.jpg)

.jpg)

.jpg)

Home Purchase Loans: How to Choose the Best Option in 2026

Buying a home in 2026 can feel like you are making 20 decisions at once: price, neighborhood, inspection, negotiations, and, quietly in the background, the financing choice that can swing your monthly payment and long-term cost for years.

The good news is that “the best” home purchase loan is not a mystery product. It is usually the loan that best fits your cash-to-close, your credit and income profile, your timeline, and your risk tolerance for payments changing.

Below is a practical framework you can use to choose among home purchase loans in 2026, without getting lost in jargon or lender sales pitches.

What “best” means for home purchase loans in 2026

Most buyers are trying to optimize some combination of these four outcomes:

- Approval confidence: Will this loan type and this lender actually close on time?

- Cash-to-close: Down payment plus closing costs, plus any appraisal gap you might need in a tight market.

- Monthly payment stability: Fixed payment versus the possibility of payment changes later.

- Total cost: Interest rate, mortgage insurance, upfront fees (including points), and how long you plan to keep the home.

A loan with the lowest interest rate is not always the best option if it requires high upfront points, comes with mortgage insurance that is hard to remove, or introduces payment risk you cannot comfortably absorb.

Step 1: Get clear on your “buy box” numbers

Before you compare lenders or loan programs, lock down the inputs that matter most in underwriting.

Start with these four borrower factors

Credit profile (not just score). Your score matters, but so do recent late payments, collections, utilization, and the depth of your credit history.

Debt-to-income (DTI). DTI is one of the most common reasons buyers are surprised during underwriting. If you are close to a lender’s DTI limit, your best loan option may be the one that keeps your payment lower (or allows more flexibility).

Cash-to-close and reserves. Many buyers focus only on down payment and forget reserves. Even when reserves are not strictly required, having them can expand your options and improve approvals.

Time horizon. The “right” loan often changes if you plan to move in 3 to 5 years versus staying for 10+.

If you are self-employed, the “numbers first” step is even more important because income calculations can differ from what you see on your tax return. If that is your situation, this guide can help you anticipate lender documentation and qualifying rules: How to Qualify For a Self-Employed Mortgage Loan.

