.jpg)

.jpg)

.jpg)

How to Compare Lower Rate Loans Without Surprises

A lower interest rate can be exciting, especially when you are buying a home, refinancing, or trying to reduce your monthly mortgage payment. But the lowest number on an ad is not always the lowest-cost loan. Some lower rate loans come with higher upfront fees, points, stricter terms, or assumptions that may not match your real financial picture.

The key is not to chase the lowest rate in isolation. It is to compare offers in a way that shows the true cost, the monthly impact, and the risks before you sign. That means looking at the Loan Estimate, APR, points, cash to close, rate lock terms, and how long you realistically plan to keep the loan.

Below is a practical framework to help you compare lower rate loans without surprises.

Start With the Same Loan Scenario

Before you compare lenders, make sure each quote is based on the same assumptions. A small change in loan amount, down payment, credit score, property type, or loan term can change the rate and fees.

For example, one lender may quote a 30-year fixed mortgage with discount points, while another may quote the same rate without points but with a larger lender fee. One offer may assume a higher credit score or a larger down payment. If you compare those offers as if they are identical, the “best” deal may be misleading.

When requesting quotes, keep these details consistent:

- Loan purpose, such as purchase, rate-and-term refinance, cash-out refinance, or equity access

- Loan amount and estimated home value or purchase price

- Down payment or current equity

- Credit score range

- Property type and occupancy, such as primary residence, second home, or investment property

- Loan term, such as 15, 20, or 30 years

- Rate type, such as fixed-rate or adjustable-rate

- Desired lock period

This gives you a cleaner side-by-side comparison and reduces the chance of hidden differences.

