.jpg)

.jpg)

.jpg)

Mortgage Mortgage Loan: What It Means and Why It Shows Up

Seeing the phrase “mortgage mortgage loan” can feel like a glitch, or worse, like you are being pitched a product you have never heard of. In most cases, it is neither. It is usually a duplication that comes from how websites, search engines, or documents label and categorize financing.

Below is what the phrase typically means, why it shows up in the real world, and what you should pay attention to instead when you are shopping for a mortgage.

What a mortgage loan actually is (plain-English definition)

A mortgage loan is money you borrow to buy (or refinance) real estate, where the home is used as collateral. You repay the loan over time, usually monthly, and your payment commonly includes:

- Principal (the amount you borrowed)

- Interest (what the lender charges for lending)

- Taxes and homeowners insurance (often collected in an escrow account)

- Mortgage insurance (if required by the loan type and down payment)

If you have ever heard “home loan,” it is often used interchangeably with “mortgage loan” in everyday conversation.

For official definitions and consumer protections, the Consumer Financial Protection Bureau maintains a helpful glossary and guides for borrowers (including the Loan Estimate and Closing Disclosure you will receive when you apply). See the CFPB’s home loan resources at consumerfinance.gov.

So what does “mortgage mortgage loan” mean?

Usually, it means the same thing as mortgage loan, just with redundant wording.

It is rarely an actual loan product name. Instead, it tends to be a labeling artifact, something created by:

- Search engines and auto-suggestions

- Website categories and page titles

- Form fields that repeat a category name

- Document templates that combine two similar terms

In other words, “mortgage mortgage loan” is typically a phrase generated by systems, not by a loan officer.

Why “mortgage mortgage loan” shows up (the most common causes)

1) Search engines try to match many ways people ask the same thing

Search engines often expand and remix phrases based on what people type. If many people search “mortgage” and many people search “mortgage loan,” systems can end up generating combined variants like “mortgage mortgage loan.”

You might see it in:

- Google autocomplete suggestions

- Search results headlines that look slightly off

- Related searches at the bottom of a results page

This is not a sign the loan itself is unusual, it is usually just search behavior.

2) Web pages and SEO tags can repeat terms

Behind the scenes, websites use page titles, headings, breadcrumbs, and structured data (like schema markup) to describe content. If multiple fields are populated with similar text, the same word can appear twice.

Examples of where duplication can happen:

- A category named “Mortgage” plus a page titled “Mortgage Loan”

- A heading template that inserts the category automatically

- A site search result page that repeats the query as a label

3) Online forms and PDFs sometimes concatenate field labels

If you have ever filled out a form that exports to a PDF, you have seen odd formatting. Many mortgage workflows rely on templates that pull in labels like “Mortgage” and “Loan” from separate fields. When those fields are combined, you can get duplicated phrasing.

4) OCR and scanning errors can duplicate words

When paper documents are scanned and converted back into text (OCR, optical character recognition), repeated words are a common error, especially around headers.

5) Paid ads and keyword matching can create awkward combinations

In digital advertising, marketers may target both “mortgage” and “mortgage loan.” Depending on how an ad platform assembles headlines dynamically, the result can be repetitive language.

This is a formatting issue, not a separate kind of financing.

When duplication is harmless, and when it is a red flag

Most of the time, “mortgage mortgage loan” is harmless. Still, it can appear in places where you should be cautious.

Harmless contexts

- Search results, autocomplete, or “related searches”

- Blog categories and article tags

- Generic website navigation labels

- A form field label that looks duplicated

Potential red flags (slow down and verify)

Be more careful if the duplicated phrase appears inside a message asking for money or sensitive data. Watch for:

- Emails or texts urging you to “act now” and click a shortened link

- Requests for upfront payment by wire, gift card, or crypto

- A “lender” who will not provide a Loan Estimate after you apply

- A website that does not clearly show a licensed company identity, NMLS information, or a secure upload process

If something feels off, verify the company independently (do not use the phone number in the suspicious message). The FTC has guidance on spotting and reporting scams at ftc.gov.

