.jpg)

.jpg)

.jpg)

Mortgage Rates in 2026: What Really Moves Them

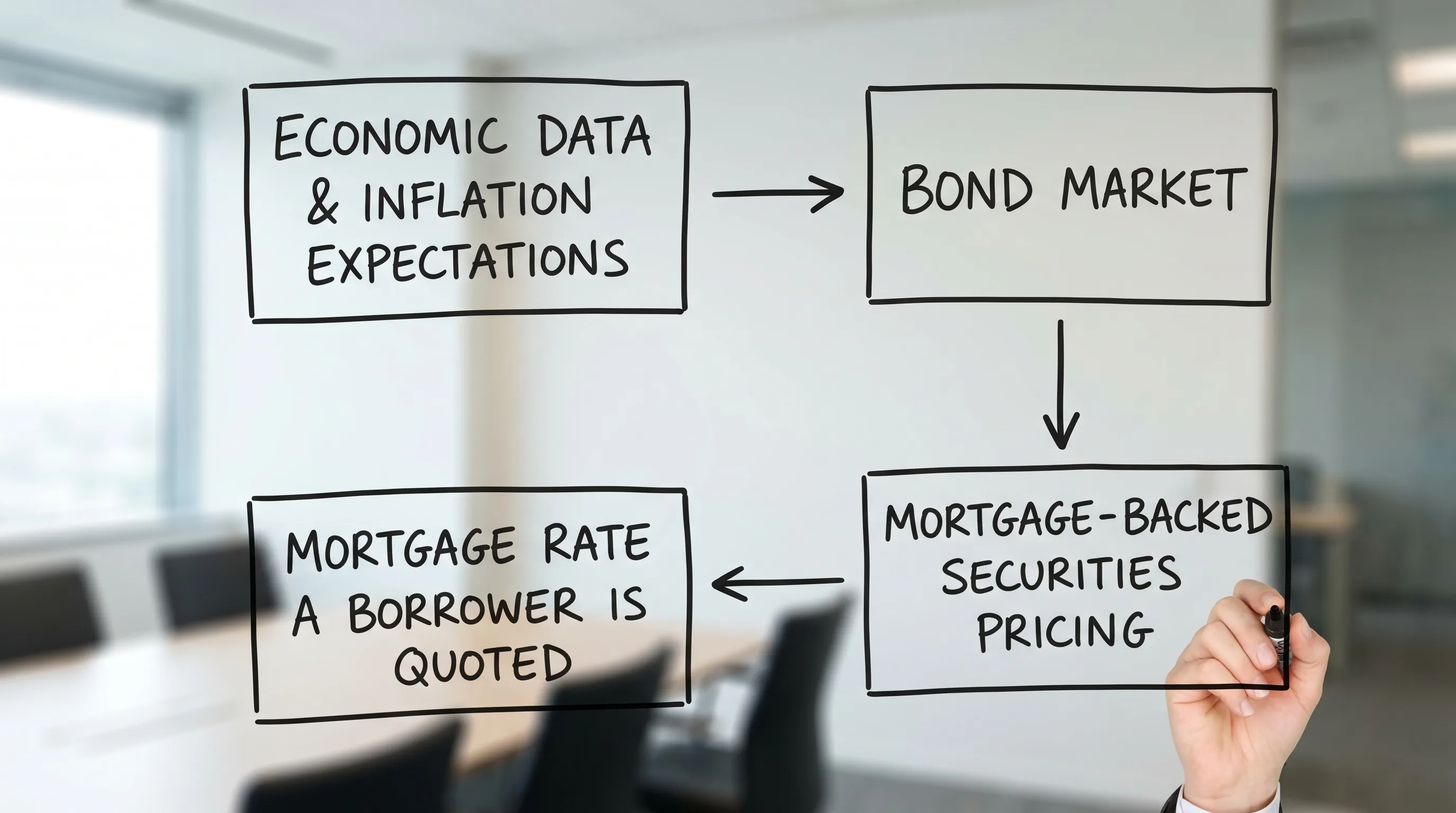

If you’re watching mortgage rates in 2026, it can feel like they change for “no reason” and always at the worst possible time. In reality, rate movement is usually a chain reaction: economic data changes expectations, the bond market reprices, mortgage-backed securities (MBS) reprice, and lenders update rate sheets.

Understanding that chain is useful for one big reason: even if you can’t control the market, you can control how prepared you are to shop, lock, and structure your loan when the market gives you an opening.

The simplest way to think about what moves mortgage rates

Mortgage rates are not set by one person or one institution. In 2026, they’re best explained as three layers that stack on top of each other:

The bond market layer (especially Treasury yields): the baseline cost of long-term money.