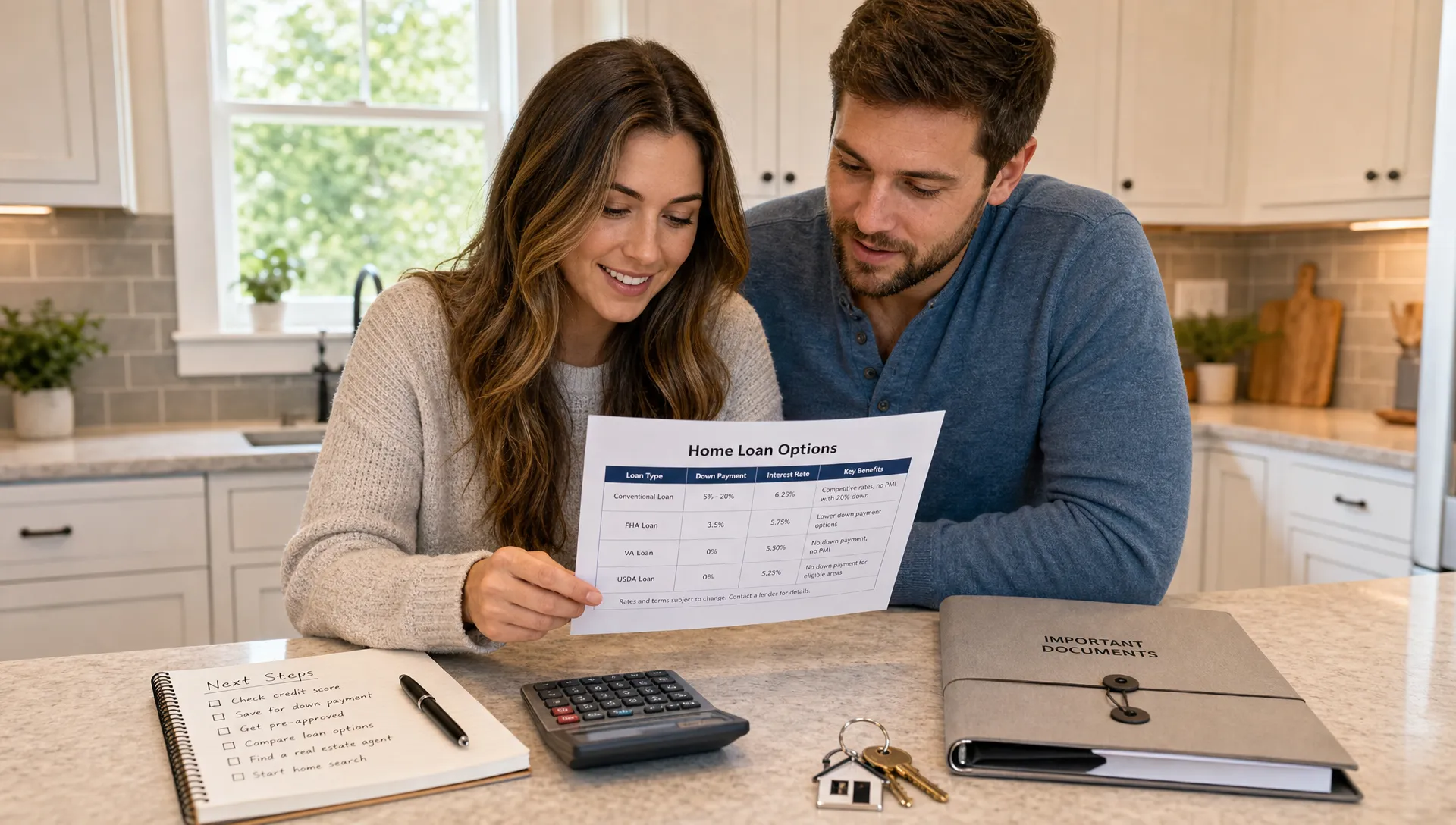

Step 2: Match the loan program to your constraints (not your assumptions)

In 2026, the fastest way to narrow home purchase loans is to identify your primary constraint, then choose the program that is designed to solve it.

If your constraint is limited down payment

- Conventional may allow low down payment for qualified buyers, and mortgage insurance can often be removed later.

- FHA can be more forgiving on credit and down payment, but mortgage insurance rules are different and can cost more over time depending on your scenario.

- VA can be a strong fit for eligible borrowers because it can reduce cash-to-close and does not use monthly PMI.

- USDA can be compelling in eligible areas for qualified borrowers, especially when cash-to-close is the main hurdle.

If you want a deeper, plain-English comparison between the two most common first-time buyer paths, use this reference: FHA vs. Conventional Loans: Which One Is Right for You?.

If your constraint is competitive offers and appraisal risk

Some programs and lender workflows are more “seller friendly” than others, mostly because they reduce uncertainty around approval and closing timelines.

What matters in practice:

- Strength of pre-approval (ideally with upfront underwriting review, not just an automated letter)

- Clarity on appraisal and property condition requirements

- Lender responsiveness for agents, escrow, and title

This is less about the logo on the application and more about whether the lender can consistently execute.

If your constraint is a higher loan amount

If you are above conforming loan limits in your county, you may be looking at a jumbo program or a lender-specific portfolio option. These loans often come with tighter requirements (credit, reserves, property type), and comparing lenders is especially important because guidelines can vary.

If your constraint is non-traditional income or a unique profile

Some buyers are great candidates for homeownership but do not fit standard documentation patterns (recent career change, variable income, complex assets). In those cases, you may need a non-QM or portfolio solution. The best option here is usually the one with clear documentation rules and a realistic path to close, not the one that looks the cheapest on an early quote.

