.jpg)

.jpg)

.jpg)

What Really Changes Your Home Payment Over Time

The payment you see at closing is important, but it is not the whole story. A home payment can shift over the years because it is made of several moving parts, not just the loan itself.

For many homeowners, the surprise is that their interest rate did not change, their loan servicer did not make a mistake, and they did not borrow more money. Yet the monthly draft still went up. That usually happens because the full cost of owning the home includes taxes, insurance, mortgage insurance, HOA dues, and personal financing decisions that can change after closing.

The better question is not only, “Can I afford this payment today?” It is also, “How might this home payment behave over the next three, five, or ten years?”

Your mortgage payment and your home payment are not always the same thing

When people say “mortgage payment,” they often mean the full amount they pay each month. But in lending, it helps to separate the pieces.

Your actual loan payment is usually principal and interest. Principal pays down the amount you borrowed. Interest is the cost of borrowing. If you have a fixed-rate mortgage, this principal and interest portion is generally designed to stay the same for the life of the loan.

Your home payment is broader. It may include principal, interest, property taxes, homeowners insurance, mortgage insurance, HOA dues, flood insurance, utilities, maintenance, and other costs tied to owning the property. Some of these are collected by your lender through escrow. Others are paid directly by you.

That distinction matters because a fixed-rate loan can still come with a changing monthly bill. The loan may be stable while the ownership costs around it move.

The parts of your payment that usually stay predictable

The most predictable part of a traditional fixed-rate mortgage is principal and interest. If you borrow a set amount, choose a fixed interest rate, and repay it over a set term, that portion is calculated upfront.

For example, a 30-year fixed-rate loan is amortized so that each scheduled payment gradually shifts over time. Early payments are more interest-heavy. Later payments pay more principal. But the scheduled principal and interest amount usually stays the same unless you refinance, modify the loan, recast the loan, or make another structural change.

A fixed principal and interest payment can give your budget a strong foundation. That is one reason many buyers prefer fixed-rate mortgages, especially if they plan to keep the home for a long time or want less payment uncertainty.

Adjustable-rate mortgages work differently. With an ARM, the rate is fixed for an initial period, then can adjust based on the loan terms. That means the principal and interest portion itself may rise or fall after the fixed period ends. If you are considering an ARM, it is important to understand the first adjustment date, adjustment frequency, rate caps, index, margin, and worst-case payment scenario.

If you want a deeper comparison of fixed loans, ARMs, and buydowns, New Era Lending’s guide to mortgage options compared can help you think through the tradeoffs.