The mortgage market layer (MBS pricing and spreads): the “mortgage-specific” premium investors demand.

Your personal pricing layer: credit, down payment, loan type, occupancy, property details, and how the loan is structured.

When people say “rates went up today,” they’re usually describing a change in layer 1 or 2. When two borrowers get very different quotes on the same day, that’s layer 3.

What the Federal Reserve does (and does not) control

A common misconception is that the Federal Reserve “sets mortgage rates.” It doesn’t.

What the Fed directly influences is short-term interest rates (via the federal funds rate target) and broader financial conditions. That influence matters because it changes:

- Market expectations about future inflation and growth

- Investor demand for bonds

- The shape of the yield curve (short-term vs long-term rates)

In other words, the Fed often moves mortgage rates indirectly through expectations. A surprisingly large amount of mortgage rate volatility in 2026 is driven not just by what the Fed does, but by what markets think the Fed will do next.

If you want to understand the “why” behind rate days, pay attention to Fed communication and meeting outcomes (statements, projections, press conferences). The Fed’s monetary policy announcements are the source documents most media summaries are based on.

Inflation expectations are the engine behind many rate moves

Inflation is one of the biggest long-term drivers of mortgage rates because investors need to be compensated for the risk that inflation erodes the value of future payments.

Two points matter in 2026:

- Actual inflation prints (like CPI and PCE) move markets, but so do surprises versus expectations.

- Inflation expectations can change faster than inflation itself, and rates often move on expectations.

Even when inflation is trending in the right direction, a single hot report can raise the “higher for longer” fear, pushing long-term yields higher, and mortgage rates often follow.

The 10-year Treasury is a key reference point (but not the whole story)

Mortgage rates tend to track long-term bond yields, especially the 10-year Treasury, because a 30-year fixed mortgage behaves like a long-duration bond with prepayment risk.

This is why you’ll sometimes see mortgage rates drop even when the Fed hasn’t cut rates, or rise even when the Fed “holds steady.” The bond market is forward-looking.

But, mortgage rates are not a simple add-on to Treasury yields. That brings us to the mortgage-specific layer.

The mortgage market layer: MBS pricing and the “spread” that borrowers feel

Most U.S. mortgages are packaged into mortgage-backed securities (MBS). Investors buying those securities care about risks that do not exist in Treasuries, including:

- Prepayment risk: borrowers refinance or sell when rates drop, which can shorten the investor’s expected return.

- Extension risk: when rates rise, refinances slow, and the bond can behave like it has a longer life than expected.

- Liquidity and volatility: MBS can require a higher yield when markets are stressed.

The gap between mortgage rates and comparable Treasury yields is often referred to as the spread. In 2026, day-to-day rate movement can come from:

- Treasury yields changing (layer 1)

- MBS spreads widening or tightening (layer 2)

That second factor is why borrowers sometimes hear, “The market improved, but mortgage rates didn’t improve as much.” It can also work in your favor when spreads tighten.

For a high-level weekly benchmark, many borrowers track Freddie Mac’s weekly survey of average mortgage rates, the Primary Mortgage Market Survey (PMMS). It won’t match your quote, but it helps contextualize whether the market is generally rising or falling.

Jobs data and economic growth: why “good news” can raise rates

In 2026, strong economic data can push mortgage rates up for a simple reason: it can imply more inflation pressure and fewer reasons for rates to come down.

Reports that often move mortgage rates the most include:

- Monthly jobs reports (employment growth, unemployment rate, wage growth)

- Inflation releases

- Consumer spending and GDP updates

This can be confusing emotionally: “The economy is doing well” can translate into “borrowing is more expensive,” at least in the near term.

Global events and investor demand can move rates fast

Mortgage rates in 2026 can react quickly to risk sentiment:

- Geopolitical conflict, energy shocks, or supply chain disruption can raise inflation fears.

- Financial stress can trigger “flight to safety” buying of Treasuries, often pulling yields down.

These moves can be sharp, and they don’t always wait for scheduled economic reports.

Housing market dynamics matter, but usually indirectly

Housing supply, demand, and home prices can influence mortgage rates, but usually through second-order effects:

- Housing strength can support broader economic growth expectations.

- The “lock-in effect” (homeowners staying put with older low rates) can constrain supply, which affects prices and transaction volume.

- Lower transaction volume can change lender competition, capacity, and pricing behavior.

In practical terms: housing conditions often affect your affordability and strategy more than they directly “set” market rates.

Policy and program changes can shift the math for borrowers

Mortgage pricing isn’t only macro. It can also be affected by rule changes, program costs, and annual updates.