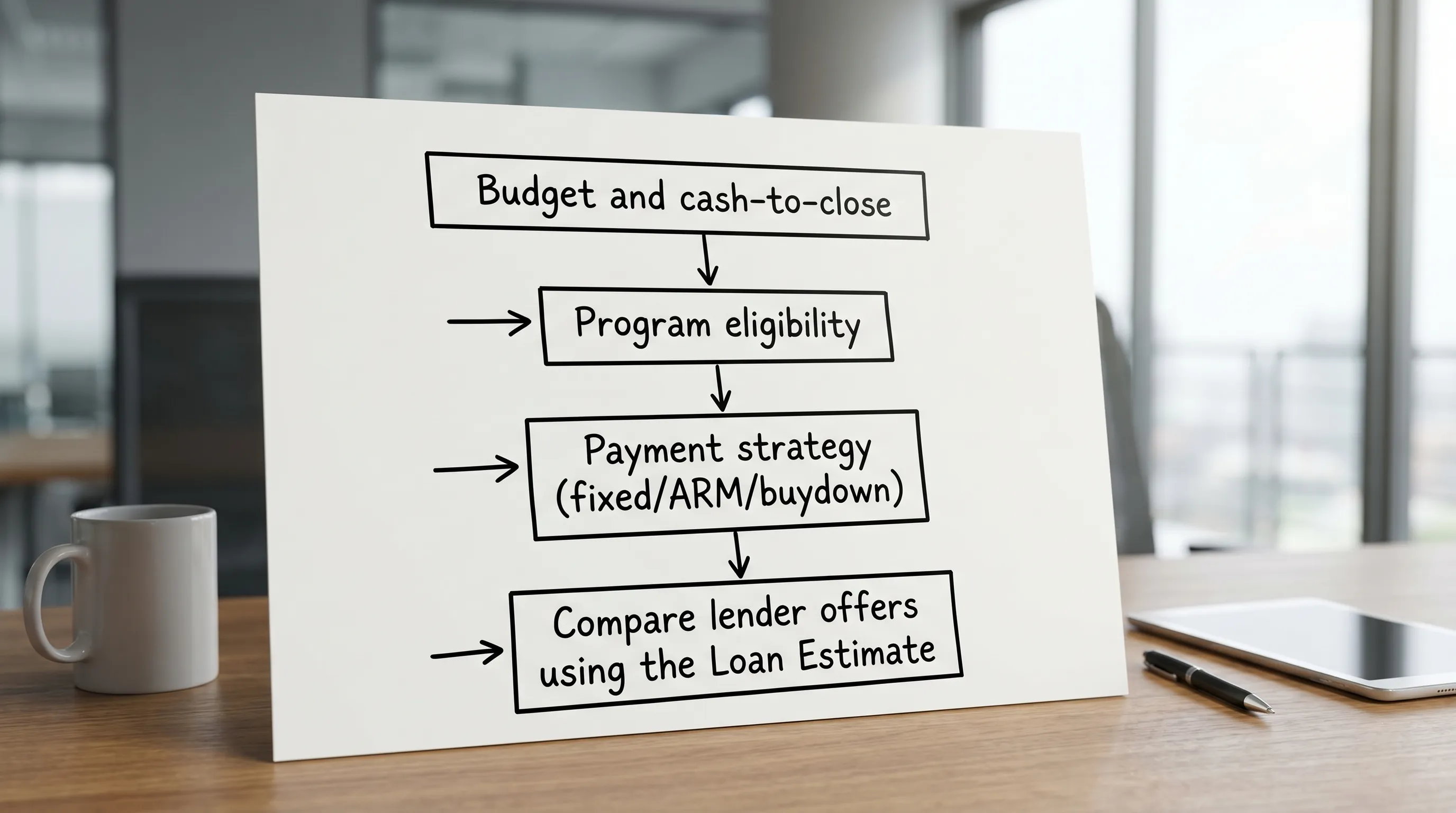

Step 3: Choose your payment strategy (fixed vs ARM vs buydown)

Once you have the right program category, you still have to choose the structure that fits how you live with your payment.

Fixed rate: when stability is the goal

Fixed-rate loans are straightforward: the principal and interest payment stays the same. They often make the most sense when:

- You plan to keep the home for a long time

- Your budget is tight and you cannot tolerate payment increases

- You prefer simplicity over optimization

Adjustable-rate mortgage (ARM): when the timeline is shorter (and the math is honest)

An ARM can lower the initial rate for a period, then adjust later. In 2026, ARMs can be useful when you have a clear plan (sell, refinance, or pay down) before the adjustment period ends.

If you are evaluating an ARM, do not stop at the teaser rate. Ask for the worst-case payment based on caps and index rules, and decide if that payment is still workable.

Buydowns: when someone else is paying, or when cash-to-close is strategic

Temporary buydowns can reduce early payments, which may help cash flow during the first year or two of homeownership. The key question is opportunity cost: would that money be better used to reduce price, cover closing costs, or strengthen your reserves?

For a deeper breakdown of these three options, including how to compare them on a Loan Estimate, see: Mortgage Options Compared: Fixed vs ARM vs Buydowns.

Step 4: Compare lenders correctly (use the Loan Estimate like a pro)

In the U.S., the Loan Estimate (LE) is the standardized document designed to help you compare mortgage offers. The Consumer Financial Protection Bureau (CFPB) provides an overview of how to read it and what each section means: Loan Estimate explainer from the CFPB.

The apples-to-apples checklist (what to line up)

To compare home purchase loans fairly, make sure each quote uses the same:

- Loan amount

- Down payment

- Credit assumptions (ask what score they priced)

- Rate lock period (a 15-day lock and a 45-day lock are not the same risk)

- Points or lender credits (and whether they are optional)

Then focus on these sections:

Interest rate vs APR. APR includes certain fees and can help you compare total borrowing cost, especially if one offer includes points.

