.jpg)

.jpg)

.jpg)

How to Get a Lower Rates Mortgage Offer

A lower mortgage rate can make a home purchase feel more affordable, reduce the lifetime cost of a loan, or improve the math on a refinance. But getting a lower rates mortgage offer is not as simple as finding the lowest number in an online ad. Mortgage pricing changes daily, and the offer you receive depends on your credit profile, loan type, property details, down payment, timing, and the way fees are structured.

The good news is that many of the biggest rate drivers are within your control. You may not be able to move the broader bond market, but you can prepare your application, compare quotes correctly, and ask the right questions before you lock.

Below is a practical, borrower-friendly guide to improving your chances of receiving a lower mortgage rate without overlooking costs that can come back later.

Understand what actually affects your mortgage rate

Mortgage rates are shaped by two categories of factors: market conditions and borrower-specific risk.

Market conditions include inflation expectations, bond yields, Federal Reserve policy, investor demand for mortgage-backed securities, and overall economic uncertainty. These factors can move rates even when nothing about your personal finances changes. Freddie Mac’s Primary Mortgage Market Survey is one commonly referenced source for tracking broad mortgage rate trends.

Borrower-specific factors are the pieces a lender evaluates when pricing your actual loan. These can include your credit score, debt-to-income ratio, loan amount, down payment or home equity, property type, occupancy, loan program, and whether you pay points.

That is why two borrowers can apply on the same day and receive different offers. It is also why an advertised rate may not match the rate available for your specific scenario. If you want a deeper breakdown of the pricing layers behind a quote, New Era Lending’s guide on how home mortgage loan rates are priced explains the moving parts in more detail.

Check your credit before lenders do

Your credit profile is one of the most important rate factors because it helps lenders estimate risk. A stronger credit score can improve your pricing, while late payments, high balances, or unresolved errors may push your offer higher.

Before you apply, review your credit reports for mistakes. You can access free reports through AnnualCreditReport.com, the federally authorized source for free credit reports from the three major bureaus. Look for accounts you do not recognize, incorrect late payments, outdated balances, duplicate collections, or personal information errors.

Then focus on the credit factors that tend to matter most:

- Paying every account on time before and during the mortgage process

- Reducing revolving credit card balances where possible

- Avoiding new credit inquiries unless necessary

- Keeping older accounts open if they support your credit history

- Resolving reporting errors as early as possible

Do not assume a small score improvement is meaningless. Mortgage pricing often changes at credit score bands, so moving into a higher band may affect your offer. The exact impact depends on the loan program, market conditions, and lender pricing at the time you apply.

Lower your debt-to-income ratio if you can

Your debt-to-income ratio, often called DTI, compares monthly debt obligations to gross monthly income. Lenders use it to evaluate whether the proposed mortgage payment fits comfortably within your financial picture.

A lower DTI can help you qualify more confidently and may open the door to more loan options. It can also reduce the chance that your file needs extra conditions or manual explanations during underwriting.

Common ways to improve DTI before applying include paying down credit cards, eliminating small installment debts, avoiding new auto loans or personal loans, and documenting all eligible income accurately. If you receive bonuses, commissions, overtime, retirement income, self-employment income, or rental income, ask early what documentation may be needed. Sometimes the issue is not income itself, but whether the lender can verify and count it under program guidelines.

If you are buying, your target price range also matters. A slightly lower purchase price, larger down payment, or smaller loan amount can reduce the projected payment and improve your DTI.

Strengthen your down payment, equity, and reserves

For purchase loans, a larger down payment can sometimes help you receive a better offer because it lowers the loan-to-value ratio. For refinances, the equivalent factor is equity. More equity can reduce lender risk and may improve available pricing.

That said, putting every available dollar into the down payment is not always wise. You still need enough cash for closing costs, moving expenses, repairs, emergency reserves, and normal life. A lower rate is helpful, but not if it leaves your budget too tight after closing.

