.jpg)

.jpg)

.jpg)

Mortgage Equity: How It Works and How to Use It Wisely

Homeowners hear the word “equity” all the time, but it is easy to treat it like a vague number on a Zestimate-style graph. In real life, mortgage equity is one of the most flexible financial levers you can have, and one of the easiest to misuse.

Used wisely, equity can lower your long-term costs, upgrade your home, or provide a safety net. Used carelessly, it can turn a stable mortgage into a payment problem (especially when rates rise or income changes). This guide breaks down how mortgage equity works, how lenders look at it, and practical ways to use it without overextending.

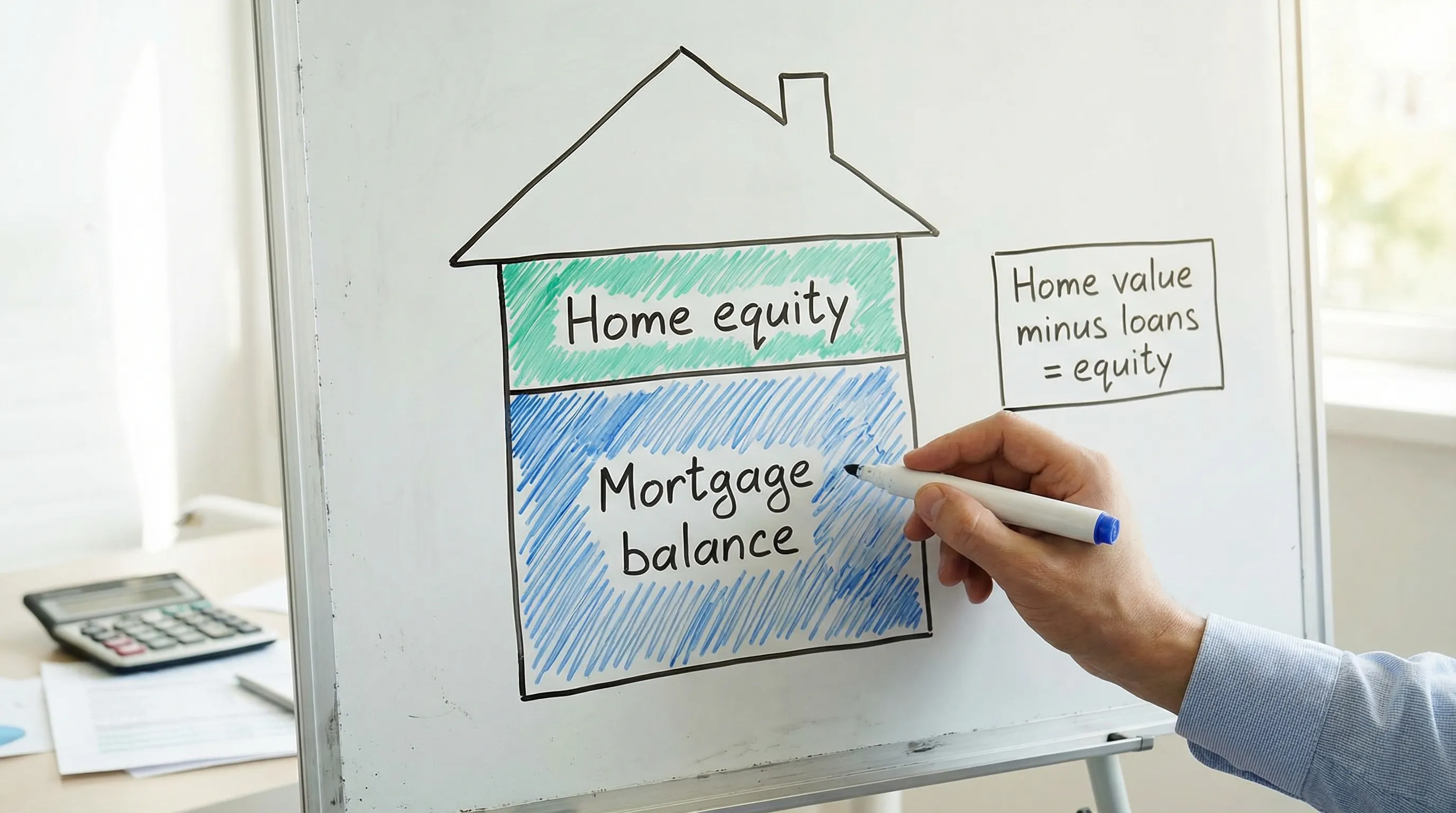

What is mortgage equity?

Mortgage equity is the portion of your home you truly “own” in dollar terms.

Equity = current home value − total loans secured by the home

Those loans usually include your primary mortgage, and may also include:

- A second mortgage (home equity loan)

- A HELOC balance

- Any other lien that must be paid off when you sell or refinance

Two important clarifications:

- Equity is not the same as cash. You typically need to borrow against it (or sell the home) to turn it into spendable money.