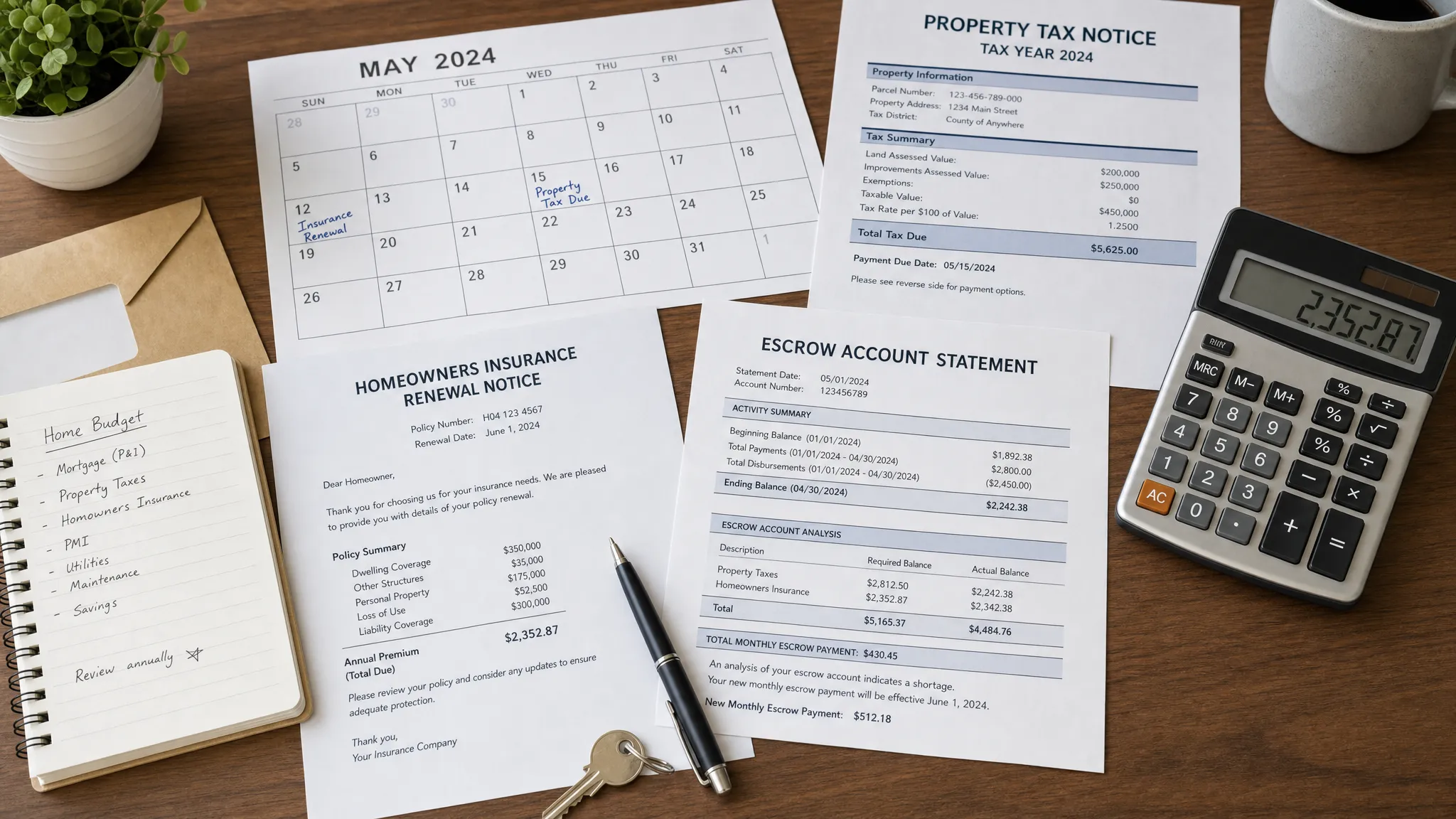

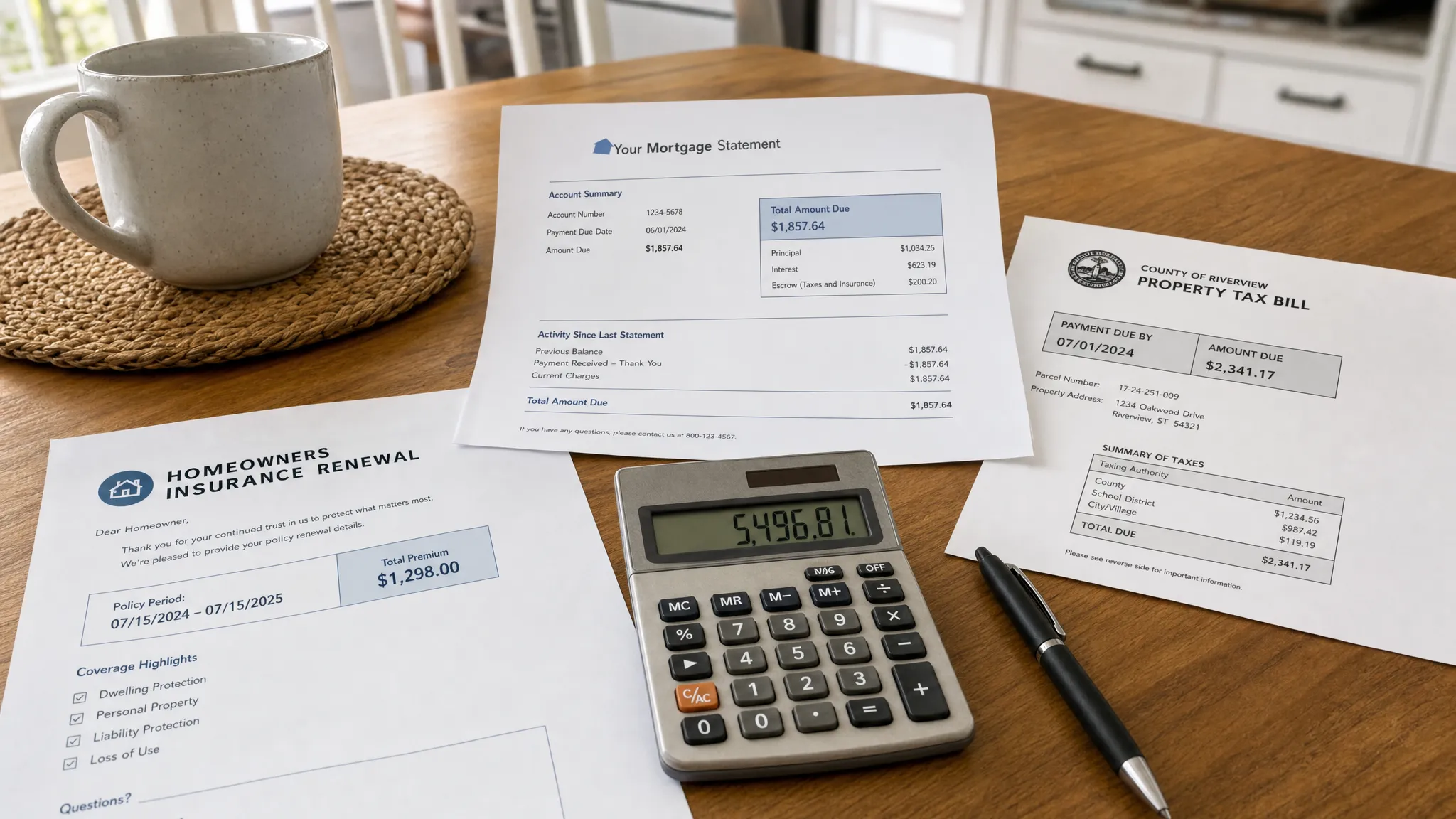

The biggest reason payments change: escrow

Escrow is one of the most common reasons a homeowner’s monthly payment changes after closing. If your loan has an escrow account, your servicer collects money each month for items like property taxes and homeowners insurance. When those bills come due, the servicer pays them from the account.

The tricky part is that taxes and insurance are estimates at closing. Later, your actual bills may be higher or lower than expected. Each year, the loan servicer typically reviews the escrow account to see whether enough money is being collected.

If your property taxes or insurance increase, your escrow payment may rise. If your account has a shortage, your servicer may spread that shortage over future payments, which can create a double effect: your new monthly escrow collection increases, and you may also pay back the prior shortage.

That is why some homeowners see a larger jump than expected. The payment is not only adjusting for the new bill. It may also be catching up from the previous year.

Property taxes can rise for reasons outside your loan

Property taxes are one of the biggest long-term variables in a home payment. They are not set by your lender. They are based on local tax rules, assessed value, exemptions, millage rates, school budgets, municipal budgets, and sometimes voter-approved bonds or levies.

Your tax bill can change when:

- The county or municipality reassesses your property value.

- A previous owner’s exemption no longer applies after purchase.

- Local tax rates increase.

- New school, infrastructure, or municipal funding measures are approved.

- You complete improvements that increase the assessed value.

- A temporary tax abatement expires.

A common first-year surprise happens when a buyer’s escrow estimate is based on the seller’s old tax bill. If the seller had owned the home for many years, had special exemptions, or benefited from assessment limits, the buyer’s future tax bill may look different.

Before buying, ask your loan officer, real estate agent, or local tax office whether the current tax bill is likely to reset after the sale. The current tax amount on a listing is useful, but it may not be the amount you pay after ownership transfers.

Homeowners insurance can change faster than buyers expect

Homeowners insurance is another major factor that can alter your home payment over time. Premiums can change because of your home, your location, your coverage choices, and broader insurance market conditions.

Even if you never file a claim, premiums may rise due to rebuilding costs, labor costs, material costs, weather risk, wildfire or hurricane exposure, claims activity in your region, or changes in an insurer’s pricing model. If your policy renews at a higher premium and your insurance is escrowed, your monthly payment can increase.