What you should focus on instead of the wording

Whether the page says “mortgage,” “mortgage loan,” or “mortgage mortgage loan,” the loan you are being offered can be evaluated with a short list of fundamentals.

1) Interest rate vs. APR

The interest rate affects your payment, while the APR reflects the rate plus many lender costs over time. APR is often more useful for comparing offers that include different fees or points.

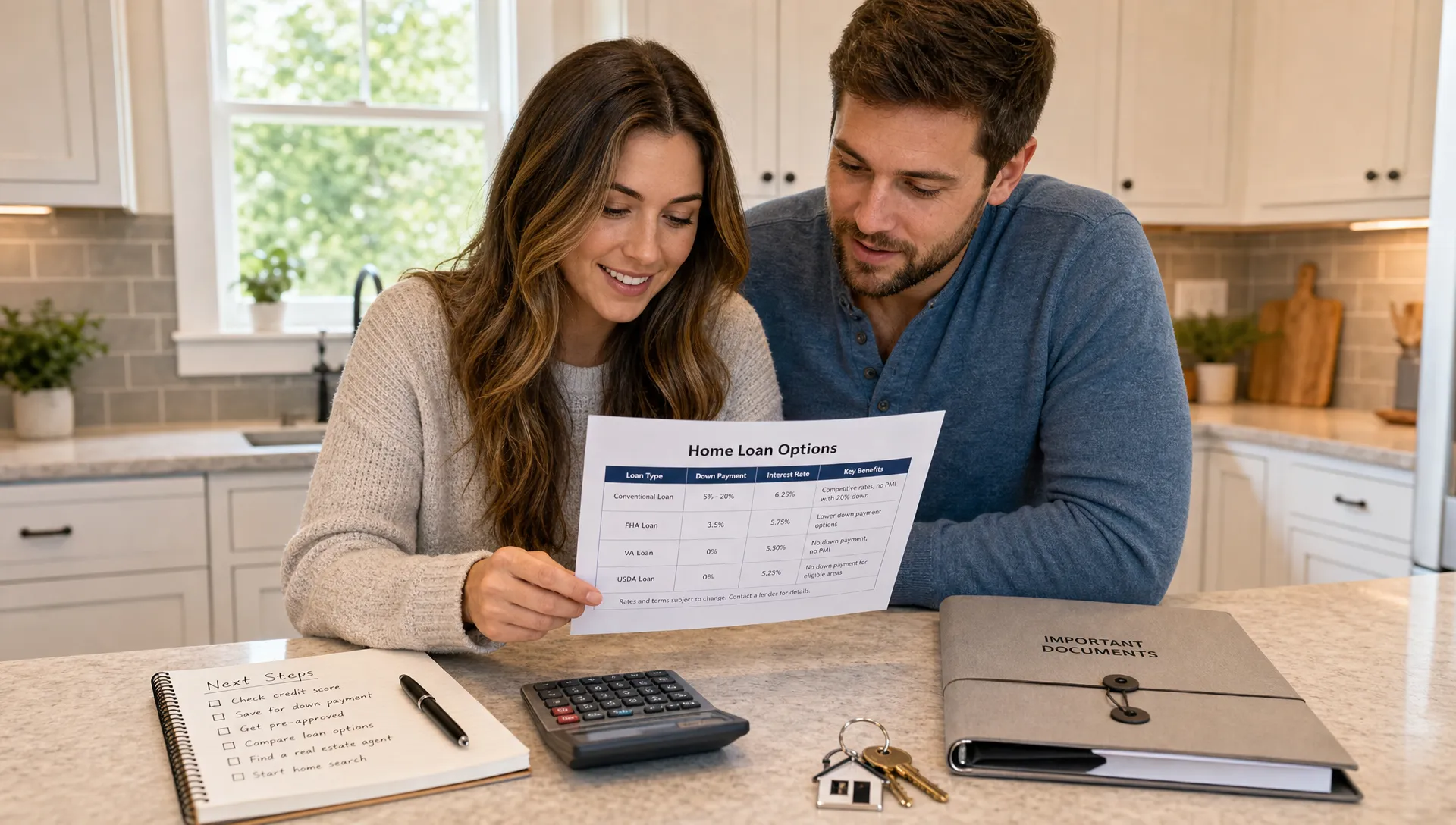

2) Loan type and program rules

The biggest differences in cost and qualification usually come from the program itself, for example conventional vs. FHA vs. VA, and whether mortgage insurance applies.

