.jpg)

.jpg)

.jpg)

Mortgage Insurance 101: PMI vs FHA MIP vs VA Options

Mortgage insurance is one of the most misunderstood parts of a home loan. Many buyers think it is “extra coverage for them,” or they assume it always lasts forever. In reality, mortgage insurance is usually a lender-protection tool that can meaningfully change your monthly payment, cash to close, and long-term strategy.

This guide breaks down the three most common “mortgage insurance” buckets you will run into in the U.S.:

- Conventional PMI (Private Mortgage Insurance)

- FHA MIP (Mortgage Insurance Premium)

- VA options (typically no monthly mortgage insurance, but a VA funding fee may apply)

By the end, you should be able to look at a Loan Estimate and quickly tell which type you have, how it is charged, and what your best exit strategy is.

First, what mortgage insurance actually does

Mortgage insurance generally protects the lender if a borrower defaults. That matters because when a lender takes more risk (for example, you put less money down), the lender often requires a form of insurance or guarantee.

This is why mortgage insurance is closely tied to loan-to-value (LTV):

- Higher LTV (smaller down payment) usually means higher risk.

- Higher risk often means PMI or MIP (or an alternative like a VA guarantee).

Important: mortgage insurance is not the same as homeowners insurance. Homeowners insurance protects you and the property against covered losses like fire, wind, liability claims, and more.

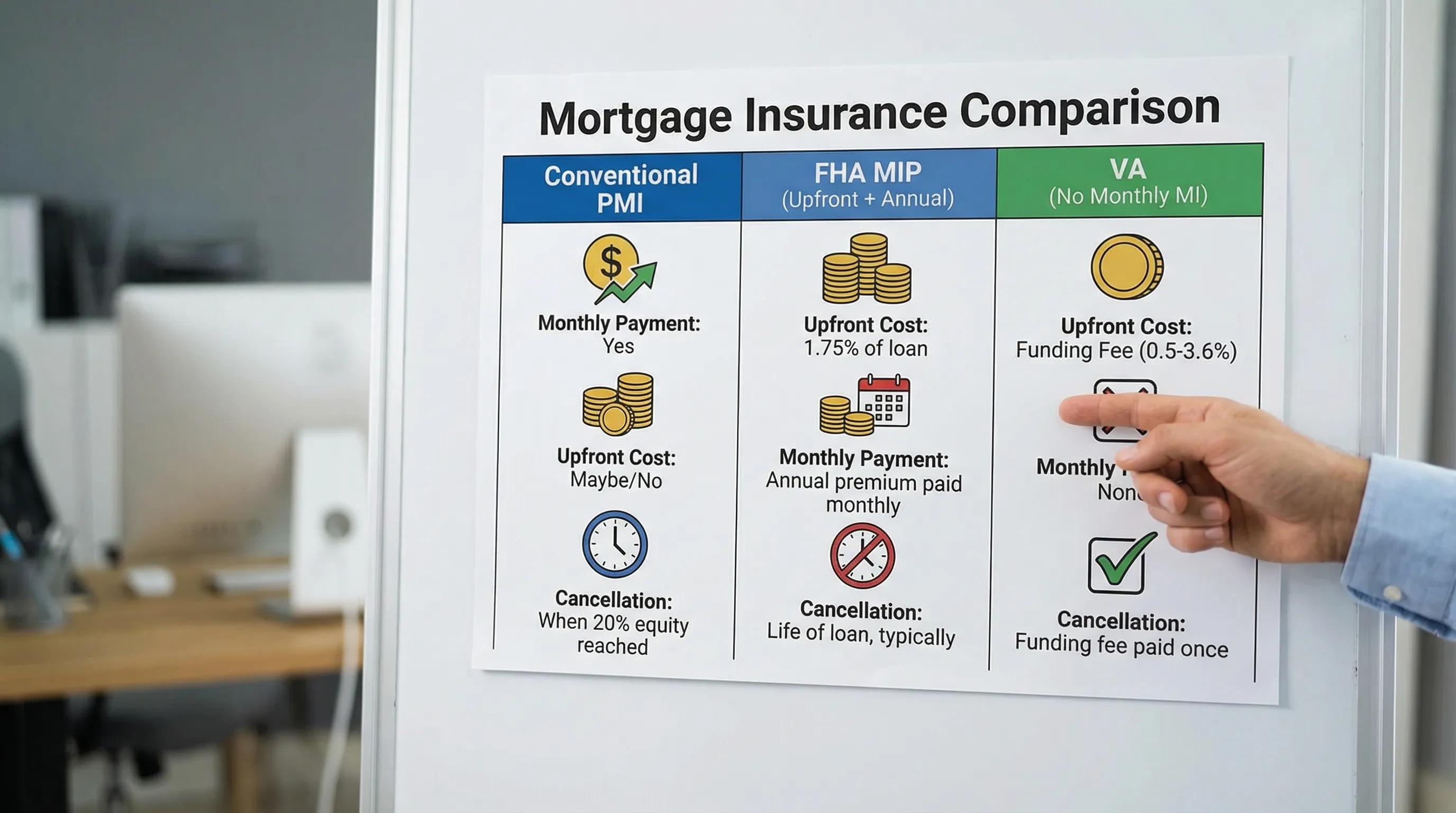

PMI (Conventional loans): how it works, what it costs, and how to remove it

PMI is most commonly associated with conventional mortgages when you put down less than 20%.