Your own coverage decisions also matter. A lower deductible may cost more each month. Additional coverage for valuables, sewer backup, flood, wind, earthquake, or higher replacement cost coverage can increase premiums. On the other hand, shopping coverage, improving home safety, bundling policies, or adjusting deductibles may reduce costs.

Insurance should not be treated as a one-time closing item. Review it annually. You want enough coverage to protect the home, but you also want to know whether a better-fit policy is available.

Mortgage insurance may raise, lower, or disappear from your payment

Mortgage insurance is often part of the monthly payment when a buyer makes a smaller down payment. But the rules depend on the loan program.

With many conventional loans, private mortgage insurance may be removable once you build enough equity and meet the program’s requirements. That can lower your monthly payment. In some cases, homeowners request cancellation based on the original value and loan balance. In other cases, a new valuation or refinance may be part of the strategy.

FHA mortgage insurance works differently. Depending on the down payment, loan term, and current program rules, FHA mortgage insurance may last for a set period or for the life of the loan. VA loans do not have monthly PMI, though eligible borrowers may have a VA funding fee unless exempt. USDA loans have their own guarantee fee structure.

This is where a small change in loan program can create a meaningful difference over time. Two loans with similar starting payments may age differently because their mortgage insurance rules are not the same.

For a detailed breakdown, see New Era Lending’s guide to mortgage insurance rules and options.

HOA dues and special assessments can change your real monthly cost

If the property is in a homeowners association, condo association, or planned community, HOA dues should be part of your home payment planning. Even when dues are not paid through your mortgage servicer, they still affect affordability.

HOA dues may rise when community costs increase. Landscaping, pool maintenance, insurance, security, building repairs, management fees, elevators, roofs, roads, and reserves all affect association budgets.

Special assessments are another risk. An association may charge owners an additional amount for major repairs or underfunded reserves. Condo owners should pay close attention to this, especially in buildings with aging systems, deferred maintenance, or rising master insurance premiums.

Before buying, review HOA documents, budgets, reserve studies, meeting minutes, insurance information, and any pending assessments. A low monthly HOA fee may look attractive, but it can be a warning sign if the association is not saving enough for future repairs.

Renovations can affect your payment indirectly

A renovation does not automatically change your existing mortgage payment unless you finance it with a new loan, refinance, HELOC, or other borrowing. But improvements can still affect your overall home payment in indirect ways.

Major upgrades may increase the replacement cost of the home, which can change insurance needs. Some improvements may increase assessed value, which can affect property taxes depending on local rules. If you use a cash-out refinance, home equity loan, or HELOC to fund the work, you may add a new monthly payment or replace your current mortgage with a new one.

That does not mean renovations are bad. Many improvements can make a home more functional, comfortable, and potentially more valuable. The key is to budget beyond the contractor estimate. Whether you are comparing local providers or browsing examples of home renovation and interior upgrade projects, remember to think through taxes, insurance, permits, financing costs, and maintenance after the work is complete.

If you plan to use home equity for renovations, compare the payment structure carefully. A cash-out refinance, home equity loan, and HELOC can all access equity, but they do not behave the same way over time.

