.jpg)

.jpg)

.jpg)

Investment Property Loans: Requirements, Rates, and Down Payment

Buying a rental or income-producing property is exciting, but financing it is a different game than buying a primary home. Investment property loans typically require higher down payments, stronger credit, and more cash reserves, and the interest rate is usually higher because the lender is taking on more risk.

This guide breaks down what most borrowers want to know up front: requirements, rates, and down payment expectations for investment property loans in 2026, plus practical tips to improve your approval odds.

What counts as an “investment property” for mortgage purposes?

In mortgage underwriting, an investment property is generally a home you do not intend to occupy as your primary residence and that you plan to rent out (or otherwise generate income from). That sounds straightforward, but definitions matter because they affect down payment, rates, and qualifying rules.

Common occupancy buckets:

- Primary residence: You live there most of the year.

- Second home: You occupy it part of the year, it’s typically a one-unit property, and it’s not primarily used as a rental.

- Investment property: You don’t occupy it as a primary residence, rental income is expected, or it’s purchased for income/return.

If you are planning to rent the property, assume the lender will treat it as an investment property unless it clearly meets second-home rules.

Common types of investment property loans (and when they fit)

There is no single “best” loan. The right choice depends on the property type, how quickly you need to close, how you document income, and how you plan to hold the asset.

Conventional (agency) loans for investment properties

Many rental property mortgages are conventional loans that follow Fannie Mae or Freddie Mac guidelines. These often offer strong long-term terms (including fixed rates), but qualifying can be more documentation-heavy.

A good fit if you want:

- A long-term rental with predictable financing

- Competitive pricing relative to other non-owner options

- A process that rewards strong credit, lower leverage, and reserves

Jumbo investment property loans

If the loan amount exceeds conforming limits, you may need jumbo financing. Requirements can be stricter, and guidelines vary by lender.

DSCR loans (Debt Service Coverage Ratio)

DSCR loans are popular with real estate investors because approval is often more focused on whether the property’s cash flow can cover the payment, instead of relying only on personal income documentation.

These can be helpful if:

- You have complex income (self-employed, multiple properties)

- You prefer qualification based more on rental performance

- You want to scale an investment portfolio

(DSCR rules and pricing vary widely, so it’s worth scenario-testing.)

Portfolio or non-QM investor loans

Some lenders offer portfolio products that don’t fit standard agency boxes. They can be useful for unique properties or borrower profiles, but rate and down payment requirements may be different.

“House hacking” with owner-occupied financing (not an investment loan)

If you buy a 2 to 4 unit property and live in one unit, you may qualify for owner-occupied financing (for example, FHA or conventional owner-occupied options), which can reduce down payment requirements. This is not the same as a pure investment property loan because occupancy rules apply.

For official FHA guidance, see HUD’s overview of FHA loan programs.