Cash reserves can also strengthen your file. Having money left over after closing shows that you are not stretched to the limit. For some borrowers, reserves may be especially important when income is variable, the property is an investment property, or the loan scenario is more complex.

The goal is not simply to maximize the down payment. The goal is to find the right balance between rate, payment, closing costs, and financial safety.

Choose the right loan program for your situation

There is no universal lowest-rate mortgage for every borrower. The right program depends on your eligibility, credit profile, down payment, occupancy, property type, and long-term plans.

Conventional loans may be competitive for borrowers with strong credit and sufficient down payment. FHA loans may be useful for borrowers who need more flexible credit or down payment guidelines. VA loans can be especially valuable for eligible veterans, service members, and surviving spouses because they may offer strong terms and no required down payment, subject to eligibility and program rules. USDA loans may be an option for eligible rural properties and borrowers.

Loan term also matters. A 15-year mortgage often has a lower interest rate than a 30-year mortgage, but the monthly payment is higher because the balance is paid off faster. Adjustable-rate mortgages may start with lower initial rates, but they introduce future rate adjustment risk, so they only make sense when the structure fits your time horizon and comfort level.

This is where personalized guidance matters. A lower advertised rate on the wrong program may cost more over time than a slightly higher rate on a loan that fits your goals, cash flow, and timeline.

