.jpg)

.jpg)

.jpg)

Should You Pay Off Your Mortgage Early?

Few money questions feel as personal as this one. Paying off your mortgage early can be a huge emotional win, but it is not automatically the “best” financial move for every homeowner.

The right answer depends on your interest rate, cash reserves, other debts, tax situation, and how much flexibility you want over the next few years. Below is a practical way to decide, plus a few smarter alternatives that can get you most of the benefits without boxing you in.

What “paying off your mortgage early” really means

In most cases, paying off your mortgage early means making extra principal payments. That can happen in a few ways:

- Adding extra dollars to your monthly payment and applying them to principal.

- Making one extra payment each year (or splitting your payment in half every two weeks).

- Making a lump-sum principal payment (for example, after a bonus or home sale).

Important detail: Extra money only helps if it is credited to principal, not treated as a “future payment.” If your servicer’s portal is confusing, call and ask how to designate an “additional principal” payment.

Why early payoff can be a great move

When you pay extra principal, you reduce the balance that future interest is calculated on. That creates a guaranteed return equal to your mortgage rate (adjusted for taxes only if you itemize and actually benefit from the mortgage interest deduction).

Here are the biggest upsides.

1) Guaranteed interest savings

Mortgage interest is front-loaded through amortization. In the early years, a larger share of each payment goes to interest. Paying extra principal earlier can reduce total interest dramatically over time.

If you are comparing options, think of extra principal as earning a “return” roughly equal to your note rate.

2) More monthly breathing room later

Once the mortgage is gone, your required monthly housing cost often drops to taxes, insurance, and HOA (if applicable). That flexibility can be valuable if you are approaching retirement, planning a career change, or simply want lower fixed expenses.

3) Lower risk, better sleep

A paid-off home can be a powerful risk-management tool, especially for households with variable income or high sensitivity to job market swings.

4) A strong payoff case if you have PMI

If you are paying monthly mortgage insurance, extra principal can sometimes deliver an outsized benefit by helping you reach the equity threshold to remove PMI sooner (rules vary by loan type). If PMI is part of your payment today, it is worth reading New Era Lending’s guide to property mortgage insurance costs, rules, and how to avoid it.

Why paying off early can be the wrong move

The biggest downside is not “math.” It is liquidity and opportunity cost.

1) You can become “house rich, cash poor”

Once extra cash is locked into home equity, accessing it again usually requires a new loan (HELOC, home equity loan, or cash-out refinance) and approval based on credit, income, and property value at that time.

If you want a deeper overview of how equity access works, New Era Lending has a helpful explainer on the HELOC system.

2) You might be ignoring higher-interest debt

If you have credit card balances or personal loans at high rates, paying those down often provides a higher and more immediate financial win than accelerating a low-rate mortgage.

3) You could underfund emergency reserves

A good rule of thumb is to maintain a cash buffer before you start accelerating long-term debt payoff. The “right” emergency fund size varies, but homeowners typically want more cushion than renters because repairs and insurance deductibles can be unpredictable.

4) You might be trading a low fixed rate for uncertain investment returns, or vice versa

Some homeowners have very low fixed mortgage rates. In that case, investing may outperform mathematically over long horizons, but market returns are not guaranteed and timing matters.

On the other hand, if your mortgage rate is high (or adjustable and likely to rise), the “guaranteed return” from payoff becomes more attractive.

