.jpg)

.jpg)

.jpg)

Can Mortgage Loan Consolidation Lower Your Costs?

Mortgage loan consolidation can be a smart move when it simplifies your finances and lowers the true cost of debt. It can also be expensive if it stretches short-term balances across a new 15, 20, or 30-year mortgage without a plan.

The key question is not just whether you can roll debts together. It is whether the new loan improves your monthly budget, total interest cost, risk level, and long-term financial flexibility.

Below is a practical way to evaluate mortgage loan consolidation before you refinance, use home equity, or combine multiple home-secured loans.

What mortgage loan consolidation usually means

In a home financing context, mortgage loan consolidation generally means using a mortgage product to combine debts into one payment secured by your home. The structure can vary depending on what you owe today, how much equity you have, and what you want to accomplish.

Common examples include:

- Combining a first mortgage and second mortgage into one refinanced loan.

- Using a cash-out refinance to pay off credit cards, personal loans, medical bills, or other higher-rate debts.

- Replacing an existing mortgage and home equity line of credit with a new mortgage.

- Using a home equity loan or HELOC to consolidate non-mortgage debts while keeping your current first mortgage in place.

Consolidation does not erase debt. It changes where the debt sits, how it is repaid, what interest rate applies, and what asset secures repayment. When the new loan is secured by your home, that tradeoff deserves careful attention.

Can mortgage loan consolidation lower your costs?

Yes, it can lower your costs, but only if you define cost correctly. Many borrowers focus on the monthly payment, which matters, but it is only one part of the decision.

