.jpg)

.jpg)

.jpg)

VA Loan Mortgage Rates: What Affects Your Rate and APR

VA loans are famous for being one of the most valuable homebuying benefits available to eligible veterans, active duty service members, and some surviving spouses. But VA loan mortgage rates are not “one rate for everyone.” Your interest rate and APR can vary meaningfully based on your credit profile, the type of VA transaction you’re doing, the lender’s pricing, and even how you choose to pay closing costs.

This guide breaks down what really moves the needle so you can compare offers correctly and make confident decisions.

First, what’s the difference between a VA interest rate and APR?

Your interest rate is the percentage used to calculate interest on your loan balance.

Your APR (Annual Percentage Rate) is a broader cost measure that typically includes the interest rate plus certain lender fees and prepaid finance charges, spread over the loan term. APR is designed to help you compare the “all-in” cost of borrowing, especially when two loans have different points or lender fees.

Two important reminders for VA loans:

- APR is most useful when you compare apples to apples, meaning the same loan type (VA), same term length, and similar lock period.

- Some VA-specific costs, such as the VA funding fee, can affect your total cost and cash to close. Whether and how a fee influences APR can depend on how it’s paid (for example, financed vs paid in cash). When in doubt, ask the lender to walk you through what is included in APR on your Loan Estimate.

If you want the official definition of what a Loan Estimate is and how it’s meant to be used, the CFPB overview is a solid reference: Consumer Financial Protection Bureau guidance on the Loan Estimate.