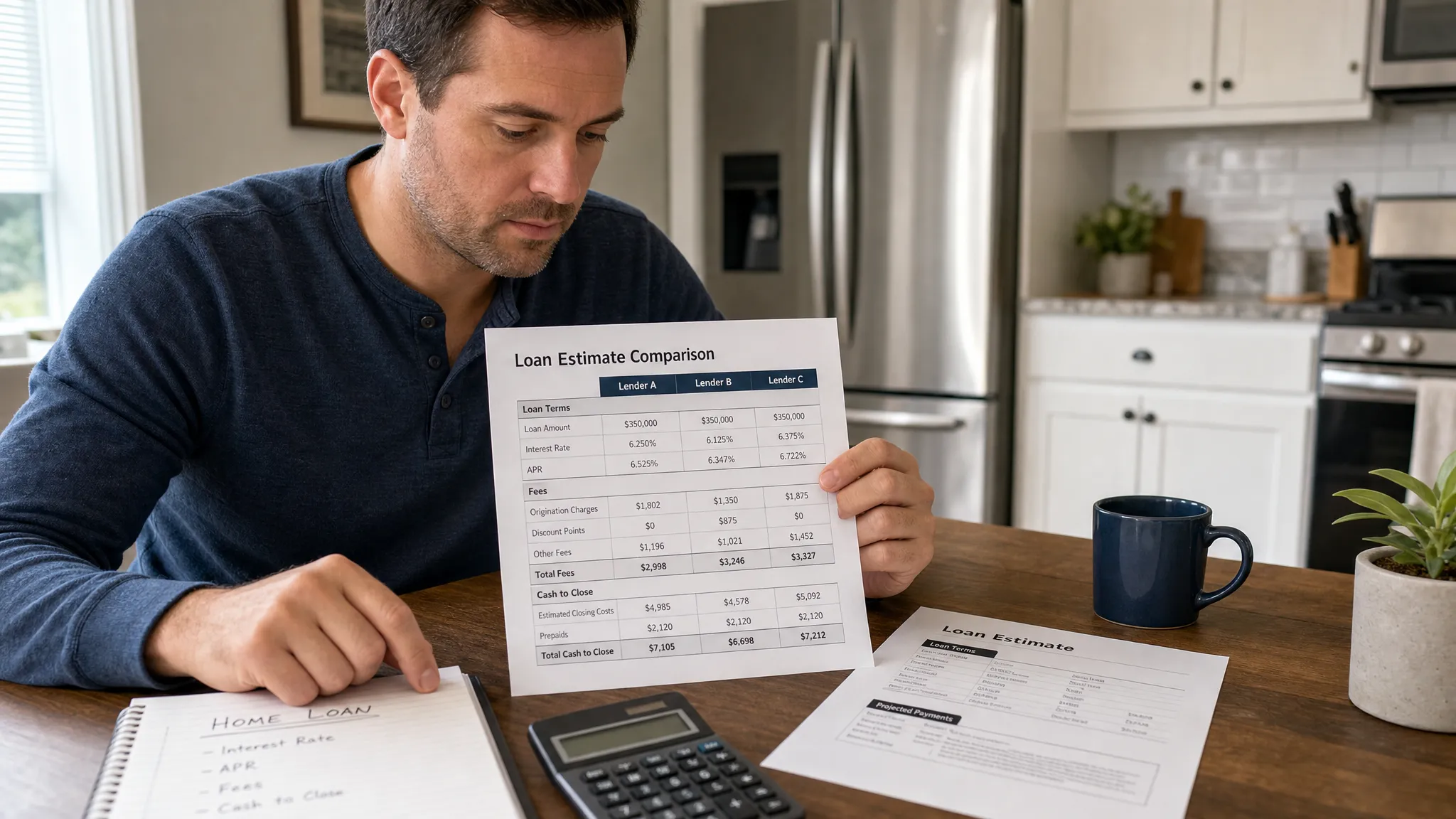

Use the Loan Estimate as Your Main Comparison Tool

Once you apply, lenders are generally required to provide a standardized Loan Estimate. The Consumer Financial Protection Bureau explains that this document is designed to help borrowers compare loan offers using the same format.

The Loan Estimate is important because it separates the interest rate from other costs. That matters because a low rate can be paired with higher upfront charges, while a slightly higher rate may have fewer closing costs.

Focus on these sections first:

Loan Estimate section | What to review | Why it matters

Page 1, Loan Terms | Interest rate, monthly principal and interest, prepayment penalty, balloon payment | Shows the basic structure and potential risks