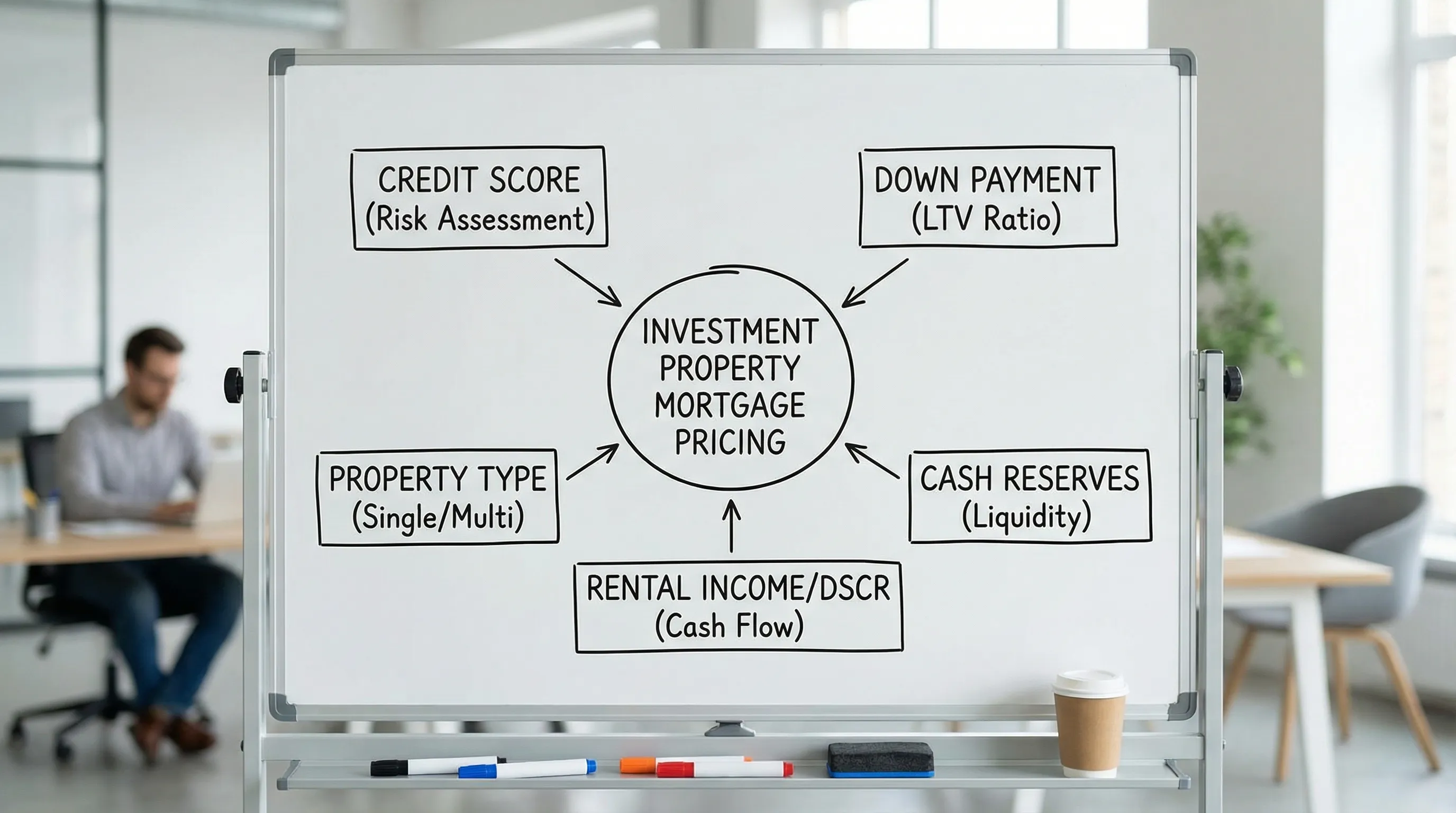

Investment property loan requirements (what lenders usually look for)

Even when guidelines differ by program, most lenders evaluate the same core risk factors.

Credit score and credit profile

Investment property mortgages typically expect:

- Higher credit scores than comparable primary-residence loans

- Clean recent payment history

- Manageable revolving utilization and minimal new debt

A higher score can improve pricing, not just approval.

Down payment and loan-to-value (LTV)

The down payment is one of the biggest differences versus a primary home. Lower LTV generally reduces lender risk, which can help both approval and rate.

Debt-to-income ratio (DTI)

DTI requirements vary by loan type and overall file strength. Lenders look at your monthly debts (including the new housing payment) relative to your income.

For investor loans, DTI can be influenced by how rental income is counted (more on that below).

Cash reserves

Many investor loans require you to show post-closing reserves, meaning liquid or semi-liquid assets left over after you pay your down payment and closing costs.

Reserves often increase when:

- You’re buying a 2 to 4 unit property

- You have multiple financed properties

- Your down payment is smaller

Property type and condition

Financing can vary based on whether the home is:

- Single-family

- Condo

- 2 to 4 units

- Short-term rental-eligible (rules vary)

Appraisal and property condition matter. Some properties (or situations like missing appliances, safety issues, or significant deferred maintenance) can create underwriting hurdles, especially for long-term conventional financing.

Down payment for investment property loans: what to expect

Down payment rules vary by lender and program, but these are common benchmarks borrowers see in the market:

- Single-family investment property: often 15% to 25% down depending on the loan type, credit profile, and whether it’s conforming or non-QM.

- 2 to 4 unit investment property: commonly 25% down (sometimes more), because multi-unit rentals can be viewed as higher risk.

- Jumbo investment property: frequently 20% to 30% down, depending on loan size, reserves, and overall risk.