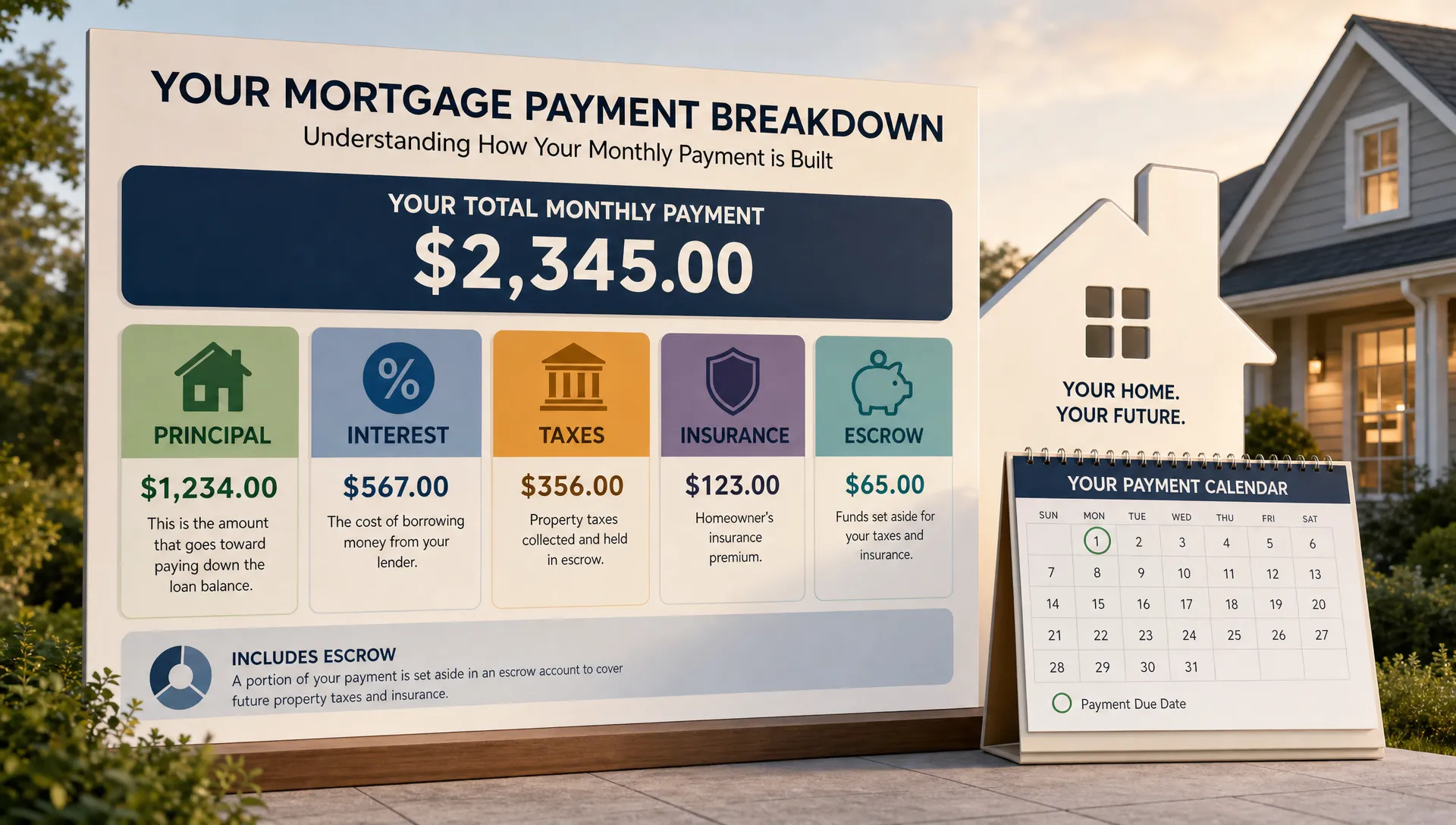

A consolidation option should be evaluated across four cost categories: monthly payment, interest rate, total interest, and upfront or rolled-in fees.

Monthly payment savings

Mortgage loan consolidation often lowers the monthly payment because mortgage rates are usually lower than credit card rates and many personal loan rates. A mortgage also spreads repayment over a longer period, which can reduce monthly pressure.

That can be helpful if your current obligations are crowding your budget. Lower required payments may make it easier to stay current, avoid late fees, rebuild savings, or manage cash flow after a life change.

But a smaller monthly payment is not automatically a cheaper loan. If you pay less each month because you extended the debt over decades, the total cost can rise even if the payment feels more manageable.