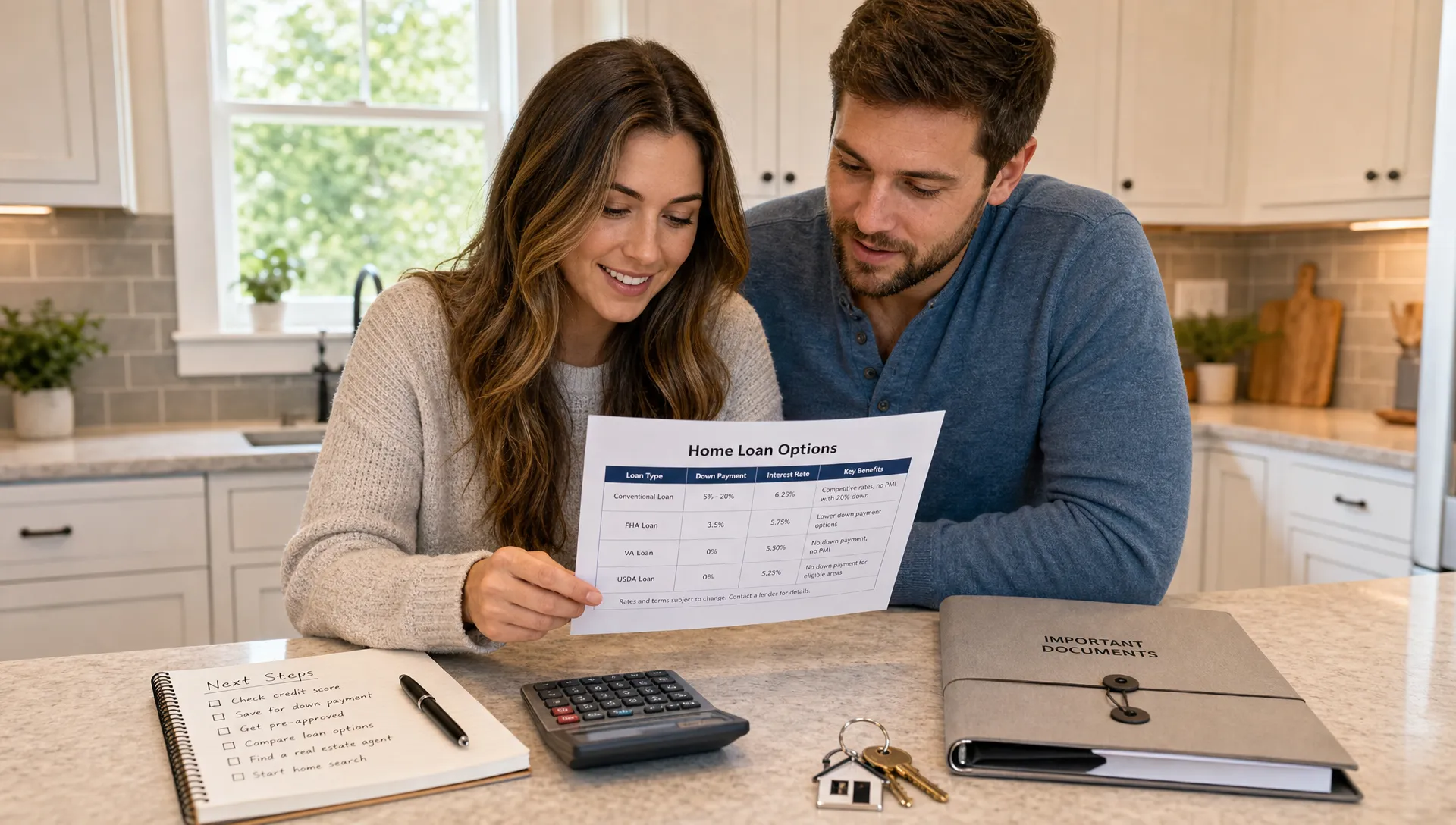

The two biggest drivers of VA loan mortgage rates

Before getting into personal factors, it helps to separate what you can control from what you can’t.

1) The market (what’s happening with interest rates overall)

VA loan rates move with the broader mortgage market. Even if your profile is unchanged, today’s rate could be different from last month’s because investors demand more or less yield for mortgage-backed securities.

What you can do about it is mostly tactical:

- Decide whether to lock your rate (and for how long)

- Compare lenders on the same day, with the same lock period

2) Lender pricing (not all VA rate sheets are the same)

Two lenders can price the exact same borrower differently due to:

- Overhead and operating model

- Risk appetite and internal margins

- How they price credits, points, and lender fees

- Whether they add “overlays” (extra rules beyond VA guidelines)

This is why shopping matters, and why comparing only the headline interest rate can backfire.

Borrower factors that affect your VA rate and APR

VA underwriting is often more flexible than conventional financing, but pricing still reflects risk. Here are the most common borrower-specific inputs.

Credit score and credit depth

In general, a stronger credit profile tends to get better pricing.

Two people can have the same score but very different pricing potential if one has:

- Long, clean credit history

- Low utilization

- No recent late payments

- Fewer disputes or recent credit events

Practical tip: if you’re 30 to 60 days from shopping, paying revolving balances down (even without paying them off) can sometimes improve your score and reduce risk flags.

Debt-to-income ratio (DTI) and cash flow

DTI still matters for VA pricing and approval. But VA loans are also known for emphasizing residual income, which is the money you have left after major obligations.

Even when a lender approves a higher DTI, better cash flow can support stronger execution and smoother underwriting, and in some cases better pricing.

Occupancy and property use

VA loans are for primary residences. If the home will not be your primary residence, it’s not a VA loan, and the pricing and guidelines change.

Even within primary residences, property characteristics can influence a lender’s comfort level (and sometimes rate) if the home is harder to value or sell.

Loan structure choices that change your rate and APR

Even with the same lender and borrower, the way you structure the loan can move your rate and APR.

Fixed vs ARM

A fixed-rate VA loan typically offers long-term payment stability. A VA ARM can sometimes start with a lower initial rate, but it introduces adjustment risk.

ARM pricing depends heavily on:

- The initial fixed period

- Caps and margins

- How long you expect to keep the home or the loan

Loan term (30-year vs 15-year)

Shorter terms often have lower rates, but higher monthly payments because you’re paying principal faster.

A rate that’s 0.50 percent lower is not automatically “better” if the payment stresses your budget or reduces your reserves.

Discount points (buying the rate down)

Discount points are prepaid interest. You pay more upfront to potentially get a lower rate.

Points can be smart when:

- You have enough cash to close without draining reserves

- You plan to keep the loan long enough to hit your break-even point

They can be less attractive when:

- You may refinance or sell relatively soon

- You’re close to a budget limit on cash to close

When you compare VA offers, ask each lender to show:

- A “no points” option

- A “points” option

- Any lender credit option (higher rate, lower cash to close)

Rate lock period and timing

A longer lock can cost more than a shorter lock because the lender is taking on market risk for longer.