Mortgage insurance. Look at both the upfront and monthly component (if applicable) and understand removal rules.

Closing costs. Separate true lender fees from third-party costs (title, escrow, appraisal). Third-party costs can vary, but lender fees and points are where quotes can differ dramatically.

Cash to close. This is the reality number that impacts your savings account.

If you do this, you will avoid the most common mistake buyers make: comparing a low rate that is “bought down” with points against a higher rate that requires much less cash upfront.

Step 5: Use a scorecard to pick the best option (not just the lowest quote)

When choices are complex, a simple evaluation framework beats gut feel.

A helpful approach is to create a weighted scorecard and force each option to earn its place. This idea is common in other industries where the wrong vendor choice is expensive, like platform selection, and the same logic works for mortgages. If you want to see what a modern scorecard process looks like (and how to validate non-negotiables with evidence), this guide is a surprisingly good model: build a weighted scorecard for choosing a platform.

A practical mortgage scorecard (example categories)

Pick 4 to 6 categories and assign weights based on your life, not the lender’s preference. For example:

- Total monthly payment (include mortgage insurance and HOA)

- Cash-to-close

- Payment risk (fixed stability, ARM caps, buydown step-ups)

- Approval certainty (documentation clarity, underwriting strength)

- Speed and communication (especially important with tight contract deadlines)

The “best” home purchase loan in 2026 is typically the one that wins on your top two categories without failing any non-negotiables.

2026-specific decision factors buyers should not ignore

1) The market can shift faster than your contract timeline

Mortgage rates are influenced by broader market forces (including inflation expectations and bond markets), and those can move quickly. For rate context and market data, the Freddie Mac Primary Mortgage Market Survey is a widely cited reference.

What to do with this information: decide in advance what you need to see to lock (payment comfort, budget certainty, timeline), then act deliberately instead of trying to time the perfect day.

2) Seller concessions can change which loan wins

If the seller is willing to contribute toward closing costs (where permitted), a slightly higher rate with lender credits or a buydown might outperform a “lower rate” option that drains your cash.

3) Underwriting speed is a competitive advantage

In many markets, the strongest offer is the one that looks most certain to close. Choosing a lender with a modern process (secure document uploads, e-signature support, clear milestone tracking) can be a real strategic edge, not just a convenience.

Quick scenarios: which home purchase loan often fits best?

Scenario A: Strong credit, stable income, moderate down payment

A conventional loan is often a strong baseline. Your optimization work usually comes down to:

- How much you put down (and what that does to mortgage insurance)

- Fixed vs ARM vs buydown, based on time horizon

- Whether paying points makes sense given how long you will keep the loan

Scenario B: Limited down payment, credit is improving

FHA may be worth a serious look, especially if it increases approval certainty or reduces the effective barrier to entry. The key is to weigh mortgage insurance rules and long-term cost, and understand your future exit plan (keep long term vs refinance later if appropriate).

Scenario C: Eligible veteran buyer prioritizing cash-to-close

VA financing can be a standout option due to benefits that can reduce monthly cost structure and keep cash available for reserves, moving expenses, and homeownership startup costs. The best fit still depends on property type and timing, so it helps to run side-by-side scenarios.

Frequently Asked Questions

Do I need 20% down for home purchase loans in 2026? No. Many buyers use lower down payment options depending on the loan program and their qualifications. The tradeoff is usually mortgage insurance or program fees, plus a higher loan amount.

What is the difference between pre-qualification and pre-approval? Pre-qualification is often an early estimate based on self-reported information. A real pre-approval typically requires documentation review (income, assets, credit) and carries more weight with sellers.

Is the lowest interest rate always the best deal? Not always. A lower rate can require discount points (more cash upfront). The best deal depends on your time horizon and total cost, including APR, mortgage insurance, and cash-to-close.

Can I change loan programs after I am under contract? Sometimes, but it can affect timelines and underwriting requirements. If you think you might switch (for example, FHA to conventional), bring it up early so your lender can plan the cleanest path.

How do I compare two Loan Estimates correctly? Align loan amount, down payment, lock period, and points first. Then compare APR, lender fees, mortgage insurance, and cash to close. If something looks too good, ask what assumptions were used.

Get a 2026 purchase loan comparison that matches your goals

If you want help choosing among home purchase loans, New Era Lending can run side-by-side scenarios based on your real numbers, then walk you through the tradeoffs with clear, human guidance. Their process is designed to be modern and straightforward, with secure document uploads and e-signature support, and they serve buyers in 39 states.

Start with a purchase pre-approval or a scenario review at New Era Lending.