When PMI is required

In many cases, PMI applies when your loan is above 80% LTV (meaning you have less than 20% equity at closing). The exact requirement can vary by program, lender overlays, and borrower profile.

How PMI is charged

PMI is typically charged as a monthly premium that is included in your total payment. It can also be structured differently depending on the lender:

- Borrower-paid monthly PMI (the most common)

- Single-premium PMI (paid upfront)

- Lender-paid PMI (the lender covers it, often via a higher interest rate)

How much PMI costs

PMI is not one-size-fits-all. It is usually based on factors like:

- Credit score

- Down payment amount (LTV)

- Loan term (often 30-year vs 15-year)

- Property type (single-family vs condo, primary vs investment)

A common rule of thumb is PMI can range from roughly 0.2% to 2% of the loan amount per year, depending on risk factors. Your actual quote could be outside that range, but it is a useful starting point for budgeting.

How to remove PMI (the big advantage of conventional)

For most conventional loans, PMI is designed to be temporary.

Under the Homeowners Protection Act (HPA), PMI generally must automatically terminate when your balance reaches 78% of the home’s original value (assuming you are current), and borrowers can often request cancellation once they reach 80% based on the original value (subject to the servicer’s rules and payment history).

That removal feature is a major reason many buyers aim for a conventional loan when they have strong credit and a path to 20% equity.

For details, the CFPB provides a helpful overview of PMI cancellation rights under the HPA: CFPB guidance on PMI cancellation.

FHA MIP: upfront and annual insurance, and why “for life” matters

FHA loans are backed by the Federal Housing Administration and are often chosen for their flexible underwriting compared to conventional financing.

But FHA almost always comes with MIP, and it is structured differently than PMI.

FHA has two MIP charges

Most FHA borrowers will see both:

- Upfront MIP (UFMIP), commonly 1.75% of the base loan amount (often financed into the loan)

- Annual MIP, charged monthly

The annual MIP percentage depends on your loan amount, LTV, and loan term, and the rules can change over time. In 2023, HUD reduced annual MIP for many FHA loans (a widely discussed change that improved FHA affordability for new borrowers). You can verify current details directly via HUD resources: HUD FHA mortgage insurance information.

FHA MIP can be much harder to remove

This is the key difference most homeowners discover too late.

For most FHA loans originated after mid-2013:

- If you put less than 10% down, the annual MIP typically lasts for the life of the loan.

- If you put 10% or more down, MIP typically lasts 11 years.

That means FHA can be great for getting into a home, but your longer-term plan often includes one of these paths:

- Build equity and refinance into a conventional loan later (if it makes sense)

- Put 10%+ down upfront if you want the built-in 11-year MIP duration

FHA MIP cost example (simple illustration)

Assume a $300,000 FHA base loan.

- Upfront MIP at 1.75% would be $5,250 (often financed).

- Annual MIP depends on the case, but if it were 0.55% annually, that is about $1,650 per year, or about $137.50 per month.

This is not a quote, but it shows why FHA’s “low down payment” benefit should be evaluated alongside the full monthly payment and long-term MIP duration.

VA options: no monthly mortgage insurance, but know the VA funding fee

Eligible borrowers using a VA home loan typically do not pay monthly mortgage insurance.

Instead, the VA program is supported by a VA funding fee (unless you are exempt), and the VA provides a guaranty to the lender.

What you might pay instead of monthly MI

- A one-time VA funding fee that can often be financed into the loan amount

The funding fee amount depends on factors like:

- First-time vs subsequent use

- Down payment percentage

- Loan type (purchase, cash-out refi, etc.)

Because the VA updates guidance periodically, the safest move is to reference the VA’s current chart when planning: VA funding fee rates.

Funding fee exemptions

Some borrowers are exempt from the VA funding fee (for example, certain veterans receiving VA disability compensation). Eligibility details are specific, so it is important to confirm your status through VA documentation.

The practical takeaway

If you are eligible for VA financing, the absence of monthly mortgage insurance can be a major monthly payment advantage compared to conventional with PMI or FHA with MIP, even after considering the funding fee.