If your closing timeline is uncertain (for example, new construction or a complex transaction), lock strategy becomes a real pricing lever.

VA-specific costs that influence APR and cash to close

The VA funding fee (and exemptions)

The VA funding fee is a unique VA loan cost that helps keep the program running for future borrowers. The amount depends on factors like your loan type, down payment (if any), and whether it’s your first use.

Some borrowers are exempt, such as certain veterans receiving VA disability compensation. For the official rules and current details, start with the VA’s housing assistance page: VA home loan funding fee information.

Key planning point: even if your interest rate is excellent, a financed funding fee can increase your loan balance, which changes your payment and long-term interest paid.

Closing costs, seller concessions, and how they’re paid

VA loans limit certain fees that can be charged to veterans, but closing costs still exist, and different lenders structure them differently.

Your out-of-pocket cost can shift based on:

- Seller concessions

- Lender credits (often paired with a higher rate)

- Whether you pay certain items in cash or finance them (when allowed)

This is exactly why APR can be helpful, but only when you compare similar loan setups.

Why two VA offers can have the same rate but different APR

This happens all the time. Common reasons include:

- One lender charges an origination fee and the other doesn’t

- One quote includes discount points

- One lender offers a lender credit to offset closing costs

- One quote assumes a different lock period

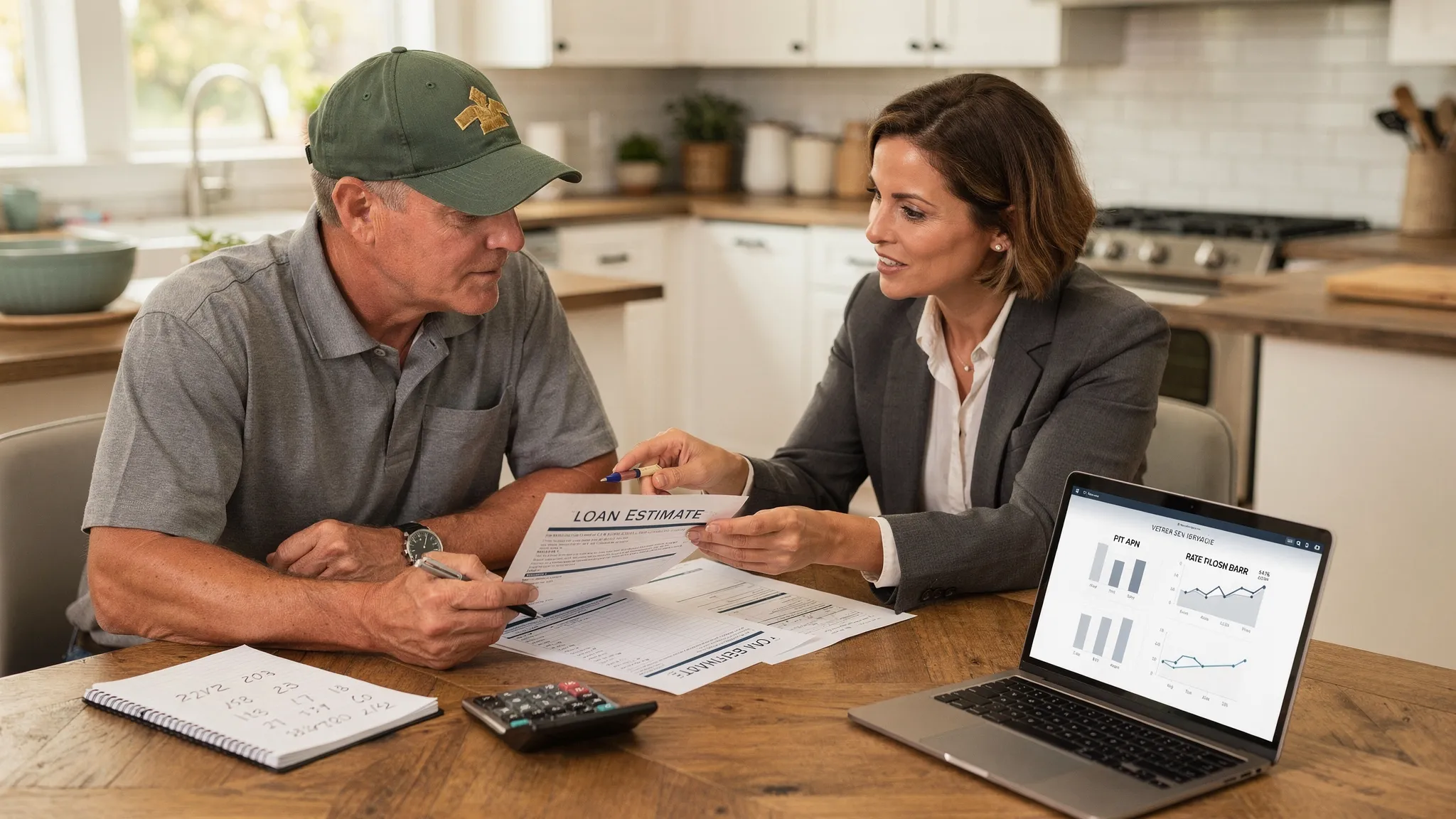

To compare correctly, request official Loan Estimates (not just worksheets) and look at:

- Interest rate

- APR

- Total loan costs

- Points and lender fees

- Credits

- Cash to close

A homeowner reality check: your “best” rate should still leave room for maintenance

A tight budget can turn a great rate into a stressful homeowner experience. When you’re deciding whether to pay points, use up reserves, or stretch your max approval, remember that homes come with ongoing costs.

If you want a practical example of the kinds of expenses that pop up after closing (especially in hot-weather markets), browsing PHX Appliance Fix Blog’s appliance repair price guides can help you sanity-check a maintenance budget alongside your mortgage payment.

How to improve your VA loan pricing before you lock

You can’t control the market, but you can control your readiness and how you shop.

- Strengthen credit where it’s easiest: reduce credit card utilization, avoid new accounts right before applying, and correct any reporting errors.