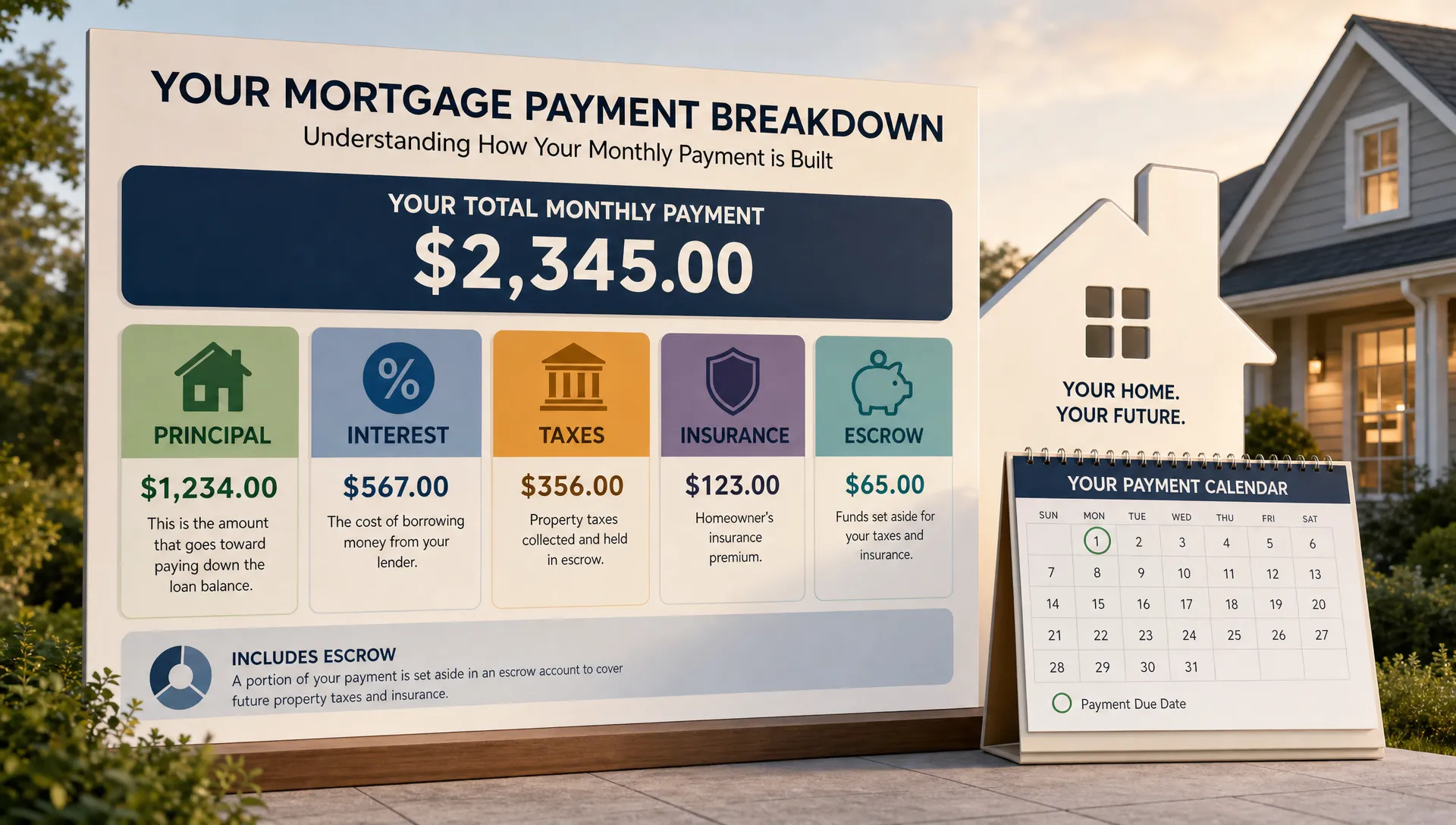

Page 1, Projected Payments | Full estimated monthly payment, including taxes, insurance, and mortgage insurance if applicable | Helps you compare real monthly affordability

Page 2, Loan Costs | Origination charges, points, underwriting, processing, and third-party fees | Reveals what you pay to get the rate

Page 2, Other Costs | Taxes, prepaid interest, homeowners insurance, escrow setup | Affects cash to close

Page 3, Comparisons | APR, total interest percentage, amount paid in 5 years | Helps compare longer-term cost Compare the Interest Rate and APR Together

The interest rate tells you how much interest accrues on the loan balance. APR, or annual percentage rate, includes the interest rate plus certain loan costs expressed as a yearly percentage.

A lower interest rate with a much higher APR can signal that the lender is charging more upfront to deliver that rate. That is not always bad, but it changes the decision. Paying more upfront may make sense if you plan to keep the loan long enough to recover the cost through monthly savings. It may not make sense if you expect to sell, refinance again, or pay off the loan soon.

A simple way to think about it:

Offer type | What it may mean | Best fit

Lower rate, higher upfront cost | You are buying down the rate with points or fees | Borrowers who expect to keep the loan for many years

Slightly higher rate, lower upfront cost | You preserve cash at closing | Borrowers who value flexibility or may move sooner

Similar rate and APR across offers | Costs are relatively aligned | Easier to compare based on service, speed, and loan termsUnderstand Points Before You Pay for a Lower Rate

Discount points are upfront fees paid to reduce your mortgage rate. One point usually equals 1% of the loan amount. For example, one point on a $350,000 loan would cost $3,500.

