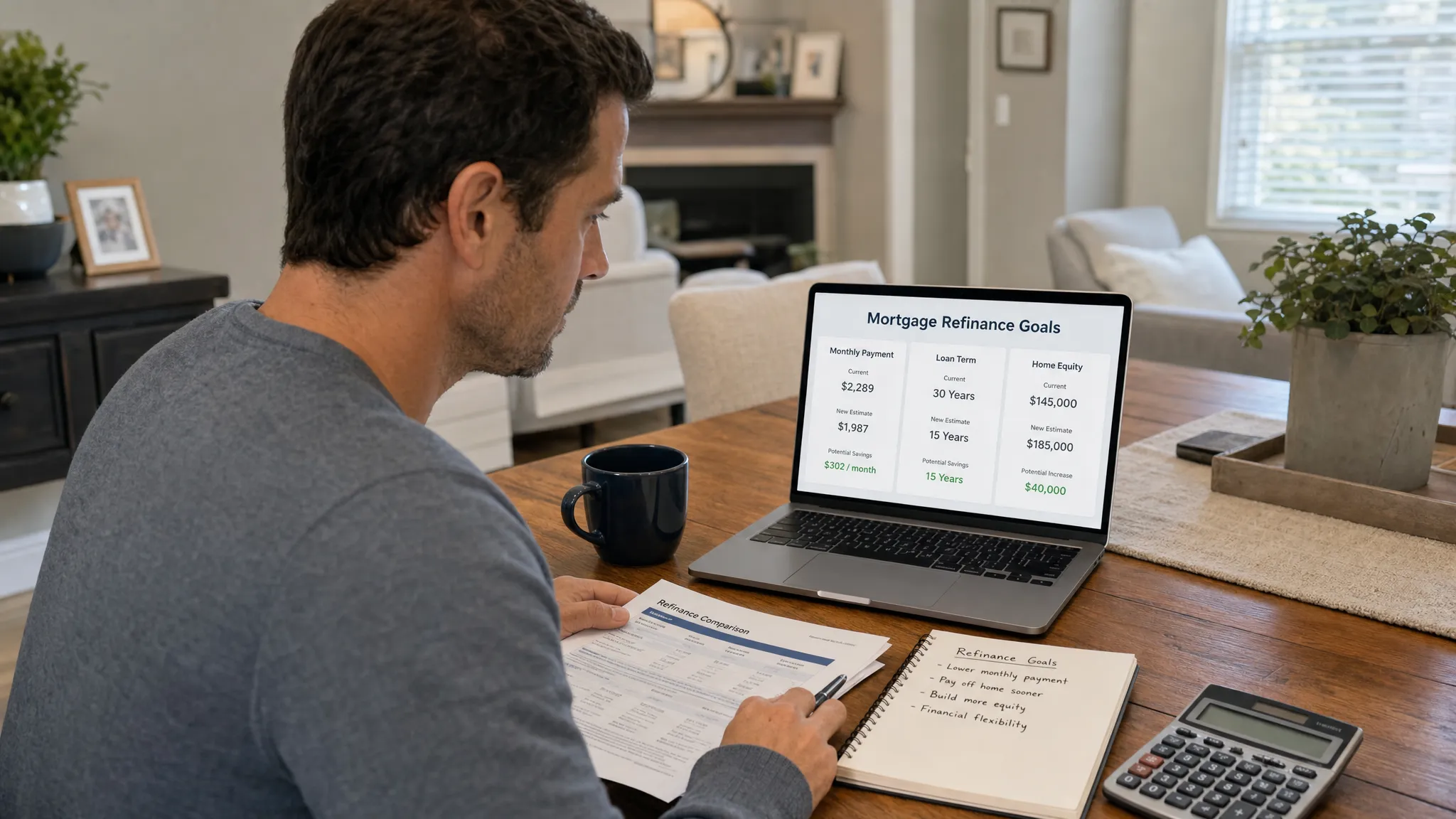

The break-even point is especially important. If refinancing saves you $200 per month and costs $4,000, the simple break-even is about 20 months. If you plan to sell in a year, that may not work. If you plan to stay for seven years, it may be more compelling.

Also compare rate and APR. The interest rate affects the monthly principal and interest payment, while APR reflects certain loan costs and can help you compare offers more consistently. Neither number should be viewed alone.

When Refinancing May Not Fit Your Goals

Refinancing is not always the right move. Even if you qualify, there are times when keeping your current mortgage may be better.

It may not make sense to refinance if the closing costs outweigh the savings, you plan to sell soon, the new loan significantly increases total interest, or you are using home equity without a clear repayment plan. It may also be risky to refinance unsecured debt into your mortgage if spending habits have not changed, since the debt becomes tied to your home.

Another reason to pause is uncertainty. If your income, job situation, or homeownership plans are changing, it may be worth speaking with a mortgage professional before making a long-term commitment.

A Goal-Based Refinance Review Can Make the Path Clearer

The best mortgage refinance option is the one that fits your actual goal, not just the one with the lowest advertised rate. A homeowner focused on monthly relief may choose a different structure than someone focused on long-term interest savings. A veteran with VA eligibility may have options that a conventional borrower does not. A homeowner with strong equity may compare cash-out, cash-in, and mortgage insurance removal scenarios.

New Era Lending combines smart mortgage technology with personalized human guidance to help homeowners review refinance paths more clearly. With secure document uploads, e-signature support, educational resources, and loan options for purchase, refinance, and equity access across 39 states, the process is designed to be simpler without losing the value of expert support.

Frequently Asked Questions

What are the main mortgage refinance options? Common options include rate-and-term refinance, cash-out refinance, shorter-term refinance, FHA refinance, VA refinance, adjustable-rate to fixed-rate refinance, cash-in refinance, and no-closing-cost refinance structures.

Which refinance option is best for lowering my monthly payment? A rate-and-term refinance or term extension may lower the monthly payment, especially if you qualify for a lower rate. However, extending the term can increase total interest, so compare both monthly and long-term costs.

Is a cash-out refinance a good idea? It can be useful when the funds support a clear goal, such as home improvements or consolidating higher-interest debt. It is less ideal when it increases mortgage debt without a plan or turns short-term spending into long-term secured debt.

Can I refinance to remove mortgage insurance? In some cases, yes. If your home equity has increased enough, refinancing into a loan without mortgage insurance may be possible. The savings should be compared against the new rate, closing costs, and loan term.

How do I know if refinancing is worth it? Review the monthly savings, closing costs, break-even point, loan term, total interest, and how long you expect to stay in the home. A refinance is strongest when it supports a clear financial goal and the numbers work within your timeline.

Ready to Explore Refinance Options That Fit Your Goals?

If you are considering a refinance, start with your goal and then compare the options that support it. New Era Lending can help you review your current mortgage, understand available refinance paths, and move forward with clear guidance instead of guesswork.