- Not all equity is usable equity. Most lenders will cap how much you can borrow based on loan-to-value (LTV) limits, credit, income, and the type of property.

How mortgage equity builds over time

Equity generally grows in three ways:

1) Your down payment (or initial equity)

If you buy a $400,000 home and put 10% down, you start with about $40,000 in equity (minus any financed fees or seller credits that affect the final numbers).

2) Paying down principal

With each monthly payment, a portion goes toward principal reduction (how much depends on your interest rate and where you are in the amortization schedule). Early in the loan, more of your payment typically goes to interest. Over time, principal paydown accelerates.

3) Home value changes and improvements

Market appreciation can build equity without you doing anything. Strategic improvements can also help, but upgrades do not always translate into dollar-for-dollar value. Appraisers look at market data and comparable sales, not your receipts.

If you want to follow the market side more closely, the FHFA House Price Index is a widely used public measure of U.S. home price trends.

How lenders decide how much equity you can use

When you “tap equity,” lenders focus less on your total equity and more on how much total debt your home will carry after the new loan.

Here are the most common concepts you will see:

Loan-to-value (LTV) and combined loan-to-value (CLTV)

- LTV compares your primary mortgage to the home’s value.

- CLTV compares all mortgages (first plus any second lien like a HELOC) to the home’s value.

Example:

If your home is worth $500,000 and you owe $325,000 on your first mortgage:

- LTV = $325,000 ÷ $500,000 = 65%

If you add a $50,000 HELOC balance:

- CLTV = ($325,000 + $50,000) ÷ $500,000 = 75%

Many equity products have maximum CLTV limits (often somewhere around 80% to 90% depending on the program, borrower profile, and property). The exact cap varies by lender and loan type, so treat any single number you see online as a guideline, not a promise.

The appraisal matters

Your “available equity” typically depends on the value used for underwriting, which is often a new appraisal (or another accepted valuation method, depending on the loan and lender). If the appraisal comes in lower than expected, your usable equity can shrink quickly.

Income, credit, and debt-to-income (DTI)

Equity alone does not guarantee approval. Lenders still evaluate whether the new payment fits your budget. The Consumer Financial Protection Bureau (CFPB) has a helpful overview of what lenders look at when evaluating affordability and ability to repay: Consumer Financial Protection Bureau.

The main ways to access mortgage equity (and what each is best for)

There is no single “best” way to use equity. The right option depends on your rate, how long you will keep the home, and whether you want a one-time lump sum or flexible access.

HELOC (home equity line of credit)

A HELOC is a revolving line of credit secured by your home. You can usually borrow, repay, and borrow again during the draw period, then repay during the repayment period.

A HELOC can make sense when:

- You want flexibility (for phased renovations, ongoing tuition payments, or a cash buffer)

- You plan to borrow only what you need, when you need it

Key watch-outs: HELOC rates are often variable, payments can rise, and it is easy to treat a line of credit like “extra income.”

(If you want a deeper HELOC-specific breakdown, New Era Lending has a separate explainer: An Overview of the HELOC System.)

Home equity loan (second mortgage)

A home equity loan is typically a lump sum with a fixed payment structure. It can be a fit when you have a defined, one-time cost (like a major repair) and want predictable payments.

Key watch-outs: you are locking in borrowing all at once, and you may pay interest on money you did not truly need.

Cash-out refinance

A cash-out refinance replaces your existing mortgage with a new one that is larger than what you currently owe, and you receive the difference in cash.

A cash-out refinance can make sense when:

- You want one loan instead of a first plus a second

- Your current mortgage terms are unfavorable for your goals

Key watch-outs: you reset the clock on your mortgage (unless you choose a shorter term), and you may give up a low existing rate. For a 2026-focused decision framework on refinancing, see: Refinance Rates for Mortgages: When to Refi in 2026.

Selling the home (or downsizing)

Sometimes the wisest way to “use equity” is not borrowing at all. Selling, downsizing, or relocating can convert equity to cash without adding a new monthly payment.

Reverse mortgage (for eligible homeowners)

For homeowners age 62+ who qualify, a reverse mortgage can convert a portion of equity into cash flow or a line of credit. This option has specific rules, costs, and long-term implications, so it is typically something to evaluate with extra care.

Smart ways to use mortgage equity (practical, not theoretical)

Equity is best used when it either:

- Improves your long-term financial position, or

- Solves a high-impact problem with a clear payoff plan

Here are use cases that tend to be “wise” when the numbers and your timeline support them.

Home improvements that protect or increase livability

Projects that address deferred maintenance (roof, HVAC, structural issues) often provide real value, even if they do not produce a perfect return on paper. Quality-of-life improvements can also be worth it if you plan to stay long enough.