Points can be helpful, but they are not automatically a bargain. The question is whether the monthly savings justify the upfront cost.

To evaluate points, calculate the break-even period:

Example | Amount

Cost of points | $3,500

Monthly savings from lower rate | $100

Break-even period | 35 monthsThis is one reason lower rate loans should always be compared based on both upfront and long-term costs. A lower rate can be smart when it fits your timeline. It can be expensive when it does not.

Look Beyond Principal and Interest

Many borrowers compare only the principal and interest payment. That is understandable, but it is not the full monthly housing cost.

Your projected payment may also include:

- Property taxes

- Homeowners insurance

- Mortgage insurance

- HOA dues, if applicable

- Escrow shortages or future escrow adjustments

Taxes and insurance can change over time, and escrow estimates are not guarantees. If one lender’s quote shows a lower monthly payment because taxes or insurance are estimated differently, the loan may not actually be cheaper.

For a more complete affordability picture, compare the full projected payment and review how much cash you need after closing. If a lower rate requires you to drain your reserves, it may create stress later.

Watch the Cash-to-Close Number

Cash to close is the estimated amount you need to bring to settlement. It includes your down payment, closing costs, prepaid items, escrow setup, and credits.

A loan with a lower monthly payment may require significantly more cash to close. That can be fine if you have strong reserves, but it may not be ideal if it leaves you without enough savings for moving costs, repairs, furniture, medical needs, or family support.

This is especially important when home financing is part of a bigger life transition. For example, some borrowers are buying a home that supports aging relatives, relocating to be closer to family, or budgeting for outside support such as professional home care services when planning long-term household expenses. Your mortgage decision should leave room for real life, not just the loan itself.

When comparing cash to close, separate the costs into three groups:

Cost category | Examples | How to compare

Lender-controlled costs | Origination fees, discount points, lender credits | Compare closely because these vary by lender

Third-party costs | Appraisal, title, credit report, recording fees | Some variation is normal, but large differences deserve questions

Prepaids and escrow | Insurance, prepaid interest, property tax escrows | These may be timing-related and not true lender savings Check the Rate Lock Details

Mortgage rates can change daily, and sometimes more often. A quoted rate is not the same as a locked rate unless the lender confirms it is locked.

Ask these questions before assuming a lower rate is secure:

- Is the rate locked or floating?

- How long is the lock period?

- Is there a cost for the lock?

- What happens if the loan takes longer than expected?

- Is there a float-down option if market rates improve?

- What loan terms or property conditions could affect the locked rate?

A very low quote with a short lock period may not help if your closing timeline is longer. A slightly higher rate with a lock that matches your purchase contract or refinance schedule may be safer.

If you want to understand why rate offers can change from one borrower to another, New Era Lending explains key pricing factors in this article on how home mortgage loan rates are priced.