To dig deeper into the VA side, New Era Lending has additional VA education you may want to read next: VA loans eligibility, fees, and common myths.

PMI vs FHA MIP vs VA: the differences that matter most

When you compare options, focus on the variables that change your real-world cost.

1) Is the cost monthly, upfront, or both?

- Conventional PMI: usually monthly (other structures exist)

- FHA MIP: upfront + monthly

- VA: typically no monthly MI, but may include a funding fee

2) Can it be removed without refinancing?

- Conventional PMI: often yes, once you reach the required equity threshold (subject to rules)

- FHA MIP: often no (especially with less than 10% down), refinancing is the common “exit” strategy

- VA: no monthly MI to remove

3) Does your credit score change the price a lot?

- Conventional PMI: credit score can meaningfully impact PMI and pricing

- FHA MIP: tends to be less sensitive to credit score than conventional PMI, but FHA pricing still reflects overall risk in other ways

- VA: loan pricing varies by lender and borrower profile, but there is no monthly MI pricing component

4) What is your likely time horizon?

- If you plan to move in a few years, an upfront fee (or financed upfront fee) vs a monthly premium can change the math.

- If you plan to stay long-term, “can I remove this?” becomes a top priority.

How to lower mortgage insurance costs (or avoid them)

There is no universal best move, but these are common strategies:

Increase the down payment (even slightly)

Small down payment changes can sometimes move you into a better bracket for PMI, or reduce the amount you finance.

Improve credit before you lock

For conventional loans, a better credit profile can reduce both rate and PMI. If you are close to a score threshold, a targeted credit plan can be worth exploring.

Consider loan program fit, not just the interest rate

Many borrowers fixate on rate. Mortgage insurance can be the hidden line item that flips which option is best.

If you are comparing FHA and conventional, you may also want this related overview: FHA vs. Conventional loans.

Build an “exit plan” upfront

Ask your loan officer:

- What would it take to remove PMI, and how long might that take based on amortization?

- If FHA, what would it take to refinance out of MIP later (credit, equity, timing, costs)?

Know your real monthly payment from the Loan Estimate

On the Loan Estimate (LE), look for the line that includes:

- Principal and interest

- Mortgage insurance

- Estimated escrow (taxes and insurance)

Then compare that total across scenarios. A slightly higher rate with no monthly MI can still produce a lower payment, and vice versa.

A quick scenario: why the “cheapest” option is not always the best

Imagine two borrowers buying the same-priced home:

- Borrower A chooses conventional with PMI that can be removed in a few years.

- Borrower B chooses FHA with a competitive starting payment, but MIP lasts for the life of the loan.

If Borrower B never refinances, they could pay MIP far longer than Borrower A pays PMI. But if Borrower B expects to refinance once equity and credit improve, FHA can still be a smart bridge.

This is why mortgage insurance decisions are really about timeline and strategy, not just today’s payment.

A practical note for buyers planning renovations or major moves

Mortgage insurance is only one part of the monthly budget. If you are buying a fixer-upper or doing a big move, remember to plan for non-mortgage logistics too, like temporary storage for furniture and materials.

Some homeowners use on-site containers during renovations. If you are exploring that route, you can review options and transparent pricing for premium shipping containers to understand what buying a container might cost in your area.

Frequently Asked Questions

Is PMI the same as homeowners insurance? No. PMI protects the lender if the borrower defaults. Homeowners insurance protects you and the property against covered hazards.

Can I avoid PMI with 10% down? Usually not on a conventional loan. PMI is commonly required above 80% LTV, but the cost may be lower with 10% down than with 3% to 5% down.

Does FHA always require mortgage insurance? In most cases, yes. FHA typically includes upfront MIP and annual MIP, and many FHA loans with less than 10% down keep MIP for the life of the loan.

Do VA loans have mortgage insurance? VA loans typically do not have monthly mortgage insurance. Many VA borrowers pay a one-time VA funding fee instead (unless exempt).

If I choose FHA now, can I remove MIP later? Often the practical path is refinancing into a conventional loan once you qualify and the numbers make sense. Whether it is worth it depends on your rate, equity, credit, and closing costs.

How do I compare PMI vs MIP correctly? Compare the full monthly payment (including MI and escrow), the upfront costs or financed fees, and your likely time horizon. Reviewing Loan Estimates side-by-side is the most reliable approach.

Want a clear mortgage insurance comparison for your exact numbers?

Mortgage insurance is highly personal because it depends on credit, down payment, property type, and how long you expect to keep the home. If you want help comparing PMI vs FHA MIP vs VA options using real scenarios, New Era Lending can walk you through side-by-side payments and long-term totals.

Explore your options at New Era Lending and get guidance backed by smart tools, transparent terms, and human support (available across 39 states).