3) Term length and payment comfort

A 30-year and 15-year loan can have very different payments and interest totals, even with the same rate.

4) Cash to close

Two offers can have the same rate but different cash requirements due to points, lender fees, credits, and prepaid items.

5) Your timeline and your “exit plan”

If you may sell or refinance in a few years, paying high upfront costs to get a slightly lower rate might not pencil out.

If you want a deeper comparison across loan programs (without getting lost in jargon), New Era Lending has a helpful overview here: Mortgage loan options: a simple guide for every buyer.

A quick way to ask better questions (and get clearer quotes)

When you talk with a lender, the fastest way to cut through confusing labels is to ask for side-by-side scenarios. You can keep it simple:

- “Can you quote this as a 30-year fixed and as an ARM, with the same down payment?”

- “What is the APR, and how much of the cost is points vs. lender fees?”

- “How much cash do I need at closing, and what could make that number change?”

- “Is mortgage insurance required, and what would it take to remove it?”

- “If I keep the home for three to five years, which option usually wins?”

The goal is to compare offers based on structure and total cost, not on whatever label a search engine or form field happened to generate.

Why this matters even more if you are building or buying a modular home

If you are purchasing new construction, a modular build, or a custom project, you may see even more odd phrasing online because the financing categories multiply (construction-to-permanent, renovation, land loans, end loans, and more).

For example, some buyers explore energy-efficient modular builds with fixed pricing and timelines, like Hubley’s modular home process (Belgium-based). Even if you are buying in the US, it is a useful reference point for how modular projects can be structured and why financing discussions sometimes include multiple “loan” labels.

In these cases, clarity matters because the right loan structure depends on when funds are needed, what the property will look like at completion, and how appraisals and inspections are handled.

How New Era Lending helps simplify the process

Confusing terminology is common in mortgage shopping because you are navigating regulation, underwriting, pricing, and a lot of documentation. The practical fix is a process that combines:

- Modern tools that make it easier to submit documents securely and review scenarios

- Human guidance that translates tradeoffs into real numbers tied to your goals

New Era Lending provides technology-driven mortgage solutions for purchase, refinance, and equity access, with personalized guidance, transparent terms, and support across 39 states. If you want to pressure-test options side-by-side, start here: New Era Lending | Smart Mortgage Solutions Made Simple.

Frequently Asked Questions

Is “mortgage mortgage loan” a real type of mortgage? In almost all cases, no. It is usually duplicated wording created by search engines, web page templates, ads, or form fields.

Should I be worried if I see “mortgage mortgage loan” on a website? Not necessarily. If it appears in search results, a page title, or navigation labels, it is typically harmless. Be cautious if it shows up in a message asking for sensitive data or upfront payment.

What should I compare if the wording is confusing? Compare the Loan Estimate details: interest rate, APR, loan program, term, cash to close, mortgage insurance, and any points or credits.

How do I know if a lender quote is legitimate? A legitimate lender can provide a written Loan Estimate after you apply, explain fees clearly, and verify identity and licensing. Avoid anyone pushing you to pay upfront by unusual methods.

Ready to turn “weird wording” into clear numbers?

If you are seeing terms like “mortgage mortgage loan” and you just want to know what your real options are, New Era Lending can walk you through purchase or refinance scenarios in plain language, backed by smart tools and a guided process.

Explore your next step at New Era Lending and get a clear comparison built around your goals, not confusing labels.