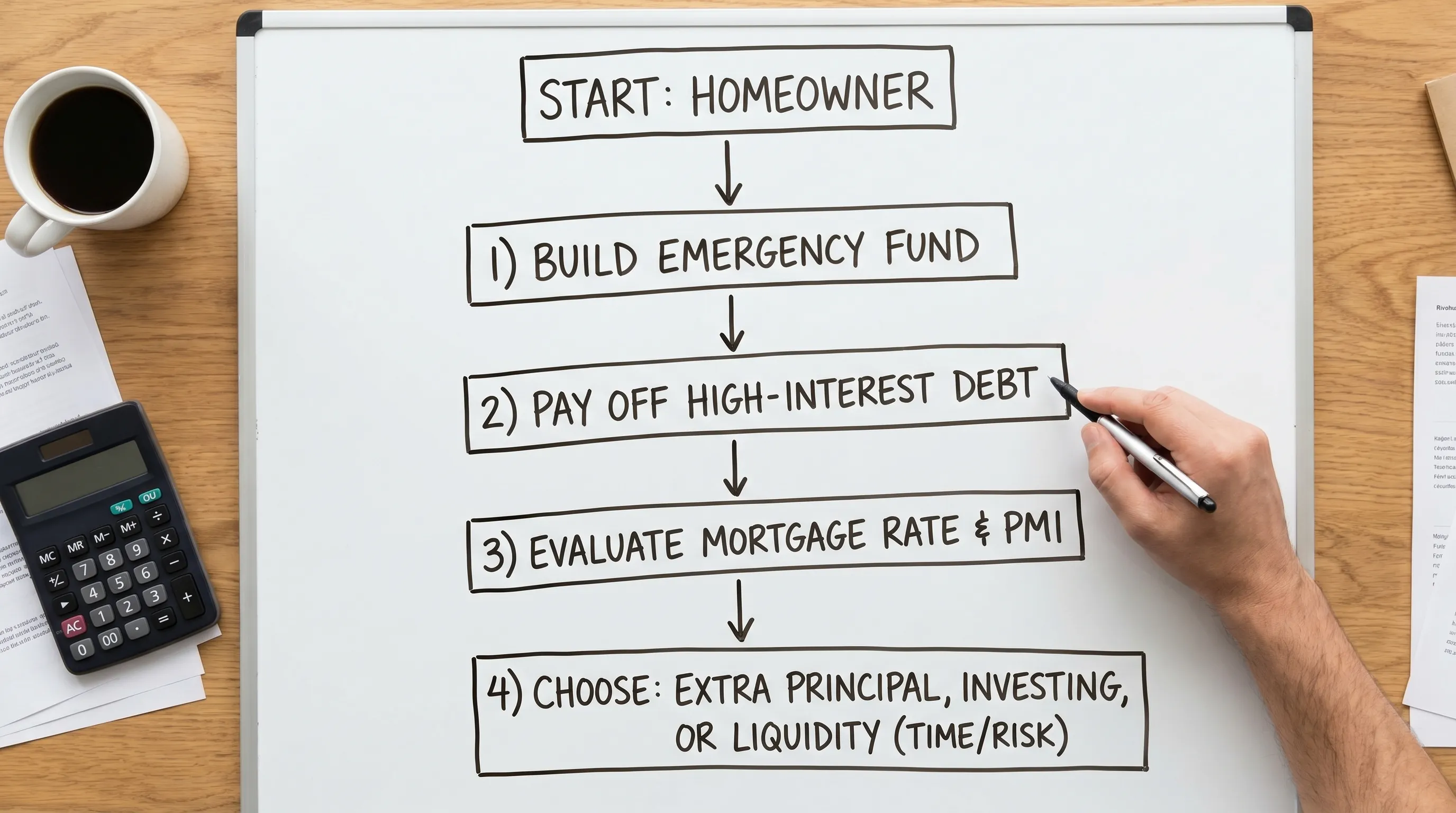

A simple decision framework (use this before you send extra money)

Use this as a quick sequence of checks.

Step 1: Confirm your basics

Before accelerating payments, verify:

- Do you have a prepayment penalty? Most modern mortgages do not, but some loans (especially certain non-QM or investor products) can.

- Are you current on taxes and insurance? Paying off early does not remove these costs.

- Do you have an emergency fund? If not, consider building that first.

Step 2: Compare your mortgage rate to your realistic alternatives

Ask yourself what you would do with the extra money if you did not pay down the mortgage.

- If it would sit in a checking account earning little, extra principal can be compelling.

- If it would go toward a diversified investment plan, compare expected long-term returns against your mortgage rate, while remembering volatility and taxes.

If you itemize deductions and the mortgage interest deduction truly benefits you, your effective cost of mortgage interest may be lower than the note rate. The IRS provides the official rules in Publication 936. Many households take the standard deduction, so the mortgage interest deduction may not change the math.

Step 3: Decide based on your time horizon

Time horizon changes everything.

- If you might sell or move within a few years, aggressive payoff may not deliver as much benefit as you expect.

- If you plan to stay long-term, the interest savings from early payoff (or shortening the term) can be much more meaningful.

Step 4: Factor in personal risk and income stability

A household with stable W-2 income, high savings, and strong retirement contributions might prioritize investing.

A household with variable commission income, self-employment income, or a single earner might prioritize reducing required monthly obligations.

If you are self-employed, better cash-flow visibility makes any payoff plan easier to stick to. That can be as simple as cleaner bookkeeping and reporting, for example using an invoicing and reporting tool like Kontozz to keep a sharper eye on what is truly “extra” each month.

Situations where paying off your mortgage early tends to make sense

The mortgage payoff decision is rarely all-or-nothing. Still, early payoff is often a strong fit when:

- Your mortgage rate is high relative to your other low-risk options.