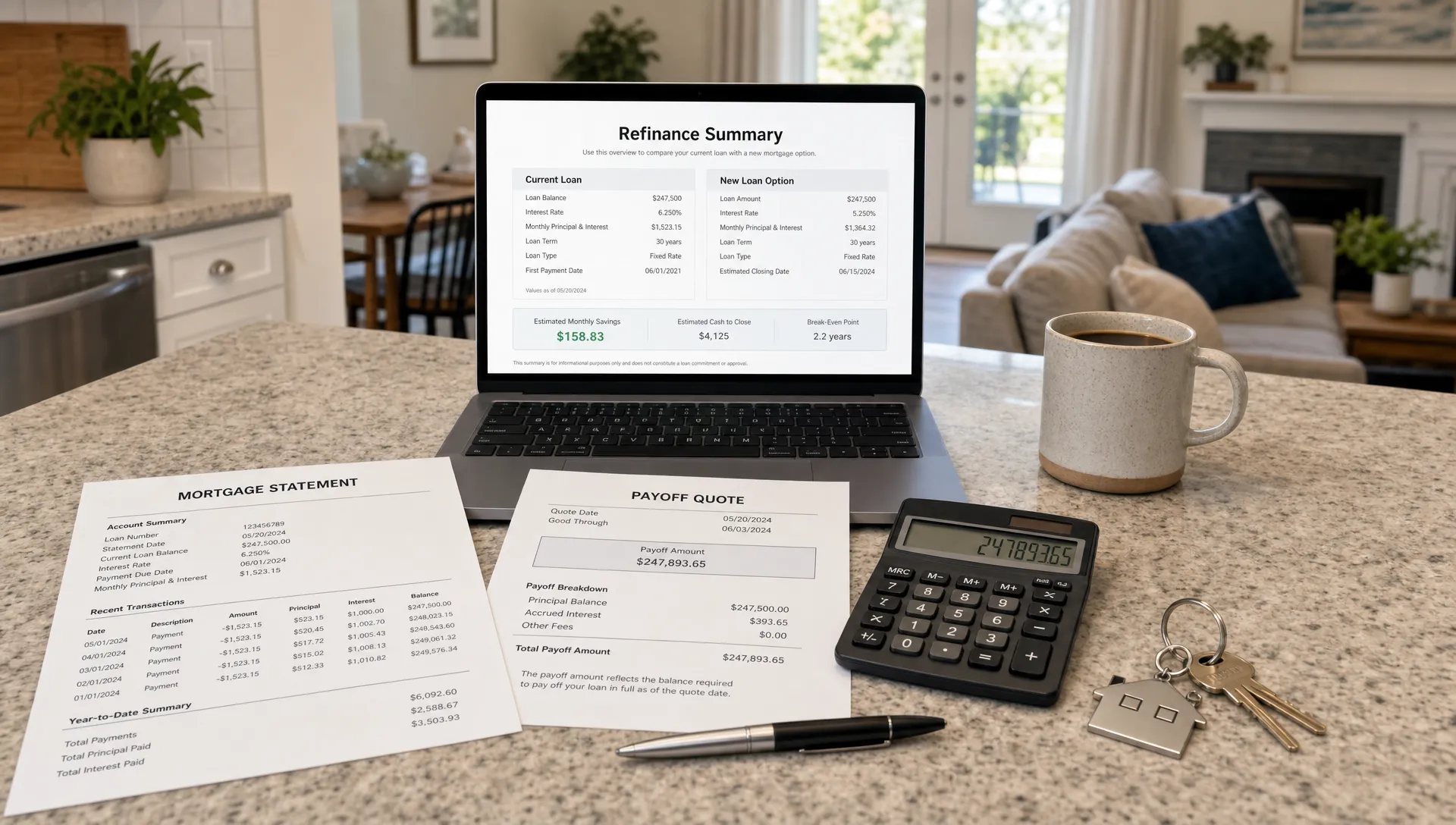

Refinancing can lower your payment, but it can also change the timeline

Refinancing is one of the most direct ways to change a home payment. A refinance may lower the rate, change the term, remove mortgage insurance, switch from an ARM to a fixed-rate loan, or allow cash-out access to equity.

But a lower monthly payment is not automatically a better deal. Sometimes the payment drops because the term is being extended. That may improve monthly cash flow, but it can increase total interest over time if you keep the loan for the full term.

A refinance can also increase your payment if you shorten the term, take cash out, roll closing costs into the loan, or move from a very low old rate to a higher new rate for a strategic reason.

Before refinancing, compare:

- The new monthly payment versus the current full payment.

- The break-even point on closing costs.

- The new loan term and how much time is being added.

- Whether mortgage insurance changes.

- The total interest cost if you keep the loan long term.

- Whether cash-out proceeds solve a real financial goal.

A refinance should match your goal, not just chase a lower advertised rate. If your goal is cash flow, the best answer may be different than if your goal is paying the home off faster.

Extra principal payments do not always lower next month’s payment

Many homeowners assume that paying extra principal will immediately reduce the next month’s required payment. Usually, it does not.

Extra principal payments reduce the loan balance faster. That can save interest and shorten the payoff timeline. But on most standard fixed-rate mortgages, the required monthly principal and interest payment remains the same unless you recast the loan, refinance, or modify it.

A recast may be available on some loan types. With a recast, you make a lump-sum principal payment, and the lender recalculates the monthly payment based on the lower balance and remaining term. Not all loans allow recasting, and there may be a fee, so ask your servicer before planning around it.