- DSCR and other investor-focused products: down payment requirements often cluster around 20% to 25%, but may move based on DSCR, property type, and credit.

A few practical notes:

- Gift funds: Some investment loan programs limit or restrict gift funds. Plan for your down payment to come primarily from your own assets unless your lender confirms otherwise.

- Closing costs still apply: Even with a large down payment, you should budget for typical closing costs and prepaid items (insurance, taxes, interest).

- Reserves are separate: Don’t assume your down payment “covers” reserves. Many programs require both.

Investment property loan rates: why they’re higher and what changes them

Investment property rates are typically higher than primary-residence rates because default risk is historically higher on non-owner-occupied homes. The gap varies by market conditions and borrower profile, but the direction is consistent.

Key factors that move your rate and pricing:

1) Down payment (LTV)

More money down usually improves pricing because the lender’s risk is lower.

2) Credit score and overall credit depth

Higher scores, clean mortgage history, and strong tradeline history can help.

3) Property type

Condos, 2 to 4 units, and unique properties may price differently than a single-family home.

4) Rental income strength and documentation

A strong lease and a solid market rent conclusion can support the file. DSCR programs will weigh property cash flow even more.

5) Points, lender credits, and APR

Two offers can have the same interest rate but different costs. When comparing, ask for a clear explanation of:

- The interest rate

- Whether points are included

- The APR (which reflects certain costs over the life of the loan)

- Total cash to close

For a deep dive on reading Loan Estimates, the CFPB’s Loan Estimate explainer is a reliable reference.

How lenders calculate rental income when you’re qualifying

One of the most misunderstood parts of investment property loans is how rental income is counted.

In many conventional scenarios, the lender may use:

- An executed lease (if available)

- Market rent from the appraisal (often via a rental schedule)

- A vacancy factor (to be conservative)

- Your tax returns (Schedule E) if you already own rentals

What this means in practice: even if your tenant will pay $2,500/month, the lender may not count the full $2,500 when calculating your DTI.

If you’re buying a property that already has tenants, documentation quality matters. If you’re buying a vacant property to rent, the appraisal’s market rent conclusion can be crucial.

Documents you’ll typically need for an investment property mortgage

Exact requirements vary, but most borrowers should plan for:

- Income documentation (W-2s, pay stubs, or tax returns depending on your situation)

- Asset statements (checking, savings, brokerage, retirement where allowed)

- Current mortgage statements and insurance info for properties you own

- Signed lease agreements (if applicable)

- Entity documents (if buying in an LLC and the program allows it)

- A clear explanation of large deposits or credit events if they exist

A smoother file is usually about two things: clarity (clean, complete docs) and consistency (your story matches your paperwork).

Ways to improve approval odds (and potentially get better pricing)

Small changes can make a big difference in investor lending. Consider these levers before you apply:

- Increase down payment if you’re close to a pricing tier (for example, moving from 15% down to 20% down).

- Strengthen reserves by keeping liquidity available through closing.

- Lower DTI by paying down revolving balances or restructuring debt.

- Be conservative with property assumptions (repairs, vacancy, rent estimates).

- Get pre-approved early, especially in competitive markets where sellers care about certainty and timelines.

Beyond the loan: don’t ignore the “execution” side of investing

Financing is one piece of a profitable rental. Your returns also depend on how quickly you can lease, how well you screen tenants, and how effectively you market vacancies.

If you’re building a small investing operation (even a single-property LLC), it can be worth getting professional help on your online presence and lead flow. A boutique team like WRM Design’s digital marketing services can support strategy, SEO, and conversion-focused web experiences that help local renters find you faster.

How New Era Lending can help you compare investor loan scenarios

Investment property loans are rarely one-size-fits-all. The “best” option is the one that aligns with your cash to close, expected hold period, and risk tolerance.

New Era Lending helps borrowers explore purchase, refinance, and equity-access strategies with a process designed to be both modern and human, combining smart tools (like secure document uploads and e-signatures) with personalized guidance. If you want to run side-by-side scenarios for an investment property purchase or refinance, you can start a conversation at New Era Lending.

If you also want broader context on loan program differences, you may find this resource useful: Mortgage Loan Programs: Compare FHA, VA, Conventional and More.