- Lower DTI if possible: paying down installment debt or removing a monthly obligation can improve both approval comfort and pricing.

- Document income cleanly: smoother files tend to close faster, which can reduce lock stress and last-minute changes.

- Choose the right structure: fixed vs ARM, term length, and whether points actually break even.

- Shop transparently: compare Loan Estimates on the same day with the same scenario assumptions (loan amount, estimated credit score, lock period, points).

What to ask a lender when you’re comparing VA loan mortgage rates

A few direct questions can prevent expensive misunderstandings:

- “Is this quote based on points, and how many?”

- “What lock period is included in this pricing?”

- “Are there any lender credits built in?”

- “Is this pricing for a purchase or an IRRRL or a VA cash-out refi?”

- “Can you walk me through what’s driving my APR on the Loan Estimate?”

Frequently Asked Questions

Are VA loan mortgage rates always lower than conventional rates? Not always, but VA loans often price competitively because they’re backed by a VA guaranty and don’t require monthly PMI. Your personal rate still depends on credit, DTI, lender pricing, and market conditions.

What affects VA loan APR the most? APR is most affected by the interest rate plus lender fees, discount points, and certain prepaid finance charges. If you compare two offers with the same rate but different fees or points, APR can differ.

Does my credit score matter on a VA loan? Yes. The VA program is flexible, but lenders still use credit to price risk. Better credit often means a better rate, a better APR, or both.

Can I buy down a VA loan rate with points? Usually, yes. Discount points can reduce your rate, but you should calculate your break-even based on how long you expect to keep the loan.

How do I compare VA lenders accurately? Ask for official Loan Estimates for the same scenario (same loan type, term, down payment, and lock period). Compare rate, APR, points, lender fees, credits, and cash to close.

Get a VA rate and APR comparison that’s actually apples to apples

If you’re ready to shop, the goal is not just a low advertised rate, it’s a loan setup that fits your timeline, cash-to-close comfort level, and long-term plans.

New Era Lending helps eligible borrowers compare VA options with transparent rates and terms, a secure tech-driven process (including uploads and e-signatures), and personal guidance so you can make the right call for your situation.

Explore your options at New Era Lending and request a VA purchase or refinance scenario comparison.