Pro tip: have a scope, budget, and contingency plan before borrowing. Renovations are a common place where homeowners overdraw and then carry the balance longer than planned.

Consolidating high-interest debt (with guardrails)

Using equity to pay off high-interest debt can reduce your interest cost, but only if you stop the behavior that created the debt. Otherwise you can end up with both: new mortgage debt and fresh credit card balances.

A good guardrail is to pair consolidation with a written payoff schedule and a plan to reduce revolving credit usage.

Building a cash buffer for variable income (carefully)

For self-employed borrowers, a HELOC (even unused) can function like an emergency backstop. The key is to treat it as a contingency, not as money to spend.

Funding a business or side income (only if risk is contained)

Some homeowners consider using equity to buy equipment, inventory, or to smooth cash flow. This can work, but it is risk stacking: your home becomes tied to business performance.

If you are exploring resale or liquidation inventory, make sure you understand margins, shipping, and cash conversion cycles before borrowing. For example, if you want to learn how pallet liquidation purchasing works in practice, resources from suppliers like wholesale liquidation pallets from American Bulk Pallets can help you understand the buying and delivery model. Still, the safest approach is borrowing less than you qualify for and maintaining a cash reserve so your mortgage payment is never dependent on quick sales.

How to use mortgage equity wisely (a simple decision framework)

Before you apply for anything, get clear on the “why” and the “how it ends.” Equity is powerful because it is large and relatively low-cost compared to unsecured credit, but that is also why it can do more damage when mismanaged.

Use this framework to pressure-test your plan:

- Define the purpose in one sentence. “I am borrowing $X to do Y by date Z.” If you cannot write that, pause.

- Choose the right structure for your goal. Flexible project, consider a HELOC. Fixed one-time cost, consider a fixed second. Restructuring the whole mortgage, consider cash-out.

- Plan for worst-case payments. If the rate adjusts or the introductory period ends, can you still afford it?

- Borrow less than the maximum. A lender maximum is not a comfort limit, it is an underwriting limit.

- Keep a liquidity cushion. Even if you have equity, you need cash for emergencies because equity access can take time and requires approval.

- Compare total cost, not just rate. Look at fees, closing costs, and how long you will carry the balance.

Common mortgage equity mistakes to avoid

A few patterns show up repeatedly when homeowners regret tapping equity:

Treating equity like “found money.” Appreciation can reverse, and borrowing turns equity into required payments.

Using short-term debt for long-term lifestyle spending. If the purchase does not improve your balance sheet or reduce risk, think twice.

Ignoring lien priority and future flexibility. Adding a second lien can complicate a later refinance (the second lien may need to be subordinated).

Overlooking timing. If you may sell or move soon, closing costs and loan setup fees can outweigh the benefits.

When it makes sense to get a personalized equity plan

Online calculators are a good start, but a real equity decision usually needs a scenario comparison. It can be worth speaking with a mortgage professional when:

- You are choosing between a HELOC, home equity loan, and cash-out refinance

- You want to keep your current first mortgage rate and only borrow a smaller amount

- You are trying to lower overall monthly obligations (not just “get cash”)

- You are self-employed or have variable income

- You are a veteran evaluating VA-eligible options alongside conventional solutions

New Era Lending’s approach combines modern, tech-forward steps (secure document uploads and e-signature support) with human guidance, so you can compare options without guessing.

Frequently Asked Questions

What is mortgage equity in simple terms? Mortgage equity is the part of your home’s value that is not owed to lenders. It is your home value minus all loans secured by the property.

How do I calculate how much equity I can borrow? Lenders usually limit borrowing using LTV or CLTV. Usable equity depends on your home’s appraised value, your current loan balances, and program limits, plus your income and credit.

Is a HELOC or cash-out refinance better? A HELOC can be better for flexible, smaller, or phased borrowing. A cash-out refinance can be better when you want one loan or need to change your primary mortgage terms. The best choice depends on your current rate, timeline, and payment goals.

Can I use mortgage equity for debt consolidation? Yes, but it is only “wise” if it lowers your total cost and you have a plan to avoid re-accumulating high-interest debt. Otherwise you can end up with more debt, secured by your home.

Does tapping equity hurt my credit? Opening a new loan or line can affect your credit score temporarily due to inquiries and changes in utilization and total debt. The bigger issue is whether the new payment improves or strains your overall finances.

Do I need an appraisal to use home equity? Often yes, especially for larger amounts, but requirements vary by lender and loan type. The value used for underwriting is what drives your available equity.

Explore your options with New Era Lending

If you are thinking about using mortgage equity, the goal is not just to “get approved,” it is to choose a structure you can live with through rate changes, life changes, and market changes.

New Era Lending helps homeowners and buyers in 39 states compare equity solutions for refinancing, cash-out needs, and home purchases using a streamlined, secure process with personalized guidance. To get a clear recommendation based on your numbers and goals, visit New Era Lending and request a scenario review.