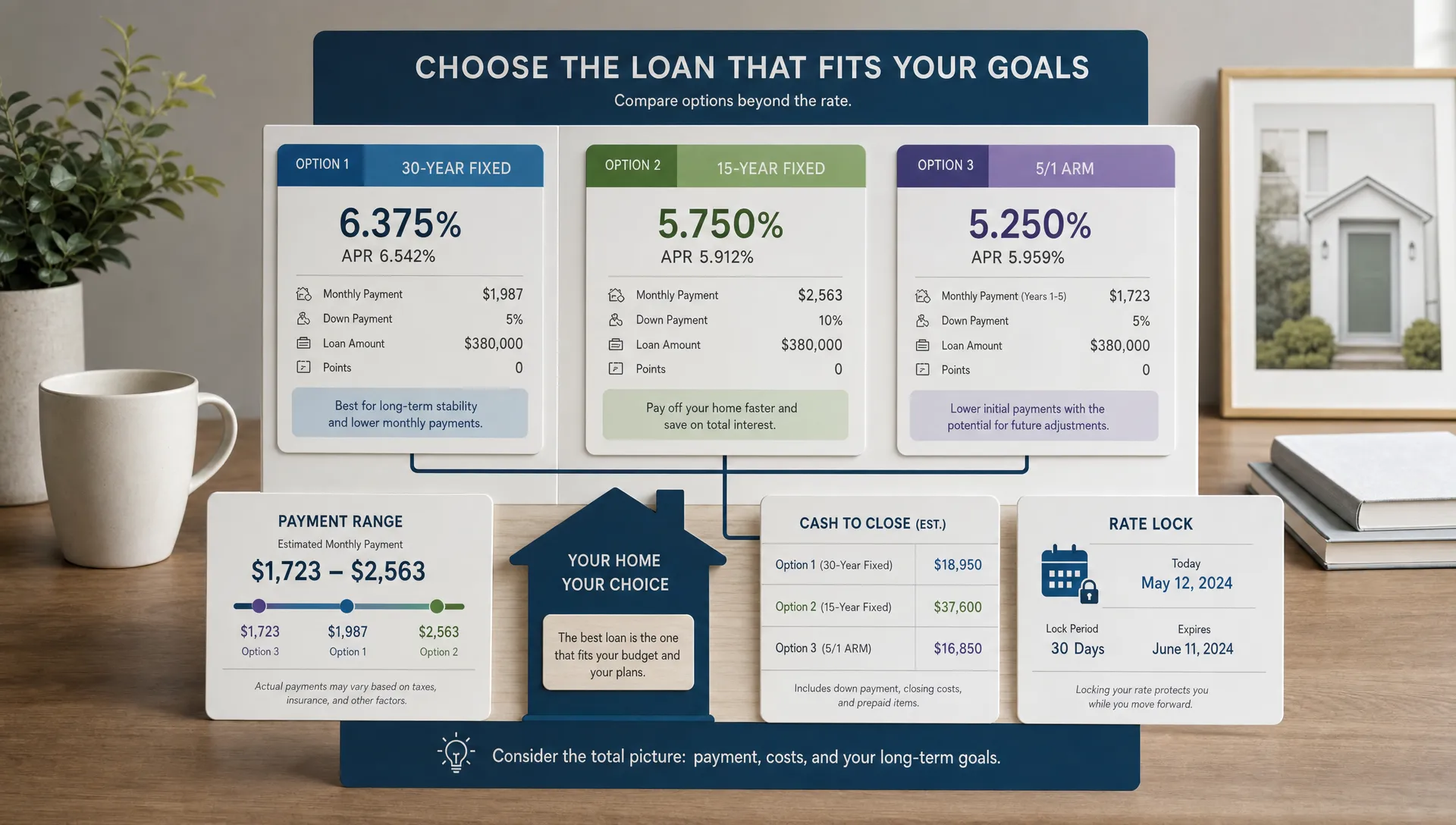

Interest rate and APR savings

The interest rate is important, but the annual percentage rate, or APR, may give a fuller picture because it reflects certain loan costs. If you are consolidating high-interest credit card debt into a mortgage with a much lower rate, the interest savings can be meaningful.

However, if you are replacing a low-rate first mortgage with a higher-rate refinance just to include other debts, the math may be less attractive. You might lower the rate on the non-mortgage debt while raising the rate on the largest balance you owe.

That is why the blended cost matters. Compare the cost of all current debts together against the cost of the new loan, not just one rate against another.