- You have no high-interest debt and a solid emergency fund.

- You are close to retirement and want to reduce fixed monthly obligations.

- You are paying PMI and extra principal could help you remove it sooner.

- Your income is variable and you value lower required payments and simplicity.

Situations where you might not want to pay off early

Paying off early is often lower priority when:

- You do not have adequate cash reserves.

- You are carrying high-interest debt.

- Your mortgage rate is very low and you are consistently investing for long-term goals.

- You expect to need liquidity soon (business investment, upcoming move, major life change).

How to run the math without getting lost

You do not need a finance degree. You just need a consistent comparison.

Start with two numbers

Interest you save by paying extra principal.

What you give up by not using that money elsewhere.

Most payoff calculators will show the interest saved and time shaved off if you add $X per month. If you are comparing payoff versus investing, also consider taxes on investment gains and your own behavior (some people invest the difference faithfully, others do not).

Watch for a common “win” people miss: principal prepayment timing

Paying an extra $200 every month starting now is usually more impactful than paying a lump sum years later, because earlier payments reduce interest sooner.

Make sure payments are applied correctly

Servicers vary. If you are uncertain, request a payoff statement or ask for instructions. The CFPB also explains how mortgage servicing and payments work, including getting a payoff statement, at the Consumer Financial Protection Bureau.

Alternatives that can be better than “pay it off ASAP”

Many homeowners want the security of payoff, but also want flexibility. These approaches can split the difference.

Option 1: Make extra payments, but keep a liquidity floor

A practical method is to only prepay after your checking and savings balances are above a set threshold.

For example, you might decide that you will only send extra principal in months when you still have at least three to six months of expenses in cash after the transfer.

Option 2: Target the mortgage insurance removal point

If PMI is the only “bad” part of your current payment, your goal may not be full payoff. It may be reaching the equity point where PMI can be removed (for eligible loans), then redirecting the freed-up monthly amount to other goals.

Option 3: Consider recasting (if your loan allows it)

A recast means you pay a lump sum toward principal and the servicer recalculates your payment based on the remaining balance and term (typically for a fee). This can lower the required monthly payment without refinancing.

Not all loans allow recasts, and the rules vary. But it is worth asking if your goal is cash flow, not necessarily paying the loan off fast.

Option 4: Refinance to a shorter term (only if the numbers work)

If you want to be mortgage-free sooner, a shorter term can be a clean solution, but refinancing has closing costs and qualification requirements.

If you are weighing this route, New Era Lending’s guide on mortgage loan refinance options to lower payment or term explains how to think about payment changes, term changes, and break-even math.

Practical tips for paying off a mortgage early (without regrets)

Automate, but keep it adjustable

Automation helps consistency, but do not automate yourself into a cash crunch. If your income fluctuates, consider a smaller automatic extra payment and add one-off principal payments in good months.

Label extra payments as “principal only”

If the portal offers multiple fields, use them. If it does not, call and ask how to ensure the extra money is applied to principal.

Do not ignore your broader plan

Mortgage payoff is one goal. You also need to plan for:

- Home maintenance and capital expenses

- Insurance deductibles

- Retirement contributions

- Education goals or caregiving responsibilities

A mortgage-free home is great, but not if it comes at the cost of underfunding the rest of your life.

Frequently Asked Questions

Is it better to pay off your mortgage early or invest? It depends on your mortgage rate, your risk tolerance, and whether you will actually invest consistently. Paying extra principal is a guaranteed return roughly equal to your mortgage rate, while investing has uncertain returns but higher long-term upside.

Does paying off a mortgage early hurt your credit? Paying off a mortgage can slightly change your credit mix, but it is rarely harmful in a meaningful way. Payment history and overall debt management matter far more.

Should I pay off my mortgage before retirement? Many people like entering retirement with lower fixed expenses, but you should balance that with liquidity needs, healthcare costs, and maintaining a cash cushion.

What if I might move in a few years? Aggressive early payoff may deliver less benefit if you sell soon. In that case, maintaining liquidity, paying down higher-interest debt, or targeting PMI removal can be more practical.

Can I make a lump-sum payment without refinancing? Usually yes, and it can reduce interest costs. Just confirm there is no prepayment penalty and ensure the payment is applied to principal.

Want a personalized payoff vs keep-cash comparison?

If you are debating whether to pay off your mortgage early, refinance to a shorter term, or keep more liquidity on hand, the right next step is to run your scenario with real numbers.

New Era Lending can help you compare options based on your goals, timeline, and current loan details, with smart tools and clear guidance throughout the process. Learn more or start a conversation at New Era Lending.