Extra payments can be powerful, but they should be made with the right expectation. They are usually a long-term interest-saving strategy, not an immediate monthly payment reduction strategy.

A simple five-year example

Imagine a buyer closes with a fixed-rate mortgage and a starting full payment of $2,400 per month. The principal and interest portion is fixed, but the full home payment still changes.

In year one, the payment is $2,400. In year two, the county reassesses the property after the sale, and the escrow portion rises by $125 per month. In year three, insurance renews at a higher premium, adding $55 per month. In year four, the homeowner’s conventional PMI is removed after meeting equity and loan requirements, reducing the payment by $140 per month. In year five, HOA dues increase by $35 per month, but they are paid separately rather than through escrow.

The loan itself did not behave unpredictably. The total cost of owning the home changed because the surrounding pieces changed.

This is why affordability planning should look beyond the first payment. A home that feels comfortable only if every estimate stays flat may become stressful when normal ownership costs rise.

How to build a home payment that ages well

You cannot control every future cost, but you can reduce surprises. The goal is not to predict every tax bill or insurance renewal perfectly. The goal is to create enough margin that normal changes do not derail your budget.

Start by estimating the full payment, not just principal and interest. Include taxes, insurance, mortgage insurance, HOA dues, and realistic maintenance. If you are still shopping, New Era Lending’s guide on estimating your monthly mortgage payment is a useful starting point.

Then ask “what if” questions before you commit:

- What if taxes rise after purchase?

- What if insurance increases by 10% to 20% at renewal?

- What if HOA dues increase next year?

- What if the temporary buydown expires?

- What if an ARM adjusts at the first adjustment date?

- What if I need to replace an appliance or HVAC system in the first year?

A strong home payment is not always the lowest payment available. It is the payment that fits your life today and still has room for tomorrow.

What to ask your lender before closing

A good loan conversation should include more than rate and cash to close. Ask how your payment is built, what can change, and what is most likely to change first.

Helpful questions include:

- Which parts of this payment are fixed, and which are estimates?

- Is the loan escrowed for taxes and insurance?

- How were property taxes estimated?

- Could the tax bill reset after purchase?

- Is mortgage insurance included, and when might it be removed?

- If this is an ARM, what is the maximum payment at the first adjustment?

- If this is a buydown, what will the payment be after each step?

- How much reserve cash should I keep after closing?

These questions help turn the payment from a single number into a real ownership plan.

Frequently Asked Questions

Can my home payment change if I have a fixed-rate mortgage? Yes. The principal and interest portion of a fixed-rate mortgage usually stays the same, but taxes, insurance, mortgage insurance, HOA dues, and escrow shortages can change your total monthly payment.

Why did my payment go up after the first year? The most common reasons are property tax reassessment, homeowners insurance renewal, or an escrow shortage. After your servicer reviews actual bills, your monthly escrow collection may be adjusted.

Can my payment ever go down? Yes. Your payment may decrease if mortgage insurance is removed, your escrow account has a surplus, you refinance into a lower payment, you recast the loan after a lump-sum principal payment, or certain taxes or insurance costs decline.

Do extra principal payments lower my monthly payment? Usually not right away. Extra principal payments typically reduce your balance and interest over time, but the required monthly payment often stays the same unless you recast, refinance, or modify the loan.

Should I choose the lowest starting payment? Not always. A low starting payment may come with tradeoffs, such as mortgage insurance, an adjustable rate, a temporary buydown, higher long-term cost, or less room for rising taxes and insurance. The best payment is the one that fits both your current budget and future risk tolerance.

Plan for the payment you will live with, not just the one you close with

Your home payment is not a set-it-and-forget-it number. It is a combination of loan terms, local costs, insurance markets, property rules, and personal decisions. Understanding which pieces can move helps you buy, refinance, or access equity with more confidence.

New Era Lending helps borrowers compare mortgage scenarios with modern tools and personalized human guidance. Whether you are buying a home, refinancing, or evaluating home equity options, the right conversation can show how your payment may look today and how it could change over time.

If you want a clearer view before you commit, connect with New Era Lending to review your options and build a mortgage plan around the full picture, not just the first monthly number.