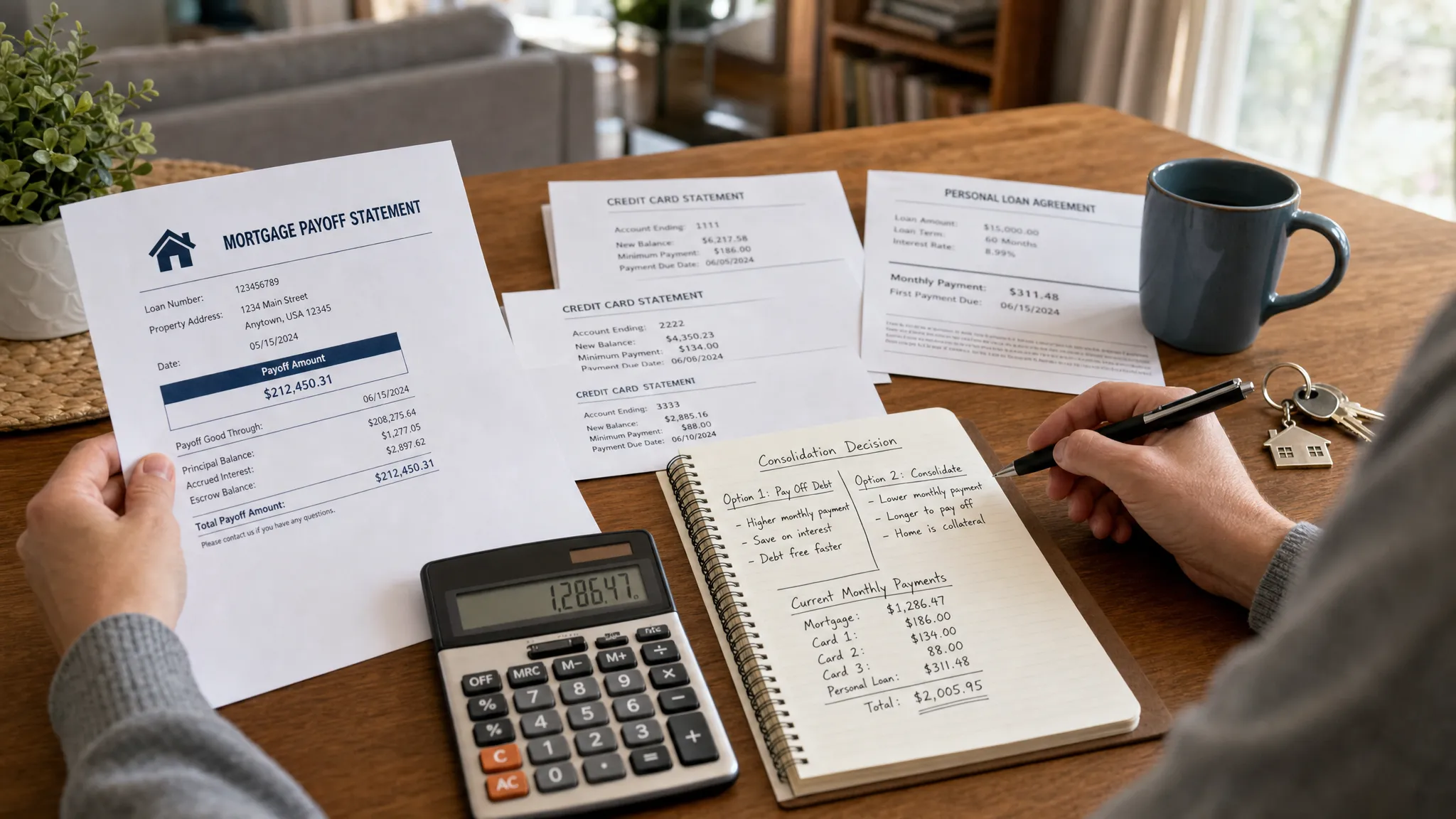

Total interest over time

Total interest is where consolidation can surprise borrowers. A $20,000 credit card balance at a high APR is expensive, but if you would have paid it off in three years, rolling it into a 30-year mortgage may keep that debt alive much longer.

One way to protect yourself is to make extra principal payments after consolidation. If the new loan lowers your required payment, consider applying some or all of the monthly savings toward the mortgage principal or a separate payoff plan. That can help you capture rate savings without turning short-term debt into long-term debt.

Closing costs and loan structure

Refinances and equity-based loans can involve closing costs, lender fees, title charges, appraisal costs, prepaid items, and other expenses. Sometimes these costs are paid at closing. Other times they are rolled into the loan balance, which means you finance them and pay interest on them over time.

Loan structure also matters. Points, lender credits, amortization, mortgage insurance, escrow requirements, and term length can all change the true cost of consolidation. If you want a deeper look at how these details affect the numbers, New Era Lending explains the major loan payment terms that can raise or lower costs.

When consolidation is more likely to make sense

Mortgage loan consolidation is more likely to lower costs when several conditions line up.