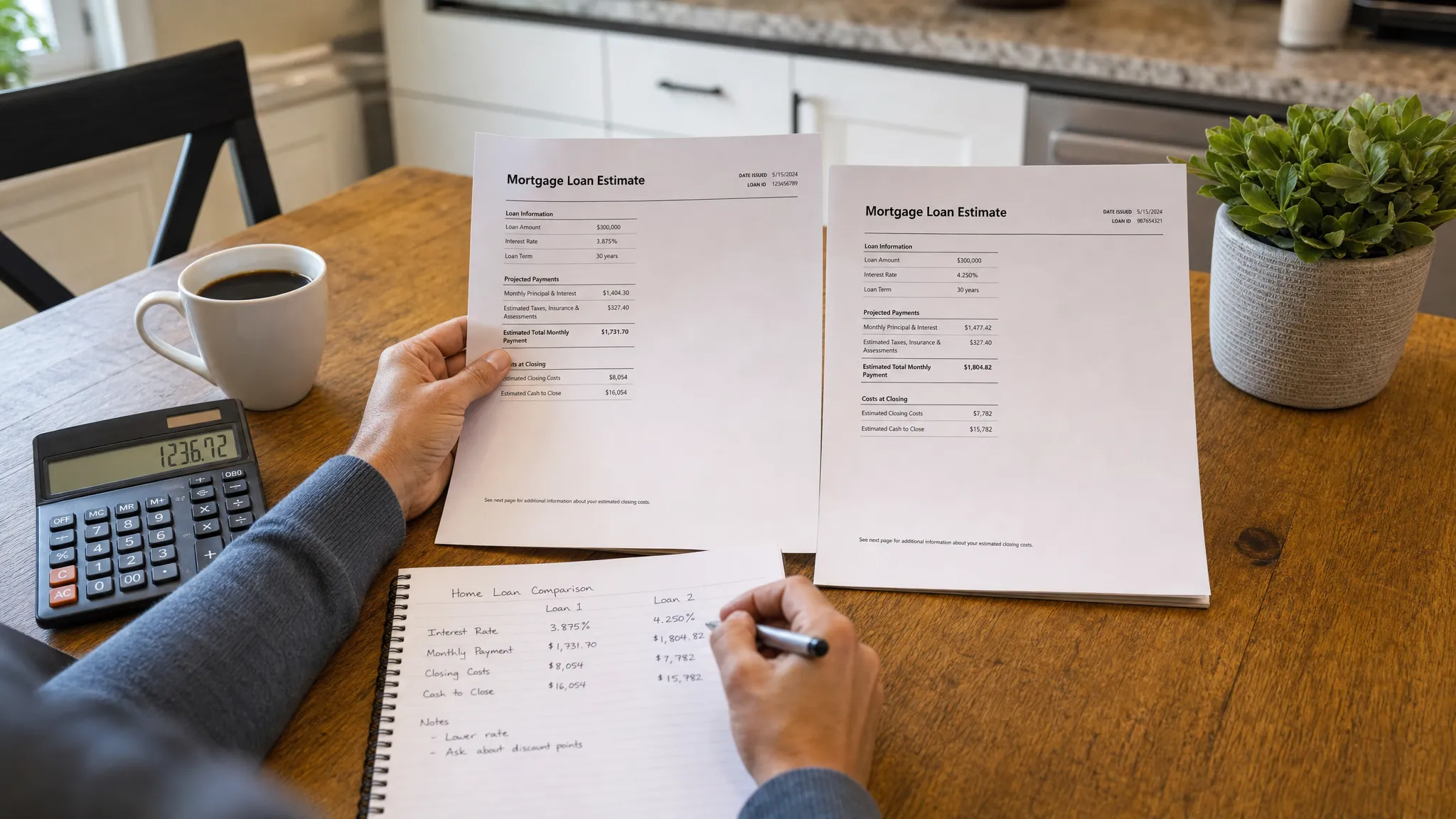

Compare quotes using the same assumptions

One of the biggest mistakes borrowers make is comparing mortgage offers that are not built on the same assumptions. A quote with points is not the same as a quote without points. A 45-day lock is not the same as a 30-day lock. A conventional quote is not the same as an FHA or VA quote. Even small differences in loan amount, down payment, taxes, insurance, or escrow assumptions can distort the comparison.

When shopping, try to request quotes on the same day using the same basic scenario. Mortgage pricing can change quickly, so a quote from Monday may not be directly comparable to a quote from Thursday.

The Consumer Financial Protection Bureau explains that the standardized Loan Estimate is designed to help borrowers compare key loan terms and costs. Review the interest rate, APR, monthly principal and interest, estimated taxes and insurance, loan costs, lender credits, cash to close, and whether the rate is locked.

New Era Lending also has a helpful guide on how to compare lower rate loans without surprises, which is especially useful if two offers look similar at first glance.

Ask lenders what would make the offer lower

You do not have to guess which factors are affecting your quote. Ask directly.

A good mortgage conversation should help you understand what is driving the rate and what options exist. You might ask:

- What credit score range is this pricing based on?

- Would a larger down payment or lower loan amount change the rate?

- Are there discount points included in this quote?

- What would the rate look like with no points?

- Are lender credits available if I prefer lower cash to close?

- How long is the rate lock, and what happens if closing is delayed?

- Is another loan program worth comparing for my situation?

These questions help separate a true lower-rate offer from one that only looks lower because the costs are shifted elsewhere.

Be careful with discount points

Discount points are upfront fees paid to reduce the interest rate. One point typically equals 1% of the loan amount, although the rate reduction varies by market, lender, and loan scenario.

Points can make sense if you plan to keep the loan long enough to recover the upfront cost through monthly savings. They may not make sense if you expect to sell, refinance, or pay off the loan before reaching the break-even point.

For example, if paying points costs several thousand dollars and saves a modest amount each month, you need to calculate how many months it takes to break even. If that break-even period is longer than you realistically expect to keep the loan, the lower rate may not be worth it.

This is the core principle behind smart rate shopping: the lowest rate is not always the best deal. If you are trying to reduce costs while protecting your cash flow, review New Era Lending’s article on how to lower rates without hurting your budget.

Time your rate lock thoughtfully

A rate quote is not fully secure until it is locked according to the lender’s lock policy. Until then, market changes can move the rate up or down.

The right time to lock depends on your closing timeline, risk tolerance, and the lender’s available lock periods. A shorter lock may cost less, but it may not be long enough if your closing is uncertain. A longer lock can provide more protection, but it may come with different pricing.