In 2026, keep an eye on items that can change year to year, including:

- Conforming loan limits (typically updated annually)

- FHA and VA program parameters (fees, eligibility rules, mortgage insurance structures)

- GSE pricing frameworks that can influence borrower-level adjustments

Because these are program and policy decisions, they can change the effective cost of financing for certain borrower profiles even if the broader market is flat.

What you can control: the borrower-level factors that move your rate

Two people can apply on the same day and see meaningfully different pricing. That’s normal. Here are the most common drivers you can influence.

Credit score and credit profile

Your score matters, but lenders also look at the overall profile: payment history, utilization, and derogatory items. If you’re within 30 to 90 days of shopping, avoid big credit moves unless advised.

Down payment and equity (LTV)

Loan-to-value (LTV) is a core risk measure. More down payment (or more equity in a refinance) can improve pricing, reduce mortgage insurance needs, or broaden your program options.

Loan type and occupancy

Primary residence pricing is typically different from second home or investment property pricing, because risk characteristics differ.

Term and rate structure

A 15-year fixed, 30-year fixed, and an ARM are different products with different risk and investor demand.

Points, credits, and the “best rate” illusion

In 2026, many advertised rates assume discount points. The better question is: What combination of rate and closing costs fits your time horizon?

If you want to go deeper on how to evaluate affordability and timing decisions alongside your broader financial goals, it helps to track cash flow and savings rate consistently. The FIYR blog is a useful resource for budgeting and long-term planning concepts that can make mortgage decisions less stressful.

Rate locks in 2026: how timing really works

Lock strategy matters more when rates are volatile.

A few practical realities:

- Locks are a risk tradeoff, not a guarantee of the “best” possible day. You’re choosing certainty.

- Longer locks often cost more (directly or indirectly) because the lender is taking more market risk.

- Float-down options may be available in some scenarios, but terms vary by lender and should be reviewed carefully.

For purchases with tight closing dates, the value of certainty can outweigh the temptation to float and hope.

A borrower’s “watch list” for mortgage rates in 2026

You don’t need to stare at charts daily. Instead, watch the few items that consistently drive repricing.

- Inflation reports: especially CPI and PCE, and the surprise versus forecasts.

- Jobs data: unemployment rate and wage growth can matter as much as headline job creation.

- Fed meetings and speeches: guidance can move markets even without a rate change.

- 10-year Treasury yield trend: direction matters more than the exact number.

- MBS spreads (harder to observe directly): if headlines say “mortgage spreads widened/tightened,” that can explain a disconnect vs Treasuries.

If you’re planning to buy in the next 60 to 120 days, the most actionable move often isn’t predicting the next report. It’s getting your file into “ready to lock” shape so you can act quickly.

How to use this knowledge when you’re actually shopping

Knowing what moves rates is only useful if it changes how you shop. In 2026, a strong approach looks like this:

First, separate market movement from quote differences. If a lender quote is far from the rest, it may be assumptions, points, lock length, or fees, not a magical rate.

Second, compare offers apples-to-apples. Align:

- Same loan type and term

- Same lock period

- Same points or lender credits (or none)

- Same estimated closing date and property/occupancy assumptions

Third, focus on the outcome you actually want. The “lowest rate” is not always the best decision if it requires expensive points and you may move or refinance earlier than expected.

Frequently Asked Questions

Are mortgage rates in 2026 set by the Federal Reserve? No. The Fed influences short-term rates and financial conditions, but mortgage rates are primarily determined by the bond market and MBS pricing, plus borrower-specific factors.

Why did mortgage rates go up even though inflation is coming down? Rates move on expectations and surprises. If inflation data comes in hotter than expected, or growth stays strong, markets may price in higher rates for longer, pushing yields and mortgage rates up.

What’s the most important market number to watch for mortgage rates? There isn’t just one, but the 10-year Treasury yield trend is a helpful reference, and big inflation and jobs reports often drive the largest moves.

Why is my rate different from the average rate I see online? Published averages often assume a specific borrower profile and may include points. Your rate depends on credit, LTV, loan type, occupancy, lock length, and the fee structure of the quote.

Should I lock my rate now or wait? It depends on your closing timeline and risk tolerance. If you need certainty to close on time, locking can reduce risk. If you have flexibility, you can discuss float vs lock strategies and the costs of longer locks with your lender.

Get a mortgage rate strategy tailored to your timeline

In 2026, the biggest mistake borrowers make is trying to “beat the market” without having their loan plan ready. A better approach is to understand what’s moving rates, then structure a loan and lock strategy around your purchase or refinance timeline.

New Era Lending combines smart technology (secure document uploads and e-sign support) with personalized guidance to help you compare options clearly and move fast when it matters. If you want a scenario review based on your credit, down payment, and goals, start here: New Era Lending.