First, the debts being consolidated carry much higher rates than the proposed mortgage or equity loan. This is often the case with credit cards, some personal loans, and certain private debts.

Second, you have enough home equity to qualify without creating a risky loan-to-value ratio. Lenders will look at your home value, current mortgage balance, proposed new loan amount, credit profile, income, and debt-to-income ratio.

Third, your credit and income documentation support favorable terms. The stronger your financial profile, the more likely you are to qualify for a structure that actually improves your cost position.

Fourth, you have a plan to avoid rebuilding the balances you just paid off. Consolidation can give a fresh start, but it becomes dangerous if credit cards are paid down and then charged back up again.

Income stability can also affect the approval process. If your household income comes from project-based or specialized industries, lenders may ask for a clearer paper trail around contracts, bonuses, or variable earnings. For instance, professionals connected to technical sectors such as renewable energy, maritime work, or industrial projects may be familiar with milestone-based work, similar to how engineering solutions providers serving renewable energy and maritime projects often operate around complex project timelines.

The stronger your documentation, the easier it is to compare options with confidence.

When consolidation may cost more

Mortgage loan consolidation can be the wrong move when the payment looks better but the long-term math gets worse.

One common issue is replacing a low-rate mortgage. If your current first mortgage has a rate that is significantly below current market options, a cash-out refinance could raise the cost on your entire mortgage balance. In that situation, a home equity loan or HELOC might be worth comparing because it may let you keep the existing first mortgage intact.

Another issue is resetting the clock. If you are 12 years into a 30-year mortgage and refinance into a new 30-year term, you may reduce the monthly payment but extend repayment far beyond your original schedule. That can increase total interest unless you make extra payments or choose a shorter term.

A third issue is securing unsecured debt with your home. Credit card debt is unsecured. A mortgage is secured by real estate. If you roll unsecured debt into a mortgage and later cannot make payments, your home is at greater risk.

Finally, consolidation can create a false sense of progress. A single payment feels cleaner, but the important question is whether your balance is falling faster and whether your financial risk is lower.

How to run the numbers before consolidating

Before deciding, compare your current debts with the proposed loan side by side. You do not need to be a financial analyst, but you do need the right inputs.

Gather these numbers before speaking with a lender:

- Current balances for every debt you want to consolidate.

- Current interest rates, minimum payments, and payoff timelines.

- Proposed new loan amount, rate, APR, term, and estimated payment.

- Closing costs, prepaid items, points, and any fees rolled into the loan.

- How long you expect to keep the home or the new loan.

- Whether you plan to make extra payments after consolidation.