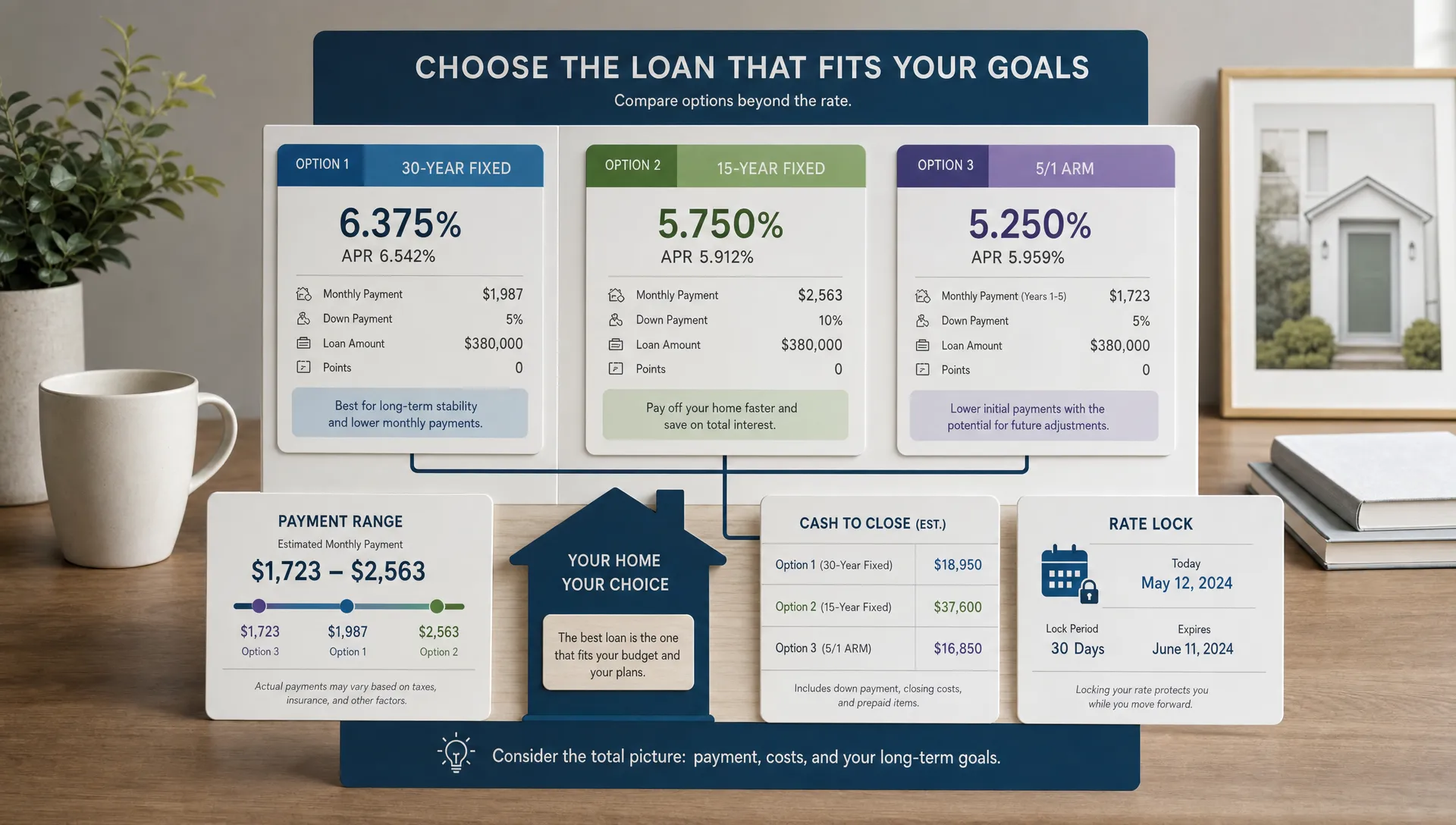

Compare Loan Type and Term, Not Just Rate

Lower rate loans can look attractive because the rate is lower than another option, but the loan structure may be different.

A 15-year fixed loan often has a lower rate than a 30-year fixed loan, but the monthly payment is usually higher because the balance is repaid faster. An adjustable-rate mortgage may start with a lower initial rate, but the payment can change later. A refinance may lower your payment by extending the term, but that can increase total interest paid over the life of the loan.

Here is how common structures differ:

Loan structure | Potential advantage | Possible surprise

30-year fixed | Predictable payment and lower monthly cost than shorter terms | More total interest over time

15-year fixed | Faster payoff and often lower rate | Higher monthly payment

Adjustable-rate mortgage | Lower initial rate in some markets | Payment can rise after the fixed period

Cash-out refinance | Access to equity while replacing the current mortgage | Larger loan balance and closing costs

No-cost or low-cost refinance | Lower upfront cost | Costs may be built into a higher rate or loan balanceCalculate the Break-Even Point for a Refinance

If you are comparing lower rate loans for a refinance, the break-even point is one of the most important numbers.