If you are buying, coordinate the lock with your purchase contract, appraisal timeline, and expected closing date. If you are refinancing, make sure your documentation is ready so the file can move efficiently once you lock.

Also ask whether the lender offers any float-down option. Not all lenders do, and terms vary, but it is worth understanding what happens if rates improve after you lock.

Keep your financial profile stable until closing

Getting a lower mortgage offer is only part of the process. You also need to protect that offer until the loan closes.

After application and especially after pre-approval, avoid major financial changes unless your loan advisor says they are safe. Do not open new credit cards, finance furniture, change jobs without discussing it, make large unexplained deposits, co-sign a loan, or move money between accounts without keeping a clear paper trail.

Even if a change seems minor, it can affect underwriting, DTI, available cash, or final approval. Lenders typically re-check parts of your financial profile before closing, so stability matters.

A faster, more organized process can also help reduce stress. Secure document uploads, e-signature support, and responsive guidance can make it easier to provide conditions quickly and keep your closing timeline on track.

Consider buying power, not just rate

A lower rate matters because it affects your payment and long-term cost. But the best mortgage offer is the one that supports your overall financial goal.

For a homebuyer, that may mean keeping the monthly payment comfortable, preserving emergency savings, and closing on time. For a homeowner refinancing, it may mean lowering the payment, shortening the term, removing mortgage insurance, accessing equity, or improving cash flow.

Before choosing an offer, compare the full picture: monthly payment, cash to close, APR, loan term, points, credits, escrow assumptions, mortgage insurance, prepayment terms, and how long you expect to keep the loan.

If a lender can explain those tradeoffs clearly, you are in a stronger position to decide whether a lower rate is truly better.

A simple checklist before you request offers

Before you start shopping for a mortgage quote, take a little time to prepare. A clean, complete borrower profile can make your quotes more accurate and easier to compare.

Use this checklist as a starting point:

- Review your credit reports and address errors early

- Pay down revolving balances where practical

- Avoid new debt before and during the mortgage process

- Gather income, asset, tax, and identity documents

- Decide your target payment, not just your target price

- Ask for quotes using the same loan amount, term, and lock period

- Compare Loan Estimates, not only advertised rates

- Calculate the break-even point before paying points

- Keep finances stable until closing

Preparation does not guarantee the lowest possible rate, but it can improve your odds of receiving a stronger, cleaner offer.

Frequently Asked Questions

What is the fastest way to get a lower mortgage rate? The fastest practical steps are often improving your credit card utilization, comparing multiple offers on the same day, asking about points and credits, and choosing the loan program that fits your profile. Market timing can help or hurt, but preparation gives you more control.

Does a higher credit score always mean a lower mortgage rate? A higher score can improve pricing, but it is not the only factor. Lenders also consider loan-to-value ratio, DTI, property type, occupancy, loan amount, term, and program guidelines.

Should I pay points to get a lower rate? Paying points may be worthwhile if the monthly savings exceed the upfront cost within the time you expect to keep the loan. If you may sell or refinance soon, a no-point or lower-cost option may be better.

Can I negotiate a mortgage rate? You can often ask a lender to review pricing, compare a competing Loan Estimate, adjust points or credits, or evaluate another loan program. The lender may not always be able to reduce the rate, but asking specific questions can reveal better options.

Is the lowest mortgage rate always the best offer? Not necessarily. A lower rate can come with higher upfront costs, longer lock fees, points, or different loan terms. Compare the total cost, cash to close, monthly payment, APR, and your expected time in the loan.

Get a clearer path to a lower mortgage offer

A better mortgage offer starts with the right preparation and the right guidance. New Era Lending combines modern mortgage technology with personalized human support to help borrowers purchase, refinance, or access equity with more confidence.

If you want help comparing loan options, understanding rates and terms, or preparing a stronger application, connect with New Era Lending and take the next step toward a smarter mortgage decision.