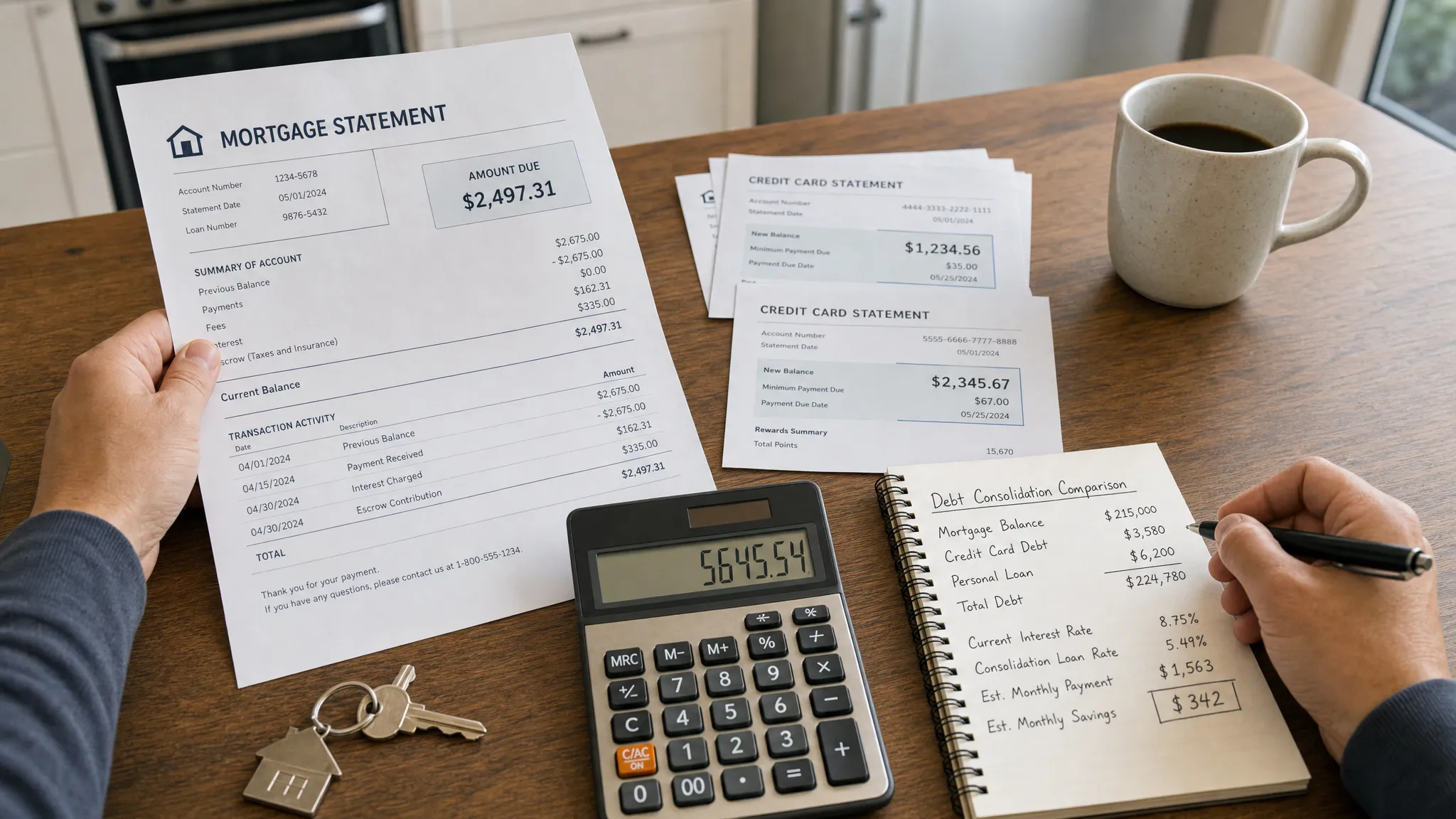

A simple break-even calculation can also help. Divide total closing costs by your estimated monthly savings. If consolidation costs $6,000 and saves $300 per month, the payment break-even point is 20 months. If you plan to sell or refinance before then, the savings may not fully materialize.

That break-even number is useful, but it is not the whole story. You should also compare total interest over the life of the new plan. A loan can break even on monthly savings while still costing more over decades.

A simple example of consolidation math

Imagine a homeowner has a first mortgage, a HELOC, and several credit card balances. The credit cards carry much higher rates than the home-secured debts, and the monthly minimums are making the household budget tight.

A cash-out refinance could combine everything into one mortgage payment. The new payment might be lower than the combined old payments, especially if the credit card rates were high. That could improve cash flow right away.

But now consider the total cost. If the credit card debt would have been paid off in four years, and it is now included in a 30-year mortgage, the homeowner may pay interest on that portion of debt for far longer. The monthly savings are real, but the lifetime savings depend on whether the homeowner makes extra payments or chooses a shorter term.

This is why the best consolidation plan is rarely just the one with the lowest payment. It is the one that supports your budget while still moving you toward less debt, not just a different type of debt.

Options to compare before choosing consolidation

A cash-out refinance is only one path. Depending on your current mortgage rate, equity, credit profile, and goals, another option may fit better.