The formula is simple:

Total refinance costs divided by monthly savings equals months to break even.

If the refinance costs $6,000 and saves $200 per month, the break-even point is 30 months. If you expect to keep the loan longer than that, the refinance may make sense. If you may move or refinance again sooner, it may not.

But monthly savings are not the only goal. Some borrowers refinance to shorten the term, remove mortgage insurance, switch from an adjustable rate to a fixed rate, or access equity. In those cases, the break-even calculation should be considered alongside the broader reason for refinancing.

For homeowners focused specifically on refinancing, this guide to comparing refinance lenders and terms can help you evaluate offers with more confidence.

Ask About Fees That Can Change

Some closing costs are more predictable than others. Others can change due to timing, property details, title issues, or changes in your application.

Ask your lender which costs are fixed, which are estimates, and what could cause changes. You should also ask whether your loan has any of the following:

- Prepayment penalty

- Balloon payment

- Temporary buydown terms

- Mortgage insurance requirements

- Escrow waiver fee

- Extension fee if the rate lock expires

- Reinspection or appraisal update fee

These are not always present, but it is better to ask before closing than to discover a condition late in the process.

Evaluate the Lender Experience

Rate and cost matter, but so does execution. A lender who communicates clearly, reviews documents early, and explains tradeoffs can help prevent last-minute surprises.

This is especially important in a purchase transaction, where delays can affect your contract, moving plans, and closing date. In a refinance, poor communication can still cost time and create uncertainty around your rate lock.

When comparing lenders, consider:

- How clearly they explain the quote

- Whether they provide a written Loan Estimate

- How quickly they respond to questions

- Whether they explain tradeoffs instead of pushing one option

- Whether technology makes document uploads and signatures easier

- Whether you still have access to human guidance when decisions get complex

New Era Lending combines a technology-driven mortgage process with personalized guidance, giving borrowers a clearer way to compare purchase, refinance, and equity-access options across the states where it operates.

A Simple Checklist Before Choosing a Lower Rate Loan

Before you commit, confirm these details in writing:

- The interest rate and APR

- Whether the rate is locked and for how long

- The cost of points, if any

- Total lender fees

- Estimated third-party costs

- Cash to close

- Full projected monthly payment

- Loan term and rate type

- Break-even point, if refinancing

- Any prepayment penalty, balloon payment, or adjustable-rate terms

If two offers are close, do not decide by rate alone. Choose the offer that provides the clearest total cost, the right payment structure, and the fewest uncertainties for your situation.

Frequently Asked Questions

Are lower rate loans always cheaper? Not always. A lower rate may come with higher points, lender fees, or cash-to-close requirements. Compare APR, total loan costs, and your expected time in the loan before deciding.

What is more important, interest rate or APR? Both matter. The interest rate affects your monthly principal and interest payment, while APR reflects certain loan costs in addition to the rate. APR is useful for comparison, but your timeline also matters.

Should I pay points to get a lower mortgage rate? Paying points can make sense if the monthly savings exceed the upfront cost over the time you keep the loan. Calculate the break-even period before choosing that option.

Can a lender change my quoted rate? A quote can change if it is not locked, if market rates move, or if application details change. Ask whether the rate is locked, how long the lock lasts, and what conditions apply.

How many loan offers should I compare? Comparing at least two or three written offers can help you understand the market and identify unusual fees or terms. Make sure each quote uses the same loan scenario.

Compare With Clarity Before You Commit

Lower rate loans can create real savings, but only when the full terms support your goals. The safest approach is to compare written estimates side by side, ask direct questions, and look beyond the headline rate.

If you are buying, refinancing, or exploring equity options, New Era Lending can help you review your choices with smart tools, transparent guidance, and a mortgage process designed to feel simpler from start to finish.