A rate-and-term refinance may be appropriate if your main goal is to improve the mortgage itself rather than pay off outside debt. A cash-out refinance may fit if you have sufficient equity and want to consolidate higher-rate debts into one new mortgage. A home equity loan or HELOC may make sense if your first mortgage has favorable terms you do not want to disturb.

Some borrowers should also compare non-mortgage solutions, such as a personal loan, a balance transfer plan, or a disciplined debt payoff strategy. These may carry higher rates than a mortgage, but they can avoid putting your home at risk and may keep repayment timelines shorter.

If you are primarily deciding between lowering your monthly payment and changing your repayment term, review these mortgage refinance options to lower payment or term before choosing a consolidation path.

Questions to ask your lender

A good lender should help you look beyond the advertised payment. Before committing to mortgage loan consolidation, ask direct questions that reveal both the benefits and tradeoffs.

Useful questions include:

- What debts are included in the new loan amount?

- What is the new monthly payment compared with my total current payments?

- What are the closing costs, and are they paid upfront or rolled into the loan?

- What is the APR, not just the interest rate?

- How much total interest will I pay if I make only the required payment?

- Will this refinance reset my loan term or extend my payoff date?

- Am I replacing a lower-rate first mortgage with a higher-rate loan?

- What happens if I make extra principal payments each month?

- Will mortgage insurance, escrow, or other payment components change?

- Are there alternatives that preserve my current mortgage?

If you are comparing rates, remember that the lowest rate is not always the best overall deal. Points, fees, credits, term length, and payment flexibility all matter.

How New Era Lending can help you evaluate consolidation

New Era Lending combines smart mortgage technology with personalized human guidance, which can be especially useful when the decision involves more than a simple rate comparison. Consolidation is personal. The right answer depends on your home equity, debt mix, income, credit profile, monthly budget, and long-term plans.

A clearer process can help you upload documents securely, review options, understand terms, and move through the lending steps with less confusion. New Era Lending offers a wide range of loan options for purchase, refinance, and equity access, including specialized veteran loan programs, across 39 states.

The goal is not just to qualify for a new loan. The goal is to understand whether the loan actually improves your financial position.

Frequently Asked Questions

Is mortgage loan consolidation the same as refinancing? Not always. A refinance replaces an existing mortgage with a new one. Mortgage loan consolidation may involve refinancing, but it can also involve using a home equity loan or HELOC to combine other debts while keeping your current mortgage.

Can I consolidate credit card debt into my mortgage? In many cases, yes, if you have enough equity and qualify for the loan. The benefit is often a lower rate or lower monthly payment. The risk is that unsecured credit card debt becomes secured by your home and may be repaid over a much longer period.

Will mortgage loan consolidation lower my monthly payment? It can, especially if you are consolidating high-rate debts or extending the repayment term. However, a lower monthly payment does not always mean lower total cost, so compare lifetime interest and closing costs.

Should I consolidate if I already have a low mortgage rate? Be careful. Replacing a low-rate first mortgage can make consolidation more expensive. You may want to compare a home equity loan, HELOC, or non-mortgage debt payoff strategy before refinancing the entire balance.

How much equity do I need for consolidation? Equity requirements depend on the loan type, lender guidelines, credit profile, property type, and overall risk factors. A lender can estimate your available equity using your home value and current mortgage balance.

Can I pay off consolidated debt faster? Often, yes. If your loan allows extra principal payments without penalty, applying monthly savings toward principal can reduce interest and shorten the payoff timeline. Confirm payment rules before closing.

Take the next step with clearer numbers

Mortgage loan consolidation can lower your costs when it reduces expensive debt, fits your budget, and supports a realistic payoff plan. It can also increase long-term costs if you focus only on the monthly payment.

Before you decide, compare the full picture: rate, APR, closing costs, term, total interest, risk, and your ability to avoid new debt. If you want help reviewing your options, New Era Lending can guide you through a personalized mortgage conversation built around your goals, not just a single payment number.